What is the demand for cocoa on the European market?

Europe is the largest importer of cocoa beans, paste, butter and powder in the world. It is also an important trade hub for cocoa and chocolate. Market demand for certified and sustainable cocoa is high. New EU regulations such as the Regulation on Deforestation-free Products (EUDR) will have a major impact on cocoa supply chains. Inflation, rising cost of living and rising prices of cocoa are reducing demand short-term. An unstable cocoa market is boosting uncertainty and making the market unpredictable.

Contents of this page

1. What makes Europe an interesting market for cocoa?

The European chocolate market was valued at $49.3 billion in 2025 (€42 billion). This was followed by North America at $34.7 billion (€30 billion) and Asia-Pacific at $19.1 billion (€16 billion). In 2024, Europe accounted for 48% of global chocolate consumption. This strong demand positions Europe as the world’s largest importer of cocoa beans and cocoa products. Demand for certified cocoa is high, and the premium/organic segment is growing too.

This study includes data for the European Union (EU) and for Europe as a whole. When Europe is mentioned, it applies to all European countries, including non-EU countries like Switzerland, the United Kingdom (UK) and Norway. When the EU is mentioned, it only applies to EU countries.

Europe is the world’s largest importer of cocoa beans

All cocoa is produced outside Europe, and almost all cocoa comes from countries on the OECD-DAC list. Europe imports most of its cocoa as cocoa beans. In 2024, the European cocoa market was valued at $9.4 billion (€8 billion). This figure does not include final product value and non-cocoa ingredients in chocolate. The EU is the world’s largest importer of cocoa beans, with 58% of global imports.

Total imports from producing countries were around 2 million tonnes in 2018 and 2019 but dropped to 1.7 million tonnes in 2020. They slowly climbed again since then to 1.8 million tonnes in 2024 (based on Eurostat and Trade Map data).

The drop from 2018-2019 levels was partially due to increased processing of cocoa beans in West Africa. Here, more beans were being processed locally and exported as semi-finished products like paste, butter and powder. European imports of paste and butter have both increased. Read more about this in the section on Europe's high demand for certified cocoa.

Cocoa bean exports were also affected by market conditions. Global production decreased a lot in 2023, especially in Côte d’Ivoire and Ghana. The price of cocoa rose from €2,000-3,000 in 2023 to €7,000-10,000 per ton in 2024-2025. This had a large impact on cocoa trade. Read more about this in the trends section.

Source: Eurostat and Trade Map 2025

Around 90% of all cocoa exported to Europe is bulk cocoa. Bulk cocoa is cocoa of low or standard quality and is traded in large volumes. The main supplying countries are Côte d’Ivoire, Nigeria, Ghana and Cameroon. European importers mainly focus on the import of bulk cocoa beans and products. For more information see the CBI study Exporting bulk cocoa to Europe.

Figure 2: Cocoa beans drying

Source: Rainforest Alliance

Many of the largest trade hubs are in Europe

Many of the world’s largest cocoa trading hubs are in Europe. The biggest hubs are the Port of Amsterdam in the Netherlands, the port of Antwerp Bruges in Belgium, the Port of Hamburg and Port of Bremen in Germany, and the HAROPA port in France. Other important cocoa hubs are Spain (mainly through the Port of Barcelona and the Port of Valencia), ports in Italy (Genoa, Vado Ligure and La Spezia) and the UK (mainly through the Port of Liverpool and Port of Hull). Switzerland is an important global hub for cocoa trading, but a lot of the trading is administrative rather than physical.

The port of Amsterdam is the largest cocoa cluster in the world. In 2024, the Netherlands was responsible for 50% of Europe’s total cocoa bean imports. The port also stores 600,000 tonnes of cocoa. Belgium followed with 17%, Germany with 8%, and Spain, Italy and France with 5% each. Together with the UK and Switzerland, these countries account for 97% of all cocoa bean imports from producing countries. This makes them most important targets for exporters that want to export cocoa beans to Europe.

When cocoa beans arrive in Europe, they are either processed in the import country or exported to other European countries for processing. The Netherlands and Belgium are the main hubs for cocoa bean re-export in Europe. In 2024, Belgium re-exported 53% of total bean imports, the Netherlands 18%, and France 18%. Together, they are responsible for 89% of all re-exported cocoa beans within Europe.

Source: Eurostat and Trade Map 2025

Europe leads the world in cocoa grinding

Europe is the world’s largest grinder, responsible for 1,750,000 tonnes in 2023-2024. This was 36% of global cocoa grinding. Asia & Oceania was next with 1,103,000 tonnes (23%). They are followed by Africa with 1,074,000 tonnes (22%) and the Americas with 891,000 tonnes (19%).

Producing countries are expanding their grinding capacity. In 2015, Côte d’Ivoire overtook the Netherlands as the world’s largest grinder. Côte d’Ivoire introduced financial incentives in 2017 to attract multinationals to invest in local processing. It is planning to further increase its grinding capacity. The goal of these investments was to increase value addition locally and make the economy less vulnerable to global market fluctuations.

As a result, some grinding is shifting from consuming countries to producing countries. Grinding in Europe decreased by 3% per year from 2020 to 2025, while origin grinding remained steady. Many multinationals have expanded their grinding operations in producing countries, especially in Côte d’Ivoire. However, the tax benefits stopped in 2023. This decision could make local grinding less attractive to multinationals in the future.

Current market conditions have impacted origin grinding. From 2022-2023 to 2023-2024, cocoa production in Côte d’Ivoire decreased by 25% and in Ghana by 31%. A larger share of the beans was also needed to fulfil export contracts. This leaves fewer beans for local processing. As a result, grinding in Côte d’Ivoire decreased by 6% and in Ghana by 18% during that time. Other key producing countries like Brazil decreased by 8% and Indonesia by 5%.

European grinding also started to feel the impact in 2025. Grinding was down at the end of 2024 and during the first half of 2025 compared to previous years. High prices and supply challenges are expected to continue to impact cocoa grinding in Europe and globally.

Although local grinding adds value, it doesn’t always directly benefit cocoa farmers. However, exporters could capture more value at origin by processing cocoa before exporting to Europe.

Europe: world’s largest importer of semi-finished cocoa products

Europe is also the world’s largest importer of cocoa paste, butter, powder and chocolate. From 2020 to 2024, paste imports rose from 343,000 to 376,000 tonnes and butter rose from 227,000 tonnes to 291,000 tonnes. Imports of powder decreased from 55,000 tonnes to 36,000 tonnes.

Source: Eurostat and Trade Map 2025

The most important importers are the Netherlands, France, Spain, Germany, the UK and Poland. Together, they were responsible for 96% of all paste, butter and powder imports in 2024 (by total volume). This share has been quite consistent over the past 5 years. For paste, the largest importers were the Netherlands, Spain and France. For butter, the key countries were the Netherlands, Germany and France. The Netherlands was by far the largest powder importer, responsible for 80% of all imports.

For exporters, it is useful to know which countries import paste, butter and powder. These countries are the best targets for your exports. It would also be useful to learn more about the key importers for each country. See the CBI Country fact sheets for more information.

Europe: world’s largest chocolate producer and exporter

Europe is the world’s largest region for chocolate production and export. Many global cocoa and chocolate companies have their headquarters in Europe. Key importers are Barry Callebaut, Ofi, Cargill, Ecom, Cémoi, Touton, Sucden and Puratos.

Europe has many chocolate manufacturers working with different cocoa qualities. Globally, six multinational companies dominate the market for final chocolate products: Nestlé, Mondelez, Mars, Hershey, Lindt & Sprüngli and Ferrero. Except for Hershey, all six multinationals have production plants in Europe. According to the Cocoa Barometer, these six companies accounted for 1.7 million tonnes of cocoa in 2025, which would represent 39% of 2023-2024 cocoa production.

Europe is not a major importer of chocolate. Most of the chocolate consumed in Europe is also made in Europe or is imported from non-producing countries. Côte d’Ivoire (40,200 tonnes), Mexico (1,500 tonnes) and Columbia (1,500 tonnes) were the only producing countries that exported more than 1,000 tonnes of chocolate to Europe in 2025.

The countries with the highest per-capita chocolate consumption are in Europe

Chocolate confectionery is the most common way that cocoa is consumed. A lot of cocoa is also consumed in beverages (such as chocolate milk), but most of the largest cocoa beverage markets are outside Europe. The main markets for chocolate milk are Brazil, Indonesia, USA, Mexico and Spain.

The world’s average chocolate consumption amounts to an estimated 0.9 kg per capita per year. Consumption is much higher for European countries. In 2023, people in Switzerland consumed the most chocolate per capita at 10.9 kg, followed by Estonia (9.0 kg), Germany (8.9 kg), Finland (8.6 kg) and Lithuania (6.9 kg).

Source: Chocosuisse 2025. Switzerland figures from 2024; other country figures from 2023

For exporters of chocolate, countries with high per capita consumption might be attractive targets. However, these countries are less interesting targets for bean or semi-finished product exporters. Most of these volumes enter Europe through the channels described in the previous sections.

Europe has high demand for certified cocoa

Europe is the world’s largest market for certified cocoa. The biggest voluntary sustainability programmes are Rainforest Alliance, Fairtrade International and organic certifications.

Rainforest Alliance

Rainforest Alliance (RA) has the largest certified cocoa programme. In 2024 RA certified 2,338,000 tonnes of cocoa, of which 1,400,000 tonnes was sold as RA-certified. This is almost one-third of estimated global cocoa production in 2023-2024.

Europe is the main market for RA-certified cocoa. The key European importing countries of RA-certified cocoa in 2024 were the Netherlands (397,000 tonnes), Switzerland (317,000 tonnes), France (179,000 tonnes) and the UK (135,000 tonnes). Together, they represented 67% of all Rainforest Alliance imports worldwide. A large share of this cocoa is re-exported to other European countries.

Source: Rainforest Alliance Cocoa Certification Report 2024

Fairtrade International

Fairtrade production and sales have been relatively steady in recent years. 250,000 tonnes of Fairtrade cocoa were sold in 2019. Sales were lower for a few years before recovering again to 255,000 tonnes in 2023. Total Fairtrade cocoa sales in 2023 represented 5% of the estimated global production in 2022-2023.

Europe is also the key market for Fairtrade cocoa. The UK and Germany are the largest markets for Fairtrade cocoa.

Organic

Europe is an attractive market for organic cocoa. However, organic cocoa imports have decreased substantially in recent years. Total organic cocoa bean imports to the EU were 42,000 tonnes in 2024. This is 45% lower than the 76,000 tonnes imported in 2020. Imports of paste, powder and chocolate increased slightly, but total volumes were much smaller than bean imports. See the section about pressure on organic cocoa for more information about the decline.

The Netherlands was the largest EU importer of organic cocoa beans at 20,000 tonnes in 2024. They were followed by Belgium (11,000 tonnes), Italy (8,000 tonnes) and Germany (2,000 tonnes).

Source: TRACES 2025

Specialty cocoa and craft chocolate are small but growing market segments

The premium cocoa segment includes cocoa with superior quality or value. Premium cocoa is often sold with higher price premiums above bulk market prices. Specialty cocoa is part of the premium segment and takes up less than 10% of the market.

Specialty cocoa is often used to make craft or bean-to-bar chocolate. Over the past 20 years, the craft chocolate industry has grown twice as much as the commodity cocoa market. 49% of all craft chocolate companies are in Europe. France, Italy, Germany, Austria, the UK and Switzerland have the most craft chocolate companies. However, the market is still very small, estimated at about 0.2% of the global cocoa market.

Cocoa for bean-to-bar chocolate can come from any origin country that produces high-quality cocoa. While most commodity cocoa comes from central and west Africa, only 4% of craft chocolate bars have West African origins. Bean-to-bar chocolate is more commonly made with cocoa from Latin America.

For more information, see the CBI studies Exporting specialty cocoa to Europe and Exporting bean to bar chocolate to Europe.

Tips:

- Access EU Trade Statistics to analyse European trade dynamics and develop your export strategy. By selecting a country as your reporting country, you will be able to follow developments such as trade flows and changing patterns in imports. See Trademap for import data for non-EU countries.

- Check the websites of the International Cocoa Organisation (ICCO) and the European Cocoa Association for the latest data on grinding in Europe.

- For more information about certification data, see the Rainforest Alliance certification data, Fairtrade cocoa dashboard and EU organic cocoa import data. Read the CBI study Exporting certified cocoa to Europe.

Recent developments significantly impacted cocoa supply and demand

The global cocoa market has changed a lot in the past few years. The cocoa market slowly recovered from the COVID-19 pandemic. However, the market has struggled again in the last few years. Production decreased and cocoa prices rose to historically high levels. Demand was affected by a global rise in consumer prices, inflation rates and trade wars. New EU regulations are further affecting global cocoa supply chains. These and other factors have had a major impact on demand.

There is a supply shortage

Cocoa production has declined considerably in recent years – this drop was largest in Côte d’Ivoire and Ghana. Côte d’Ivoire dropped by 501,000 tonnes and Ghana by 204,000 tonnes compared to the previous season. Together they amount to 98% of the total reduction in global production. In early 2025, there was hope that 2025-2026 would be a better harvest in Ghana and Côte d’Ivoire. But more recent predictions anticipate a 10% decline in the West African harvest of 2025-2026.

Production in West Africa is declining for several reasons. Droughts, fires and the impact of climate change are affecting production. Bad weather conditions and El Niño negatively impacted cocoa yields. Years of underinvestment in cocoa production has prevented farmers from making the necessary investments in their farms. Old trees are dying. In Ghana, illegal mining (galamsey) is destroying cocoa farms and making farms less productive. The swollen shoot virus has infected 31% of total growing land in Ghana. Farmers struggle to get access to loans at affordable rates, which can be as high as 100%. Rising farming and certification costs make cocoa farming unprofitable.

This has led to export issues. For example, in 2023 Côte d’Ivoire stopped selling contracts for cocoa exports for the 2023-24 season due to uncertainty about meeting sales volumes. Ghana changed its financing approach for the first time in 30 years and will not raise a new syndicated loan. In August 2024, the ICCO reported a production deficit of 462,000 tonnes for the 2023-2024 season.

Global supply is expected to remain lower in the short term. However, oversupply is a possibility in the future. Many new farms are being created in response to the higher price of cocoa, especially in Latin America. When these start to supply cocoa in 3-5 years, it may lead to an oversupply of cocoa. If this happens, cocoa prices may collapse again.

Predictions for the coming 1-3 years vary. ICCO predicts that production will recover in the 2025-2026 harvest. Ecuador is increasing production, and the outlook is favourable for West Africa. However, other experts are predicting another year of low production from West Africa. Illegal gold mining, cocoa swollen shoot virus and a general lack of investment continue to affect production. This uncertainty will keep the cocoa market volatile.

Figure 8: Cocoa beans in a European warehouse

Source: Long Run Sustainability

Farmers are still struggling despite higher prices

The price of cocoa rose steeply from $2,000-3,000 per tonne in 2023 to $12,000 per tonne in 2024 and again in early 2025. The futures price has fluctuated between $6,000 and 10,000 since then. Prices came down somewhat in 2025, but are expected to remain high in the short term. With the instability in the market, it is hard to predict the prices long-term. However, some are expecting prices to stabilise somewhere between the early 2023 price and the record-high price of 2024.

While some farmers have benefited from higher prices in the short term, high prices have not addressed structural inequities in the cocoa market. The price was low for many years, and as a result farmers were unable to invest in their farms or even cover basic costs. Most cocoa farmers have not earned a living income for decades. Cocoa farmers in Ghana earn less than half of what they need to sustain themselves and their families. With many farms in poor conditions, farmers could not take advantage of higher prices.

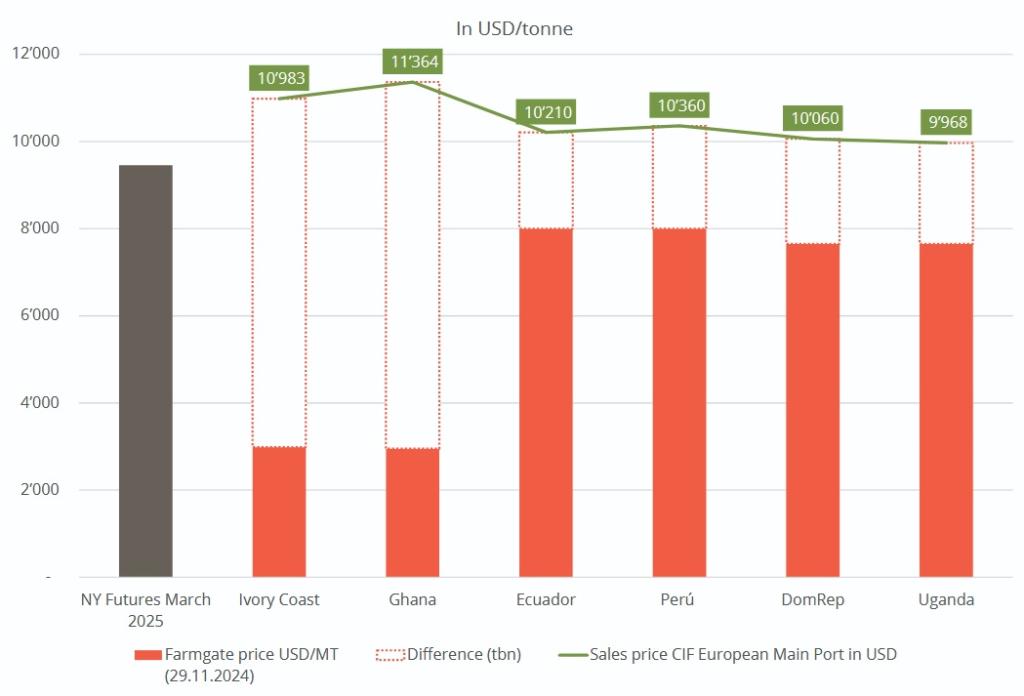

This applies especially to Côte d’Ivoire and Ghana, where prices are regulated. The farmgate price is set based on forward contracts before the start of the cocoa season. As a result, the farmgate price was based on the low historic prices rather than the current high prices.

As a result, farmers were only receiving around 30% of the market price in 2024 compared to up to 90% in Latin America. Farmgate prices rose for the 2025 season for Ghana and Côte d’Ivoire. However, the Ghanaian cedi has lowered in value and the cost of production and labour keeps rising. As a result, the countries and their farmers are still not benefiting fully from higher prices. Farmers could have a short-term advantage if global market prices dropped below the farmgate price. However, lower market prices would cause farmgate prices to decrease again long-term.

Figure 9: Farmgate price and sales price (reference date: 29 November 2024)

Source: SWISSCO Issue brief 2024

The price of chocolate has risen too

With the cost of cocoa climbing, chocolate companies are increasing the price of chocolate. For example, in the UK the price of chocolate confectionery in 2025 was 12% higher than the year before and increased by 27% over 2 years. Mondelez increased the price of Milka chocolate by 48% by making the bars smaller and more expensive. Consumers bought less chocolate as a result. For example, in the Netherlands chocolate Easter egg sales dropped by 12.5%.

The rising cost of living and inflation could cause a shift in demand of European consumers to lower-cost chocolate products. This may reduce demand for organic or specialty cocoa, which already represent only a small share of the market. Demand could shift to commercial, bulk cocoa.

EU regulations influence which cocoa can be shipped to Europe

There are new regulations that could impact the cocoa you export to Europe. The most important ones are the EU Regulation for Deforestation-free Products (EUDR), the EU Corporate Sustainability Due Diligence Directive (CSDDD), the Corporate Sustainability Reporting Directive (CSRD) and the regulation prohibiting products made with forced labour on the EU market.

EUDR

The EUDR entered into force on 30 June 2023. Companies must comply with the regulation by 30 December 2025. Micro and small enterprises (MSEs) will have until June 2026. From this date onwards, cocoa can only be placed on the EU market if it is deforestation-free, legal, and covered by a due diligence statement. Deforestation-free means that land used for cocoa production has not undergone deforestation after 31 December 2020. However, the EUDR may be delayed by a year. For more information, see our study Tips to become EUDR-compliant in cocoa.

The EUDR could put further pressure supply. Not all cocoa will be EUDR-compliant, and this cocoa cannot be exported to the EU. If exporters do not have the necessary data and evidence, it will be difficult to sell cocoa to the EU once the EUDR is in effect. Trade flows may change as compliant cocoa starts to flow to the EU and non-compliant cocoa to other markets. It is not clear yet how much cocoa will be compliant.

CSDDD

The CSDDD requires companies to identify and address their adverse human rights and environmental impacts. This applies both inside and outside Europe. EU member states have until 26 July 2026 to transpose CSDDD’s requirements into national law.

The CSDDD targets large EU companies with over 1,000 employees and over €450 million turnover worldwide. Non–EU companies with over €450 million turnover in the EU are also in range. SMEs are not covered by the CSDDD.

Exporters that do not meet these requirements are not targeted by the CSDDD, but your customers in the EU can ask for data or information to help them comply. Although the impact is not yet clear, it is important for exporters to prepare for the CSDDD. See the CBI study 9 tips to become more socially responsible in the cocoa sector for more details.

CSRD

The CSRD encourages accountability and transparency. Companies must provide information on social and environmental risks and on the impact of their activities on people and the environment. The CSRD will be mandatory for all companies with over 250 employees and over €40 million in annual turnover.

Although most exporters are probably not affected by the CSRD, some exporters may need to comply. Exporters may also get information requests from your buyers if they fall under the CSRD. See the CBI study 8 tips to go green in the cocoa sector and the EU website for details.

Omnibus

An omnibus approach is being developed to combine the CSRD with the CSDDD and EU taxonomy. The proposed omnibus makes the CSDDD much weaker. The directive would apply to fewer companies and limit the obligations only to their direct suppliers. It also removes obligations for climate transition plans and reduces the penalties. This process was not completed when this report was published. The current requirements apply until the proposal is accepted.

Tariffs are disrupting the market

In April 2025, the USA started raising tariff rates on imports from 190 countries and territories. This included key cocoa exporters like Côte d’Ivoire and Ghana.

The tariffs have affected other producing and consuming markets. Because of higher tariffs, cocoa may be shipped to the USA through other countries with lower tariffs. European companies could also move factories to the USA or increase their production there. For example, Lindt is exploring a move to the USA for the production of seasonal chocolate. For exporters, these shifts could mean that your buyers, volumes sold, importing countries and shipping routes change.

In September 2025, cocoa was declared exempt from US tariffs. However, there is still a lot of uncertainty in the market, which will continue to impact global cocoa and chocolate exports. Deals made between the USA and specific African countries will also continue to affect markets.

Recent developments give multinationals advantages over SME exporters

Multinationals are becoming more powerful and dominant in the cocoa sector. This is making it more difficult for local exporters to export to Europe. It also makes them more dependent on selling to a small number of multinational buyers.

Multinationals are growing their business by acquiring smaller companies. Examples include Fuji Oil acquiring Blommer in 2018, Baronie taking over Cémoi in 2021 and Mars acquiring Hotel Chocolat in 2024. In 2025, Touton may be sold to Hartree, Ferrero will acquire Kellogg and CPK Group, and Hershey will acquire LesserEvil.

Some mergers and acquisitions are becoming more difficult for multinationals. The Mars acquisition of Kellanova is currently on hold, partly due to concerns by the EC about the dominance of multinationals. Mondelez attempted to take over Hershey but was unsuccessful. Ben & Jerry’s is trying to separate from Unilever.

Multinationals are also becoming more dominant in producer countries. In Côte d’Ivoire, the top exporters were Cargill, Barry Callebaut, Olam, Ecom, Sucden and Touton. In 2022, they exported 71% of the country’s cocoa. In Cameroon, Olam and Cargill were responsible for 84% of bean exports in 2019-2020. Barry Callebaut processed 89% of all cocoa processed in Cameroon. The top-2 exporters in Ecuador are Olam and Barry Callebaut.

The power of multinational cocoa buyers is impacting local exporters. In Côte d’Ivoire, shortages have caused local exporters to default on their contracts. These bean shortages affect local exporters more than international exporters. Typically, it is also easier for multinationals to buy certified cocoa. Local exporters cannot compete because multinationals have a monopoly on certified cocoa.

This trend could make it more challenging for SME exporters to gain entry to the European market.

Tips:

- Stay informed about the cocoa sector. Check the ICCO’s monthly review of the cocoa market. Subscribe to newsletters like Confectionery News, Cocoaradar or World Cocoa Foundation (WCF) to receive the latest information.

- Invest in the future of cocoa farmers and work with your buyers to ensure that farmers can earn a living income. Implement good purchasing practices together with your suppliers and buyers.

- Read the CBI study Tips to become EUDR compliant for more information. Look for support if this is needed. There are many service providers available. See for example this benchmarking of EUDR solutions.

- Read the CBI study Trends in the European cocoa market to learn more about which trends offer opportunities in the market.

2. Which European markets offer most opportunities for cocoa?

Europe is an interesting market for exporters of cocoa beans, paste, butter and powder. The Netherlands, Germany and Belgium stand out as the most interesting markets for cocoa bean exporters. Other markets like France, the UK and Switzerland are also attractive. These 6 countries are also among the largest importers of cocoa paste, butter and powder, and are likely to remain the largest cocoa importers short-term and long-term.

The Netherlands: world’s largest cocoa bean and product importer

The Netherlands is the largest importer of cocoa in the world. It handles about 20-25% of the global cocoa trade annually and about 50% of European bean imports. In 2024, the Netherlands imported 901,000 tonnes of cocoa beans from producing countries, which was 99% of their total bean imports. Between 2020 and 2024, bean imports increased by 5% per year. However, this followed a large dip from 2018-2019 when the Netherlands imported more than 1 million tonnes per year.

The Netherlands is also Europe’s biggest importer of cocoa paste, butter and powder from producing countries. This share is 45% for paste, 39% for butter and 80% for powder. Cocoa paste and butter imports have been rising, while powder imports are going down.

The Dutch cocoa grinding industry is a key player in cocoa processing. It has Europe’s largest grinding industry and the second-largest globally after Côte d’Ivoire. Total grinding was 600,000 tonnes in 2023-2024, which was 34% of all European grinding. Between 2003 and 2020, cocoa grindings grew by 1.9% annually. The Netherlands has the expertise and focus on innovation and sustainability. It also has a large concentration of cocoa facilities and companies.

The Netherlands is a hub for cocoa import and export. Among members of the Dutch platform DISCO, only 4% of imported cocoa was used for the Dutch consumer market in 2020. It is Europe’s largest exporter of beans, paste, butter and powder. Germany is the most important destination for all re-exports.

Certification is important for Dutch imports. 26% of all Rainforest Alliance sales in 2024 went to the Netherlands, the largest share in the world. 100% of the cocoa bought by Retail and Small Manufacturers members of DISCO is certified. The Netherlands is also the EU’s largest importer of organic cocoa; it imported 20,000 tonnes of organic cocoa beans in 2024, representing 48% of total European imports.

Cocoa imports to the Netherlands are likely to remain steady short-term and long-term. The Port of Amsterdam is expecting agricultural imports to remain stable from 2023 to 2040. Companies are investing in the port and are therefore unlikely to shift to other European ports. Demand in Europe could affect overall European cocoa imports, but the Netherlands will likely remain the biggest European cocoa port.

For exporters, this means that the Netherlands is Europe’s most important target for beans, paste, butter and powder. However, it is also a key competitor if you are exporting these products to other countries like Germany and Belgium.

Germany: Europe’s second-most interesting destination for cocoa beans and products

Germany only imports 37% of their beans from producing countries. However, this volume is still the second largest in Europe with 152,000 tonnes in 2024.

The focus on European trade is increasing. Between 2020 and 2024, Germany started buying more beans from within Europe. Imports from producer countries fell by 6% annually, with most of the decrease coming in the last 2 years. Imports from other European countries grew by 1% per year during this time.

Most cocoa beans enter Germany through the Port of Hamburg and the Port of Bremen. Major investments are expected to expand the future capacity of the ports. The port of Bremen is investing to strengthen their position as a logistics hub. The Port of Hamburg is investing €1.1 billion in port infrastructure. China is also investing in the growth of the Port of Hamburg. These developments could lead to long-term growth in cocoa imports.

Germany is Europe’s second-largest cocoa grinder with 460,000 tonnes for 2023-2024. Grinding in Germany and the rest of Europe is impacted by the high cocoa prices and supply chain challenges. Fourth-quarter grindings in 2024 were 8% lower than the year before. Grindings and stocks continued to decrease in 2025. Key companies include A&D Trading, August Storck, Stollwerck (part of Baronie group), Schokinag Schokolade Industrie, Cargill and Barry Callebaut.

Despite the large grinding industry, Germany still imports a lot of cocoa paste and butter too. In 2024, it imported 23,000 tonnes of paste and 70,000 tonnes of butter from producing countries.

Germany has Europe’s largest chocolate manufacturing industry. In 2022, almost 4.2 million tonnes of confectionery products were produced in Germany, valued at over €14 billion (including non-chocolate confectionery). This makes confectionery the fourth largest sector of the German food industry.

{kind=link}

The chocolate industry is impacted by high cocoa prices and supply issues. Chocolate production volume was down 6% in 2024 (although higher retail prices for chocolate boosted the total value of chocolate). However, the German chocolate market is expected to grow by 5% per year in 2025-2030.

{kind=link}

There is a lot of interest in Germany for the sustainability of cocoa production. In 2023, all members of the German Initiative on Sustainable Cocoa (GISCO) committed to enabling a living income for 90% of all cocoa-producing households supplying to GISCO members by 2030. Germany also has social due diligence laws, covering human rights in the supply chains of tropical commodities like cocoa and coffee.

Germany has a large market for certified cocoa, for both local consumption and export to other European countries. The proportion of certified cocoa in German confectionery has climbed steadily since 2011. While only 3% of chocolate confectionery contained certified cocoa in 2011, this figure rose to 86% in 2024. Rainforest Alliance enjoys 45% brand awareness among German consumers.

Source: BDSI 2025

Local importers include Albrecht & Dill Trading and Walter Matter. The biggest chocolate brands are Milka (owned by Mondelēz), Ritter Sport and Lindt & Sprüngli. Together they account for more than 57% of the tablet market. All these companies buy and sell certified cocoa.

Belgium: focus on importing cocoa beans

Belgium is famous for its high-quality chocolate. The term ‘Belgian chocolate’ refers to chocolate produced by the rules of the Belgian Chocolate Code. It makes sure that key production steps take place in Belgium to protect its reputation. In 2024, Belgium was responsible for 12% of global chocolate exports. This made Belgium the second-largest chocolate exporter in the world.

The importance of Belgian-made chocolate makes Belgium an important destination for cocoa beans. Belgium is Europe’s second-largest importer of cocoa beans from producing countries, with 317,000 tonnes in 2024. The top suppliers were Côte d’Ivoire, followed by Ghana and Nigeria, with Ecuador and Peru as the main Latin American sources.

Cocoa beans enter Belgium via the second-largest cocoa port in Europe, the port of Antwerp Bruges. A large share of these imports is re-exported to other European countries. The main destinations are Germany (74%) and France (20%). This makes Belgium, like the Netherlands, a key entry point for suppliers from producing countries.

Very little semi-finished cocoa is imported from producing countries. Over 99% of their paste, butter and powder imports come from within Europe. This makes it challenging for exporters from producing countries to compete in the market for cocoa paste, butter and powder.

Belgium is a large manufacturer and exporter of chocolate products. In 2021, Barry Callebaut invested €100 million to build the world’s biggest chocolate factory in Belgium. The factory processes over 260,000 tonnes of chocolate each year. Other key processors in Belgium are Cargill and Puratos. The investments made by these large companies will keep Belgium a key import country short-term and long-term.

Belgium is an interesting market for Fairtrade-, Rainforest Alliance- and organic-certified cocoa. In 2021, 65% of the chocolate produced in Belgium was covered by a certification scheme or corporate sustainability scheme. This percentage has increased every year since 2018. Fairtrade has grown a lot in Belgium over the last few years. The retail market share for Fairtrade cocoa has increased from 4.6% in 2018 to 22% in 2023.

Direct imports of Rainforest Alliance cocoa also increased substantially in 2024, from below 1,000 tonnes per year to 31,000 tonnes in 2024. With 128 members registered in 2024, Belgium has the fifth most Rainforest Alliance members in the world.

Belgium is Europe’s second largest importer of organic cocoa, importing 11,000 tonnes of organic cocoa beans in 2024 that represent 27% of total European imports.

Switzerland: important trade hub

Switzerland is home to a strong chocolate manufacturing industry that produces many famous international brands. Large manufacturers include Lindt & Sprüngli, Cailler and Frey. Over 70% of all chocolate produced in Switzerland is exported. Swiss chocolate exports were worth $1.2 billion in 2024 (€1.0 billion).

Many of the largest cocoa and chocolate companies have trading offices in Switzerland, including Barry Callebaut, Cargill, Sucden, Hershey and Nestlé. The presence of these multinationals in Switzerland ensures that the country will remain important for cocoa exporters in the short and long term.

However, a lot of the cocoa that is traded by these offices never reaches Switzerland. Instead, it is often transported directly from one country to another by Swiss firms. Companies base their trade hubs in Switzerland for several reasons, including tax privileges, Switzerland’s financial centre, and Swiss regulations and policies. Their main processing and manufacturing plants are based elsewhere.

Despite the presence of some of the largest global cocoa companies, Switzerland was only Europe’s seventh largest bean importer from producing countries with 62,000 tonnes in 2024. However, Swiss imports are growing. Bean imports from producing countries increased by 7% per year from 2020 to 2025, paste imports by 11% per year, and butter and powder both by 18% per year. This trend is likely to continue in the future.

Swiss imports come almost entirely from producing countries. In 2024, this accounted for 98% of total cocoa bean imports. Switzerland imports cocoa beans mainly from Ghana and Ecuador. The country does not import significant volumes of paste, butter or powder from producing countries.

The opportunities for premium products have been growing significantly. The market for fair cocoa is large in Switzerland, as is the market for organic products. Swiss Fair Trade promotes long-term and fair-trading relationships, stable and transparent prices, fair working conditions and sustainable farming methods. This can be through Fairtrade International, but it can also be through other ethical programmes.

While 82% of all cocoa imported into Switzerland was sourced from ‘sustainable production’, only 37% was certified. The rest was verified through company sustainability programmes. The certified share is stable, while the verified share (company sustainability programme) is increasing. This could indicate that companies aim to achieve the 100% target in 2030 by increasing the company sustainability programme share.

United Kingdom: interesting market for specialty or certified cocoa

The bean import and export market in the UK has seen significant changes since the country left the EU in 2020. Trade with the EU has become more complex and time-consuming. This is not a short-term disruption but will likely persist longer-term.

This disruption has also had a major impact on the trade of cocoa beans. Total bean imports averaged 109,000 tonnes per year in 2019-2020. Bean imports then dropped to an average of 62,000 tonnes per year in 2021-2024. This decrease was mostly because the UK stopped trading beans with the EU. Bean imports from European countries have dropped from 40,000 tonnes in 2019 to around 400 tonnes per year since then. Bean re-exports dropped from 26,000 tonnes in 2019 to 6 tonnes in 2024.

Despite these declines, the UK remained the eight-largest importer of cocoa beans from producing countries in 2024. Cocoa bean trade with the EU has almost disappeared. So exporters also don’t have to compete with EU countries on their bean exports. For exporters, this provides more opportunities for direct exports to the UK. If demand stays constant, direct exports will be the best way to reach the UK market.

Source: Eurostat and Trade Map 2025

The UK is a large market for cocoa and chocolate. It is among the largest chocolate-consuming countries in Europe. The British chocolate market is also becoming more specialised. An increase in artisanal chocolate makers and high-end shops serves more demanding and educated consumers.

Consumers in the UK have high awareness about certification. Rainforest Alliance has 58% brand awareness in the UK. It is also a major market for Fairtrade. Chocolate is the second-most popular Fairtrade product in the UK. Fairtrade chocolate is sold by many retailers and companies. The focus lies more on the social side of sustainability in cocoa, distinguishing it from other markets.

France: growing interest in sustainability

France is the fourth-largest importer of cocoa beans in Europe, with 128,000 tonnes in 2024. Between 2020 and 2024, imports dropped by 5% annually. About 67% of France’s cocoa beans came directly from producing countries, with Côte d’Ivoire and Ghana as main origins. Smaller exporters are Ecuador, Cameroon and Nigeria.

HAROPA Port is the main entry point for cocoa beans imported into France. From 2021 to 2027, they will invest €700 million to modernise the port. This will increase their capacity long-term. HAROPA includes 2 of the largest cocoa market players, Cargill and Barry Callebaut. The combination of investments and the presence of multinational importers will keep HAROPA an important port for cocoa exporters long-term.

There is a large, growing cocoa-processing industry in France. Export of butter and chocolate has been increasing. However, 2024 was a down year for total cocoa bean imports. While total imports were around 60-65,000 for several years, this dropped to only 42,000 in 2024. Bean re-exports also decreased during this time. This ismost likely a direct result of the global cocoa crisis. Imports could increase again when supply goes up and prices decrease.

French interest in sustainability has surged in recent years. Retailers are making more commitments and taking concrete action. The French Initiative on Sustainable Cocoa was launched in 2021, further advancing sustainability commitments. France has become one of the fastest-growing markets for certified cocoa. In 2024, Rainforest Alliance imports were 179,000 tonnes. Fairtrade cocoa imports grew by 8% to 17,000 tonnes in 2023 and overall Fairtrade sales grew by 4%.

Tips:

- Refer to our country studies for more specific information and market insights. Fact sheets are available for Belgium, France, Germany, the Netherlands, Switzerland and the UK. Check the CBI website for all country fact sheets.

- Check out the websites of the national chocolate confectionery associations for more information about the chocolate industry in Belgium, France, Germany, the Netherlands and Switzerland, or CAOBISCO for the European association.

- In your target market, check out the websites of big and small chocolate makers, importers and cocoa processors. These company websites will provide some initial information on their cocoa sourcing and preferences.

- Visit European trade fairs to meet potential business partners. Major cocoa trade fairs in Europe include Salon du Chocolat (Paris and other cities) and Chocoa (Amsterdam). Other important trade fairs are ISM (Germany), Anuga (Germany), PLMA (the Netherlands, for private-label manufacturing) and Biofach (Germany, for organic produce). Attending such events can provide you with additional insight into the preferences of European buyers about origin, flavour and sustainability certification. It can also help you meet potential buyers.

3. Which products from developing countries have the most potential in the European cocoa market?

The European cocoa market is large and diverse. There are opportunities for exporters from many countries and with many different types of products. The most interesting market segments for each supplier depend on product quality, type of cocoa, volumes, and whether it’s certified or part of a sustainability programme.

Most European cocoa imports are bulk cocoa beans

Cocoa beans are the most important cocoa product imported by Europe. European countries import most of their cocoa beans, part of their semi-finished products, and almost none of their chocolate from producing countries. Local processing adds value for exporters, but could also lead to lower demand for your products. European buyers still focus mainly on bean imports. This is important to keep in mind for exporters.

Source: Eurostat and Trade Map 2025

Most beans are imported as bulk cocoa. The bulk cocoa market accounts for about 90% of the total cocoa market. It is highly price-oriented and follows futures prices. There are few possibilities for value addition. The bulk market is interesting for exporters that can supply large volumes at standard product qualities.

The main origins for bulk cocoa are in Central and West Africa. Côte d’Ivoire, Ghana, Cameroon and Nigeria supply 78% of Europe’s cocoa bean imports from producing countries. However, the distribution is changing. Europe is importing less from Côte d’Ivoire and Ghana while buying more from Nigeria. Imports from smaller African origins are also increasing.

Latin America is also becoming more important to European bean imports, exporting bulk and fine flavour cocoa. Ecuador’s share has increased from 5% to 8%. Peru, Colombia, Nicaragua and Bolivia have all increased too.

Source: Eurostat and Trade Map 2025

Certification (mostly Rainforest Alliance) is more and more required in the bulk cocoa market as an entry requirement. This is due to stricter sustainability demands of manufacturers and retailers in Europe. Certification also focuses on these origins. 72% of Rainforest Alliance cocoa in 2024 and 87% of Fairtrade cocoa in 2023 were produced in Côte d’Ivoire and Ghana. See the section on certification for more details.

Europe: large market for cocoa paste, butter and powder

Europe has a large market for cocoa paste, butter and powder. The most important sources are Côte d’Ivoire and Ghana. In 2024, Côte d’Ivoire exported 214,000 tonnes of paste, 81,000 tonnes of butter and 24,000 tonnes of powder. Ghana exported 88,000 tonnes of paste, 55,000 tonnes of butter and 23,000 tonnes of powder. Combined, these volumes represent 78% of all European imports from producing countries.

Cameroon and Nigeria are also important West African exporters of paste and butter. Most of Nigeria’s exports go to Germany, while Cameroon mainly exports to the Netherlands and France.

Indonesia and Malaysia are also large exporters. However, most of the beans used for paste and butter were not produced there but were instead imported from West Africa. This makes Indonesia and Malaysia potentially attractive countries for bean exporters.

Source: Eurostat and Trade Map 2025

There is potential for new export countries as Europe starts to focus on other countries. For example, paste exports from Peru, Mexico and Malaysia increased significantly from 2023 to 2024. Butter exports from Brazil went from less than 100 tonnes in 2023 to over 7,000 tonnes in 2024. The market is therefore still interesting for exporters that are not in the top-6.

Certified cocoa is important in the European market

Europe is the world’s largest market for certified cocoa. Large volumes of Rainforest Alliance and Fairtrade cocoa are imported every year. The largest supplier of certified cocoa beans to Europe is Côte d’Ivoire. Next are Ghana, Nigeria, Cameroon and Ecuador.

Rainforest Alliance and Fairtrade certification are heavily focused on West Africa. In 2024, Côte d’Ivoire exported 953,000 tonnes of Rainforest Alliance cocoa, followed by Ghana (136,000 tonnes), Nigeria (106,000 tonnes) and Cameroon (117,000 tonnes).

For Fairtrade cocoa, the largest exporters in 2023 were Côte d’Ivoire (165,000 tonnes), Ghana (39,000 tonnes), Peru (19,000 tonnes) and the Dominican Republic (10,000 tonnes). These are global exports, although the main destination of the exports is the European market.

The chart below shows 2023 exports for both programmes. 2024 data was not available for Fairtrade.

Source: Rainforest Alliance and Fairtrade 2025

Rainforest Alliance certification is most useful for producers supplying one of the main chocolate brands or leading retailers. It is less needed when selling to smaller brands or to private label manufacturers without sustainability commitments.

Organic cocoa is under pressure

The European market for organic cocoa is expanding. Market awareness is high and consumer demand is rising. However, higher prices and cost of living are putting pressure on demand. New EU regulations are also affecting supply. As a result, organic cocoa production and imports have declined the past few years.

Sierra Leone has the largest area dedicated to organic cocoa, with 165,000 hectares in 2023. Other significant organic producers are the Dominican Republic (114,000 hectares), the Democratic Republic of the Congo (DRC, 84,000 hectares) and Peru (41,000 hectares). The area for the DRC and Peru decreased since 2022.

These 4 countries are also the world’s largest exporters of organic cocoa to the EU. In 2024, the Dominican Republic exported 10,000 tonnes of organic cocoa to the EU, followed by Sierra Leone (9,000 tonnes), Peru (7,000 tonnes) and the DRC (5,000 tonnes). Together, they accounted for 74% of organic cocoa exports to the EU.

Imports from these countries have declined significantly in the last 5 years, with the EU only importing about half of the 2020 volume in 2025. Note that these figures do not include non-EU countries like Switzerland, Norway and the UK.

Source: TRACES 2024

One reason for the decrease is that there is less organic cocoa available. Organic certification is also becoming more complex and costly. However, the organic market is expected to recover and expand again over the long-term. Read more about organic cocoa in the CBI study Exporting organic cocoa to Europe.

Specialty, craft and fine flavour cocoa are interesting niche markets

There is an increasing demand for specialty and premium chocolate products worldwide. These products are made from high-quality cocoa, often defined as fine flavour cocoa. Fine flavour cocoa is of a higher quality and is typically produced in smaller volumes. It is estimated that 5% of the world’s production is fine flavour cocoa. Fine flavour cocoa is part of the specialty market. The ICCO designates countries that produce fine flavour cocoa.

Specialty cocoa is mainly sourced from Latin America and the Caribbean. Ecuador is the world’s main exporter of fine flavour cocoa. 70% of Ecuador’s cocoa production can be considered fine flavour cocoa, although not all cocoa will be sold as such. Peru and the Dominican Republic also have significant fine flavour cocoa exports. Despite its small market share, it is the fastest-growing segment in the chocolate market. This could be an opportunity for suppliers of high-quality cocoa.

For more information about fine flavour and specialty cocoa, see the CBI study Exporting specialty cocoa to Europe.

Company programmes are used to meet sustainability commitments

Company sustainability programmes are becoming increasingly important. These programmes are developed by cocoa traders, processors or manufacturers.

Company sustainability programmes are not considered certification programmes, since they are not independently developed and audited. They are often less complex and less transparent than certification schemes. The standards are usually not publicly available.

Many brands have commitments for ‘sustainable’, ‘responsible’ or ‘ethical’ sourcing. They usually accomplish these targets with a combination of cocoa that is certified, sourced as part of their own sustainability programme, or sourced through the programme of their suppliers.

There are many combinations in the market. The approaches for the 6-largest chocolate manufacturers are shown below.

Table 1: Responsible sourcing commitments of the 6-largest chocolate brands

| Manufacturer | Volume (tonnes, 2025) | Commitment | Status | Commitment programmes |

|---|---|---|---|---|

| Mondelez | 430,000 | 100% by 2025 | 91% in 2024 | Own programme Cocoa Life |

| Nestlé | 367,000 | 100% by 2025 | 88.9% in 2024 | Own programme The Nestlé Cocoa Plan, along with Rainforest Alliance certification |

| Mars | 335,000 | 100% by 2025 | In progress | Own programme Responsible sourcing, builds on existing requirements from Fairtrade and Rainforest Alliance |

| Hershey | 220,000 | 100% | Achieved | Fair Trade USA, Rainforest Alliance and other independently verified programmes through suppliers that meet Cocoa Key Requirements |

| Ferrero | 208,000 | 100% | Achieved | Independently managed sustainability standards such as Rainforest Alliance, Cocoa Horizons or Fairtrade Foundation |

| Lindt & Sprüngli | 145,000 | 100% | Achieved | Own programme The Lindt & Sprüngli Farming Program or other sustainability programmes |

Source: Cocoa Barometer 2025 and company websites

Many traders and processors also have their own sustainability programmes, like Ofi Cocoa Compass, Barry Callebaut Cocoa Horizons, Cargill Cocoa Promise, Sucden, Touton PACT, Blommer Sustainable Origins, ETG And Cémoi Transparance Cacao. Some of these also form part of the sourcing strategies of global companies and their brands. The table below shows the volumes and shares that are publicly reported.

Table 2: Company sustainability programmes of the largest traders and processors

| Manufacturer | Total cocoa volume (tonnes, 2025) | Share of total volume (%) | Programme(s) | Source |

|---|---|---|---|---|

| Barry Callebaut | 998,000 | 26% | 256,000 tonnes Cocoa Horizons. | Cocoa Horizons 2024-2025 mid-year report |

| Ofi | 1,000,000 | Not reported | Not reported. | 2023 sustainability report Ofi |

| Cargill | 888,000 | 18% | 54% Rainforest Alliance, Fairtrade, Promise Verified, or customers’ own programmes for Cargill Cocoa Promise. Equals 18% of total volume. | 2024 ESG report Cargill |

| ECOM | 810,000 | 29% | 78% verified or certified sustainable for ‘ECOM origin-sourced supply chains’. Equals 29% of total volume. | 2024 Cocoa Sustainability Report Ecom |

| Sucden | 409,000 | 27% | 27% Rainforest Alliance and Fairtrade cocoa sales. Unknown customer programme volume. | 2024 Responsibility Report Sucden |

| Touton | 308,000 | 51% | 55% of beans and 21% of derivatives certified or part of a sustainability programme. 51% of total volume (not calculated to cocoa bean equivalent) | 2023-24 Sustainability Report Touton |

Source: Cocoa Barometer 2025 and company websites

Traders or brands could approach farmer groups about becoming part of their company programme. This could lead to a long-term commitment and partnerships with the brands or traders. However, be sure to ask detailed questions before agreeing to become part of a programme. Ensure that the conditions and financial incentives are attractive enough to make the commitment. Ask for clear details about the requirements and expectations.

Tips:

- Speak with your buyers to make sure that there is demand for certified cocoa. Make sure that there is market demand for certification. See if certification is economically viable and that it ensures long-term relationships with buyers.

- Consider organic certification and whether this is possible for your cocoa production. It takes time and effort to switch to organic certification. Check the Nitidae report about the transition towards organic cocoa production, the Naturland guide about growing organic cocoa or the ICCO manual for Pesticide Use in Cocoa for more information about organic production.

- For exporters, consider getting Fairtrade- and Rainforest Alliance-certified as a supply chain actor. This is usually an easier certification process than certification for producers. Exporters usually need to have a license to buy and sell certified cocoa. However, first discuss this with the farmer groups and buyers that you work with. Read the CBI studies on certified cocoa, organic cocoa and specialty cocoa to learn more about specific market dynamics and opportunities.

- Focus on the premium, specialty and fine flavour cocoa markets in Europe if you offer high-quality cocoa. Establish direct trade relationships with smaller traders and chocolate makers. Read the CBI studies on buyer requirements and on how to do business with European cocoa buyers to learn more.

- Be aware that many cocoa buyers now require compliance with new EU legislations, including extra information on legal compliance, social due diligence, traceability and geolocations. Read the CBI studies with tips on going green in the cocoa sector and how to become more socially responsible in the cocoa sector for more details.

Long Run Sustainability carried out this study in partnership with Ethos Agriculture on behalf of CBI.

Please review our market information disclaimer.

Search

Enter search terms to find market research

Do you have questions about this research?

The price of cocoa has increased for producers. Unfortunately, production has also fallen for most producers. This has led to a feeling that they are unable to really benefit from this increase. Prices would need to stabilise around the current level in order to bring about real long-term change for producers.

Bakary Traore, Executive Director at ONG IDEF