Which trends offer opportunities or pose threats on the European outbound tourism market?

Sustainability is the number-1 top trend in tourism today. Regulations around sustainability in tourism are changing in Europe. Suppliers will need to meet these criteria to do business with European businesses. AI in tourism is also transforming the industry for both businesses and consumers.

In the future, growth in tourism will be driven by younger generations – Gen Y and Gen Z. They still want authentic and unique experiences. A wide range of niches have appeared to meet their needs. But the ongoing cost-of-living crisis, along with health and safety concerns as a response to global insecurities, may impact growth.

Contents of this page

- Main trend: tourism sector transformation and sustainability

- AI is transforming the travel industry, both for businesses and consumers

- Demographic trends driving tourism change and growth

- Niche experiences and activity trends present opportunities

- Transformational and experiential travel continues to be popular

- Luxury and wellness evolving as major sustainable tourism trends

- Cost-of-living crisis and concern for personal safety impacting travel decisions

- Learning from trending destinations in 2026

1. Main trend: tourism sector transformation and sustainability

Making sustainability part of how businesses work is transforming all industry sectors. Tourism is responsible for a lot of harmful carbon emissions. Becoming more sustainable is very important and needs to be carried out quickly within the global tourism industry. This is what global travellers, who want to live and travel more sustainably, want. Every year, more and more travellers talk about how important travelling sustainably is to them. The idea of regenerative tourism is becoming more popular.

Sustainability in Tourism

Sustainable development in tourism is defined by the United Nations World Tourism Organisation (UNWTO) as ‘tourism that takes full account of its current and future economic, social and environment impacts, addressing the needs of visitors, the industry, the environment and host communities’.

Making the transition to a sustainable business is now more than just a trend. It has become a pressing and essential task to tackle the climate crisis and meet the commitment to reduce carbon emissions. Tourism is a big contributor to global climate change. Also, the sector is predicted to grow at an average of 6.6% a year between 2023 and 2032. This is around twice as much as the expected growth of the global economy, at 3.0% in 2025 and 3.1% in 2026.

In the meantime, the global commitment across all sectors is to halve emissions by 2030 and reach net zero by 2050. At the moment, national commitments are not good enough to reduce greenhouse gas emissions by this amount. They are projected to be ‑2.6% by 2030 instead of the ‑43% that is needed.

Figure 1: Current shortfall of national plans to reduce greenhouse emissions

Source: United Nations Climate Action, 2025

Sustainability regulations in Europe

Regulations around sustainability in tourism are changing in Europe, and requirements for businesses are becoming stricter.

The EU Sustainability Regulations White Paper 2025, launched by the Global Destination Sustainability Movement (GDS-Movement) and the European Travel Commission (ETC), explains 3 new EU laws. These laws will change how tourism businesses talk about and report sustainability. The new laws are the Corporate Sustainability Reporting Directive (CSRD), the Empowering Consumers for the Green Transition Directive (ECGTD) and the Green Claims Directive (GCD).

Together, they want companies to be honest and clear about their impact on the environment and people. The CSRD asks large companies for standard reporting on their environmental and social actions. It gives smaller businesses a simple, voluntary way to start doing the same.

The ECGTD and GCD are very important for small tourism businesses. They are based around preventing greenwashing. The ECGTD wants to stop companies from using unclear or false green words or phrases like ‘eco-friendly’ or ‘climate-friendly’, unless they can prove them. The GCD adds strict rules on how to check and prove these claims, and bans fake or self-made eco-labels.

Even though very small businesses are not affected right away, they will need to follow these rules sometime in the future. These new laws will help small tourism businesses become more trusted by visitors, by using real evidence, clear communication and approved sustainability certificates.

But in June 2025 it was reported that the GCD is back in the review stage. There is no timeline for implementation.

European people are getting better at being sustainable. Positive attitudes towards sustainability in everyday life are becoming normal. At home, Europeans often recycle and act responsibly where they can. Common actions include saving water, limiting use of natural resources like electricity, walking/cycling or taking public transport, and investing in electric vehicles. This is why it is not surprising that they like to act in the same way when they travel abroad.

The CBI offers a free Corporate Social Responsibility e-learning course. It covers the main CSR themes of climate, decent work, gender and youth. You can register online with the ITC SME Trade Academy.

Stay up to date with these developments, because they will impact your business in the coming years. Bookmark the CBI study What are the requirements for tourism services in the European market? and check it often so you can see any updates as they happen.

Figure 2: The climate is changing

Source: Markus Spike on Unsplash

Regenerative tourism

Regenerative tourism and sustainable tourism are closely linked. Their main aim is to keep the tourism sector going while minimising and reducing harmful effects. Ideally, it should also make a positive impact. Regenerative tourism is about looking after the places where tourism happens, ongoing growth, and helping the living systems that support tourism get stronger.

Even though people have been learning about sustainability for over 30 years, regenerative approaches are still very new and changing all the time. There is no accepted set of practices yet. We know that tourism must meet sustainable goals to survive. But regenerative thinking is something different. It is a new way of thinking that is changing as a response to the many current global crises, like climate change, inequality and biodiversity loss.

From a tourist’s perspective, Booking.com’s Travel & Sustainability Report 2025 found that almost two-thirds (69%) of travellers wanted to leave places they visited better than when they arrived. This fits with the goal. The study also shows that more people than ever before (53%) are now conscious of tourism’s impact on local communities as well as the environment. These findings prove there is a growing market of tourists are very interested sustainable travel where it is readily available.

You can find more details about the concept and practical applications of regenerative tourism in a new study by CBI. It also gives several case study examples of regenerative tourism in practice by small tourism businesses. Check out the study Building regeneration into your tourism business to find out.

Overtourism

Overtourism is still getting negative publicity. It remains a serious problem for many well-known destinations. In 2025, many European cities had anti-tourism protests. In these protests, residents drew attention to the pressures on locals and their way of life as a result of mass tourism. For example, in Barcelona activists sprayed tourists with water pistols to ‘cool down’ runaway tourism. Staff at the world-famous Louvre Museum in Paris staged a walk-out. They said the museum was suffering under the weight of so many tourists every day.

There are many initiatives in place to tackle overtourism. More and more destinations are trying out new things around regulation, technology, targeting new markets and developing infrastructure. There are many initiatives by places like Machu Picchu, the Galapagos Islands and Bhutan, along with European cities like Barcelona, Venice and Dubrovnik.

On the other hand, overtouristed destinations give lesser-known destinations the opportunity to attract visitors who are consciously choosing to avoid overcrowded hotspots. These destinations are sometimes referred to as ‘dupes’. There are some examples in the table below.

Table 1: Dupes – alternative destinations to overtouristed destinations

| Dupe/Alternative Destination | Overtouristed Destination |

|---|---|

Lombok, Indonesia Koh Rong, Cambodia | Bali, Indonesia |

Palawan, Philippines | North and South Malé Atolls, Maldives |

Kuélap, Peru Choquequirao, Peru | Machu Picchu, Peru |

Lake Toba, Northern Sumatra | Hotspots in Java |

Da Nang, Vietnam | Phuket, Thailand |

Luang Prabang, Laos | Chiang Mai, Thailand |

Ladakh, India | Kathmandu/Everest Base Camp, Nepal |

Dagala Thousand Lakes Trek, Bhutan | Northern India/Nepal Trekking Circuits |

Granada, Nicaragua | Cartegena, Colombia |

Namib Desert, Namibia | Kruger Park/Victoria Falls circuits |

Source: Acorn Tourism Consulting, 2025

Recent initiatives to tackle overtourism include:

- From April 2026, Indonesia will be restricting the number of daily visitors to the Komodo National Park, a UNESCO World Heritage Site. The idea is to protect it from overtourism and reduce pressures on the natural environment.

- Like other European coastal cities, by 2030 the French port of Cannes wants ban all cruise ships carrying over 1,300 people. In the meantime, from 2026 it plans to halve the number of very large ships in the harbour and limit the number of daily passengers to 6,000.

- In Greece, international arrivals keep rising unsustainably. So, Greek tourism stakeholders are starting to use a high-value, low-density model (HVLD) on the island of Corfu. It is aimed at wealthy travellers by investing in luxury hospitality. The idea behind this strategy is to preserve Corfu’s natural beauty and historical charm by encouraging longer stays and high spending.

- There are other sustainable strategies to fight against overtourism that many places are starting to use. They include encouraging out-of-season travel, promoting lesser-visited destinations, community-based tourism and ecotourism.

Be aware of the ‘say-do’ gap

The say-do gap in sustainable tourism is the difference between what people say they will do and what they actually do. This happens for many reasons, but cost and convenience are main factors.

Research has been done into the say-do gap to understand consumer perspectives. A study by the World Travel & Tourism Council (WTTC), Bridging the Say-Do Gap, offers help for businesses that want to close the gap. In the study, there are six consumer types. They range from those who rank sustainability very highly to those who are least likely to make a sustainable change.

To bridge the say-do gap, it is important to make it easy to adopt sustainable behaviours. The study offers different actionable recommendations to appeal to most travellers. Examples are highlighting economic and personal benefits, making sustainability hassle-free, and showing that environmental action supports wider benefits. Tour operators must make it easy for consumers to make sustainable choices and provide relevant information. Making your business fully sustainable is one way to do this.

Consumer demand for sustainable travel options rises as attitudes become the norm

There is growing European interest in sustainable travel. Travelling sustainably is becoming more important. This is despite economic uncertainties and high cost of living that is impacting livelihoods. The climate crisis has encouraged people to make more sustainable travel choices. There are many positive intentions behind sustainable travel. Booking.com’s Travel & Sustainability Report 2025 found that:

- Sustainability is important for 84% of travellers.

- Travellers’ own attitudes mean they are changing the way they travel. 39% look for advice on travelling at different times of the year and 36% visit alternative destinations. In 2025, 67% of travellers turned off the air conditioning in their accommodation when they were not there. In 2020, this was only 43%.

- 77% of travellers look for authentic experiences that are representative of local culture.

- 73% want their spending to go back to the local community.

What this means is that, despite the say-do gap, you should work sustainably as much as you can. You should also always explain what you do and how you measure your impact.

Get certified as a sustainable tourism business

Under the European Green Deal, European tour operators and other tourism service providers must put sustainable practices in place into their businesses. This is required to meet the commitment to reduce carbon emissions to net zero by 2050. Some European buyers will only work with businesses that are certified as sustainable. It will help you if you can become a certified business. European tour operators often use these schemes: Travelife for Tour Operators, the Good Travel Seal and TourCert. Other schemes that appeal to environmentally conscious European travellers are Green Globe and Earthcheck. Some tour operators are choosing to become B Corp Certified as a coalition of certified companies.

GSTC scheme is changing

There are lots of certification schemes on the market. Many conform to the criteria established by the Global Sustainable Tourism Council (GSTC). But in 2025 the GSTC changed its system to make it more exact and easier for everyone to understand. It is now only possible to be GSTC-certified if you use a certification body that is GSTC-accredited.

These changes help travellers and tourism businesses know which sustainability certificates are real and reliable. But it does mean many businesses that were GTSC-recognised (like Travelife) are no longer GTSC-certified.

Still, the GSTC standards are the backbone of global tourism sustainability actions and they should be the basis for your own actions.

Good Travel Scan

A good starting point is the Good Travel Scan. It is especially aimed at small businesses and family-run enterprises to help them be more sustainable. It starts with a self-assessment survey with 27 questions based on the GSTC criteria. If their results are 50% or more, businesses can apply for Green Destinations Good Travel Scan recognition and be included in the Good Travel Guide.

Understand the benefits of certification

- Increased sales. European buyers are more likely to want to do business with you if you are certified. A study found that 66% of global consumers are happy to pay more for products and services from companies that are committed to social and environmental responsibility.

- Improved reputation. European buyers can trust that your claims are true. Official certification adds credibility to your sustainability actions. It reassures tourists that you care about the environment and local communities and that you are not greenwashing.

- Reduced costs. Operating your business sustainably can lead to financial savings in energy, water use and waste.

- Increased employee satisfaction. Employees are more likely to be engaged and productive when your team has a shared goal and commitment, working together to make a meaningful contribution.

What does this mean for SMEs?

For SMEs, getting the most benefits out of responsible tourism and having the least harmful impacts are essential for sustainable and regenerative tourism. Be very clear about sustainable actions and the benefits to locals and the environment. This is important for effective marketing, management and long-term sustainability of tourism products.

There are many successful sustainable and regenerative tourism programmes on the market today that serve as best-practice case studies. Have a look at these initiatives to see how your business compares:

- Mdumbi Backpackers, sustainable hostel in South Africa;

- Long-term conservation at Singita Kwitonda Lodge, Rwanda;

- LAK Tented Camp, Vietnam, created to preserve cultural integrity and environmental protection;

- Global Himalayan Expedition, India, clean energy impact expeditions to support remote Himalayan communities;

- KARA-TUNGA Tours, a social enterprise in Uganda, all tours benefit and involve the local communities.

Looking ahead: sustainable tourism

By 2030, the tourism industry will be focused on giving back more than it takes. It will also want to help nature recover, support locals and protect culture. Sustainable tourism is changing fast and many actions are expected to become standard:

- More tourism enterprises will have sustainability at the core of their businesses. These include hotels, transport companies and tour operators. Reporting will be transparent and honest – business success will depend upon it.

- Technology will be essential to ensure sustainability. It can help with things like managing visitor numbers, protecting busy areas, and sharing real-time data about sustainability.

- Green fuels like biofuels will change the air and cruise sectors. Other sustainable travel options like electric vehicles and train travel will be more affordable and easily available.

- Sustainable accommodation choices like ecolodges and community homestays will be very popular and more common. This is because these are ways to support local communities and preserve nature and environments.

- The luxury and wellness market will be defined by sustainability. High-value, low-density tourism models will grow.

- Tourists themselves will have a positive impact on a destination through their choices. CBT (community-based tourism) and volunteering, enjoying authentic slow travel, staying locally and for longer, and participating in meaningful interactions with local people and places will be popular options for eco-conscious tourists.

2. AI is transforming the travel industry, both for businesses and consumers

Artificial intelligence (AI) is transforming the global travel industry fast. It is now becoming an everyday tool for both travel companies and consumers. The trend shows a strong shift towards using AI to plan, manage and experience travel more efficiently. It also helps businesses compete more effectively in a digital world. Businesses across the tourism sector are using it to streamline operations, improve marketing and offer more personalised experiences.

This growing use of AI shows a clear trend: travel is becoming more data-driven and experience-focused. Businesses know that travellers expect immediate answers, relevant recommendations and seamless digital journeys. AI makes all of this possible by combining automation with personalisation.

How businesses are adopting AI

Many travel companies are starting small. They experiment with AI in specific areas before expanding. Chatbots and virtual assistants are now common on hotel and tour operator websites. Their big benefit is that they offer real-time answers to customer questions. AI is used to create social media posts, blog content and promotional videos in several languages. This can help reach international audiences.

Behind the scenes, AI supports customer relationship management. It does so by analysing data to predict what travellers will want next. AI can look at the best time to contact a client and suggest personalised offers. It can even detect market trends earlier than manual research could.

The rise of generative AI, or gen AI, is creating new marketing opportunities as well. Companies used to compete for visibility on search engines. Now they now need to make sure their offers can be found by AI assistants and travel chatbots that come up with recommendations. This shift is encouraging businesses to rethink how they present their destinations and products online.

How consumers are using AI

Travellers are also becoming active users of AI. Instead of browsing many websites, they are asking AI-powered assistants to suggest itineraries, compare destinations or find deals. Tools like ChatGPT, Gemini and Layla can plan entire trips. They can combine flight options, accommodations and attractions in seconds. This means consumers expect faster and more personalised advice than ever before. As AI assistants become more accurate, they are influencing how people make decisions.

For travel companies, this means both a challenge and an opportunity. The more visible and well-described their offers are, the higher the chance that AI systems will discover and recommend them. But it is clear that platforms like ChatGPT and Gemini continue to feature overtouristed places. This is because there is lot of information about them already on the internet. It is important – and an opportunity – to make sure lesser-visited places are also widely promoted online so that AI can find them.

To help you as you market your products and to think about how AI will discover you, read the blog How AI Prompts Can Help Discover Hidden, Off-Season Experiences.

CBI has created a series of AI Tourism Content Creation YouTube videos and tutorials to help you build AI knowledge and skills: Basics, Research & Planning, Itinerary Improvement, Blogging & Traffic, Social Media and Email Marketing.

The importance of balancing innovation and trust

While the benefits of AI are clear, businesses must manage its use carefully. Poor data quality, lack of transparency or relying too much on automation can lead to errors or loss of customer trust. Human oversight and management remains essential, especially when dealing with complex travel arrangements or personal information.

Looking ahead

The trend towards AI in tourism is expected to grow rapidly in the coming years. Businesses that start using it thoughtfully, combining technology with human creativity and service, will be in the best position to attract modern travellers. AI is not replacing people in tourism. It is helping businesses to deliver smarter, faster and more personalised travel experiences. The future of travel will be shaped more and more by how well both businesses and consumers use AI to explore the world.

Key insight

AI can collect data, write messages and create content, and make travel suggestions very quickly. But it cannot replace human understanding, empathy, knowledge and experience. AI works best when people guide it. So, make sure that whenever you use AI, you work with the information it produces and make it your own.

You must also be aware that guidelines around the use of AI are always changing. Bookmark the page of the EU Artificial Intelligence Act, with up-to-date developments and analyses of the EU AI Act.

Tips:

- You need to digitalise your business. If you do not embrace digitalisation or explore what AI can do for you, you will find it difficult to grow in a competitive market.

- Look at some of the gen AI tools and see what you can use to add value to your business. Some are free to use.

- Add a chatbot to your website – it is easy to do so. Ask your website developer to help you. Most online website builders offer this functionality. Use this step-by-step guide to help you.

- Use the CBI studies Concrete tips for using AI in the tourism sector and How to prepare your tourism business for AI to help you understand what AI is and how best to use it. They offer lots of advice and useful case studies.

3. Demographic trends driving tourism change and growth

The future of tourism is being shaped by large groups of people with different motivations, behaviours and needs. Understanding each potential target market will be very important to successfully attract these markets.

Gen Z and millennials

The younger generations are still active travellers and will be one of the most important travel groups in the coming years. They will become more independent, wealthy and demanding. Future travel will be shaped by characteristics, motivations and needs that are specific to this large group of young travellers.

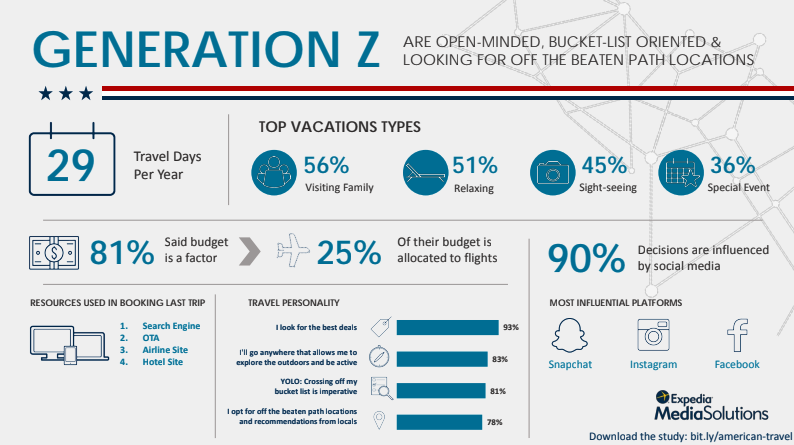

Figure 3: Gen Z travel characteristics

Source: Expedia, 2018

Both groups think travel is more important than things. They know a lot about technology because they grew up with it. They expect instant access to information and value personalisation. These generations widely use digital tools like apps, chatbots and AI planners. Over half of Gen Z use AI tools for travel planning. They are also heavy users of social media channels, especially Instagram, TikTok, YouTube and Facebook. They use these channels for travel inspiration. These platforms are crucial to attract them.

Solo travellers

Solo travel is a growing market among a wide base of adventurous travellers who seek self-discovery, flexibility and freedom. Especially solo female travel is growing and it is estimated that 84% of solo travellers are women. Solo travellers are a good market to focus on as they are spending more on travel than in previous years.

The older market, aged 50+, is also driving growth in solo travel. Life changes like divorce or death, or just being a single person who wants to travel, are feeding the interest. Some solo travellers in this age group leave their partners at home, because they have different travel interests. Health and wellness, cultural immersion and friendships are important to this group.

Growth in this market is also being driven by digital nomads. These are people who work remotely when they travel. Many digital nomads travel alone (43.4%). There are probably over 40 million digital nomads worldwide. Digital nomads are often environmentally friendly. They prefer to slow down and immerse themselves in the local culture rather than move to new places too often. At the moment, most digital nomads are from the US (44%) followed by the UK (7%). Elsewhere in Europe digital nomads come from Germany, France, Netherlands and Spain.

Older travellers

The baby boomer generation (60+) is a group of tourists who are very particular about how they want to travel. They like to travel even if they have more needs. People of this generation are still the wealthiest group of travellers around the world. They are prepared to pay for very special experiences, and often have more time for travel.

Baby boomers want active, authentic and luxury travel experiences. But as they get older, they may need different services around mobility and health concerns. This group may also prefer comfort, safety and high-quality service.

Emerging middle classes in developing markets

Rising incomes among middle-income populations throughout Asia, Latin America and Africa wil start impacting global outbound tourism. The number of middle class households in emerging markets is projected to nearly double over the next 10 years.

These markets have enthusiastic travellers with time and money. China and India are 2 interesting examples of countries with large, mobile middle classes that are very interested in outbound travel and learning about new cultures. Vietnam’s middle class is expected to be one of the fastest-growing markets over the next 5 years.

Even though they probably have different motivations and travel behaviours than the major markets of Europe and North America, they are well worth exploring. On the other hand, the needs of these new markets may come with different challenges, like language.

Looking ahead

There is also the next generation of travellers who will, in time, be the next major consumer group – Gen Alpha. This group is aged 13+ today and is already having an impact on family travel decisions. One survey found that 70% of parents say they consider their Gen Alpha children’s preferences when planning holidays.

They are the first generation to grow up in a world that is completely dominated by smartphones, social media and instant digital connectivity. So, their needs will probably be more demanding that those of their older counterparts, Gen Z.

Build your knowledge about the different markets. Use the CBI studies on baby boomers, Gen Y, Gen Z, solo tourism, the women-only tour market, attracting domestic and regional markets and the accessibility market to identify opportunities to attract specific target groups.

4. Niche experiences and activity trends present opportunities

There are some interesting trends that could present opportunities, depending on your tourism products. They include up-and-coming trends like quiet escapes, cooler destinations and night-time experiences. These trends show a growing desire among travellers for calm, comfort, and meaningful connections with nature and place. Destinations can meet these needs by developing quiet, off-season and after-dark offers that match these motivations.

Quiet-cations/silent travel

Consumers seek time away from the ‘rat race’, busy city life, work and stress. This means there is more demand for quiet places where being alone, peacefulness and quiet can be refreshing. Rather than seeing many sights in a day, quiet travellers slow down. They spend time in nature and engage mindfully with their surroundings. This crosses over with slow tourism and maybe also with a digital detox where people disconnect from their devices. Internet searches for ‘quiet places’ have gone up by 50% over the year.

Example: A 5-day meditation retreat in a quiet space to find peace, at a Buddhist monastery in Lumbini in Nepal. The trip is focused on quiet and spirituality and on learning about Buddhism. There are many activities that people like to take part in on this type of quiet-cation, like yoga, forest bathing, woodland walks, and natural therapies that can attract this type of traveller.

Cool-cations

There is growing evidence that travellers are more often looking for cooler destinations for trips during the summer months. This is driven by 2 motivations – comfort and health (avoiding extreme heat) and novelty and experience (exploring less-visited destinations that offer fresh air, nature and peace). Tour operators are promoting more regions that are traditionally cooler, like Scandinavia or Iceland.

For example, the foothills of mountains and places at higher altitudes have more temperate climates and can offer ‘highland escapes’. Examples are the Andes in South America, or South Highlands in Tanzania. The Mufindi Highlands Lodge in Tanzania states on its website that it has a ‘cool climate through the year. This makes it a reinvigorating escape, regardless of the season’. Promoting your destination as a ‘cool destination’ is a good way to attract visitors who want to travel in more temperate climates, especially in the European summer months.

Shoulder-season travel

Early spring and autumn are becoming popular travel periods for Europeans. This time is often cheaper, less crowded and cooler. This matches the cool-cation trend. Promoting shoulder-season packages is a common sales tactic. There are many advantages to shoulder-season travel. It spreads tourism more evenly throughout the year. It also helps destinations to reach new markets, like older people who can travel outside of school holidays. Accommodation providers can also improve their average occupancy rates.

Example: This trend is often promoted through competitive pricing. If you cater to off-season travellers you should check that other businesses catering to them, like accommodation providers, restaurants, bars and shops, are open too.

Noc-tourism or night tourism

This refers to ‘night-time tourism’. This means travellers want experiences at night rather than during the day. Activities that can be done during the night or at dusk include night safaris and wildlife walks after sunset when animals become active. There is also stargazing and other astronomy experiences (related to darker skies tourism). Other examples are after-dark city tours, night openings at museums, illuminated architecture, and street food markets at night.

Like shoulder-season travel, for operators it has the benefit of making the day longer. For consumers, it offers benefits like fewer crowds and cooler times of the day. They also get the opportunity to experience a destination’s culture and traditions that are unseen in daylight hours. Interest in dark skies has been growing, and Booking.com research found that 62% wanted to visit darker sky destinations.

Figure 4: Night tours of street food markets are a good way to modify a daytime tour

Source: Vernon Raineil Cenzon on Unsplash, 2019

Examples: There are many opportunities for noc-tourism in places with dark skies and no light pollution. For example, in Namibia the local company Namibia Experience offers different stargazing tours for ‘photographers, serenity seekers and nature lovers’. These tours are accompanied by Astro Guides who can explain the starry universe. Alternatively, an after-dark food tour in Accra, Ghana takes place after dark. This is when the streets and stalls come alive with food, culture and social interaction. So, it gives a different feel than a daytime tour.

Vegan travel

There are rising numbers of vegetarians, flexitarians and vegans across Europe. These have led to more demand for vegan-based travel experiences. There are many reasons for this. The pandemic encouraged healthy eating. People are also becoming more aware of environmental factors around food production. Animal welfare has played a part in encouraging vegetarianism, veganism and flexitarianism as well.

Examples: More vegan or vegetarian food tours can be found on the market. India is a very common destination for this type of tour, as the diet is largely vegetarian. The Lima Vegan Peruvian Food Tour in Artsy Barranco combines vegan food with culture in one of the world’s best-known food destinations.

Looking ahead

To stay competitive, tourism stakeholders need to continue looking for ways to make their products stand out from others on the market. Adding value and interest to any tour is essential to attract the market of curious Gen Y and Gen Z. These travellers are very keen on immersive experiences. Always keep up to date with new trends so you can adapt and develop tourism products to meet their needs.

5. Transformational and experiential travel continues to be popular

Transformational travel is a major trend that has been growing strongly since the end of the pandemic. It focuses on personal growth, self-discovery and transformation. It is about having an experience that is personally fulfilling in all sorts of ways. Transformational travel includes all sorts of concepts. Some concepts are meaningful travel, regenerative travel, volunteering, cultural exchanges, learning a new skill and doing work placements.

It is also about experiential travel. This means going on a trip to immerse oneself in a place. It is about having an authentic experience rather than just visiting a place and ‘looking in’. And it is also about sustainable travel and making strong and positive connections with local people and places.

This type of travel is one of the fastest-growing niche markets. It is driven by developing a demand for unique, authentic experiences that are also transformative. These types of experiences include community-based tourism (CBT). Examples are tours led by indigenous communities; agritourism; and wellness tourism, like focused around traditional therapies like Jamu traditional healing in Indonesia or Curanderismo folk-healing traditions in Mexico.

There are many examples on the market today. The Tomarapi Ecotourist Lodge in Oruro, Bolivia is a community enterprise managed by local Aymara families. They offer guided hiking tours plus accommodations. Coffee tours in Colombia are good examples of agritourism: this 3-day tour offers ‘coffee, chocolate and amazing landscapes’.

Figure 5: In Colombia, agritourism offers immersive experiences

Source: Acorn Tourism Consulting, 2024

Looking ahead

Transformational travel is here to stay, and it will have a big impact on tourism. But there is a growing expectation that to really be transformational, benefits must be real and measurable. That is why sustainability certification will become more common. Industry experts say that communities and local stakeholders will be more in control of decisions about their local destinations and tourism. This will probably support a greater understanding of a destination, its communities and visitors for transformational experiences.

Tips:

- Check your trips for their immersive, authentic and transformative qualities. Make sure to use storytelling in your descriptions to inspire your guests. Storytelling is a powerful way to bring emotion across and showcase unique experiences, culture and history. Use all forms of content – text, images and videos – for the best effect. Read this blog by Trekksoft, Unlocking the power of brand storytelling in the tourism industry, for useful information.

- Include your sustainability credentials in all your marketing. This is becoming more essential every year. European buyers will not do business with you unless you can prove you are a sustainable tourism business.

- Find out more about agritourism and CBT in the CBI studies What opportunities are there on the European agritourism market? and What opportunities are there for community-based tourism from Europe?.

6. Luxury and wellness evolving as major sustainable tourism trends

Luxury and wellness tourism are evolving as big sustainable tourism trends. Modern travellers don't just want indulgence or excess. They look more for experiences that promote physical health, mental wellbeing, and meaningful connections with nature and culture. This shift has led to the rise of destinations offering eco-luxury and wellness-focused experiences. Examples are yoga and meditation retreats in Bali, rainforest spas in Costa Rica and safari lodges in Kenya that blend comfort with conservation.

Figure 6: Wellness and luxury are evolving as a big trend

Source: Jared Rice on Unsplash, 2020

For tourism operators in developing countries, this trend offers good opportunities. Wellness-oriented products like natural hot spring resorts, traditional healing experiences and eco-friendly boutique accommodations are becoming more common these days. They usually attract high-value travellers who often stay longer and spend more. From a sustainability perspective, locally managed businesses employ local people and invest in sustainable infrastructure. They should also support preservation of cultural and natural heritage.

Looking ahead

Luxury and wellness tourism is expected to evolve even further as travellers become more conscious of their impact on the planet and their personal wellbeing. Combining technology, personalised wellness programmes and regenerative tourism practices will probably shape the next phase of this trend. For developing destinations, embracing these innovations can put them in a good position for sustainable, high-value tourism. They can offer experiences that feed both people and the planet.

Find out more about the luxury and wellness tourism niche markets in the CBI studies What are the opportunities for luxury tourism from Europe? and What are the opportunities on the European wellness tourism market?.

7. Cost-of-living crisis and concern for personal safety impacting travel decisions

The ongoing cost-of-living crisis that still has an impact on most of Europe is affecting travel decisions. Prices are still high and 93% of European say they are ‘worried about making ends meet’. This means that travellers are actively cutting costs and looking for cheaper accommodations or better-value trips and tours. Searches for ‘free things to do’ have gone up. Searches for ‘dupes’ (see the above section on the 'Main trend') have also gone up as travellers look for cheaper places to visit.

Global insecurities are also having an impact on travellers’ perception and decisions. The ongoing war in Ukraine, political tensions in Eastern Europe and the conflict in the Middle East are still a main cause for worry for the travelling public. Tourists are excited to travel. But they are now more careful about where they choose to go so they can be sure of their safety. Post-pandemic, health remains an issue for tourists too.

Digitalisation and contactless systems have helped transform the tourism industry. They are improving security, addressing hygiene and offering convenience. Contactless payments reduce the need to handle cash or touch payment machines. This lowers the chances of passing on viruses or diseases. In hotels, mobile check-ins and check-outs and smart key cards speed up processes for visitors and help with health concerns.

Facial recognition at airports also improves security. QR codes in restaurants, so diners can see the menu on their phone are being used more often. The ease of contactless systems has become a ‘must-have’ for many consumer groups, especially Gen Y and Gen Z. Older consumers enjoy these conveniences too.

Tour operators can play an important role in reassuring guests by being open and transparent about the risks in their destinations. Having a page on your website to reassure visitors of the measures that are in place to keep them safe is a good idea. Be sure to include all the measures you are taking to reduce the likelihood of contracting Covid-19 or other viruses. For example, having hand sanitisers and masks easily available.

Looking ahead

Travel choices will continue to be price-sensitive for a large group of European outbound travellers for some time to come. Also, in these globally uncertain days the need for strong safety and security measures is now the new normal, and this will continue well into the future. Contactless solutions will keep changing to become ever more efficient, convenient and safe.

Tips:

- Take a good look at the value of your tourism product and make sure you are delivering what you promise. Offer discounts in shoulder season or off-peak times if you can, or early-bird discounts.

- Understand all the risk factors in your destination, including safety, security and medical risks. If you do not already have one, put together a risk management policy. The CBI study How to manage risks in tourism will help you do this.

- Make sure you have a page on your website that clearly explains your safety and security measures. Be very clear about what you do to keep people safe. This will help you gain their trust.

8. Learning from trending destinations in 2026

Many trending destinations have natural landscapes, activities and experiences which look set to match travellers’ demand for experiential and authentic experiences and new niches like ‘dupe’ destinations, quiet-cations and cool-cations. If you research what is working well in other destinations, you can learn from that and adjust or adapt your own tourism product to take advantage of current trends.

Table 2: Emerging adventure destinations around the world in 2025

| Emerging Destination | Description |

|---|---|

| El Salvador | El Salvador is attracting more attention today as a lesser-visited country in Central America. Ruta de las Flores is a scenic hiking trail in the highlands. Its name means Flower Route, because of the beautiful wildflowers that appear in the spring. The route connects 5 cobblestoned towns, so that visitors can immerse themselves in the unique Salvadorian culture. There are grand churches, locally grown and harvested coffee, and bustling local life. |

| Guyana | Guyana has long been a destination for the most adventurous tourists. It also has a very good reputation for sustainability. Tourism development is focused on supporting remote community economies and biodiversity conservation. In dense tropical rainforest, adventure tourists can birdwatch, fish (catch-and-release) in Amerindian villages. They can also abseil down Kaieteur Falls, the world’s highest single-drop waterfall. |

| Kyrgyzstan | Kyrgyzstan is known for its dramatic alpine scenery, glacial lakes, and strong nomadic culture and CBT initiatives. Hiking is a key activity, as over 90% of the country is mountainous. Launched in 2024, the long-distance Kyrgyz Nomad Trail is the longest hiking trail in Central Asia. It was recently expanded by 1,000 km to lesser-visited areas. |

| Malawi | Malawi is getting more attention from travellers looking for an African destination that is less travelled and more authentic. It has a variety of landscapes, including the huge Lake Malawi, forests, high plateaus and game reserves. Several reserves have been restored, improving the quality of big-game safaris. Tourism stakeholders are promoting the HVLD model, and a recent Tourism Act aims to raise quality of the tourism experience rather than increase visitor numbers unsustainably. |

| Mongolia | Mongolia’s wide-open landscapes, nomadic culture and trekking opportunities are becoming more attractive to those looking for remote, off-the-grid adventures. It is another destination known for CBT experiences. Tourists spend nights in traditional yurts with views of snow-capped mountains. It is one of the least populated countries in the world. This makes the country appealing to those who are looking for experiential, authentic travel experiences. The government has an ambitious plan to boost tourism to 10% of GDP by 2030. It is also attracting a new market from the USA. |

| Paraguay | Paraguay is a considerably lesser-visited country in South America. But interest in this country with small colonial towns, lush and wild nature, and a rich cultural indigenous and Spanish heritage is growing. Access to the country is also improving. Paraguay still has a slower pace of travel and offers authenticity. In November 2025, the country launched a new campaign to attract visitors in the 2025-2026 season. They used the slogan ‘Cordillera shines with its culture, nature and tradition’.

|

| Saudi Arabia | Over the past few years Saudi Arabia has been transforming its tourism sector as part of plans to diversify the economy away from oil. It has been investing a lot in leisure, culture, nature and luxury tourism, developing resorts and islands on the Red Sea. Sustainability is at the basis of all the development, especially in places like Al Ula. This is a major heritage site known for its rock art and stargazing opportunities. The main challenge for Saudi Arabia is to continue managing tourism growth sustainably. The idea is to reduce pressure on the environment and nature, especially the mega projects. |

| Sierra Leone | Sierra Leone has come out of decades of various conflicts and has worked hard to improve its reputation. The country has many natural assets, like beaches, rainforests, national parks, and adventure activities. Tiwai Island is a wildlife sanctuary that has just been designated Sierra Leone’s first UNESCO World Heritage Site. |

Source: Acorn Tourism Consulting, 2025

Acorn Tourism Consulting Limited carried out this study on behalf of CBI.

Please read our market information disclaimer.

Search

Enter search terms to find market research

Do you have questions about this research?

In 2026, travellers expect experiences that reflect who they are and what they need in that moment. Companies that design flexible, value-driven and personalised offerings will stand out in a market where meaning matters more than mass.

Isabel Mosk, Tourism Strategist at Sherpa’s Stories