What is the demand for home decoration and home textiles in the European market?

The European market for home decoration and home textiles (HDHT) peaked in 2022. This is after a bounce back from an import dip due to international trade disruptions. However, increased prices and low consumer confidence pose a challenge. Many imports come directly from developing countries. Because European importers often re-export products, you should focus on segments rather than countries. The mid to high-end markets are particularly suitable. If you can meet the need for sustainability and add unique value, there is potential across the sector.

Contents of this page

1. What makes Europe an interesting market for home decoration and home textiles?

European HDHT imports peaked in 2022, following strong recovery from previous trade disruptions. Consumers’ renewed focus on the home and garden is expected to keep driving demand, with sustainability becoming more and more important. At the same time, relatively high prices and low consumer confidence make consumers less eager to spend. Developing countries play a key role in the market. The mid- to high-end segments offer opportunities and allow you to avoid competing with mass production from countries like China in the low-end segment.

European imports peaked in 2022

Marketing and services for the European HDHT market generally take place within Europe. However, a lot of production takes place in lower-cost (developing) countries outside of Europe.

Source: UN Comtrade, 2025

Europe’s HDHT imports grew from €146 billion in 2020 to €169 billion in 2024, at an average Compound Annual Growth Rate (CAGR) of 3.7%. This included relatively low imports in 2020 due to the Covid-19 pandemic, after which imports bounced back with 20% growth in 2021. This large increase was most likely due to delayed shipments from 2020. Modest growth followed in 2022, before imports returned to values comparable to pre-pandemic levels in 2023.

The worldwide HDHT import market showed the same pattern. With a stable global market share of about 39%, Europe is a key market for HDHT products.

Similarly, Europe’s direct HDHT imports from developing countries grew from €58 billion in 2020 to €78 billion in 2024, at a CAGR of 7.7%. This translates to a market share of 46% in 2024. However, the actual market share is probably much higher because a lot of intra-European trade consists of re-exported products from developing countries. This makes Europe a particularly interesting market for you.

These overall data mainly reflect home decoration imports, which generally account for almost 90% of total European HDHT imports. However, a closer look at home textile imports reveals a different pattern.

Source: UN Comtrade, 2025

Unlike in home decoration, most of Europe’s home textile imports come directly from developing countries – about 60% on average. This translates to €12 billion worth of home textiles out of a total value of €18 billion in 2024.

Rising prices and low consumer confidence challenge the market

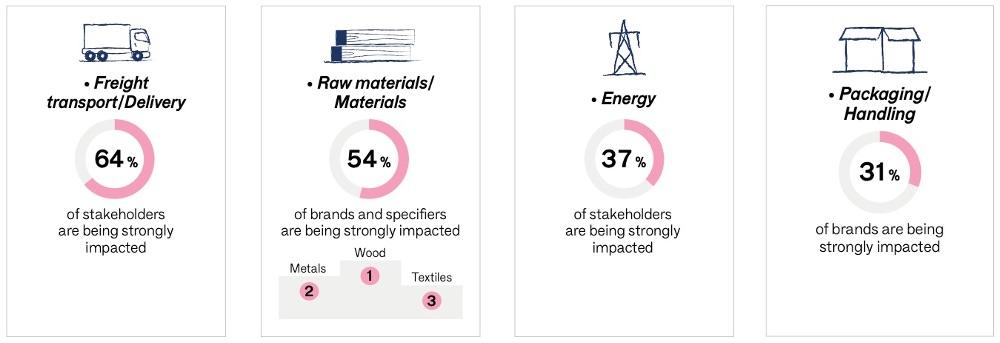

The recent changes in HDHT imports had various causes. The effects of the COVID-19 pandemic and the war in Ukraine have disrupted international trade. First, the pandemic caused costs of raw materials, energy and transport to rise. In January/February 2022, key HDHT stakeholders estimated their costs to be 19% higher compared to the year prior.

Figure 3: Impact of cost increases on HDHT companies, January–February 2022

Source: Maison&Objet Barometer – Issue 3

After that, costs rose further due to the war in Ukraine. By October 2022, 42% of the HDHT companies were strongly impacted in their business by the energy crisis. These longer-term cost increases forced HDHT companies to raise their prices. These higher prices may also deter consumers. In 2025, the rise in costs was still a challenge. As some costs came back down again, some companies responded by lowering their prices again too. However, consumer prices generally continue to be higher than before the pandemic.

Consumer spending and confidence are under pressure

The HDHT sector is sensitive to economic cycles. When economic circumstances and prospects are down, consumers postpone buying items that they do not urgently ‘need’. When economic conditions are good, purchases of such non-essential products tend to rise.

European consumer confidence fell sharply in March 2022 due to the situation in Ukraine and the resulting energy crisis. This shows a large drop in households’ expectations about the general economic situation in their country, and their own future financial situation. Consumers’ intent to make major purchases also declined. Although consumer confidence has improved since then, it remains below the long-term average. In line with this, in May 2025 about half of consumers in Europe’s leading HDHT markets still intended to spend less on furniture.

Source: OECD, 2025

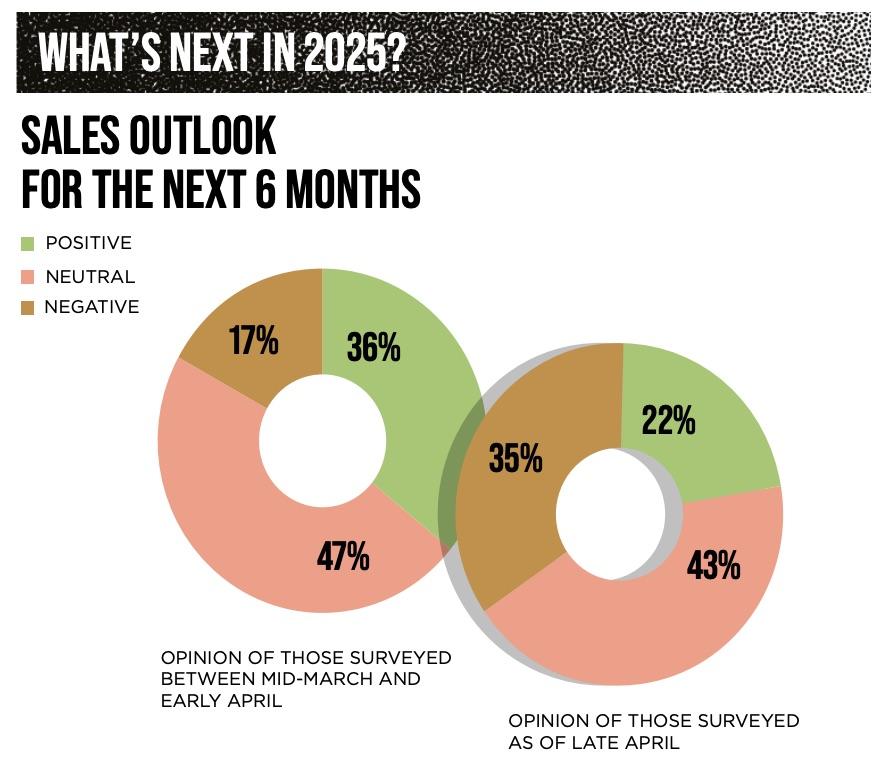

General 2025–2026 forecasts for consumer spending (‘private consumption expenditure’) growth in the leading European HDHT markets are relatively positive. This seems to be reflected in the April 2025 Maison&Objet Barometer. For most European HDHT professionals, sales were the same (37%) or up (26%) in October 2024 through March 2025 compared to the same period in the previous year. For April–September 2025, 47% of international HDHT professionals expected their sales outlook to be neutral. Prospects were positive for 36%.

However, after the original survey, the US announced various international trade tariffs. As a result, 32% of the HDHT professionals who provided updated projections lowered their outlook. 7 out of 10 respondents feared that the tensions over customs tariffs would affect their businesses.

Figure 5: HDHT professionals’ sales revenue prospects for April–September 2025

Source: Maison&Objet Barometer – Issue 10

The combination of high prices and low consumer confidence may lead consumers to trade down towards lower-end products. They might also save up for more timeless items as offered by the mid-high to premium segments. At the same time, pandemic-related lockdowns have led to an increased focus on the home and garden, and trends like wellness and ‘home sweet home’. The importance of the home and garden is generally expected to stay high and drive demand for HDHT products. This may partially compensate for the pressure that the cost-of-living crisis puts on consumer spending.

Tips:

- For more insights into the effect of rising prices, check out 8 strategic options for small businesses to overcome inflation and 7 business tips for dealing with high inflation.

- See our study about the trends in the European HDHT market for an overview and an analysis of their effect on demand.

Demand for sustainable HDHT is growing

Sustainability is becoming a must in the European HDHT market. The European Green Deal includes both environmental and social requirements. In this context, many European laws are under revision and new legislation is being and has been developed. Some of this will apply to you directly, and some indirectly through your buyers. If you prepare well and can meet the requirements, this new legislation can create opportunities.

Relevant EU sustainability legislation

Particularly relevant sustainability legislation for the HDHT industry includes the:

- Corporate Sustainability Due Diligence Directive;

- Forced Labour Regulation;

- Ecodesign for Sustainable Products Regulation;

- Green Claims Directive proposal;

- Textile Regulation revision proposal;

- Deforestation Regulation;

- Packaging and Packaging Waste Regulation.

Well-known sustainable initiatives (like BSCI, ETI, Sedex or WFTO) and certifications (such as FSC, GOTSor OEKO-TEX Made in Green) can help you prove your sustainability.

Besides these legal developments, European consumers are also adopting more sustainable lifestyles more often. In Europe’s leading HDHT markets, most consumers believe that leading a sustainable lifestyle is important. At the same time, the current cost-of-living crisis drives the need for sustainable products to be affordable. According to an IFH KÖLN study for Messe Frankfurt, rising prices have made sustainable products less affordable for nearly half of the consumers in leading European HDHT markets. Many worried that they can afford less sustainable products in the future.

Although there are no official trade data on sustainable HDHT products, HDHT retailers have previously noticed growing interest from their customers in ethical products. This includes items made with natural or recycled/recyclable materials, using socially responsible modes of production. Despite the cost-of-living crisis, 55% of British adults in a 2024 survey say it is important that their HDHT products are made sustainably. Retailers have also noted increased demand for recycled products, upcycled products and second-hand/pre-owned items. Interest in these products is also reflected in British consumer behaviour, for example.

* in the previous 12 months

Source: Deloitte

Tips:

- Use sustainable solutions for raw materials, production, transport and distribution, consumer use, and waste disposal.

- Clearly communicate your sustainable values through your marketing materials. If your products have a unique origin and/or story, communicate the special techniques, materials, producers, processes or meanings. This may add value to your concept and that of your importer.

- For more information, see our study on sustainability in HDHT, our tips to go green and tips to become socially responsible,and our webinars on sustainability in the European HDHT market and sustainable innovations for your HDHT business.

- For more information on relevant legislation, sustainability initiatives and relevant certifications, see our study on buyer requirements.

- Prepare for the new and upcoming EU legislation. Discuss with your buyers what they need from you, for example when it comes to their due diligence obligations, and how you can help each other in the process.

China dominates the European HDHT market

China is Europe’s main HDHT supplier. The country has large-scale and highly mechanised production systems. They also have good availability of (especially man-made) raw materials. These factors make China a competitive supplier. However, rising labour costs have affected its price competitiveness, and trade disruptions impact exports. European importers are looking for suppliers in other (developing) countries more often. They want to diversify their collection, become less dependent on China as a single supplier, and/or order shorter runs to reduce stock risk.

* Excluding China

Source: UN Comtrade, 2025

Nevertheless, China’s HDHT exports to Europe grew from €41 billion in 2020 to €55 billion in 2024. This translates to a CAGR of 7.8% and a direct market share of 32% in 2024. The other leading suppliers are all European countries, trading (and often re-exporting) within Europe. Germany is the largest, with €15 billion in 2024. Poland follows with €11 billion, Italy with €9.8 billion, France with €7.5 billion and the Netherlands with €6.2 billion.

Countries’ roles in the European market

European countries have different roles in the market. Some are mainly importers and others are mainly manufacturers. Western European countries are mainly importers, and most Western European importers are re-exporters. They do not just sell their products in their own country, but they distribute them across the continent.

European production mainly takes place in Eastern Europe, mostly because of relatively low transport and labour costs. This can make these countries a good alternative for European buyers to source low- to mid-end products. Western and Southern Europe also produce some high-end products from well-known premium brands with a long history.

In general, your focus should be on the mid- to high-end market. These segments offer you good opportunities if you can add value to your products. This can, for example, be done via design, craftsmanship, and sustainable aspects. This allows you to avoid competition from mass-producing low-cost countries at the lower ends of the market, like China.

Developing countries outside of China are performing relatively well

The interest in finding alternatives to Chinese suppliers could benefit companies from other developing countries, like you. Their combined supplies of HDHT products to Europe grew from €17 billion in 2020 to €23 billion in 2024, at a CAGR of 7.6%. With this, their direct import market share grew from 12% to 14%.

Out of these countries, the 6 leading suppliers are:

- India – €4.1 billion

- Vietnam – €3.9 billion

- Türkiye – €3.9 billion

- Pakistan – €2.9 billion

- Indonesia – €1.4 billion

- Bangladesh – €1.2 billion

Categorising these imports reveals that China almost completely focuses on home decoration (92–93%). The supply from other developing countries is more balanced, with about two-thirds home decoration products and one-third home textiles. Individual countries clearly differ in their focus category.

Home decoration supplies from developing countries other than China

Source: UN Comtrade, 2025

When it comes to home decoration exports from developing countries other than China to Europe, Vietnam is the largest. It directly supplied 2.5% of Europe’s home decoration imports in 2024. India followed with a direct market share of 1.5%, Türkiye with 1.4%, and Indonesia supplied a further 0.9%. Serbia and Thailand accounted for about 0.4% each.

Vietnam mainly specialises in home decoration (about 95%) rather than home textiles (about 5%). Like producers from China, Vietnamese suppliers are very productive and can produce at low cost. They generally have a good idea of what is commercial and trendy, and effectively combine handmade and mechanised production. As a result, they can be an effective (second or dual-sourcing) alternative to China. Although there are exceptions, Vietnam mainly produces for the lower-end segments with limited design value. This should generally not be your focus.

Manufacturers from India, Indonesia and Thailand are likely more direct competition for you. These producers often have access to a wide range of natural materials and skilled craftsmanship. This allows them to compete in the mid- to high-end segments of the European market. These countries each have their own offering and established place in the market. For example, Indonesia is Europe’s leading supplier of rattan furniture, as the country is estimated to produce up to 80% of the world’s rattan.

Turkish suppliers provide a mix of industrial and handmade production at relatively low costs. They benefit from their location close to Europe, which allows them to offer short delivery times. Eastern European countries also offer a convenient location and relatively low labour costs. Serbia joined the top 6 largest suppliers of home decoration from developing countries other than China in 2022, overtaking Ukraine which now comes seventh. Bosnia-Herzegovina is in tenth position.

Home textile supplies from developing countries other than China

Source: UN Comtrade, 2025

Pakistan, Türkiye and India are key players in the European home textiles market. Together, these countries directly accounted for about a third of imports in 2024. Bangladesh supplied another 4.9%, followed by Egypt and Vietnam with about 1% each.

Leading suppliers Pakistan and India are high-volume, low-pricing sourcing hubs for home textiles, with access to cheap labour. These countries are worldwide leading cotton producers, with a large spinning capacity to make textile products from this cotton. Their producers also have the wider power looms that are required to efficiently manufacture bigger-width items. Vietnam also specialises in high-volume, low-cost production. Like in home decoration, you should avoid competing on price: focus on the mid- to high-end segments of the home textiles market instead.

Bangladesh is a more direct competitor to you. With its reasonable prices, large skilled workforce and abundance of renewable natural materials, Bangladesh can produce home textiles for the mid- to high-end market. Egypt, on the other hand, is famous for its high-quality Egyptian cotton. This makes the country a strong player in high-end cotton products. As in home decoration, Turkish home textile manufacturers benefit from their convenient location and relatively low-cost labour.

South and Southeast Asia dominate the supplies of home textiles to Europe – not just from developing countries but worldwide. Cambodia, Tunisia and Sri Lanka are also fairly large home textile suppliers that are performing relatively well in the European market.

Tips:

- Compare your products and your company to your competitors. You can use the ITC Trade Map to find exporters per country to compare aspects like market segment, price, quality and target countries.

- See the CBI’s studies per HDHT product group to determine the competition for your specific products.

- Avoid competing on cost with mass-producing countries in the low-end market, unless one of your core competencies is to continuously improve the efficiency in your production chain. Instead, add value to make your products stand out.

- For more information about segments in HDHT, see the CBI’s study on market channels and segments.

2. Which European markets offer the most opportunities for home decoration and home textiles?

The larger Western European economies are the main importers of HDHT products. However, importers in these countries generally re-export their products to various countries across Europe. Your best strategy is therefore to focus on a segment rather than a specific country.

Source: UN Comtrade, 2025

Europe’s leading importer of HDHT products is Germany, which had a 16% market share in 2024, followed by France (13%) and the United Kingdom (12%). Together, these countries account for almost half of all European HDHT imports. The Netherlands (8.2%), Italy (6.7%) and Spain (5.7%) are smaller markets that had a share of less than 10% but that were still in the top 6 importers.

Most Western European importers, however, resell their imported products across Europe, or a specific European subregion like Scandinavia or the Benelux. This explains why in HDHT, small countries like the Netherlands often import much more than they consume.

Focus on segments

In terms of marketing, you should know that countries are not markets. The HDHT market consists of different segments, ranging from low- to high-end (see the CBI’s study on market channels and segments). Every European country has these segments, although their size may vary. As such, it makes much more sense to focus on a segment in your product group and connect to importers in that segment instead of in a specific country. These importers will then sell your products in that segment across Europe.

Source: UN Comtrade, 2025

Germany is Europe’s largest importer

Europe’s leading HDHT importer is Germany. The country is the largest economy in Europe, home to nearly a fifth of the European Union’s population. Germany’s large domestic market, role as a trade hub, and relatively high HDHT imports from developing countries make it an interesting market for you.

Germany’s HDHT imports grew slightly from €27 billion in 2020 to €28 billion in 2024, at a CAGR of 0.4%. Because Germany managed to keep its imports fairly stable during the trade disruptions of 2020, this growth is relatively modest. The country’s role as a key trade hub in Europe may have helped it maintain its strong performance. Imports peaked at a strong €31 billion in 2021/2022.

Direct HDHT imports from developing countries performed well. They grew from €12 billion in 2020 to €15 billion in 2024 at a relatively strong CAGR of 5.1%. They peaked at €17 billion in 2022. As a result of this strong performance, their direct import market share grew from 44% to 53%. This was well above the European average of 46%, making Germany the largest European market for HDHT imports from developing countries. Germany’s main suppliers from developing countries are China, Türkiye, India and Vietnam, followed by Pakistan, Bangladesh and Indonesia.

In 2024, the total German HDHT import value consisted of €25 billion worth of home decoration products (88%) and €3.3 billion worth of home textiles (12%). While 50% of home decoration imports came straight from developing countries, for home textiles this share was much larger at 71%. This matches the European pattern.

France relies on intra-European trade

France is the second largest European importer of HDHT products. Its HDHT imports grew from €19 billion in 2020 to €23 billion in 2024. Imports were relatively low in 2020 but bounced back strongly to a peak of €24 billion in 2022. This resulted in an overall CAGR of 4.3% between 2020 and 2024.

As a result of trade disruptions in 2020, France substituted some of its direct imports from developing countries with supplies from European trade hubs like Germany, the Netherlands and Belgium. However, they seem to be shifting back now. Developing countries’ direct share of France’s HDHT import market grew from 29% in 2020 to 44% in 2024, just below the European average. This suggests the French market may offer opportunities for you.

China, India, Vietnam, Türkiye and Pakistan are France’s leading suppliers from developing countries. Opportunities for (nearby) countries that are highly proficient in French, like Tunisia and Morocco, are relatively good, as this makes it easier for French importers to do business with them.

French imports generally consist of around 90% home decoration products and 10% home textiles. Again, the direct market share of developing countries is much higher for home textiles (70% in 2024) than for home decoration (41%).

Brexit stimulates direct trade with the United Kingdom

The United Kingdom (UK) could well offer you opportunities, seeing the country’s high imports from developing countries and potentially increased interest in direct sourcing. The UK’s withdrawal from the European Union (Brexit) has led to relatively low consumer confidence levels since 2016. At the same time, Brexit has resulted in British buyers importing more directly from developing countries, rather than via European importers. This allows them to avoid additional fees now that they are no longer part of the EU single market.

The UK’s HDHT imports grew from a relatively low €18 billion in 2020 to €20 billion in 2024, with a peak of €23 billion in 2022. This translates to a CAGR of 2.5%. Similarly, its direct imports from developing countries grew from a modest €10 billion in 2020 to €13 billion in 2024. This translates to a relatively strong CAGR of 5.3%. With that, developing countries’ direct import market share grew from 57% to 63%. This was the highest share in Europe, making the UK the second largest European market for HDHT imports from developing countries.

However, quite a lot of these imports come from China – the UK’s leading supplier with a direct market share of 47% in 2024. Other leading suppliers from developing countries are India, Vietnam, Pakistan and Türkiye, followed by Indonesia and Bangladesh.

In 2024, British imports consisted of 87% home decoration products (€18 billion) and 13% home textiles (€2.6 billion). Developing countries were the main source for both, but at 75% their direct market share of home textile imports was particularly large.

The Netherlands is an important European trade hub

Despite being a relatively small country, the Netherlands is Europe’s fourth largest HDHT importer. This is because the country is also a key trade hub, re-exporting imports across Europe and relying on the ‘Rotterdam effect’. Dutch imports grew from €12 billion in 2020 to €14 billion in 2024 at a CAGR of 3.4%. This included a peak of €15 billion in 2021/2022. Like its fellow trade hub Germany, the Netherlands kept its imports fairly stable in 2020.

Dutch direct HDHT imports from developing countries grew from €5.1 billion in 2020 to €6.1 billion in 2024, following a peak of €6.9 billion in 2022. This translates to a CAGR of 4.7%. With that, their direct import marketshare grew from 42% to 44%. China, India and Vietnam are the Netherlands’ main suppliers from developing countries, followed by Pakistan, Türkiye, Indonesia and Cambodia.

In 2024, Dutch imports consisted of 90% home decoration products (€13 billion) and 10% home textiles (€1.4 billion). Developing countries’ direct import market share was 43% for home decoration and 55% for home textiles. This matches the general European pattern.

Italy’s imports have stabilised after a dip

Italy could offer opportunities considering the strong recovery of its HDHT imports. Being particularly affected by the pandemic, Italy experienced a GDP drop of -8.8% in 2020. The country’s HDHT imports were hovering around €10 billion, before falling to €8.6 billion in 2020. However, they recovered strongly in 2021 and 2022. Since then, they have stabilised at about €11 billion. This translates to a relatively strong CAGR of 7.3% between 2020 and 2024.

Italy’s HDHT imports from developing countries grew from a relatively low €3.4 billion in 2020 to €4.7 billion in 2024, at a strong CAGR of 8.5%. This included a peak of €5.6 billion in 2022. For 2024, this resulted in a modest direct import marketshare of 41%. Italy’s leading suppliers from developing countries are China, Türkiye, India, Pakistan and Vietnam, followed by Bangladesh, Myanmar and Indonesia.

In 2024, Italian HDHT imports were made up of €10 billion worth of home decoration (89%) and €1.3 billion (11%) worth of home textiles. Developing countries’ direct share for home decoration was 38%. At 66%, the share for home textiles from developing countries was rather high.

Spain’s imports have also bounced back

Spain is the sixth largest European HDHT import market. In 2020 the Spanish economy experienced the largest drop in Europe, with a decrease in GDP of -11%. Spain’s HDHT imports dropped to €7.2 billion in 2020, but they came back strong in 2021. In 2024, they reached €9.7 billion at a strong overall CAGR of 7.5%. This is the highest CAGR in Europe, but the relatively low import values in 2020 partly account for that.

Spain’s imports from developing countries grew from €3.5 billion in 2020 to €5.1 billion in 2024, at an impressive CAGR of 9.6%. As a result, their direct import market share grew from 49% to 53%. This was well above the European average. China, India, Vietnam and Pakistan are Spain’s main suppliers from developing countries, followed by Türkiye, Bangladesh and Indonesia.

In 2024, home decoration made up 89% (€8.6 billion) of Spanish HDHT imports, and home textiles 11% (€1.1 billion). The direct developing country share was especially large for home textiles at 72%.

Tips:

- Do not just focus on specific European countries. Particular market segments (high, middle or low) generally behave similarly across countries, whether they are mature or emerging markets. Your best approach is to identify the appropriate segment for your products and let your buyers distribute your products across Europe within this segment.

- Use European HDHT trade associations to find buyers. Key associations include EURATEX (textiles) and EFIC (furniture). National associations like HWB (Germany), the Giftware Association (UK) and VIIA (the Netherlands) can also be useful.

- Visit European trade fairs to find buyers. The main European HDHT trade fairs are Ambiente, Heimtextil (home textiles) and imm cologne in Germany, and Maison&Objet in France. Other interesting events in the key markets include spoga+gafa (garden) in Germany, the Autumn Fair and Spring Fair in the United Kingdom, showUP and Design District in the Netherlands, Salone del Mobile in Italy and Intergift in Spain.

- See the CBI’s tips for finding buyers for more information on how to search for and/or attract new buyers.

- See the CBI’s studies per HDHT product group for more specific trade statistics for your products.

3. Which products from developing countries have the most potential in the European market?

The European HDHT market offers opportunities. Particularly promising product groups include basketry, carrying products (bags), candles, home furniture, bed textiles and homewear. These groups show good potential based on trade statistics and sector trends.

The HDHT sector is large and very diverse, even within the individual home decoration and home textile sub-sectors. These sub-sectors are further divided into categories, consisting of various product groups. Analysing these product groups can give you a broad idea of promising products for the European market. However, you should keep in mind that the true potential of a product also depends on factors like its quality, price, style and design, and thus the segment you target with it.

The European HDHT market generally offers you good opportunities, especially in the mid- to high-end segments. To appeal to consumers in these segments, your product needs to stand out. You should use design, decoration, craftsmanship and the story behind your products to stand out from your competition. Using special (sustainable) materials, techniques and patterns are good ways to add value. If you support this with an active sales strategy, you can be successful.

This section highlights 6 promising HDHT product groups to give you an idea of the potential in the European market: basketry, carrying products (bags), candles, home furniture, bed textiles and homewear. Of course, opportunities are not limited to these products – there is potential across the whole sector.

Basketry

A traditionally strong product group in HDHT is basketry. Unlike in many other HDHT product groups, Europe’s basketry imports did not drop during the trade disruptions of 2020. They stayed fairly stable at €586 million, before peaking at €929 million in 2022. After returning to more ‘normal’ levels in 2023, they resumed growth to reach €739 million in 2024. This translates to an overall CAGR of 6.0%, which is well above the sector average of 3.7%.

Europe’s basketry imports mainly come from developing countries. In 2024, developing countries directly supplied about 77% of them. China is the leading supplier with a 38% import market share in 2024 (€284 million), but this share has declined (from 44% in 2020). At the same time, the combined direct import market share for other developing countries such as Vietnam, Indonesia, Madagascar and Bangladesh grew from 36% in 2020 (€209 million) to 39% in 2024 (€288 million). This translates to an export value CAGR of about 8.4%.

Baskets are both decorative and functional storage items. They help consumers create both physical and, as a result, mental space. This type of ‘decluttering’ fits in well with the long-term sector trends of wellness and shared living. The pandemic boosted these trends, as restrictions forced people to spend more time together at home.

Source: UN Comtrade, 2025

Basketry also fits in well with the growing importance of sustainability. About 80% of the basketry that Europe imports is made from natural materials. In 2024, 9% was bamboo, 12% rattan and 59% ‘other’ natural materials like sea grass, jute, water hyacinth and abaca. However, using natural materials does not automatically make a product sustainable. The raw materials must come from responsibly managed, renewable sources. Paints and dyes should also preferably be natural. This partly explains the declining market share of China, which uses a lot of manmade materials.

In addition, when baskets are made by hand this further contributes to the concept of sustainability. Basketry can reflect its origins in its materials, techniques and meanings. It is traditionally a key part of the fair-trade segment. Especially handmade items that feature traditional patterns, weaving techniques or unique materials. These baskets are often made by women in rural areas. Africa has a strong tradition in basketry – from Ghanaian bolga baskets to raffia baskets from Madagascar. Asia also has a tradition in basketry, as do some Latin American cultures.

Video 1: xN Studio – fair trade basket weaving in Uganda

Source: xN Home

Bags

Carrying products, or bags, are a large product group with good potential. This is the largest home textiles group among Europe’s HDHT imports, both overall and for exporters in developing countries. Bags within the HDHT sector are mainly functional. They range from shopping and travel bags to office and school bags. More fashion-oriented personal accessories belong to the apparel sector, rather than HDHT.

When the COVID-19 pandemic restricted travel and forced people to stay home, they did not need bags to carry their items around. This contributed to a sharp drop in imports. When restrictions were lifted, people needed bags again for activities like travelling, commuting, playing sports and shopping. Even during the current cost-of-living crisis, European consumers continue to travel. In line with this, European imports of bags bounced back. As a result, imports grew from a relatively low €18 billion in 2020 to €23 billion in 2024, at a CAGR of 7.2%.

Developing countries’ direct import market share grew from 44% in 2020 to 52% in 2024. Leading supplier China accounts for about a third of Europe’s imports. Its export value dropped sharply from €7.4 billion in 2019 to €5.2 billion in 2020. They then recovered to €8 billion in 2024. At the same time, the combined direct imports from other developing countries (like Vietnam, India, Indonesia, Cambodia and Myanmar) increased from €2.5 billion in 2020 to €4.0 billion in 2024. With that, their market share grew from 14% in 2020 to 17% in 2024.

The largest category in this product group includes textile travelling bags, rucksacks and shopping bags. Such textile items are a good alternative to disposable plastic bags, which are used less and less following restrictions set by the EU’s Plastic Bags Directive. Internationally, most consumers use their own shopping bags. For example, 86% of Dutch people bring their own bags for grocery shopping, 70% for clothes shopping, and 77% for other kinds of shopping. Popular types include foldable bags, linen/cotton bags, backpacks and bicycle bags.

The rising demand for sustainability is also expected to boost long-term interest in bags from materials like jute, sea grass, mela leaf, catkin, or recycled materials. This offers opportunities for countries that are rich in these types of resources, like Bangladesh.

Sustainable alternatives to disposable plastic bags

A 2022 Euroconsumers study shows reusable plastic shopping bags (LDPE) sold at supermarket checkouts are the most environmentally friendly option – but context is key. A ‘life cycle analysis’ of different types of shopping bags considered all the resources used to make, ship, use and dispose of them.

For an LDPE bag, 1 or 2 uses are enough to pay for its environmental impact – depending on whether or not it contains recycled materials. Jute bags need 36 to 68 uses to have less impact than LDPE. Cotton bags must be used just over 100 times due to the water and energy consumed in their production. Organic cotton bags would have to be used 154 times because organic cultivation requires more land. However, the study suggests that up to 90% of the energy footprint of bags comes from shipping them from Asia to Europe.

Of course, the longer consumers keep using a bag, the more sustainable it becomes. You can facilitate this in your design: by making your bags durable and attractive, you invite consumers to keep reusing them.

Candles

Another well-performing product group is candles. The European Candle Manufacturers Association estimates that 700 million kg candles are consumed each year in the EU. Home wellness products like scented candles are popular in Europe, with 57-73% of French, German, British and Italian survey respondents in 2023 regularly buying/using them. The popularity of scented candles is reflected in a recent international survey, in which 75% of HDHT retailers also sell fragrances, scents and perfumes – including scented candles. 53% of these retailers have noticed increased demand for such products.

Like basketry, Europe’s candle imports did not drop during the trade disruptions of 2020. They grew from a steady €1.7 billion in 2020 to €2.2 billion in 2024, at a strong CAGR of 6.3%. This includes a peak of €2.5 billion in 2022. Developing countries’ direct market share grew from 20% in 2020 to 31% in 2024. Although most of these candles came from China, other developing countries also performed well – including Vietnam and India, as well as countries like Indonesia, Türkiye, Tunisia, Morocco and Cambodia. Their combined market share grew from 4% in 2020 to 6% in 2023, as their supplies nearly doubled from €67 million to €124 million.

Candles play a key role in wellness, especially when they are scented. Scents are known to have an effect on people’s wellbeing. According to the National Candle Association, selecting candles based on their scent or fragrance can be a great way to improve your mood, reduce anxiety, and even combat fatigue or loneliness. Candles also make good gifts that fit in well with the home sweet home trend, especially to create a cosy atmosphere during the darker months and the holiday season. In a 2024 survey, fragrances, wellness products and gifts were among HDHT retailers’ best-performing categories in terms of sales. This continued into 2025.

Video 2: IKEA – Scented plant-based wax candles in glass and ceramic jars

Source: IKEA

Plant-based ingredients and organic wax are used more and more to offer a more sustainable alternative. For example, soy wax has become a popular option. Beeswax candles are a niche category, often offering a mix of natural ingredients and handmade production.

Home furniture

Home furniture made from wood, metal and other natural (wood-like) materials is a much broader home decoration product group than basketry and candles. It includes items like chairs, tables, beds, stools and sofas. This is the largest European HDHT imports product group, both overall and for exporters in developing countries. Imports grew from €35 billion in 2020 to €40 billion in 2024, at a CAGR of 3.3%. They were fairly stable during 2020’s trade disruptions, before peaking at €45 billion in 2021–2022.

Although this is a strong product group, the cost of living crisis has put pressure on consumers’ intentions to make major purchases like large pieces of furniture. This was likely shown in a 13% decline in imports in 2023. However, import growth resumed in 2024. The returning interest in furniture was also reflected in the April 2025 Maison&Objet Barometer. 63% of retailers (outside France) sold the same or higher volumes of furniture between October 2024 and March 2025 compared to the same period in the previous year.

Developing countries’ direct import market share grew from 36% in 2020 to 40% in 2024. This was boosted by an impressive 21% import increase in 2024. Leading supplier China’s share fluctuated between 24% and 30%, when the combined share of other developing countries (like Vietnam, Türkiye, India and Indonesia) was fairly stable at about 11%.

Within this product group, Europe mainly imports wooden furniture (more than 60%). This includes upholstered pieces with wooden frames. Other natural materials like rattan, bamboo and cane are also popular, although this category is much smaller (about 2%). Indonesia is a particularly strong player in rattan, supplying about half of Europe’s rattan home furniture imports.

Video 3: H&M Home – rattan lounge chair

Source: H&M Home

Your furniture needs to stand out to keep appealing to consumers, even when budgets are limited. For example through its design, materials or craftsmanship. Smaller furniture pieces that require less of an investment, like side tables or multifunctional poufs, may be particularly attractive.

This fits in well with the trend of shared living and smaller living spaces, which suggests that (smaller) flexible and multifunctional furniture has particular potential. Pieces that are easy to move and/or modular (with individual components) allow consumers to rearrange their furniture according to their current needs. Items that are collapsible and/or can easily be stored offer extra space and flexibility, and added functionality may provide storage space. These types of furniture also fit in well with consumers’ need to keep their homes clutter-free.

Bed textiles

Another large product group is bed textiles – the second largest of Europe’s home textile imports from developing countries, after bags. It consists of products like duvet covers, bedspreads and pillowcases. European overall bed textile imports grew from €4.1 billion in 2020 to €4.3 billion in 2024, at a CAGR of 1.3%. This includes a peak of €5 billion in 2022.

As is common in the home textiles sub-sector, China plays a relatively modest role in this market with a 12% import market share in 2024 (€535 million). Together, developing countries other than China directly supply nearly a third of Europe’s bed textile imports (€2.8 billion in 2024). Pakistan is a particularly important player, directly supplying 44% of Europe’s bed textile imports in 2024 (€1.9 billion).

Trendy sustainable materials for bed textiles include organic cotton, hemp and bamboo. Ramie and soy silk are popular for duvet covers too. Bed textiles also play a role in the wellness trend. Because a good night’s sleep is essential, comfortable bed textiles that create a relaxed atmosphere are a must. In fact, sleeping is among the most important activities for achieving a sense of wellbeing at home. Plus, 33% of people consider sleep important for improving mental health. As a continuing consumer trend, wellness is set to keep driving long-term demand.

Video 4: URBANARA – ethically produced bed textiles of natural materials

Source: URBANARA GmbH

Homewear

Homewear has a special place in home textiles. This large product group consists of sleepwear and bathrobes. Thesehich are products you wear rather than use around the house. Europe’s homewear imports grew from €2.8 billion in 2020 to €3.3 billion in 2024, at a CAGR of 4.2%.

With 24% of imports in 2024, China was Europe’s leading individual homewear supplier. However, other developing countries played a much larger role in this product group. This is particularly true for those that specialise in textiles and clothing, like Bangladesh (18%). Their supplies grew from €1.3 billion in 2020 to €1.7 billion in 2024, at a CAGR of 7.3%. With that, their combined direct import market share grew from 47% to 53%.

There is a lot of mass production in the home textiles sector from countries like India. But there are opportunities for smaller-scale producers that pay more attention to detail. Cotton is the most common material, accounting for more than half of Europe’s imports. Other natural materials account for about 9%. This includes more luxurious fabrics like silk and cashmere, or blends of these fibres. Popular sustainable options include organic cotton and bamboo fibres.

Video 5: CARE BY ME – bathrobe of 100% GOTS-certified organic cotton

Source: CARE BY ME

Homewear also fits in with the wellness trend. Like cosy bed textiles, comfortable sleepwear is key to a good night’s sleep. And a luxurious, soft bathrobe adds to the relaxing spa experience that many consumers are recreating in their own home. Simple and affordable products that help consumers unwind and improve their wellbeing at home can make a big difference.

Tips:

- See our studies per HDHT product group for an analysis of the potential of your specific products. These include studies on products such as basketry, textile travel accessories, office and school bags, candles, soap, bed textiles, and homewear.

- See our study about the trends in the European HDHT market for an overview and an in-depth analysis of their effect on demand.

- For more information about the European ban on single-use plastics and other legislation, see our study about the requirements your products must comply with on the European HDHT market.

- Keep in mind that for most product groups, the potential is highest in the mid- to high-end market segments. Avoid having to compete on price at the lower ends of the market unless you specialise in low-cost/high-volume production. For more information, see our study on market channels and segments in HDHT.

Globally Cool carried out this study in partnership with GO! GoodOpportunity and Remco Kemper on behalf of CBI.

Please review our market information disclaimer.

Search

Enter search terms to find market research