Which trends offer opportunities or pose threats on the European home decoration and home textiles market?

Millennials and Gen Z are quickly becoming Europe’s main consumers and professional buyers. As a result, these generations strongly influence the home decoration and home textile (HDHT) sector and strategies. Their main reasons for buying relate to how products can improve their mental and physical wellness. Sustainability is an important part of this. These consumers want brands to help make the world a better place through social and environmental responsibility.

Contents of this page

- Sector transformation: millennials and Gen Z become the dominant consumer group

- Sustainability: social and environmental responsibility

- Wellness

- New circular business models

- Changing global supply chains

- Home sweet home

- Shared living and tiny spaces

- Playfulness

- Digitalisation in marketing and services

- Handmade under pressure

1. Sector transformation: millennials and Gen Z become the dominant consumer group

In the coming decade, the European HDHT market will increasingly focus on:

- Sustainability;

- Shorter distribution chains;

- Digitalisation in marketing and services.

However, the biggest change will be in consumers’ reasons for buying. By the 2030s, a new generation of consumers and professional buyers will be in charge: a mix of millennials and Gen Z. Their values will shape what products are produced and sold, and how.

The market will need to offer products that help these consumers satisfy their key reason for buying: improving their wellness. To put it simply: millennial and Gen Z consumers want to feel good about what they buy. They prefer offers that improve their wellbeing and provide meaningful social/environmental benefits. These topics are closely related. For example, 6 out of 10 millennials and Gen Z feel guilty about their negative environmental impact. This makes sustainability another core reason for buying.

HDHT companies must adjust

HDHT importers, retailers and brands need to move closer to these new consumers.

This has various aspects:

- In-depth market intelligence – marketers need to know what drives these consumers, how they live and work, their disposable income and their buying behaviour.

- Sustainability – businesses must actively embrace sustainable values and practices and be transparent to increase trust and loyalty amongst customers.

- Storytelling – effective storytelling creates engagement, inspires and builds loyalty amongst these consumers, who are more open to new cultures and origins and like to learn about materials and techniques.

- Communication channels – sales and marketing must be more online (social media), using consumer reviews and influencers to build trust among peers.

- Content – communication must be brief, to-the-point, visual and transparent, since these consumers demand proof.

- Co-creation – these consumers want to be involved in the design process, for example through feedback loops or brand champions/influencers.

- Convenience – businesses must offer convenience in buying (online, 24/7, delivered and easily returned) and in clever solutions for shared living and tiny spaces.

- Selling and production cycles – cycles must be shorter and less dependent on traditional ideas of seasonality, with less volume but competitive prices.

Business models are evolving

The business models that can deliver the desired wellness benefits are:

- Sustainable – value-driven concepts with social and environmental values and practices at their core;

- Connected – market intelligence, customer relationship management and active sales;

- Creative – design-led in terms of product, production, service, staff policy and marketing.

Tips:

- Become familiar with new consumer groups, for example via GWI’s reports on millennial and Gen Z consumer behaviour.

- See our study on the European demand for HDHT for relevant trade figures.

- Check the CBI’s News & Stories for the latest news in the sector. To stay updated, subscribe to our newsletter.

- For inspiration, consult the exhibitor lists of the main European HDHT trade fairs like Ambiente,Maison&Objet, Heimtextil, spoga+gafa and imm cologne.

2. Sustainability: social and environmental responsibility

Sustainability is quickly becoming part of the core consumer needs in HDHT. In Europe’s leading HDHT markets, most consumers believe that leading a sustainable lifestyle is important. For example, many consider sustainability highly or extremely important when buying home textiles. People want to consume responsibly instead of consuming less. Millennials and Gen Z want to create a better world, and more and more older generations want to help out with this as well. This will reshape the industry.

Solutions are expected to mainly come from the industry, in improving both their environmental footprint and their social responsibility. Companies are expected to take a stand. They should do as they say when it comes to the fairness of their own human resource and supplier policies.

True sustainability is a combination of:

- People: social aspects;

- Planet: environmental aspects;

- Profit: economic aspects such as affordability, marketability and productivity.

Video 1: CBI webinar on sustainability in the European HDHT market

Source: CBI

Consumers find environmental and social responsibility in HDHT important. In 2024, the most valued sustainable or ethical practices in furniture and homeware according to British consumers were:

- Producing sustainable packaging and products;

- Reducing waste in manufacturing processes;

- Committing to ethical working practices;

- Supporting the adoption of circular practices;

- The practice of and respect for human rights;

- Protecting and supporting biodiversity;

- Reducing carbon emissions;

- Conserving water and other natural resources;

- Adopting diversity and inclusion practices;

- Providing reliable data on carbon emissions.

Aside from being better for people and the planet, consumers often think sustainable home furnishings are better quality. This idea of durability further adds to the appeal of sustainable products.

The European Green Deal and a circular economy

European legislation is also moving towards increased sustainability, making it a requirement rather than an option. With the adoption of the European Green Deal, the European Union (EU) strives to become climate-neutral by 2050. This will help make sustainable corporate behaviour a must.

Relevant EU sustainability legislation

The Green Deal provides a legal framework for social and environmental sustainability. It includes new and updated laws, as well as proposals. Relevant sustainability legislation for the HDHT industry includes the:

- Corporate Sustainability Due Diligence Directive;

- Forced Labour Regulation;

- Ecodesign for Sustainable Products Regulation;

- Green Claims Directive proposal;

- Textile Regulation revision proposal;

- Deforestation Regulation;

- Packaging and Packaging Waste Regulation.

Well-known sustainable initiatives (like BSCI, ETI, Sedex or WFTO) and certifications (such as FSC, GOTS or OEKO-TEX Made in Green) can help you prove your sustainable conduct.

A main building block of the Green Deal is the circular economy action plan. In a circular economy, waste is eliminated through repair, reuse and recycling.

Video 2: Repair, reuse and recycle!

Source: European Parliament

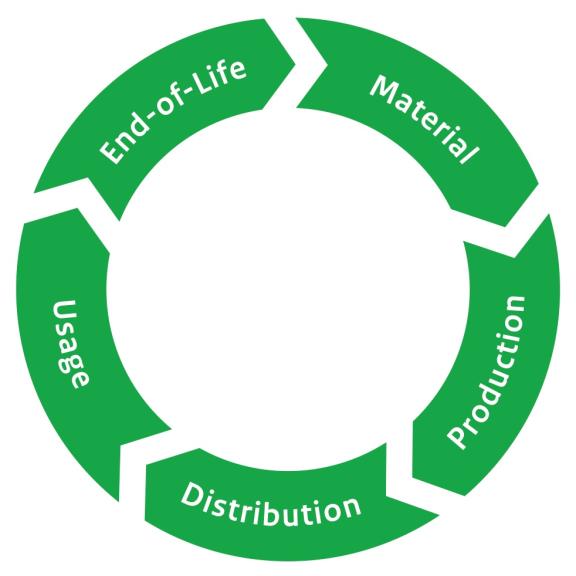

A typical product lifecycle consists of 5 stages. In a circular economy, a product’s end of life starts a new cycle. Waste no longer ends up in landfills, but is used to create a new material.

Figure 1: A circular product lifecycle

Source: CBI Sustainable Design Training

You can introduce (more) environmentally friendly and socially responsible practices in each stage. As a producer, you have the most control over the first 3 stages: material, production and distribution.

Table 1: Examples of sustainable practices per stage of the product lifecycle

| Environmentally friendly practices | Socially responsible practices | |

|---|---|---|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Estimates show that over 80% of a product’s environmental impact is determined during the design phase. This means you have an important role to play in the process.

One example of a manufacturer that employs both socially and environmentally responsible practices is Ashoka Exports. This Indian company offers a variety of jute and cotton bags, including shoppers, laptop bags and pouches for bathroom accessories. To achieve their mission of ‘Greening Growth Globally’, they use verifiable and transparent social and environmental compliance measures, including Sedex’s social audit SMETA, GOTS (organic cotton) and GRS (recycled cotton). Ashoka also provides medical insurance to its employees and consistently invests in development projects for the community.

A related trend is material innovation, which can be divided into 3 categories:

- Recycling post-industrial or pre-/post-consumer waste;

- Engineering ‘from the lab’;

- Applying agricultural side products or excess harvests.

Video 3: CBI webinar on sustainable innovations

Source: CBI

Another frontrunner is Malai. Malai has developed a durable and compostable vegan bio-composite material. The material is made from organic and sustainable bacterial cellulose grown on agricultural waste from the coconut industry. The company works alongside Southern India’s coconut farmers and processing units. Their ‘waste’ coconut water would normally be released into the drainage system and cause pollution. Malai rescues this coconut water and uses it to create a flexible material that works as faux leather for bags, and home and fashion textiles.

Video 4: Circular coconut waste-based material

Source: Malai

Forecast

Millennials and Gen Z try to influence things through their buying behaviour. They want to buy from companies that chelp make the world a better place. For example, 55% of British adults say it is important that their HDHT products are made sustainably (up to 60% of those aged 25–34). They are willing to pay 15% more for this (up to 21% for those aged 25–34).

At the same time, higher prices can be a barrier. An international survey showed that 50% of consumers are not sure whether they would pay a premium price for sustainable products in times of inflation. For example, most consumers in leading European markets are prepared to spend more on sustainable home textiles. However, 49% are less able to afford sustainable products due to price increases.

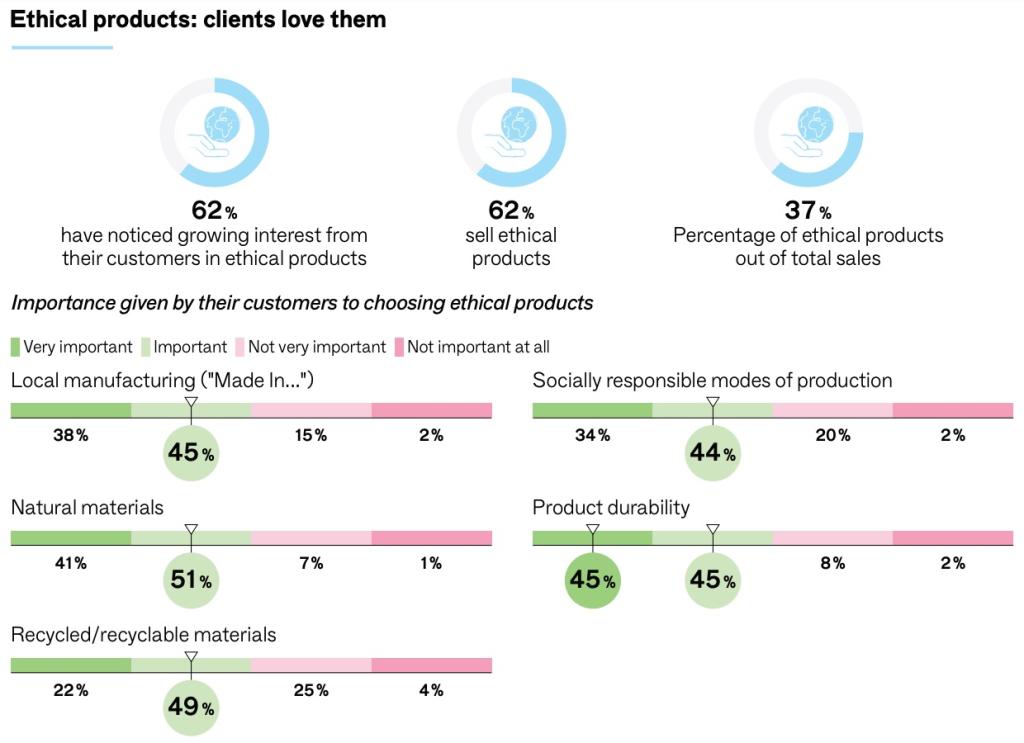

Sustainability is a central and integrated part of millennials’ and Gen Z’s wellness needs. As these generations become the dominant consumers and professional buyers, this trend is likely to continue to grow. In all sectors, sustainability is now one of corporate buyers’ top 3 purchasing criteria. 36% of companies are willing to leave suppliers that do not meet their sustainability criteria, and 57% say they will be willing to do so by 2027. The growing importance of sustainability in HDHT is reflected in a Maison&Objet survey from 2021.

Figure 2: Popularity of ethical products among clients of HDHT retailers

Source: Maison&Objet Barometer – Issue 1

Opportunities

- Recycling/upcycling materials from local consumption/production can be an opportunity. Waste or offcut materials from the industry are often readily available and relatively cheap.

- Consumers are interested in the story of your value chain. Not just to make sure that materials are really recycled, but because consumers appreciate knowing that an item used to be part of something else.

- Using your cultural heritage to introduce new patterns and colours to buyers and consumers makes your products unique. You can mix these designs with cultural elements.

- Being well-prepared for the new legislation can give you a competitive advantage.

- Social/environmental certification can add value and credibility to your concept.

- Positive gender values can make you stand out.

Threats

- Sustainable products do not automatically sell for higher prices. Price is mainly influenced by design value, quality and finish.

- Western brands are also creating concepts based on recycling/upcycling. This means that design expectations are quite high, and that you will also be competing with European designers.

- You must be able to support any sustainable claims you make, preferably with certifications. Many buyers already require this, and the proposed Green Claims Directive could make it mandatory.

- Taking a stand on political or social issues creates a following, but you also risk losing some customers. Non-confrontational communication is important.

- In the long term, buying local (‘Made in Europe’) to reduce environmental impact could become a threat to you.

Tips:

- Actively promote your products’ environmental and social sustainability. Use your website, social media and trade fair participation to tell your story.

- Take advantage of low-cost waste materials for recycling/upcycling. Negotiate well with suppliers and explain the benefits of you taking their waste (for free). Set up an effective supply chain to collect and process the materials.

- Study good practices of innovators like La Termoplastic F.B.M. cookware and Kinta’s fair-trade home accessories, as well as positive gender values like IKEA’s handwoven rugs.

- For more information on sustainability, see our study on sustainability in HDHT, our tips for going green and becoming socially responsible, and our webinars on sustainability in the European HDHT market and sustainable innovations for your HDHT business. Our study on buyer requirements provides more information about legislation, sustainability initiatives and certifications.

3. Wellness

The search for health and happiness has become an important focus. Many people, especially younger generations, live under stress from peer pressure on social media and struggle to find homes. The climate crisis is a major concern. To improve their mental and physical wellness, a key question is: ‘How can I buy better to feel better about myself?’

This includes:

- Feeling more connected to others;

- Improving one’s knowledge and skills;

- Living a more active, healthier lifestyle, closer to nature;

- Becoming more creative.

Products that help achieve these goals will appeal to millennials and Gen Z. For them, climate change is more personal than for their parents’ generations. As such, sustainability has become a core personal wellness issue. This makes it a stronger reason for buying for these generations than for any before. They want products with social and environmental benefits, so they feel good about their purchase.

For 73% of consumers in an international survey, wellness is an essential element of any brand's strategy. 89% of people did more to improve their wellbeing in 2024 than in 2023. In 2024, fragrance and wellness products were some of HDHT retailers’ best-performing product categories.

The home is closely connected to mental wellness. In an IKEA survey, 40% of respondents who felt more positive about their home also saw a positive impact on their mental health. Many associate clean, decluttered spaces with a greater sense of calmness. In fact, decluttering can reduce stress and make people feel happier, less anxious and more confident. According to the IKEA survey, sleeping and relaxing (for example by reading under a warm blanket) are the most important activities for achieving a sense of wellbeing at home.

Video 5: Ethically produced bed textiles of tencel and linen

Source: URBANARA

This focus on wellness translates into several important HDHT market trends:

- Wellness categories (like yoga, spa, leisure and the garden) will be in demand;

- Social and environmental values are part of the primary wellness values;

- Marketing communication should highlight specific wellness benefits and take a stand on important social and environmental issues but in a gentle tone of voice;

- Storytelling will focus on stories that allow consumers to learn about new (sustainable) materials, techniques, processes and cultures;

- Design trends will attempt to be ‘bio-centric’ (with full consideration for the planet), for example through natural dyes and timeless designs;

- Convenience through digitalisation of the shopping journey.

A good example of a company that has embraced sustainable and ethical practices is CRC. This WFTO guaranteed company offers a range of home accessories and gifts in various materials, including textiles, ceramics and paperware. They strive to ‘impact the lives of artisans in as many ways as possible’ and create self-sufficiency among artisan groups. CRC’s storytelling focuses on its impact, including saving the environment, breaking social barriers, empowering women and promoting urban employment.

Forecast

Wellness will continue to be the main trend in HDHT for the coming decade. In 2024, mood boosting and wellbeing were the main reasons for British consumers to redecorate. All developments described above will start, continue, grow stronger, and need a more central place in the business practices of both European companies and their suppliers.

Opportunities

This trend offers opportunities for products/product groups that:

- Are related to the various aspects of wellness, like spa and yoga items (soap, hammam towels), candles, garden furniture, easy chairs, bed textiles and travel accessories;

- Include natural raw materials or colours;

- Are related to leisure, hobbies, sports, toys and games;

- Appeal to the new ‘young old’ consumer;

- Offer attractive stories;

- Are sustainable and transparent.

Threats

- Sustainability has become a personal issue directly linked to consumers’ wellbeing, especially for younger generations. Products without clear social/environmental benefits may be ignored.

Video 6: CBI webinar on wellness in HDHT

Source: CBI

Tips:

- Follow discussions around this key trend through the Global Wellness Institute or research institutes like McKinsey.

- Communicate your products’ specific wellness benefits.

- Collaborate to offer one-stop shopping. For example, if you offer soap you can cooperate with fellow producers to offer a coherent bathroom collection including textiles and accessories.

- Study good practices, like Madat’s fair-trade items for spa/yoga practices or Comme Avant’s handmade organic zero-waste soaps and sustainable clothing/linen.

4. New circular business models

With their commitment to sustainability, millennials and Gen Z also introduce values like ‘sharing over possessing’. These topics are key drivers of new circular business models that extend the lifecycle of HDHT products. Full circularity is generally not yet possible for small and medium-sized enterprises (SMEs) in developing countries. But there is much innovation in the industry. Recycling, upcycling and experimenting with alternative materials are popular options that you can participate in.

Another way to extend the lifecycle of HDHT products is through retail concepts like sharing, leasing, buy-backs and reselling. These business models minimise environmental impact by keeping products in use for as long as possible. They also provide flexibility and make products available to consumers with smaller budgets. Second-hand furniture is a well-established market in many European countries. Strong growth is expected.

Source: YouGov

The combination of sustainability and affordability makes these concepts especially popular among millennials and Gen Z. These environmentally conscious generations value sharing over owning. They generally have less disposable income than older consumers. The flexibility of these concepts also makes it easier for them to adapt to life events like moving house (often rental) and starting a family.

An example of a company rolling out such new business models is IKEA. The company aims to make its product range 100% circular by 2030. It focuses on products that can be repaired and reused before being recycled or remanufactured. Besides offering spare parts and publishing disassembly instructions, IKEA has launched buy-back (and reselling) programmes. It has also been piloting leasing/rental concepts.

Video 7: Why the future of furniture is circular

Source: IKEA

Besides large retail chains experimenting with circular business models, companies are emerging with circularity as their core business model. For example, Selency and Whoppah are popular online marketplaces where European consumers can buy used home furnishings.

Forecast

With the growing influence of millennials and Gen Z, the popularity of circular business models is expected to rise. In a 2019 study among customers of German interior design shop Connox, the most common reason for never having rented furniture before was not having thought of it (PDF in German). This supports a 2018 study by the European Commission, suggesting that increasing consumer awareness of second-hand, renting/leasing and repair markets enhances engagement in the circular economy.

As circular concepts become more common, consumer awareness increases. In 2023, HDHT professionals reported a growing demand for circular products:

- 80% noted a growing demand for recycled products;

- 72% for upcycled products;

- 63% for pre-owned items.

In 2023, most HDHT retailers offered upcycled products and products made with recycled materials. Nearly half of them sold second-hand products. 64% of HDHT retailers thought it will be essential to offer second-hand/pre-owned products in the future, compared to 41% in 2021.

Opportunities

- Using pre-/post-consumer and post-industrial waste can reduce material costs.

- Circular business models can open up new markets.

- Teaming up with distributors to create buy-back/reselling and refurbishment programmes facilitates longer-term buyer loyalty.

- Recycled/vintage materials allow you to create a luxury positioning based on a ‘limited edition’ concept.

Threats

- Recycled materials may run out. This could force you to phase out popular product lines.

- Using recycled materials may create concerns about the precise material content and the relevant legal requirements. New sustainability legislation may pose a challenge especially if the materials’ origins are not traceable.

- ‘Big Business’ usually has more control over the product lifecycle. For SMEs, it can be difficult to compete.

- Concepts like refurbishment and reselling may decrease the need for new production.

Tips:

- To facilitate a long product lifecycle, take circularity into account when designing your products. For example, designs should allow for easy replacement of parts, and materials should be durable (preferably recyclable). An interesting example is Occony’s circular Peak Chair, made of recyclable waste materials.

- For inspiration and more information on how to design products for new business models, see for example IKEA’s Circular Product Design Guide.

5. Changing global supply chains

In marketing, distribution channels are becoming shorter. For example through manufacturers selling straight to retail. Physical distribution is concerned with the logistical supply chains of materials and semi-/end-products. Here, different forces make supply chains more complex, and sometimes longer.

Global supply chains have been under pressure. European importers have realised that political shocks can severely disrupt distribution and markets. Governments have imposed bans and tariffs, and consumers want to know where products come from.

Importers have been trying to make their supply chains less vulnerable, through:

- Second sourcing – contracting multiple suppliers for the same (or a similar) product;

- Vertical integration – taking more control over their supply chain by building the capacity of their existing suppliers, or actually taking over suppliers;

- Pre-stocking – building inventory which can be sold in case of new disruptions, often asking manufacturers to keep such (unpaid) stocks;

- Reshoring – contracting European manufacturers to produce (part of) an existing collection that was previously imported;

- Longer lifecycles – extending product lifecycles.

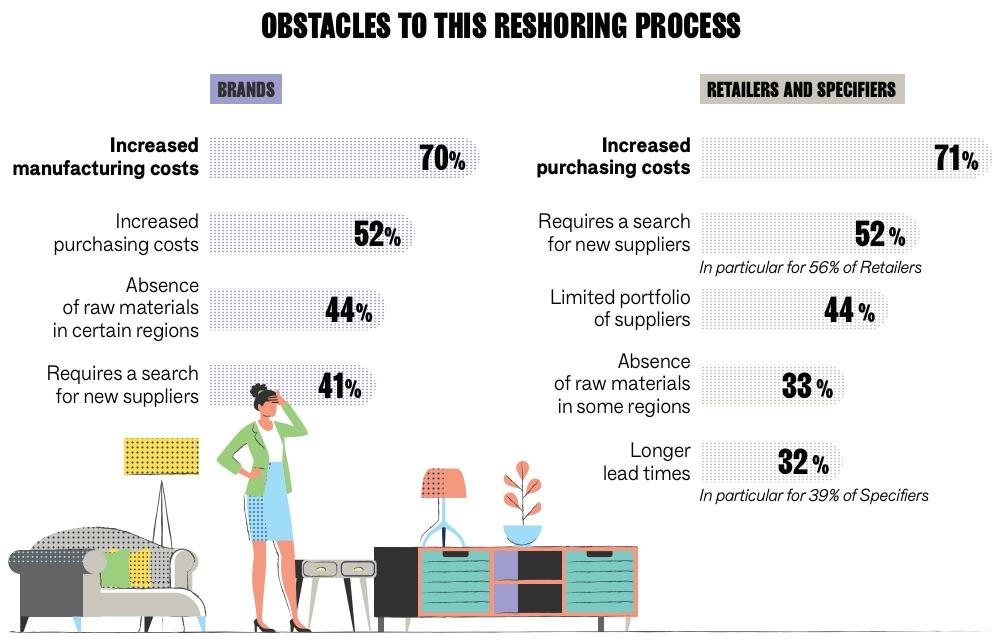

According to McKinsey, value chains shifting away from their current top producers (like in second sourcing) could present a real opportunity for some developing economies in the HDHT sector. Reshoring may be a hot topic, but it is not that easy in practice. Redesigning supply chains takes time, and effects may not be visible in the short term. Also, the value for money of reshored HDHT products often disappoints. 5 years after the start of the Covid-19 pandemic, only a few dozen European companies across sectors have reshored some of their production.

French bag brand CABAIA explains that domestic production is not feasible because there is no production capacity, and they would have to increase their prices 12 times to be profitable. Instead, this B Corporation manufactures its products in Poland, Türkiye and China. Their factories are BSCI and/or SMETA audited to ensure ethical compliance and optimal working conditions.

Figure 4: Obstacles to reshoring HDHT

Source: Maison&Objet Barometer – Issue 4

The changes in supply chains create a more secure distribution system to Western Europe. But they also make the supply chain more fragmented, less efficient and more costly. These costs will be passed on to companies and consumers. For example, if Western importers second-source end-products from Southeast Asia but manufacturers there still source components from China, the supply chain becomes more tangled, less transparent and possibly more costly.

Forecast

Governments will increase their direct involvement in trade through tariffs and by facilitating sourcing closer to home. Their aim is to increase security in the delivery of goods and improve sustainability in distribution chains.

At the same time, increased US-China trade tariffs could indirectly affect the European market and your opportunities too. Chinese producers may redirect their exports towards Europe at lower prices (‘dumping’). This could lead to more competition, especially at the lower ends of the market. To protect the EU internal market from harmful imports, a new import surveillance task force will monitor import trends. The European Commission can use the EU’s trade defence toolbox, including anti-dumping measures.

Consumers will become used to longer lead times, higher prices and items not always being available. They may favour quality over quantity when buying products (timeless rather than trendy), learn to like a product longer, and/or share and exchange items with others. Younger generations in particular will ask more questions about product origins and whether these align with their values.

Opportunities

- Importers will look for second sources – especially in East Asia – to become less dependent on single sources.

- This may also lead to a more favourable financial context for East Asian exporters, including government subsidies and improved terms for working and investment capital from banks.

- Businesses with verifiable sustainable practices have a competitive advantage.

- Focus on design, craftsmanship, sustainability and storytelling to add value and avoid competing with low-end mass-produced items.

Threats

- East Asia’s dependence on China for inputs may limit its bargaining position.

- Some production may be re-shored to European suppliers.

- Chinese direct investment may replace the original ownership of East-Asian manufacturers and exporters.

- Chinese dumping practices may lead to more competition at the lower ends of the market.

Tips:

- Be a preferred partner for importers looking for second-sourcing opportunities. Key factors are production capacity, value for money, excellent communication and social/environmental compliance.

- Improve your linkages to important stakeholder groups like financial institutions, material suppliers, government bodies and labour pools.

- Be unique in your materials and techniques to avoid being replaced.

- Tell the stories of your production and artisans to add value.

6. Home sweet home

In times of disruption, consumers appreciate the comfort and safety of their home, family and friends. This means a revival of ‘cocooning’. The ‘home sweet home’ trend involves people (across generations) enjoying each other’s company, entertaining, cooking and dining, or simply relaxing. This relates to items that create a cosy atmosphere, as well as cookware and dinnerware for ‘slow dining’. In a 2025 Maison&Objet Barometer, kitchen and gourmet products remained as some of the best-performing categories in HDHT.

This trend also involves disconnecting from the troublesome outside world. For older consumers with a relatively high disposable income, the home forms a retreat. It is a place of luxury, with high-quality furniture and decoration, often in nostalgic styles. Popular materials include comfortable, heavy textiles, dark wood, and metal. Patterns are bold and colours are cosy and warm, including darker rich reds and purples, sophisticated blues and browns.

Video 8: Retro revival

Source: John Lewis

The way consumers decorate their home reflects their personality. In this context, both consumers and buyers appreciate good storytelling that evokes an emotional connection. The story behind your product and company can highlight key aspects like your environmentally and socially responsible values and activities. As European consumers travel to more distant places, they are discovering new stories.

When products are handmade from sustainable materials, this further adds to their sustainable concept. HDHT products can reflect their origins in their materials, techniques and meanings. They can have cultural stories to tell, especially in the fair-trade segment. These products can also tell the story of the importance of meaningful work and income in developing countries – especially for women. This has kept many interesting artisan skills alive.

Forecast

As millennials and Gen Z start new families, cocooning will become a mainstream lifestyle trend. Spending time with friends and family is the main stress reliever for European consumers, who say it brings them a lot of pleasure.

In addition, one of the things that makes many consumers feel most content is cooking or eating homemade meals. The cost-of-living crisis has led 44% to plan to cook more at home. Luxury retro styles need to attract younger affluent consumers to stay relevant.

Opportunities

- The luxury aspect of this trend may offer good margins.

- The luxurious ‘home sweet home’ style is based on supreme craftsmanship and a stable colour palette.

- Interior decorators carrying this style are found at all major European HDHT trade fairs.

- The cocooning aspect has growth potential and will move along with the preferences of younger generations.

- Cocooning is particularly promising for specialists in home textiles, home accessories, Christmas items and cooking/dining.

Threats

- The luxury trend is fading. Margins may be good, but volumes relatively small and turnaround low.

- The cocooning trend will become mainstream and mid-market, attracting high-volume/low-cost suppliers.

Tips:

- Study the history of interior design, using luxury home magazines, like Architectural Digest and Coveted.

- Follow terms like 'hygge' (Danish) and 'lagom' (Swedish). These translations of the cocooning style indicate this is an international trend, with a strong presence in Scandinavian design.

- Study good practices. For example, Versmissen’s products create ambience for the wealthy consumer.

- Check Maison&Objet and Ambiente for relevant distributors.

7. Shared living and tiny spaces

About 55% of the world’s population lives in urban areas, and the UN expects 68% by 2050. Europe will mainly be home to small- to medium-sized cities, growing at twice the rate of megacities. This will create pressure on urban space and raise housing prices. As a result, consumers are adjusting to tiny urban properties. They are adopting new forms of shared living more and more, often with multiple generations together. Homes are adapted to or designed with shared and private spaces. This creates new directions in HDHT.

In their private spaces, consumers like to display their personal style. Values related to differentiation, eclecticism, personal taste and style are important. These are mainly associated with mid-high/premium markets. Items for tiny/shared living spaces must be more flexible, convenient and multipurpose. Such values are found primarily in the mid-/lower-end market.

To improve their wellbeing, consumers in small urban spaces are creating a closeness to nature through flowers and plants. In 2023, 74% of specifiers reported an increasing demand for green outdoor spaces and/or terraces in residential projects. Tiny balcony gardens are trendy, offering clever seating and gardening solutions. Urban consumers are also increasingly working from home. This further adds to the required multifunctionality and flexibility of their living space.

Video 9: Adjustable desk

Source: OAKO Denmark

Forecast

As urbanisation grows and hybrid working becomes the norm, urban consumers will be looking for suitable solutions. For example, increasing functional space was a common reason for British consumers to redecorate in 2024.

Obra Cebuana is a Filipino manufacturer of furniture and home accessories. Their collection of expressive stools combines the styles and craftsmanship of Visayan culture with the country’s abundant natural resources. The Porcupine Stool uses a rattan folding technique resembling origami. The Aloha Stool combines fibreglass with laminated rattan slats. The Pouf Stool consists of rattan strips with a colourful wash. These designs prove that tiny living does not mean furniture has to be boring.

Opportunities

This trend offers opportunities for products/product groups that:

- Can be used around the house, like occasional furniture;

- Are lightweight, collapsible, flat-pack and easily stored;

- Are multipurpose;

- Feature flexible components or several style options.

Because shared living creates demand for both volume (shared spaces) and value (private spaces), there are opportunities across the market.

Threats

- Products with values related to convenience and functionality are often price-sensitive. This means you can expect price pressure and high-volume requirements.

Tips:

- Create clever solutions for tiny spaces. Offer (multifunctional/modular) products that allow folding, nesting, flat-packing, stacking, et cetera.

- For shared living, either control your costs and improve productivity for the shared decoration segment or develop high-level design for private quarters.

- For more information on market segmentation, see our study on market channels and segments.

- Study good practices of players like IKEA and Habitat. They offer collections based on functional design for large segments of lower-middle and middle markets. For the higher-end, look at distributors with identity-driven product ranges like Iittala and Le Jacquard Français.

- Use sources like home magazines, industry portals, trade fairs and our market intelligence to stay informed about urban consumers. Megatrend analyses like 2030: the mega-trends and Megatrends for 2020-2030 describe how they influence work and living.

8. Playfulness

Playing is essential. It strongly connects to 3 human priorities: a stress-free and happy life, (children’s) self-love and advocacy, and connection and family togetherness. As such, playing is closely related to happiness and mental wellness. People play to have fun and fulfil their need for optimism, escape and invention. It stimulates social connection, reducing loneliness and isolation and providing a distraction from worries. Because of this, consumers welcome new opportunities and concepts to imagine, escape, explore, create and connect.

Playfulness at HDHT product level has various expressions, including:

- Bold colours, shapes or patterns – like Jonathan Adler’s style;

- Functional items that are figurative as if to play with – like Alessi kitchenware;

- Modular items that let consumers ‘construct their own product’ – like HAY’s kaleido trays;

- Items that use cultural styles in a surprising way – like Kitsch Kitchen’s style;

- Items that look badly made or damaged – like MAARTEN BAAS’s Clay chair;

- Items that use ‘dark’ or surreal humour – like those by Ibride.

Video 10: Rearrangeable fabric vases made with traditional hat-making techniques

Source: MOBJE

Forecast

The younger generations are playful and creative, and will push this trend further. The combination of play as an essential human need and the current crises makes this an enduring trend.

Opportunities

- This trend represents an expressive style in all segments and has a deep permanent link to European consumers’ tastes.

- It encourages consumers to practise playful interaction and co-creation through flexible and customisable concepts. Creativity is deeply connected to wellness.

Threats

- Humour and light-heartedness can come across as inauthentic when they are adopted just to be trendy.

- What is considered funny is personal and/or cultural. Your humour may appeal only to specific niches.

Tips:

- Give your cultural patterns a (respectful) twist for a playful effect.

- Use modularity to let consumers ‘create’ from the components.

- Imagine you are a child when designing for this trend.

- Develop collections that are both playful and sustainable. Sustainability can be quite serious in style (natural, spiritual), but it does not have to be.

- Study good practices of brands with a playful style.

- If you offer games or toys, consider expanding into playthings for outdoor areas.

9. Digitalisation in marketing and services

Digital technology is becoming more important in every aspect of our lives. The pandemic has accelerated this. In 2024, 19% of EU consumers ordered furniture, home accessories and garden products online (in the 3 months preceding the survey), up from 15% in 2023. This varied from up to 10% in mainly Eastern European countries to about 30% in countries such as Denmark and the Netherlands.

Consumers generally prefer to buy from brands with both an online and a physical presence, so that they can gather information and inspiration online and in person. Online is considered ‘better’ than offline across many criteria, including variety, reviews, price, comparison of brands and products and – perhaps surprisingly – fun. Online is inferior in only 2 aspects: the ability to try the right product and get advice from staff. This is why shoppers still visit physical shops: to try that chair or feel that cushion.

E-commerce

Selling directly to European consumers through your own website can be complicated and costly. You are responsible for factors like aftersales and consumer payment systems. This is not realistic for most exporters from developing countries. In addition, the General Product Safety Regulation requires you to have an ‘economic operator’ in the EU who is responsible for product safety. Supplying to a European wholesaler or retailer with a strong online presence is more feasible.

Online channels can also help consumers (and professional buyers) find out where products come from and how they are made. The HDHT sector has digital solutions specifically for those looking for sustainable options. For example, consumer platform Avocadostore brings together sustainable fashion and home items. Sourcing platform Linking Maker & Market showcases SMEs from CBI programmes. Ambiente’s Ethical Style Guide lists sustainable trade-fair participants.

Important European HDHT trade fairs have now become hybrid, hosting permanent online business-to-business (B2B) marketplaces. Examples are Maison&Objet’s MOM and Messe Frankfurt’s affiliated nmedia.hub. These allow for convenient B2B sourcing and one-stop-shopping. Other relevant marketplaces include Faire and Fairling.

Digital innovations

Digital innovation is moving fast. Important areas in HDHT include:

- Product visualisation – Augmented Reality (AR) and 3D technology;

- Generative Artificial Intelligence (AI) – for activities like communication and marketing;

- Design – digital options like digital printing, 3D printing and digital sample development;

- Blockchain technology – tracking orders/transactions, monitoring supply chains, facilitating traceability, preventing counterfeiting, and creating digital product passports;

- Smart products – ranging from remote-controlled curtains/lighting to built-in phone chargers.

Forecast

Millennials and Gen Z are already online-focused, and consumers in general are increasingly comfortable with digital technology. 58% of all shopping worldwide is online. This is predicted to reach 64% in the coming decade. Growth is driven by working from home, as 65% of consumers report shopping online more as a result.

Digitalisation and digital technology will become more relevant for exporters from developing countries, in areas like marketing, communication, sustainability and production. The new Ecodesign for Sustainable Products Regulation introduces digital product passports, and the Regulation on Deforestation-free Products requires geolocation data of the production area. The home is also becoming ‘smart’, playing into the consumer’s need for convenience. IKEA is a frontrunner in this.

Opportunities

- Online marketplaces can be a cost-effective way to achieve global distribution.

- Exporters gaining experience with e-commerce in export markets can exploit this in their domestic markets and create effective online concepts, and vice versa.

- AI can be useful in creating marketing campaigns, especially across language barriers.

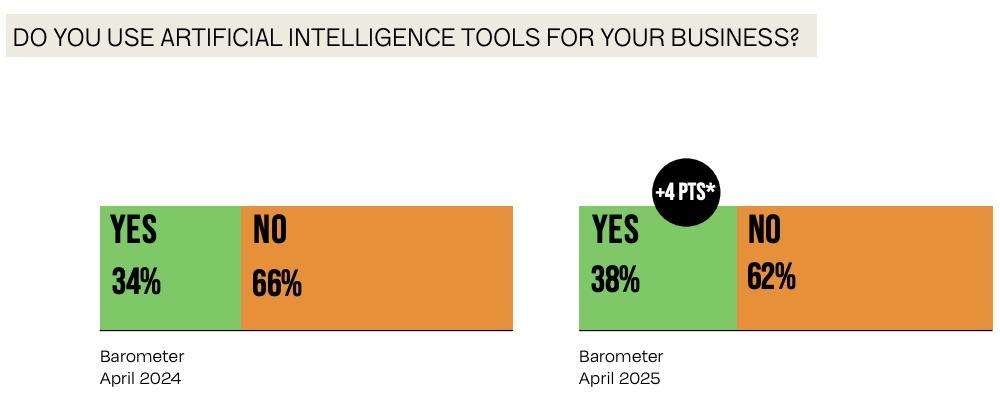

Figure 5: The use of AI for business among HDHT professionals

Source: Maison&Objet Barometer – Issue 10

Threats

- Digitalisation generally speeds up communication and service delivery, as well as expectations concerning response time.

- In online shopping, price is a leading reason for buying. Price competition is expected to grow.

- There is much discussion around digitalisation and mental health, which may create a countertrend.

- AI could help with basic communication but cannot replace your authentic tone of voice and story.

Tips:

- Embrace digitalisation where you can, starting with online marketplaces.

- Increase your online visibility with an attractive website and social media. For more information on this and digital B2B platforms, see our tips for finding buyers.

- Ensure that relevant staff is computer-literate and well-versed in social media and websites. Invest in training in these areas and in copywriting/photography skills.

- See our special study about alternative distribution channels for more information on international business-to-consumer (B2C) e-commerce.

- For more information on digitalisation in HDHT, see our tips for going digital.

10. Handmade under pressure

HDHT product prices heavily depend on the cost and availability of raw materials, energy and transport. Occasional cost increases are not usually passed on to the consumer, but put pressure on margins. However, current disruptions have resulted in longer-term cost increases. This has forced many HDHT businesses to raise prices. At the same time, the cost-of-living crisis has made consumers hesitant to spend.

The combination of high prices and low consumer confidence may lead consumers to trade down towards the lower segments. This may lead to a race to the bottom, with increasing price competition. It may also put the handmade segments in the mid-high and premium markets under pressure, in a potential countertrend scenario.

Forecast

HDHT retailers order conservatively. They order similar items from familiar wholesalers to avoid risk. In the next couple of years, the retail landscape is expected to consolidate in favour of retail chains and towards lower price segments.

One possible negative scenario would be consumers buying more affordable mass/industrially produced HDHT products. This would lead to fewer handmade products being introduced into the market. As a result of more limited availability, consumers would no longer ‘understand’ how products are made. This could lead to less appreciation for handmade craftsmanship and a less prominent role for producers. This, in turn, could lead to a lower value perception and less consumer engagement with the handmade segments in the mid-high/premium markets.

The first signals of this are coming from the home textiles market. Here both professional buyers and consumers are less aware of and focused on the beauty of handwoven and hand-dyed products. Price premiums for handmade are already small. This may become a new reality in HDHT unless storytelling urgently becomes a priority. Consumers’ desire to increase their skills and knowledge is a key aspect of improving their wellbeing, which offers opportunities amongst millennials and Gen Z. They are very open to ‘making’ and ‘maker’ stories.

Opportunities

- Lean and cost-effective exporters who can supply large volumes for the mid-/lower-end markets should focus on larger importers, catering to large networks of retailers. They have the continued buying power and trust among retailers to help them sustain their business.

- Smaller exporters can sell directly to small and individual retailers. This may require keeping stock in Europe and using fulfilment services.

- Consumers will always celebrate and give gifts. This area in HDHT is stable and relatively unaffected by economic hardship.

- Connecting or reconnecting with the domestic market may make sense.

Threats

- Professional buyers and consumers may become less aware and appreciative of the added value of handmade products if their focus shifts towards the lower-end market.

- Eastern European countries are strong competitors – especially in the mid-/lower-end markets.

- European consumers are focusing on experiences like travel, which may affect HDHT sales.

Tips:

- Tell the story behind your product and company to educate consumers and buyers about the added value of handmade products.

- Be authentic through special materials, high-level craftsmanship and sustainability. This makes you stand out in a market that may be price-sensitive but still values quality, beauty, storytelling and social and environmental responsibility.

- Connect with colleagues for joint export-marketing approaches, to offer both volume and broader collections. Joint investments in marketplaces, design innovation, and promotion could help you create one-stop-shopping concepts for larger importers, bring stock into Europe and reduce the cost of doing so.

- Combine shipments with other exporters to lower transport costs.

Globally Cool carried out this study in partnership with GO! GoodOpportunity and Remco Kemper on behalf of CBI.

Please review our market information disclaimer.

Search

Enter search terms to find market research