What is the demand for outbound tourism on the European market?

Global outbound tourism has recovered from the pandemic. There is continued growth in the first half of 2025. Germany and the UK are the largest European markets, and demand from all source markets is high. The highest growth in arrivals to South America, Africa and Asia was between January and June 2025. Traditional destinations are still popular among Europeans, including Türkiye, Egypt and Morocco. Emerging destinations that are becoming more popular include Vietnam, Sri Lanka, Jordan, Tunisia and Indonesia. Popular niches are adventure, community-based tourism, culture, food, nature and wellness.

Contents of this page

1. What makes Europe an interesting market to target?

Europe is an interesting market to target because it is the largest outbound travel market. It makes up over half of all international outbound regional markets in 2024 (51.6%). Now that the sector has recovered, growth is expected to slow to a new normal.

There is increased demand for off-the-beaten-track destinations like Paraguay, Brazil and Mongolia. But the state of the global economy makes growth more difficult. It creates uncertainty among consumers. Making sustainability a part of all aspects of a tourism business is still a major requirement.

Current status of worldwide tourism

The tourism sector achieved made a full recovery in 2024 as international tourist arrivals reached 1.47 billion. This was slightly lower than arrivals in 2019 (1.68 billion), although the effect of this on each region varies. Growth has continued into the first half of 2025 (January to June) with overall growth of 5.1%. This is despite ongoing geopolitical crises and trade tensions that are having global impacts on many sectors.

Table 1: Status of International Tourism Arrivals 2022 to 2024

| Region | 2019 (millions) | 2023 (millions) | 2024 (millions) | % change 2019-2024 | % change 2024 vs 2025 (Jan-June) |

|---|---|---|---|---|---|

| World | 1,468.0 | 1,307.0 | 1,470.0 | 0.1% | 5.1% |

| Europe | 745.8 | 710.6 | 758.6 | 1.7% | 3.9% |

| Asia and the Pacific | 362.1 | 237.8 | 317.8 | -12.2% | 10.7% |

| North America | 146.6 | 126.6 | 137.3 | -6.3% | 0.2% |

| Central America/Caribbean | 37.0 | 39.7 | 44.3 | 19.7% | 0.2% |

| South America | 35.9 | 33.8 | 36.7 | 2.2% | 13.9% |

| Africa | 68.8 | 65.2 | 73.9 | 7.4% | 12.4% |

| Middle East | 71.6 | 93.4 | 101.2 | 41.3% | -4.2% |

Source: UN Tourism, 2025

Analysis of tourism statistics by region shows the following:

- Middle East: the fastest-growing region in international arrivals during 2024, 41.3% higher than 2019 arrivals. But arrivals went down by 4.2% between January and June 2025. This was probably because of geopolitical tensions in the region.

- Central America/Caribbean: international tourism was 19.7% higher in 2024 than in 2019. This was the second-highest growing region, even though there was flat growth in the first half of 2025 (0.2%).

- Africa: tourism growth in 2024 was 7.4% above levels reached in 2019. Between January and June 2025, there was a 12.4% increase in international arrivals – the second-highest growing region. Both North Africa and sub-Saharan Africa had double-digit growth of 14% and 11%, respectively.

- South America: has recovered from the pandemic as international arrivals were 2.2% higher than those of 2019. In the first half of 2025, the region reported the highest growth among all regions in tourist arrivals (13.9%).

- Europe: international tourist arrivals in 2024 were 1.7% higher than in 2019. The region reported 3.9% growth between January and June 2025.

- North America: international tourist arrivals have not yet recovered to 2019 levels. There was still flat growth in the first 6 months of 2025 (0.2%). The region also reported flat growth in the first half of 2024 (0.2%).

- Asia and the Pacific: the region has not yet fully recovered from the pandemic. Tourist arrivals in 2024 were still 12.2% below 2019 figures. This was the slowest recovery worldwide because the region reopened to tourism later than other regions. But in the first half of 2025, international arrivals grew by 10.7%. They reached 92% of pre-pandemic figures. Intra-regionally, Northeast Asia had the highest growth (20.1%) compared to South Asia, which saw a 5.4% decline.

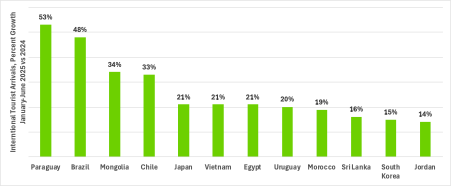

It is interesting to analyse international tourist arrivals by country to see how regional growth is being driven. The chart below shows countries outside Europe where international tourist arrivals were strongest in the first half of 2025.

Figure 1: Countries outside Europe reporting the most growth in January- July 2025 compared to 2024

Source: UN Tourism, 2025

Other countries reporting notable growth in this period include Bahrain (13%) Tunisia and South Africa (12% each), Uzbekistan and Laos (11% each), Malaysia and Indonesia (9% each), and Mexico (7%).

Future projections and challenges

Industry experts like UN Tourism, the World Travel & Tourism Council (WTTC) and investment research organisations say that international arrivals will grow more slowly. The growth rate will be 3-5% from 2026 onwards, after a positive rebound following the pandemic during 2024 and early 2025. Growth will vary by region.

The International Air Transport Association (IATA) also expects growing revenues and increased passenger numbers in 2025. Passenger growth will probably be at 5.8%, a slower rate than in 2024. This is another sign that post-pandemic catch-up is now fading. Tourism will settle into a new normal.

But there are still global challenges to tourism growth. These are linked to the state of the global economy. Global growth was estimated at 3.0% in 2025 and 3.1% in 2026 according to the IMF. Uncertainties like high inflation, higher trade tariffs and geopolitics will keep having an impact on global and regional economies in the coming months. There is low economic growth in many European countries. High inflation affects spending on things like holidays.

Other challenges to tourism growth include current conflicts occurring around the world. The Russia-Ukraine war has now been going on for almost 4 years. Both countries’ tourism sectors have been severely impacted. Russian airspace is still closed to most Western airlines. This makes flights more expensive and longer.

There is instability in the Middle East because of the conflict between Israel and Hamas. It is still causing security concerns in the region. International tourist arrivals to Israel continued to fall in 2024. But arrivals to Jordan went up in the first half of 2025.

There are also other geopolitical factors affecting tourism. Like the trade tensions between the US and China, tensions in the South China Sea and disruptions to trade in the Red Sea. They all have the power to disrupt tourism, raise costs and create uncertainty.

Tip:

- Keep up to date on global, regional and national issues that might impact tourism in your destination. Make sure you understand these issues. This will help you confidently reassure your buyers when they are worried. Be sure to take suitable actions to deal with issues when necessary.

- Keep your risk management policy up to date. It is important to be prepared for as many crises as you can imagine. Use the CBI study How to manage risks in tourism to help you.

Sustainability requirements

At a global level, doing business in a sustainable way to deal with the effects of climate change has never been more important. 107 countries have pledged to net-zero targets, including the European Union (27 countries) and the UK. There has been a lot of publicity around this issue and people throughout Europe are very aware of it.

Regulations around sustainability in tourism are changing in Europe and requirements for businesses are becoming stricter. The EU Sustainability Regulations White Paper 2025 explains 3 new EU laws that will change how tourism businesses talk about and report sustainability. They are: the Corporate Sustainability Reporting Directive (CSRD), the Empowering Consumers for the Green Transition Directive (ECGTD) and the Green Claims Directive (GCD). Learn more about sustainability in tourism and how the sector is responding. The CBI study Which trends offer opportunities or pose threats on the European market? explains more.

To find out how to start taking sustainable actions in your business, read the CBI study How to be a sustainable tourism business.

Analysis of outbound tourism volumes from Europe

Europe makes up 51.7% of global outbound tourism (1,470 million international arrivals in 2024). In 2024, there were 758.6 million international arrivals from Europe. This number was up 1.7% compared to 2019. Every European region reported growth in outbound tourists.

Europeans made 1.19 billion trips in 2024, up 4.4% compared to 2023. Of these, 850 million were domestic tourism trips (71%) and 250 million were taken within the EU (21%). This is not surprising: most Europeans prefer travelling to short-haul destinations. There are many neighbouring countries that are easily accessible, are familiar to Europeans and have excellent tourism offers. The remaining 90 million trips (8%) were made outside the EU.

Source: Eurostat, 2025

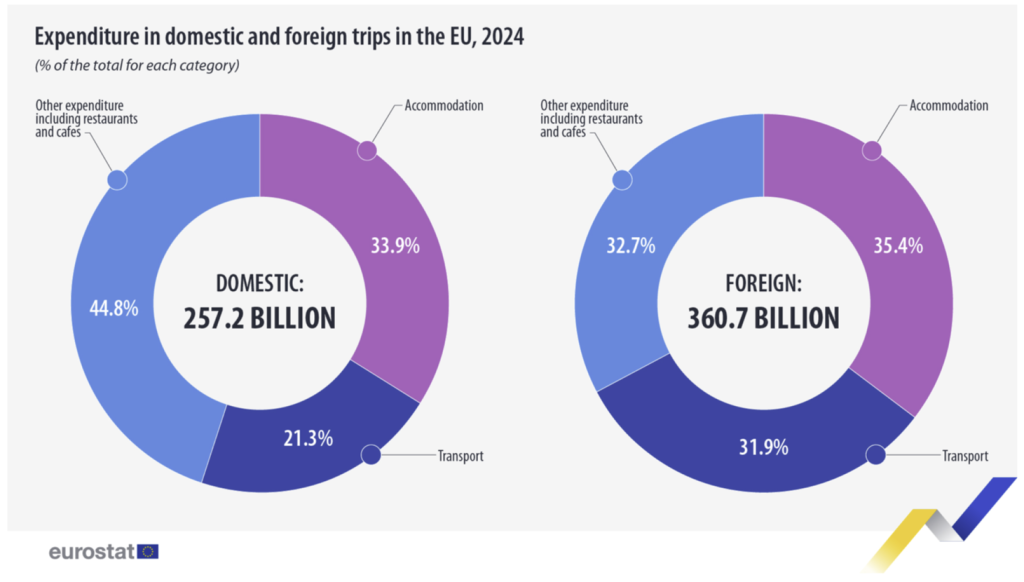

Analysis of expenditure shows that Europeans spent around 40% more on foreign trips than they did on domestic trips. As expected, they spent more on travel and transport when travelling abroad than on domestic trips. Although this chart focuses on travel within the EU, it is useful to highlight how outbound travel generates greater revenue than domestic tourism.

Figure 3: Expenditure in domestic and foreign trips in the EU, 2024

Source: Eurostat, 2025

The number of trips outside Europe went up in 2023, compared to 2022. Africa was still the most popular continent for Europeans. It made up 3.8% of trips (up from 3.2%). This was followed by Asia (3.7%, up from 2.6%), North America (2.4%), and Central and South America (1.5%).

Source: Eurostat, 2025

You can see from the chart below that trips to Africa have almost gone back up to pre-pandemic levels. Trips to Asia still have not quite reached 2019 levels. But it is important to remember that Asia opened up more slowly than other regions.

Source: Eurostat, 2025

Türkiye, Egypt and Morocco were still the most popular destinations for Europeans in 2023. These countries made up 11%, 4% and 4% of trips, respectively. All these countries have been top destinations for European travellers for many years. They have minimal time differences because they are all conveniently located close to the European continent. There is good access and they are well served by air travel, including low-cost carriers (LCCs). They also appeal to tourists on different budgets. What they all share is a pleasant, warm climate that appeals to Europeans.

33 million Europeans travelled to Türkiye, making it the top destination by far. Egypt was the next most-visited destination, with 7.3 million Europeans, followed by Morocco (4.1 million). But we can also see that emerging destinations like Tunisia, Vietnam and Indonesia are interesting for the European market.

Source: UN Tourism, 2024

A deeper analysis of UN Tourism data shows there are differences in where Europeans prefer to go. The table below shows, for example, that:

- For German nationals, the top destinations were Türkiye (5.6 million arrivals) and Egypt (1.3 million).

- For British tourists, the preferred destinations were Türkiye (3.3 million) and Mexico (0.6 million).

- On the other hand, French tourists like to travel to Morocco (1.5 million) and Tunisia (0.8 million).

- Spanish tourists also like Morocco (0.9 million), but Mexico (0.4 million) as well.

Source: UN Tourism, 2024

What this shows is that there are clear differences in preferences between European countries. Language is clearly one reason. Morocco has a high proportion of French speakers, while in Mexico Spanish is the common language. We look into these factors in more detail in the section below, Which European markets offer the most opportunities for tourism suppliers in developing countries?

Analysis of global and European value of tourism

International tourism spending has gone up a lot since 2023. In 2024 it reached €1,603 billion. This was 12.7% higher compared to 2023 and 20.6% higher compared to 2019. These figures do not take account of inflation.

European countries are big spenders on outbound tourism. The 6 major European markets are all in the top-14 source countries by outbound expenditure. Germany, the UK and France are the top-spending markets after the US and China. All markets reported higher spending abroad in 2024, compared with 2019. These high spending increases could be partly because of increased costs as a result of the cost-of-living crisis.

International tourism expenditure went up a lot in all top European source markets. Spending by Dutch tourists went up by almost 50% in 2024 compared to 2019. This is followed by British tourists, whose spending went up by over one third (38.5%). In the first half of 2025, outbound expenditure by British, Dutch and German tourists went up a lot, by 74.8%, 46.75 and 43.0%, respectively.

Table 2: International tourism spending by top source markets, 2019, 2023 and 2024

| Country | 2019 (€ billion) | 2023 (€ billion) | 2024 (€ billion) | % change (2019 vs 2024) |

|---|---|---|---|---|

| World | 1,329.0 | 1,422.0 | 1,603.0 | 20.6% |

| China | 227.4 | 179.8 | 231.6 | 2.6% |

| United States (USA) | 117.9 | 146.7 | 164.2 | 34.7% |

| Germany | 83.3 | 106.8 | 111.1 | 33.4% |

| United Kingdom (UK) | 76.8 | 92.4 | 110.1 | 38.5% |

| France | 48.3 | 51.8 | 55.2 | 14.4% |

| Australia | 31.5 | 39.2 | 42.1 | 36.1% |

| Canada | 31.6 | 36.3 | 40.1 | 26.7% |

| Russia | 32.3 | 32.2 | 35.9 | 7.5% |

| Italy | 27.1 | 31.6 | 33.0 | 21.9% |

| India | 20.5 | 30.8 | 32.3 | 81.3% |

| Spain | 24.8 | 26.3 | 30.0 | 20.8% |

| Singapore | 24.9 | 23.9 | 28.9 | 9.7% |

| South Korea | 29.2 | 25.6 | 27.0 | -10.8% |

| Netherlands | 18.3 | 23.4 | 26.6 | 45.2% |

Source: UN Tourism, 2025

Outside the top-14, Belgium, Switzerland and Norway are the next most important European outbound tourism spenders. This makes them interesting European markets to target.

Tip:

- Monitor trends and patterns around tourism in your target markets. Google Trends and Looker Studio have different free online tools to help you do this. Google Trends shows the popularity of top search queries in Google search. Looker Studio creates graphs, charts and tables to help you visualise this data. CBI has created several Data Studio Dashboards to help you understand demand and recovery of the biggest outbound markets. Read the study How to forecast tourism demand with Google Trends and Data Studio for more information. You can also watch the video on how to use dashboards for additional support.

2. Which European markets offer the most opportunities for tourism suppliers in developing countries?

The European markets offering the most opportunities for tourism suppliers in developing countries are Germany, the UK, Italy, France, the Netherlands and Spain. They are the largest outbound overnight tourism markets from Europe. The UK figures in the chart below include overnight tourists and day visitors.

Sources: UN Tourism, 2024

Research done by CBI in 2025 among the 6 top source markets showed that Türkiye, Africa and South/Southeast Asia were the top regions visited by respondents in 2024 across all markets. The main findings were that:

- Africa was the top destination for France (11.5% of respondents had travelled there in 2024). It was also the top market for Middle Eastern destinations (6.0%).

- Germany was the top market for Türkiye (9.0%) and a key market for Africa (7.5%).

- Respondents from Italy travelled to many different destinations – Africa (4.8%), South/Southeast Asia (3.9%), Türkiye and the Middle East (3.5% each).

- South/Southeast Asia was the most popular destination for the Netherlands (7.5%) followed by Türkiye (3.5%).

- Türkiye was the top destination for Spain (3.5%), and Spain was the leading market (2.7%) for South America, where most people speak Spanish.

- UK was a top market for Africa (8.9%), Türkiye (8.5%), South/Southeast Asia (7.9%) and North Asia (6.7%).

Germany

Germany has the largest population in Europe, around 83 million. It is also Europe’s largest economy although GDP growth is expected to be flat in 2025 (0.2%) and growth in 2026 projected to be 1.1%. Still, Germany’s economy ranks around third to fourth in the world.

The state of the economy means that consumer confidence remains low. This shows concerns over inflation, energy costs and job security. But inflation has eased and unemployment is still relatively low. Germany maintains a very high standard of living. Its per-capita income is above US$60,000 and it has high rankings on human-development measures.

Outbound travel shows a mixed outlook. Price pressures mean around 32% of Germans say they may skip a major holiday in 2025, compared with 17% in 2022. But the country’s overall travel and tourism sector is rebounding strongly and expected to break pre-pandemic records in 2025. This includes renewed growth in international trips.

German outbound travel market

Germany is Europe’s largest outbound travel market. In 2024, German nationals made 108.8 million outbound trips. The total international tourism expenditure was US$118.4 billion.

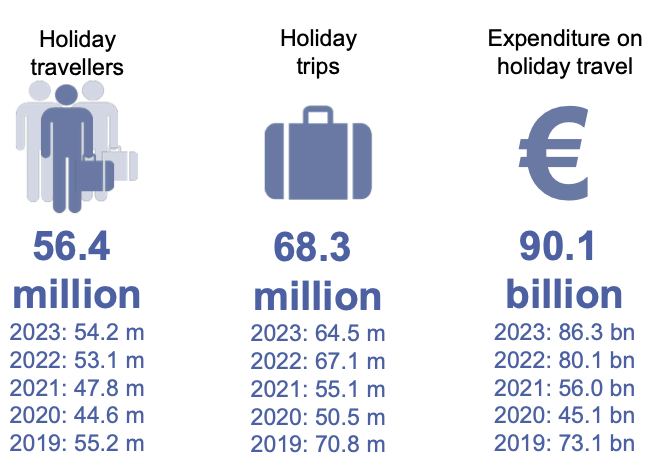

In 2024, Reise Analyse reported that 56 million German nationals took 68 million trips of 5+ nights. While there were more holiday travellers than ever before, there were 2 million fewer trips than reported in 2019. Still, total spending on holiday trips reached a new record of €90 billion. In the short-haul market (trips between 1 and 4 nights) there were 94 million trips with a total spending of €37 billion. Both were record figures.

Figure 9: Volume and value of German holiday travel in 2024 (5+ nights)

Source: Reise Analyse, 2025

Germans like to travel to many different destinations. In 2024, the share of international travel was 76% (down 2% from 2023) compared to domestic travel (24%). Europe was the top destination (57%). Türkiye is still the most popular destination outside of Europe for German tourists. It made up 8.5% of all outbound trips in 2024, a small increase over 2023.

German travel trade

The German travel trade market is mature, with around 2,300 tour operators and 9,000 travel agencies. A small number of operators control almost 50% of the market, including TUI, a leading European travel agency, and DERTOUR Travel. GetYourGuide is Germany’s most well-known OTA. They have a strong presence in the European market.

Retail agencies are still more important in the German market that other markets. But they are facing more competition from online travel portals. Tour operators and travel agencies are represented by the German Travel Association (DRV).

To identify tour operators and travel agents on the German market, take a look at this listing, which is divided by holiday type.

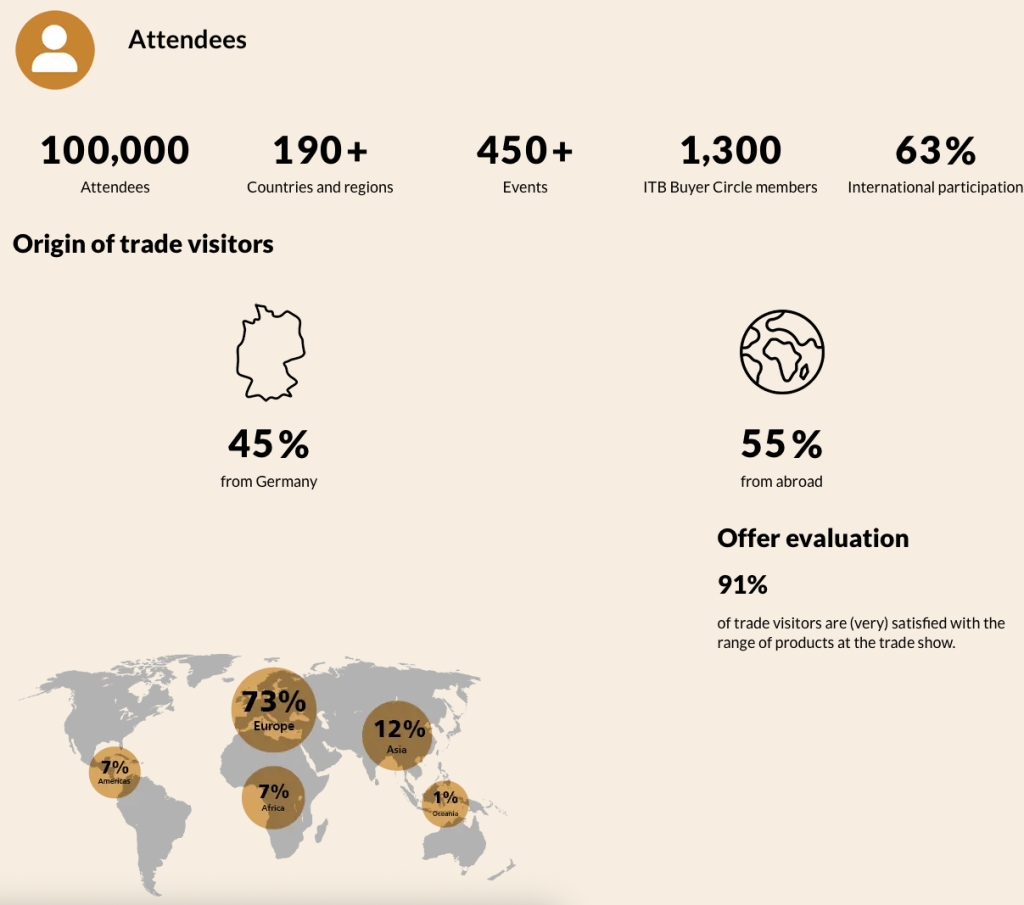

Germany is home to the largest travel trade show in the world every year in March, ITB Berlin. In 2025 it attracted 100,000 visitors and 5,600 exhibitors from more than 190 countries. It also hosts regional shows at ITB Asia, ITB China and ITB India.

Figure 10: Facts and figures about ITB Berlin

Source: ITB Berlin, 2025

German travel behaviour

Germans are travelling for longer periods. The average trip length in 2024 was 13 days, almost as long as in 2023. It is longer than in both 2022 (12.6 days) and 2019 (12.4 days). Germans are spending about the same amount on their trips as they did in 2023, an average of €1,319.

In other CBI research, a breakdown of expenditure on trips taken in 2024 found that Germans spent more than one-third of their budget on accommodation (38.0%). This was more than any of the other source markets except for the Netherlands. This was followed by food and drink (22.0%). Activities made up 14.1% of German budgets, more than other source markets except for France.

Source: CBI, 2025

Online sales channels are becoming more important in the German market. In 2024, over 54% of all holiday trips were booked online, compared to 51.3% in 2023. This is in line with current trends. At the same time, face-to-face bookings fell to 35%. This is another long-term downward trend.

German characteristics and travel motivations

Germans are especially motivated by nature. They enjoy beautiful scenery and wildlife, and going to the beach is a top pastime. They like to be active too, with walking/hiking and cycling as important activities. Culture is also important, and visiting cities, shopping and enjoying local food and wine are key appealing activities. Other motivations include:

- Relaxation and escape from routine (51.5%);

- Spending time with friends or family (50.3%);

- Being immersed in local cultures and people (45.2%).

Sustainability is important, and Germans like to minimise their impact on destinations when they travel. Research conducted by CBI in 2025 found that among German tourists:

- 59.7% felt that choosing local activities to benefit locals was either important or very important;

- 44.5% think that their environmental impact when they travel to a destination is either very important or important.

Other research conducted by the EU in 2021 found that:

- 54% would choose to consume locally sourced products while on holiday;

- 47% would be prepared to pay to protect the natural environment;

- 45% planned to reduce waste while on holiday;

- 43% would travel to less-visited destinations.

United Kingdom

The UK has a population of about 69.9 million. Its economy is one of the largest in Europe and worldwide. The International Monetary Fund (IMF) predicts GDP growth of around 1.3% for both 2025 and 2026. This is one of the highest percentages of all source markets. But inflation also remains the highest in the G7 (Group of Seven – Canada, France, Germany, Italy, Japan, the UK and the US).

British people enjoy a high standard of living. But growth in living standards is widely reported to be the slowest among major Western economies, and consumer confidence is weak.

UK residents were expected to travel abroad more in 2025, with 70% adults planning overseas holidays. But 75% of those planned to actively seek spending less. They choose shorter breaks, look for cheaper (or free) options, find lower-cost airlines, cheaper hotels etc.

British outbound travel market

The UK is the second-largest outbound tourism market in Europe. In 2024, British nationals took 91.4 million trips, representing 6.1% growth compared to 2023. But this is still lower than 2019 levels (93.1 million). Still, British tourists spent £77,396 billion in 2024, up 6.8% from 2023.

The future for outbound tourism is expected to be strong despite economic difficulties. The UK outbound travel market is estimated to be worth US$94.24 billion by 2025. It is projected to reach US$224.17 billion by 2035 – a CAGR of 8.6%. But ongoing economic uncertainties may affect the recovery of tourism. Affordability is now a big factor for British tourists when deciding where to go on holiday.

British outbound travellers spent 9.6 nights on trips overseas in 2024, down from 10.4 nights in 2023. Still, overall spending went up by 6.8% year-on-year, and by 0.7% per trip.

Table 3: British outbound travel – trips, nights, length of stay and spending, 2024

| Year | Total trips | Total nights | Average length of stay | Spent, £ million | Average spent per trip, £ |

|---|---|---|---|---|---|

| 2019 | 93,086,000 | 904,905,000 | 9.7 | 62,325 | 669.54 |

| 2023 | 86,205,000 | 895,965,000 | 10.4 | 72,436 | 840.28 |

| 2024 | 91,435,000 | 880,833,000 | 9.6 | 77,396 | 846.46 |

Source: ONS, 2025

British people travel to a many different countries. They have the highest preference out of all main source markets for visiting developing destinations. Türkiye has kept on being the most popular long-haul destination for British tourists for many years, followed by India. India and many African countries like Kenya and Tanzania are traditionally popular destinations for UK nationals because of historical ties.

The table below shows especially good growth in 2024 to Egypt (209.2%), Morocco (30.6%) and Türkiye (27.4%). You can see that arrivals to the top-5 destinations are higher than they were in 2019. Other destinations that British people liked in 2024 include Japan, Tunisia, Jamaica, Brazil and Sri Lanka.

Table 4: Outbound arrivals of British nationals to developing countries, 2019-2024

| Country | 2019 | 2023 | 2024 | % Change 2023-2024 |

|---|---|---|---|---|

| Türkiye | 2,288,000 | 3,204,000 | 4,082,000 | 27.4% |

| India | 1,606,000 | 1,942,000 | 2,053,000 | 5.7% |

| United Arab Emirates | 1,293,000 | 1,305,000 | 1,400,000 | 7.3% |

| Morocco | 808,000 | 951,000 | 1,242,000 | 30.6% |

| Egypt | 171,000 | 249,000 | 770,000 | 209.2% |

| Pakistan | 768,000 | 641,000 | 625,000 | -2.5% |

| Thailand | 520,000 | 506,000 | 593,000 | 17.2% |

| Mexico | 685,000 | 538,000 | 567,000 | 5.4% |

| Australia | 550,000 | 418,000 | 565,000 | 35.2% |

| Hong Kong (China) | 342,000 | 331,000 | 369,000 | 11.5% |

| South Africa | 487,000 | 377,000 | 346,000 | -8.2% |

| Nigeria | 265,000 | 332,000 | 251,000 | -24.4% |

Source: ONS, 2025

British Travel Trade

There are more than 7,500 travel agencies and tour operators in the UK. The market size is estimated at £28.7 billion. Some of the leading tour operators are Jet2holidays, loveholidays and On the Beach Travel.

The market of tour operators in the UK that specialise in holidays to developing countries is large. Tour operators have global reach. This means their customer base extends further than the UK, to Europe and North America.

Many specialise in adventure travel or in regions, like Africa or Asia. Others specialise in activities like cycling trips or hiking. Some focus on luxury, budget or solo travel. Examples include Explore UK, Intrepid Travel, World Expeditions and Kuoni. Use the ABTA member search listing to find UK tour operators, or use internet listings like this one from TourRadar.

There are some interesting travel trade shows hosted in the UK. World Travel Market (WTM) is a global B2B (business to business) trade show that hosts more than 40,000 professionals from 184 countries yearly in November. It is a good way to network with other businesses. There are regional WTM shows in the Middle East, Latin America and Africa. LATA Expo and Experience Africa want to link buyers from the UK and Europe with suppliers from each continent.

British travel behaviour

By share, British tourists spent more than one-third of their budget to accommodations (37.7%). They spent one-fifth on food and drink (21.8%), less than all other source markets. They also spent less on activities than other source markets (12.2%).

Source: CBI, 2025

Online booking platforms were the most popular method to book trips. Over half of respondents said they often booked their trips online (52.2%). But they also often used different other methods. Examples were booking directly with accommodation providers and/or airlines (37.4%), and OTAs for experiences (30.4%).

British characteristics and travel motivations

Travel is important to UK nationals, and they are experienced overseas tourists. Travel helps them to recharge, escape their daily routine and discover new experiences. They like immersive experiences at destinations, but hygiene, accessibility, convenience and safety are still important to them. British tourists like to take part in activities. This is one of the top factors influencing their final decision. Value for money is important for British tourists, so they want cost-effective tours and experiences.

Other motivations include:

- Spending time with friends or family (50.6%)

- Relaxation and escape from routine (47.0%)

- Adventure and exploration (39.6%)

British tourists are sustainably minded. Like the German market, they are most interested in choosing local activities to benefit locals (66.6%). They also like to think about their environmental impact when travelling to a destination (51.8%) and while travelling around (49.7%).

France

France has a population of around 67 million. Its economy is highly developed and diverse. It is the second-largest in the EU after Germany. According to the European Commission, economic activity in France will slow down to 0.7% in 2025 and grow by 0.9% in 2026. It is predicted to rise to 1.3 % in 2026. [NG5] Like the rest of Europe, French nationals are also experiencing a cost-of-living crisis and high inflation.

French outbound travel market

The French made 37.9 million outbound trips in 2024, spending US$54.0 billion. CBI research found that in 2024, French tourists spent an average of €1,407.52 per trip or €133.34 per night. The French outbound travel market was estimated at US$72.9 billion in 2025. It is projected to reach US$124 million by 2034 – a CAGR of 5.4%. The French prefer to travel within their own country, and around 25% choose to travel abroad.

Outside of Europe, Africa is a popular continent for travel among French nationals. Morocco was the most popular destination for French tourists, along with Tunisia and Egypt. Historical ties and the French language are some of the reasons for this choice of destination among French nationals. Countries with a history of speaking French are more common options for French outbound tourists.

France is the most important source market for West Africa as a region, based on UN Tourism data. In 2024, 47% of all tourist arrivals to Senegal were from France. Madagascar was another important destination. In 2023, there were 96,943 French visitors to the country – 37.4% of all tourist arrivals.

French travel trade

The French travel trade is large and complex. There are about 4,800 travel agencies in France. There are also many independent tour operators specialising in adventure tourism around the world. Retail agency networks include Selectour, Havas Voyages and Prêt à Partir. Most businesses are in Paris. All businesses that offer travel services must be registered with Atout France, the France Tourism Development Agency.

Tour operators include Voyageurs du Monde, Voyages d’Exception and Continents Insolites. You can find listings of French tour operators online, like this one on Les Entreprises du Voyage (EDV). You can also find information about the tour operator market through the French tour operator association, SETO.

France hosts several annual travel trade fairs, including IFTM Top Resa for the international and French markets, organised every September. The ILTM targets international and French luxury travel suppliers and buyers.

French travel behaviour

According to CBI research, French outbound travellers spent an average of 10.6 nights in 2024. By share, France was the top-spending market on activities (14.6%) and shopping (12.3%). Accommodation accounted for more than one-third (37.1%), and food and drink for 22.6%.

Source: CBI, 2025

Online booking platforms are the preferred method of research among French travellers. 81.0% of respondents used them either frequently or sometimes. But word of mouth is almost as important to them (71.4%). This shows how important good reviews are. French people also like to use websites and guide books. For booking, online platforms are also the preferred method for services and experiences. But French travellers also like to book directly with providers or use retail agencies.

French characteristics and travel motivations

French tourists especially value the natural environment of a destination. Off-the-beaten-track destinations are becoming more popular. Cultural offerings are very important to French tourists, and so are sites of religious importance.

The French are known for their independent nature. Many French tourists like to make their own decisions and prefer to travel individually rather than as part of a group. Travelling solo is relatively popular among the French population. The French are more formal and demanding of respect. They often speak English less well than other nations. If you can speak to them in French it will be appreciated. Reassurance about health and safety precautions are important for French holiday choices and decision-making.

Other motivations that are important to French travellers include:

- Relaxation and escape from routine (45.5%);

- Being immersed in local cultures and people (44.6%);

- Spending time with friends and family (43.7%).

Like other European markets, sustainability is becoming a way of life. Choosing local activities while on holiday was the most popular sustainability action for French respondents. Almost two-thirds (63.5%) said it was either very important or important.

According to EU research in 2021, almost half of French people (48%) feel that sustainably certified accommodations are important. Individually, French tourists are more often deciding to travel less but stay longer. They might also make different travel choices – like taking the train instead of flying. They also have a strong preference to:

- Eat locally sourced products while on holiday (52%);

- Take steps to reduce waste while on holiday (45%);

- Know that more of their money directly benefits local communities (39%);

- Take holidays outside of the main tourist season (39%).

Italy

Italy has a population of around 59 million. Its economy is the eighth-largest in the world and the third-largest in the eurozone. Italy is an advanced country, although economic growth is weak and there are long-term challenges around high public debt and an older workforce. GDP is projected to grow by around 0.5% in 2025.

Italy’s standard of living is high by global standards. But income growth is slow and there are regional gaps between the richer north and poorer south. Most Italians are well-educated and often speak English at a good level. But they appreciate information being made available in Italian.

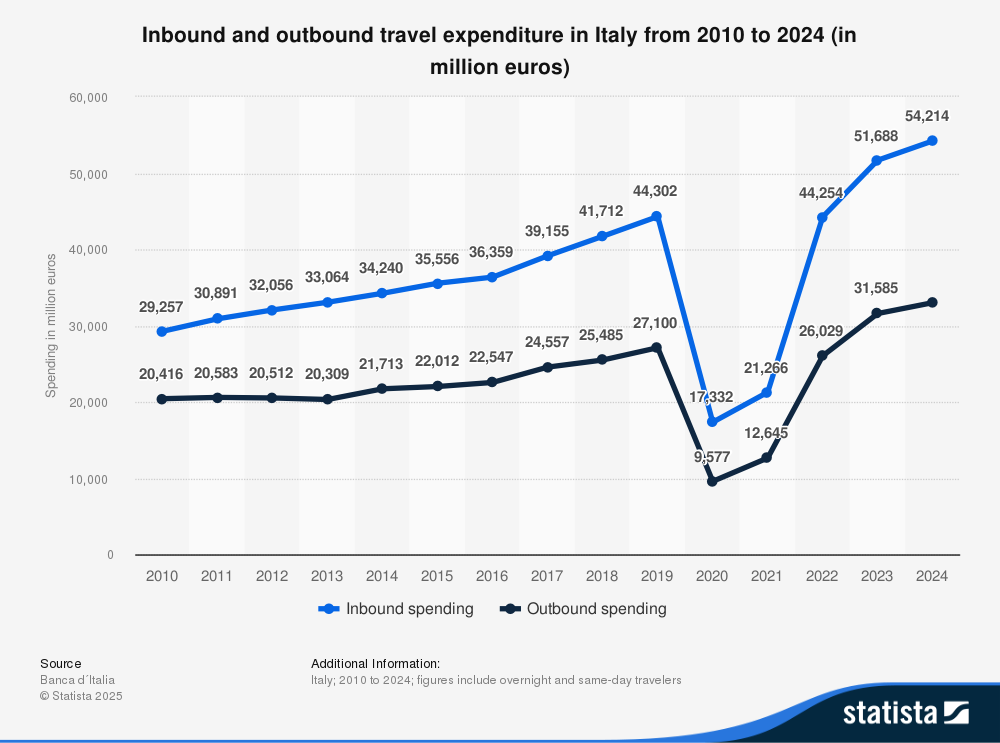

Italian outbound travel market

Italian outbound travellers – overnight and day visitors – made 34.6 million outbound trips in 2024. They spent €33 billion, up 4.5% from 2023. Outbound expenditure has been rising since the end of the pandemic and is now 50.4% higher than spending reported in 2019.

Figure 14: Inbound and outbound travel expenditure from Italy, 2010-2024

Source: Banco d’Italia, Statista, 2025

Europe made up 87.1% of outbound travel in 2024. Outside of Europe, Asia was the most popular region for Italian outbound travellers in both 2023 and 2024, with 2024 arrivals increasing by 4.7%. In 2024, arrivals to Africa went up by more than one-quarter (26.2%) and spending in the continent by over 35.8%.

Italians stay the longest in the Caribbean and the Central and South American regions (13.9 nights), and the shortest in Africa (10.8). This is probably because it is relatively easy to reach the popular North African countries (Morocco, Egypt, Tunisia). These are the most popular destinations for Italian travellers.

Table 5: Outbound tourism from Italy, 2023-2024

| Continent visited | Traveller numbers (millions) | % Change 2023-2024 | Expenditure (€ millions) | % Change 2023-2024 | Average length of stay | |||

|---|---|---|---|---|---|---|---|---|

| 2023 | 2024 | 2023 | 2024 | 2023 | 2024 | |||

| Caribbean, Central & South America | 1.0 | 1.1 | 7.9% | 1,566 | 1,601 | 2.3% | 13.6 | 13.9 |

| Asia | 2.2 | 2.3 | 4.7% | 3,661 | 4,275 | 16.8% | 12.5 | 11.5 |

| Oceania | 0.7 | 0.7 | -0.4% | 1,408 | 1,527 | 8.4% | 11.7 | 11.9 |

| Africa | 0.6 | 0.7 | 26.2% | 527 | 715 | 35.8% | 9.6 | 10.8 |

Source: Banco d’Italia, 2025

Other popular destinations for Italian tourists are Madagascar, Indonesia, Jordan, Vietnam and South Africa.

Italian travel trade

Italy’s travel trade is large and mixed, with around 9,000-10,000 registered agencies and operators. Most are based in northern and central Italy, where incomes and travel demand are higher. The market is worth about €10 billion a year, and online sales have grown quickly since the pandemic. Many Italians still use travel agents for long-haul trips or complex holidays. But online booking and digital platforms are now a big part of the business.

OTAs are well-established in the market. Italian consumers especially like to use Booking.com, Expedia, Lastminute.com and eDreams. One of the largest tour operators in Italy is Alpitour. It has a turnover 6 times larger than the next biggest player, Gattinoni. Tour operators specialising in travel to developing destinations include The Labyrinth, Yana Viaggi and Viaggi Solidali. The Italian Federturismo Confindustria represents tourism businesses. You can find members in the listing on its website.

BIT Milan is the largest B2B travel trade show in Italy, with more than 2,000 exhibitors and 50,000 visitors. It is organised every year in February.

To find out more about the Italian travel trade and how to work with Italian tour operators, download Visit Britain’s Italy Market Profile.

Italian travel behaviour

Like other markets, especially France, Italians spend the largest share of their travel budget on accommodation and food and drink (34.7% and 24.7% respectively). It is the top-spending market for food and drink. Around 13.0% of budgets is spent on activities. This is the highest among the source markets along with France and Germany.

Italian tourists like to book trips well in advance, sometimes up to 11 months before travelling. They highly value recommendations from friends and family (52%), and use review sites often (41%). They like to do a lot of online research before making decisions. They prefer to book their own travel arrangements using online platforms (85.6%). This percentage is higher than other European countries. Italians are less likely to book package holidays.

Italian characteristics and travel motivations

Italians look for active and cultural trips and want personal discovery, not just relaxation. They like the natural environment and enjoy natural attractions and wildlife experiences. Italians are also very outgoing and like to eat out and socialise. The typical Italian tourist has 1 or more of the following characteristics:

- Older, wealthier Italians will travel at any time of the year;

- Italians like guided tours with Italian-speaking guides;

- Security, high-quality accommodation and good food are important to them;

- Over one-quarter of Italians like to travel outside the high tourist season.

Other motivations include:

- Relaxation and escape from routine (42.7%)

- Being immersed in local cultures and people (42.4%)

- Personal growth and learning new things (39.7%)

Italians are more and more sustainably minded. Very few said that sustainability was not important to them when they travel. Choosing local activities to support locals was more important to them than to other markets (64.2%). As a nation of ‘foodies’, they also want to consume locally sourced produce while on holiday (42%). They prefer to travel outside the high season (27%), which offers good opportunities to attract Italians in low and shoulder seasons.

The Netherlands

The Netherlands is a small country in northwest Europe, with about 18 million people. It has an open, trade-focused economy – one of the largest in Europe. De Nederlandsche Bank predicts steady growth of roughly 1–1.5% a year for the following 2 years (2025-2027). The Dutch enjoy a very high standard of living. But consumer confidence fell sharply after recent price rises and global shocks. As a nation, Dutch people are among the most environmentally aware. Adopting sustainable principles is more common in the Netherlands than in many other European countries.

Dutch outbound travel market

Travel is extremely important to Dutch people. It is estimated that 85% of the population take tourism trips for personal reasons. In 2024 they made 27.3 million outbound trips, spending US$26.7 billion.

Türkiye was the most popular destination for Dutch tourists in 2022. Morocco and Mexico were also popular. Other notable destinations for Dutch tourists both before and after the pandemic included Malaysia, Vietnam, India and Colombia.

Dutch travel trade

The Dutch travel trade is made up of around 3,800 travel agencies, tour operators, and group organisers like schools and associations. While many Dutch nationals book holidays independently, organised trade is still important for packaged and group travel. The industry is large and growing, and travel agencies generated around €25 billion in 2025. Online and digital booking channels dominate, and tour operators are recovering steadily after the pandemic.

Big travel agents include TUI Nederland, Corendon and Sunweb. There are also many adventure tour operators attracting the large market of Dutch adventure tourists, including Vamonos and SNP Natuurreizen. ANVR is the Dutch association of travel agents and tour operators; you can find a list of the 428 members of the association online. Online listings are useful to find tour operators and travel agents, like this one from Kompass.

Vakantiebeurs is a major tourism and leisure fair held in the Dutch city of Utrecht every year, and is part of Dutch Travel Week. It is also important for buyers from the other Benelux countries (Belgium and Luxembourg). It is both B2B (business to business) and B2C (business to consumer) and attracts more than 70,000 visitors for 900 exhibitors.

Dutch travel behaviour

According to Eurostat, 10.2 nights was the average length of stay for Dutch trips abroad. The Dutch spent of €790 per trip on average. Dutch tourists are price-conscious and want good value. Like other European markets, most of the travel budget is spent on accommodation (40.9%). The Dutch also spend more than average on food and drink (23.9%).

When planning a trip, the Dutch rely heavily on word of mouth from friends, colleagues and relatives (53%). They also use their own personal experiences to help shape their decisions (40%). As tech-savvy consumers, Dutch tourists also use websites that collect customer reviews and ratings, like Tripadvisor, to gather information.

Dutch characteristics and travel motivations

Nature and culture are important to Dutch tourists. They are an adventurous market but look for destinations that are less crowded, with good sustainable credentials. Authentic experiences and value for money are also important to them. They value relaxation and the opportunity to get away from the stresses of everyday life.

Many Dutch people speak multiple languages at a good level, especially English. They are interested in other cultures and are careful with their money. They are direct and straightforward in their business dealings, and Dutch tourists behave in a similar way. Dutch tourists are well-organised when it comes to planning their holidays. They often research trips up to 6 months in advance. They are very comfortable using the internet to book their trips. Few Dutch tourists use traditional travel agents to book their trips these days.

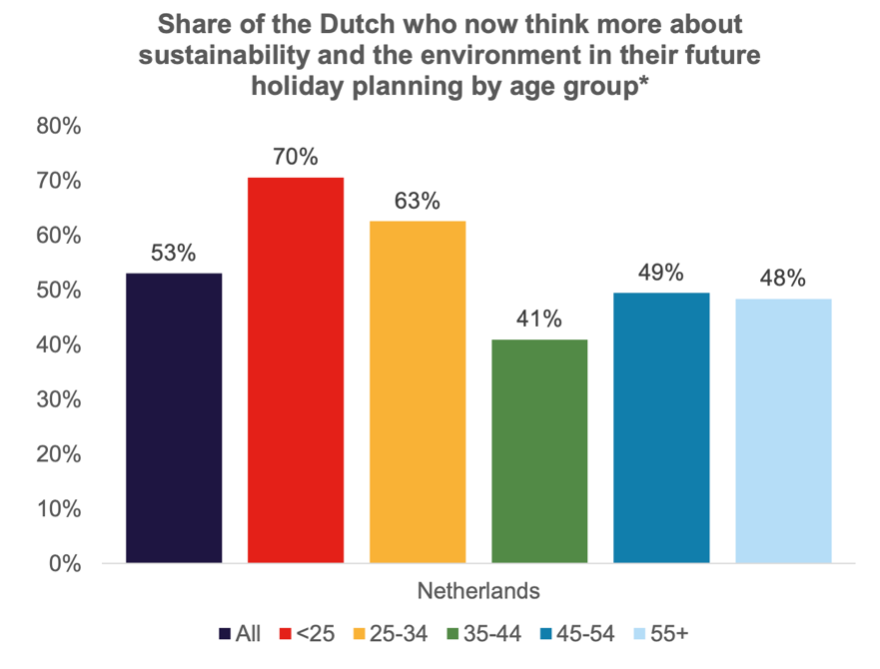

The Dutch are very concerned about the environment and like to travel sustainably. The younger age groups show the strongest intention to change their behaviour when travelling. Actions include using other forms of transport rather than flying and minimising their use of plastic to help the environment. More Dutch people are becoming vegetarians (11% of the population), especially in the younger generation aged 18-24. Destinations with good vegetarian cuisines will be popular choices for conscious consumers.

Figure 17: Importance of sustainability to the Dutch

Source: Visit Britain, 2025

Dutch travellers also like to take in part in local activities that benefit local communities (51.3%). Other EU research found that Dutch tourists like to take practical action to travel sustainably. They aim to:

- Take holidays outside of the high tourist season (45%);

- Eat locally sourced products while on holiday (44%);

- Reduce waste while on holiday (44%);

- Travel to less-visited destinations (43%).

Spain

Spain has a large population (48.8 million) and a well-diversified and resilient economy. It has the fourth-largest economy in the EU. The economy is expected to experience GPD growth of 2.9% in 2025 and 2.3% in 2026. But, like other European consumers, Spanish tourists look for good-value experiences as the cost of living continues to decide how much they spend.

Spanish outbound travel market

Spanish tourists made 19.9 million outbound tourism trips in 2024, spending a total of US$29.3 billion. Spanish-speaking countries are popular outbound destinations for Spanish tourists: Mexico, Colombia, Costa Rica and Chile are among the most visited. But arrivals to these places are still below those achieved in 2019.

Arrivals to Morocco, Türkiye and Egypt all went up in recent years. This probably happened because they are the most convenient destinations. Other destinations that appeal to Spanish tourists are Vietnam, South Africa and Tunisia.

Spanish travel trade

The Spanish travel trade is made up of ‘mayoristas’ (tour operators), ‘mayoristas-minoristas’ (tour operators/retailers) and ‘minoristas’ (retail travel agents). 20% of them are in Madrid and there were around 9,700 businesses in 2020. Personal relationships are very important to Spanish business people, and take time to develop.

The top tour operators in Spain are Travelplan, Tourmundial and Catai Tours. You can find out more about the Spanish travel trade in this Trade Market Profile. CEAV is the Spanish federation of tour operators and travel agents. There is a useful members list on their website.

FITUR (Feria Internacional de Turismo) is the leading international tourism fair in Spain. It is organised every year in January, and aimed at B2B and B2C. The fair attracts lots of visitors (155,000) and exhibitors (9,500+) from over 150 different countries.

Spanish travel behaviour

According to Arival, Spanish travellers’ average length of stay was 7.2 days. This number is lower than the other source markets. They also spent less than other markets – €1,928 per trip. Spanish tourists spend about one-third of their budget on accommodation (36.9%) and a quarter on food and drink (23.8%). This is broadly in line with other European nations.

Source: CBI, 2025

Spanish tourists value recommendations from friends and relatives. They use different online websites to book their trips, including OTAs (online travel agents). Cultural offerings are the most important factor to them, closely followed by nature and price. Spanish tourists like to make their bookings online. They usually plan their trips abroad 1 to 6 months in advance, depending on the destination.

Spanish travel motivations

Beach destinations are the most popular among Spanish outbound tourists (37%), followed by rural/nature destinations (17%). Spaniards also like to join in religious activities. This is probably because many are Catholic and actively take part in religious festivals and ceremonies. Food and drink experiences, CBT and ecotourism are also becoming more popular among Spanish tourists. When choosing a destination, cultural offerings at a destination are the most important factor they consider (44%), along with the natural environment (43%).

Spanish tourists are among the most sustainably minded when they travel. They are very proactive to minimise their impact on destinations. They like to:

- Consume locally sourced products while on holiday (71%);

- Reduce waste while on holiday (68%);

- Take holidays outside of the high tourist season (53%);

- Travel to less-visited destinations (52%);

- Reduce water usage while on holiday (52%);

- Contribute to carbon-offsetting activities (52%).

Tips:

- Use this Visit Britain guide to Understanding the international travel trade to learn how the global travel trade works. You can use it to reach new markets.

- To find out more about European markets, do your own internet research. Many countries’ tourism organisations publish market profiles and consumer insights, like Visit Britain, South Africa Tourism and Tourism Australia. Although the focus is on inbound markets, they can give you valuable information about different nations’ characteristics and motivations.

- Find buyers on the European market using the CBI study 10 tips for finding buyers on the European tourism market.

3. Which tourism products from developing countries are most in demand from European markets?

The top tourism products for European tourists are adventure tourism, community-based tourism, cultural tourism, food tourism, nature tourism and wellness tourism. They are all closely aligned with adventure tourism, the fastest-growing niche in the tourism sector. What these niches have in common is that they offer immersive experiences for tourists. These experiences are a major trend in the market today.

Adventure tourism

Adventure tourism has 3 elements – a physical activity, being outdoors in nature and an immersive cultural experience. There are 2 types of adventure tourism: soft adventure and hard adventure. Soft adventure has the largest number of participants, as activities are often low-risk and require little or no experience. Hard adventure requires more skill and comes with greater personal risk. But adventure trips often include soft and hard adventure activities alongside cultural and nature-based activities.

Europeans are the second-largest group of adventure travellers after North America. They want to explore new landscapes and go on adventures all over the world, especially in developing countries. Germany and the UK are the top markets.

Many Europeans book trips with specialist tour operators like Global Adventures (Germany), KE Adventure Travel (UK) and Voyages d’exception (France). Fully independent travellers (FITs) use OTAs to find adventure experiences. They often book directly with local tour operators and/or local communities. OTAs catering to the adventure market offer multi-day, day or custom tours – some OTAs are Evaneos (France), KimKim (US), Responsible Travel (UK) and Much Better Adventures (UK).

Community-based tourism (CBT)

CBT means community-led tourism experiences where communities own and manage their own tourism programmes. Local communities benefit through economic empowerment and skills development. CBT programmes inspire tourists and promote cross-cultural understanding.

CBT offers especially good opportunities for small communities to enter the tourism market. There are destination leaders in CBT provision, like Costa Rica, Vietnam and India which have been promoting CBT successfully for many years. There are up-and-coming destinations too, like Colombia. This country has emerged from decades of conflict to offer CBT to develop economic self-sufficiency for remote communities and promote peacebuilding.

European CBT tourists are motivated by the ‘feel good factor’ of immersive, cultural experiences and the desire to ‘make a difference’ to local lives. They can be found across all ages and consumer groups. FITs prefer to book directly with communities or through OTAs. Tourists from Spain have the highest preference for CBT, followed by the UK, France and the Netherlands.

European tour operators usually sell CBT as part of wider adventure packages, either scheduled or tailor-made tours. They often work with local CBT organisations of DMOs in the destination. The UK has the largest market for operators that specialise in cultural and adventure trips. Take a look ar Culture Contact, for example. OTAs are also platforms for CBT, and local providers can list their products directly on the platform. Earth Changers is another good British example.

Figure 19: Community homestay in rural Colombia

Source: Acorn Tourism Consulting, 2023

Cultural tourism

Cultural tourism is about travelling to experience and learn about the culture of a country or region. It includes tangible features (built heritage) and intangible features of a destination’s history, and heritage like music, local lifestyles, homestays and the arts.

It is possibly the largest tourism niche in the world today. It crosses over with many other niches, like CBT, urban experiences, religious tourism and food tourism. The market for European cultural tourists is also large, estimated to make up 40% of all European tourism. Tourists from Italy, France and the Netherlands have the greatest interest in cultural tourism. Germany has the largest market of European cultural tourists.

Cultural tourists have specific characteristics. They are usually well-educated and tech-savvy, and are wealthy, active and frequent travellers. They also often stay longer in a destination and spend more per day. They look for personal interactions with local host communities.

Figure 20: Learning about heritage is a major motivation for cultural travel

Source: Lightscape, Unsplash, 2024

The market for European buyers is also large. Most European tour operators offer cultural tourism, for example Window to Travel (UK) and Nomade Aventure (France). Specialist cultural tour operators include Martin Randall (UK) and Envoy Tours (Armenia). OTAs sell many cultural tours ranging from part or full-day sightseeing tours to private guides, cooking classes, guided tours, skip-the-line tickets and major attractions. Withlocals (Netherlands) and Viator (US) are 2 examples.

Food tourism

Food tourism is a very large tourism niche that has become more popular amongst outbound tourists. It is diverse and there are many activities like food festivals, food museums, cooking classes, wine trails and artisan producer visits.

Europeans often choose food experiences as immersive and authentic experiences. Showcasing local cuisines offers lots of opportunities for local operators to develop unique food tourism products. It can also help to stimulate year-round tourism. The European market is estimated to make up 35% of food tourists worldwide. All major European markets want to take part in food experiences.

Figure 21: Food, CBT and agritourism are popular experiences

Source: Acorn Tourism Consulting, 2025

The European market of buyers is a mix of tour operators for longer trips and OTAs for short food experiences. Tour operators usually include food experiences within a broader trip, for example Original Travel (UK) and Essential Escapes (UK). There are fewer specialist food tour operators, like Gourmet on Tour (UK). For short experiences, OTAs are the most common platforms. There are specialist platforms like Traveling Spoon (Netherlands) and Eatwith (US), and larger activity-based OTAs like Viator (US).

Nature tourism

Nature tourism is travel for the purpose of enjoying natural areas and environmentally friendly experiences. These should be sustainable and low-impact, and help protect the natural environment for the long term. Demand for authentic and immersive experiences in natural surroundings is very high on the European market. Germany has the largest market for nature tourists, followed by France and the Netherlands. Ecotourists are often happy to pay more for experiences if they are meaningful and immersive.

European tour operators usually offer different experiences in nature packages, like trekking, cycling, wildlife safaris and birdwatching. Ecotourism experiences are often included in a nature package. Sometimes they are sourced directly, like an ecolodge in a rainforest destination. European tour operators that specialise in nature and ecotourism include Better Places (Netherlands), Positive Impact Tourism (Netherlands), Far and Wild Travel (UK) and ASI Reisen (Germany).

Wellness Tourism

Wellness tourism refers to wellness activities undertaken while on a leisure trip. Worldwide, people are now more interested in their own health and want to stay fit, both physically and mentally. Wellness includes many traditional activities like yoga, meditation, spa treatments, hot springs tourism, eating healthily and staying fit. ‘Feel good’ activities like CBT, walking, cycling and swimming are also seen as wellness, so its includes a lot of things.

Wellness tourists are either primary or secondary. Primary wellness tourists usually stay in all-inclusive wellness resorts that focus on a whole package of wellness. Secondary wellness tourists are a much larger group, making up almost 9 in 10 wellness trips. These tourists take part in wellness activities as part of a wider trip. They are more interested in the cultural link between a destination and wellness remedies that are special to it. This is the group that offers the best opportunities to local tour operators.

Figure 22: Yoga is a popular activity in wellness destination Rishikesh, India

Source: Gokul Gurung, Unsplash, 2023

The European market for wellness is the largest in the world, along with North America. Germany, the UK and France are the most important source markets for wellness tourism. The Netherlands, Spain and Italy are also important markets. Germans are experienced wellness travellers and spending time in nature is important to them. The UK market has a focus on mental wellness and often chooses yoga and meditation retreats. The French are a higher-spending market. When possible, they may travel further to French-speaking countries, like Madagascar.

There are many specialist wellness tourism providers on the European market, like Healing Holidays (UK) and Wellnessurlaub (Germany). OTA platforms like GetYourGuide (Germany) and Musement (Italy) offer wellness trips, tours and experiences. If you want to offer wellness products to Europeans you will need to comply with strict regulations. For example, around health, safety, cleanliness and qualified practitioners. These are key to keeping wellness tourists safe and generate confidence in local operators’ abilities and professionalism.

Tips:

- Find out more about all these tourism niches in the detailed CBI studies listed in Attracting tourists from Europe. Browse all the studies and pay attention to other niche segments and target groups that might be interesting to you.

- Research other trends in the market in the CBI study Which trends offer opportunities or pose threats on the European outbound tourism market?. If you adapt to tourism trends, you will be able to compete more effectively and attract European tourists.

Acorn Tourism Consulting Limited carried out this study on behalf of CBI.

Please read our market information disclaimer.

Disclaimer: The statistics quoted throughout this study come from a range of sources. Because of variations in data collection and presentation methods, figures may not always be directly comparable.

Search

Enter search terms to find market research