What trends offer opportunities or pose threats in the European cocoa market?

Europe buys and grinds more cocoa than any other region in the world. Most of the cocoa comes from West Africa, especially Ghana and Côte d’Ivoire. These countries are facing several issues, including low yields, climate change and low incomes for farmers. Because of these persisting problems, European companies and governments are looking for new ways to make the cocoa supply chain fairer and more sustainable. For cocoa exporters it is important to understand these new rules and trends to keep selling to Europe in the future.

Contents of this page

- Regulatory compliance is becoming the core driver of the European cocoa market

- Cocoa’s recent price movements reflect a structural shift rather than a series of short-term spikes

- Digital tools are becoming a basic necessity

- Agroforestry and regenerative cocoa systems are gaining traction

- Premium chocolate segment is small but growing

- Storytelling: increasingly important on the cocoa and chocolate market

- Health, wellness and functional benefits increasingly influence chocolate consumers

- Lifestyle choices are also influencing consumer preference

This study identifies key trends that are shaping the European the cocoa market in the short term (1-3 years) and long term (beyond 3 years). The first trends focus on long-term sector transformation driven by sustainability, regulation and innovation, and are presented in the yellow box below.

1. Regulatory compliance is becoming the core driver of the European cocoa market

Sustainability in Europe is moving from voluntary to mandatory, and this is reshaping the cocoa market. Regulatory compliance is now a main driver. To sell cocoa in Europe, exporters must meet sustainability rules such as legal sourcing, no deforestation and strong traceability.

Certification, digital traceability systems and close work with farmer groups are practical ways to meet these requirements. Companies that are well organised and prepared for the new rules can continue doing business in Europe and build a stronger reputation. Checking your compliance with sustainability rules and sustainability initiatives will now be normal when a buyer wants to buy your cocoa. Buyers will expect clear proof, not promises. Therefore, keeping data well organised in digital form is essential to show where the cocoa comes from and that it meets the rules.

The following sections describe the mandatory sustainability regulations and the changes that are expected in the coming months and years.

European Union’s mandatory sustainability regulations

The mandatory sustainability requirements are part of the European Green Deal (EGD) to make Europe climate-neutral by 2050. The EGD introduces stricter environmental and sustainability standards and adds requirements for export companies from developing countries. This will impact trade within the EU and imports to the EU.

One of the policy areas of the Green Deal is the From Farm to Fork strategy, which aims to create a healthier and more sustainable food system with an ambitious goal of a 50% reduction in the use of pesticides by 2030. As part of this measure, the EU seeks to enforce environmentally friendly pest control practices.

Some rules as part of the EGD are driving the transformation in the cocoa sector:

- EU Regulation on deforestation-free products (EUDR) – for deforestation-free cocoa;

- Corporate Sustainability Due Diligence Directive (CSDDD) – for respect for people and nature;

- Corporate Sustainability Reporting Directive (CSRD) – for reporting on sustainability.

Following them will give you the opportunity to sell cocoa on the European market. Also, sustainability certifications and labels such as Fairtrade, Rainforest Alliance and Organic can provide concrete support. They do not replace companies’ own responsibility but make it more structured and verifiable. They offer standards, monitoring tools such as audits, and reliable data that make due diligence stronger and more effective.

Now let’s explain each one of the rules in simple terms.

European Union Deforestation Regulation (EUDR)

The EU Deforestation Regulation was officially adopted and entered into force on 29 June 2023. According to this rule, cocoa must not come from land that was deforested after 31 December 2020. If you want to export cocoa to the Europe Union, you must:

- Show where your cocoa was grown using GPS or mobile apps;

- Prove that the land was not deforested after 2020;

- Share this information with your buyer or through the EU’s online system.

Example: If your cocoa farm was deforested in 2018 and you have GPS coordinates, you can sell to the EU. If your farm was deforested in 2022, you cannot sell that cocoa to Europe.

For large and medium companies, enforcement begins from 30 December 2026. For small and micro companies, enforcement begins from 30 June 2027. Large operators are companies with 250+ employees and over €50 million in annual turnover. Small businesses have fewer than 50 employees and an annual turnover below €10 million. Micro businesses typically have fewer than 10 employees and an annual turnover below €2 million.

National cocoa industries have already started finding ways to comply with this regulation. For instance, the Peruvian cocoa industry has already begun adapting to new regulations. To support Peru’s efforts, Solidaridad coordinates innovative pilot programmes while working with its partners to conserve forests and support small-scale cocoa producers.

Ghana and Côte D'Ivoire, the two major exporters of cocoa beans, are also putting up nationwide strategies to monitor deforestation and support farmers in complying with the rules. Ghana’s cocoa traceability system has moved from pilot to national rollout. The Ivorian Government has taken steps to address challenges through policies like a zero deforestation strategy and the Cocoa & Forests Initiative. The World Cocoa Foundation (WCF) has introduced a standardised deforestation risk assessment methodology for its members.

The Corporate Sustainability Due Diligence Directive (CSDDD)

The Corporate Sustainability Due Diligence Directive (CSDDD) officially came into force in July 2024. It is now only mandatory for very large firms (5,000+ workers and €1.5B turnover). This rule says that companies must check their supply chains to make sure there is no child labour, forced labour, pollution or unsafe working conditions. As a cooperative or exporter, you must:

- Know who is growing your cocoa and how they grow it;

- Fix problems if you find them (e.g. poor working conditions);

- Keep records and share them with buyers.

For example, if your cooperative hires workers, you must make sure they are paid fairly, work safely, and aren’t children. If there is a problem, you must act and show what you did.

The rule therefore requires cocoa cooperatives and businesses that export to the EU to create clear codes of conduct. These codes should explain how the business acts responsibly in three main areas:

- Ethics: Doing business in a fair and open way;

- Social Responsibility: Treating workers and farmers fairly, paying them a living income and helping local communities;

- Environmental Responsibility: Protecting forests, saving nature and working to reduce carbon emissions.

These codes of conduct should guide the company’s daily work and show that it follows the CSDDD requirements. Read the Centraleyes blog on understanding the CSDDD to learn more about how it matters and how to prepare

Corporate Sustainability Reporting Directive (CSRD)

The Corporate Sustainability Reporting Directive (CSRD) came into force on 5 January 2023. It requires companies to disclose their environmental, social and governance (ESG) impacts. In other words, companies must report how they treat people and the planet. This includes farming, labour, environmental and business practices. The CSRD strengthens the rules on how companies report social and environmental information. The scope has been reduced to firms with 1,000-1,750 workers and €450M turnover. First reports are now due in 2028-2029.

ESG data to be collected includes emissions data (such as carbon dioxide (CO2) emission from farming and transportation), information on labour practices and community impacts and the use of resources like water, fertilizers and pesticides. This regulation also requires you to provide clear records of operations, payments and sustainability initiatives.

Exporters must share data about your cocoa: how it’s grown, how workers are treated, and how forests are protected. Always use simple formats that buyers can understand. Sometimes they may be asked to give proof using photos, documents or maps.

For example, your buyer may ask: ‘How many workers do you have? Do they wear safety gear? Is your cocoa grown without harming the forest?’ You must answer clearly and honestly.

The CSRD also requires companies to have their sustainability reports independently checked to ensure the information is accurate. This means companies must hire an outside expert, either a professional auditor (like the ones who check financial accounts) or a specialised sustainability expert, to review their environmental and social claims.

The expert examines the company’s data and confirms whether the sustainability information is truthful and reliable. This independent verification builds trust because stakeholders know the company’s environmental and social achievements have been checked by someone with no reason to exaggerate or hide problems. Therefore, it introduces a digital system to organise and classify sustainability data, making it easier to compare and access.

EU Omnibus Proposal

There is a high number of rules and extensive paperwork required. So the EU wants to harmonise these rules and make it simpler for companies to follow and reduce the burden, especially for small companies. This led to the European Union's Omnibus Package proposal in February 2025. This proposal has not been approved yet by the European Parliament and the Council. But if it gets approved it will mean less paperwork for small companies and more time to comply with the rules.

In case of approval, big companies will still need to submit full reports, so small suppliers must provide good information. Example: You may not need to write long reports, but your buyer might ask for basic data like farm location, worker numbers and farming methods. In the meantime, cocoa stakeholders and civil society have pushed back this proposal to preserve robust due diligence and climate accountability.

You should therefore continue working closely with your buyers to support them, to ensure that their supply chains are more transparent and responsible, in line with the current CSDDD, CSRD and EU Taxonomy regulation requirements.

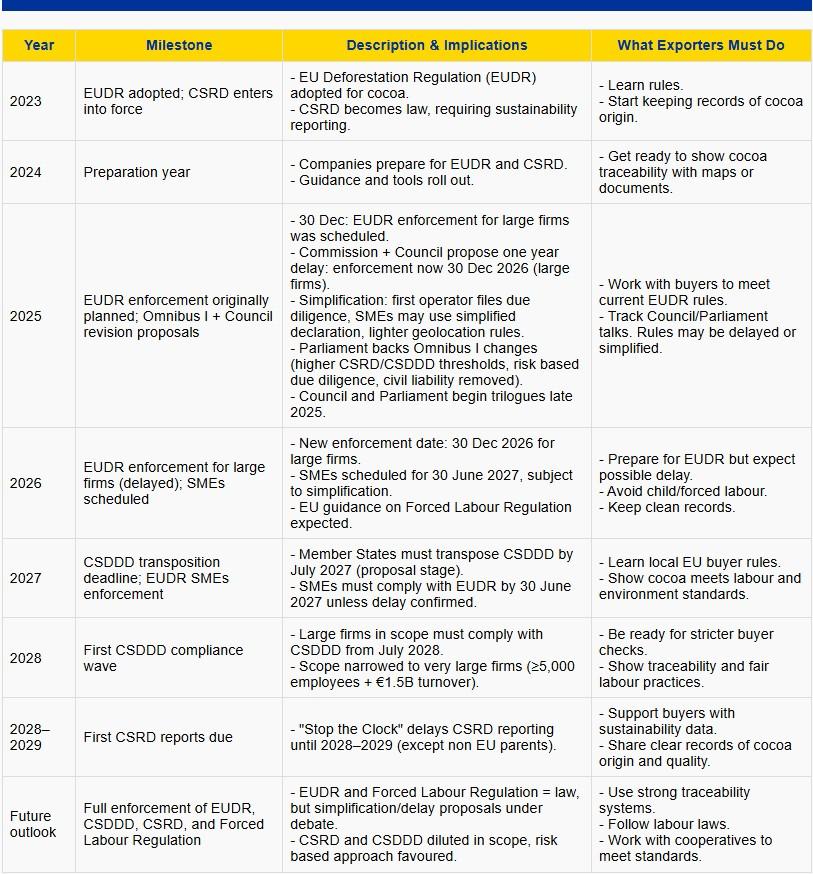

Figure 1 presents infographics summarising EUDR, CSDDD, and CSRD timelines and implications.

Figure 1: Timelines of EU sustainability rules and implications for exporters

Source: Amonarmah Consults

Tips:

- The EU has introduced a country risk classification; check this list to see where your country falls. Countries are classified into low-risk, standard-risk and high-risk. If your product comes from a low-risk country, only 1% of those operators will be randomly selected for audit by EU authorities.

- Work closely with EU-based buyers to understand their reporting needs under CSRD. Buyers may provide guidance or support in aligning with reporting standards.

- Refer to the UNDP Sample Code of Conduct for Small and Medium Enterprises to learn more when writing your own code of conduct.

- Refer to the ILO’s Checkpoints for Companies on Eliminating and Preventing Child Labour and download the app to your iOS or Android device to help your practices and promote decent work and social protection.

- Refer to our tips to go green and become socially responsible in the cocoa sector.

2. Cocoa’s recent price movements reflect a structural shift rather than a series of short-term spikes

Yearly average prices moved well above historical norms over the past two years because supply has not kept up with demand. There are a number of underlying causes. There is constant under-investment at farm level, aging trees and low productivity. Climate stress (including droughts, irregular rainfall and disease), pest and diseases also affect cocoa production. Finally, there are land-use pressures such as illegal mining, and higher compliance costs linked to strong EU laws. These have led to a structural imbalance within the cocoa industry.

In 2024, futures prices rose when markets anticipated shortages due to drought and disease in West Africa. They then eased as rainfall improved soil moisture and flowering. This shows potential yield recovery. As of mid-September 2025, prices were below their late‑2024 highs but remain high relative to long-term averages.

Most farmers have not benefited from higher cocoa prices. This is because in several producing countries, futures markets, fixed farm-gate pricing, export taxes and high borrowing costs limit farmers from receiving the high prices. Rising input costs for fertiliser, labour and crop protection further hurt their small profit margins. Meanwhile disease, drought and low yields reduce the volumes farmers can sell. This reinforces the investment gap and keeps supply constrained, feeding the structural imbalance.

Downstream, chocolate companies are adjusting to higher average ingredient costs rather than reacting only to instability. Some are reformulating recipes, diversifying sourcing, or securing supply when prices soften. But retail chocolate prices remain high due to cocoa costs, general inflation and other processing expenses. Many brands have raised prices or reduced pack sizes. Premium and ethical brands are also emphasising origin, quality and impact to support higher price points.

Cocoa prices patterns are responding to fundamentals such as fears of scarcity, which pushes prices up, and signs of improved supply, which pushes prices down. Cocoa prices are declining recently for several reasons (Figure 2). First, demand from manufacturers is weaker due to higher costs and tighter profit margins. Europe’s recent data shows that cocoa grindings, which measure how much cocoa is being used, dropped significantly by 5.4%, 3.7% and 7.2%, respectively, in Q4 of 2024, Q1 of 2025 and Q2 of 2025. The decline indicates that companies are using less cocoa. This trend is expected to continue until supply improves. Second, there are signs of improved cocoa production and hence supply, particularly in West Africa, which leads to even more lower prices.

Source: ICCO, 2025

In the short term, prices are expected to continue to decline further if weather is fine and supply rebuilds to meet demand. In the medium term, if weather stays good and rehabilitation efforts advance, prices may stabilise as supply and demand move closer to balance. But a full return to historic lower prices is not likely.

In the long term there will still be challenges with supply. This means there may not be enough cocoa available in the future due to climate change situations. For chocolate makers, this means they must make tough decisions. They can either focus on making quick profits now or invest in improving their supply chains to ensure they have enough cocoa in the future. Basically, they need to choose between making money today or planning for a more stable supply later. But if adjustments in chocolate makers’ recipes to use less cocoa become the norm, demand will be low, keeping prices low.

Given these conditions, chocolate makers in cocoa-producing countries have to deal with changing cocoa prices. They should also keep in mind that consumers are very sensitive to prices. This means they need to balance their costs with what consumers are willing to pay for chocolate. They can still differentiate themselves through origin branding and focused premium niches. Exporters also face higher capital needs and stricter sourcing standards but can capture more value through strong digital traceability.

Tips:

- Stay informed about the cocoa sector. Check the ICCO’s monthly review of the cocoa market. Subscribe to newsletters like Confectionery News, Cocoaradar or World Cocoa Foundation (WCF) to receive the latest information.

- Invest in the future of cocoa farmers and work with your buyers to ensure that farmers can earn a living income. Implement good purchasing practices together with your suppliers and buyers.

3. Digital tools are becoming a basic necessity

New digital tools emerge to comply with the new regulations. This includes traceability as well as remote sensing. Cocoa buyers and chocolate manufacturers are using digital tools more and more to track cocoa from the farm all the way to the final product. These tools include blockchain, which securely records every step in the supply chain. Bar or QR codes, which are placed on cocoa bags or chocolate bars, allow you to see exactly where the cocoa came from.

For example, Ghanaian craft chocolate maker Kabi Chocolate developed a unique approach to connect consumers to the source of their chocolate, They do this by adding an art card with a QR code to their packaging (Figure 3). This code links to a video showcasing the Ghanaian story behind their chocolate, including a virtual tour of their cocoa farms. This approach connects consumers directly to the source and differentiates Kabi Chocolate in the market.

Figure 3: Kabi Chocolate’s example of QR-enabled storytelling with their packaging

Source: Kabi Chocolate

Remote sensing digital trend relates to the use of satellite images to check that farms are free from deforestation. Projects like TraceX and Ghana COCOBOD’s Cocoa Management System (CMS) platform are helping farmers by registering their farms, mapping their land with GPS, and maintaining digital records.

If you are a cocoa exporter or supplier, this trend will directly affect your business. European buyers now expect digital proof of where your cocoa comes from. This means you will need to register farmers, map farms with GPS and keep detailed records of your sourcing. Without these traceability measures, you risk losing access to European buyers. This may lead to you being excluded from the European market. This is especially important under the EUDR, which requires geolocation data and proof of legal production for all cocoa entering the EU.

In the future, full digital traceability may become a basic requirement for doing business in the European cocoa sector. Besides this, buyers may use real-time audits, remote monitoring and artificial intelligence tools to monitor and check your supply chain. Manual records may soon not be enough, and exporters who do not adopt digital systems may be excluded from key markets.

For example, Ghana’s cocoa sector is moving from paper-based systems to digital platforms that track every bean. Through its Cocoa Management System (CMS) platform and the Cocoa Traceability System launched in August 2025, Ghana COCOBOD has begun attaching bar codes to every cocoa bag (Figure 4). When scanned, it provides all information about farmers and farms from which the cocoa beans were obtained. Embracing digital traceability will now help you stay competitive and connected to the global cocoa market.

Figure 4: Cocoa bags with bar codes for traceability

Source: Amonarmah Consults

Tips:

- Read more about the simple three-phase traceability system in place in Ghana.

- Digitise your supply chain records and link them to GPS-mapped farms. Use platforms like FarmForce or SourceMap, or open-source GIS tools.

- Partner with local service providers offering traceability services.

4. Agroforestry and regenerative cocoa systems are gaining traction

Climate change is already having a serious impact on regions where cocoa is grown. Rainfall has become more unpredictable, temperatures are rising, pests and diseases are spreading faster, and soil fertility is declining. These changes are reducing cocoa yields and putting farmer incomes at risk.

While climate adaptation practices have long been an important strategy to address these challenges, the discussion has recently shifted towards agroforestry systems and regenerative cocoa. A regenerative cocoa system is a way of growing cocoa that restores soil, supports nature and improves farmer livelihoods while producing cocoa.

Agroforestry (Figure 5) and regenerative cocoa farming are growing fast, especially among organised farmer groups and certified cooperatives. In Côte d’Ivoire, more than half of cocoa farmers (54%) say they are already planting more trees to protect their farms and increase yields. Large chocolate companies are also investing in sustainable farming and plan to reach 100% sustainable cocoa by 2025-2030. This means that in the next few years, more farmers will join these programmes.

By 2028 and beyond, agroforestry and regenerative systems are expected to become common across many cocoa cooperatives. The Swiss Platform for Sustainable Cocoa (SWISSCO) notes that cocoa companies aim to meet near-term goals by 2030 and net-zero emissions by 2050, making sustainable cocoa a long-term requirement. At the same time, Africa’s carbon-credit market is expected to grow nearly 19 times by 2030. This is opening new income opportunities for exporters and farmer groups that use climate-smart cocoa systems and can show proof of low-carbon production.

Figure 5: Agroforestry cocoa farm

Source: Amonarmah Consults

In the next paragraphs we show different governments, companies and NGOs programmes and initiatives. They are geared towards agroforestry and regenerative cocoa systems to protect the future of cocoa production.

In the Amazon, sustainable cocoa farming is being used to generate carbon credits. Agroforestry projects combine cocoa with native trees, restoring degraded land and protecting rainforests. This approach aims to increase farmer income, biodiversity and climate resilience. These will in turn contribute to both local communities and global climate goals.

Ghana has advanced climate adaptation in cocoa farming by promoting sustainable practices like agroforestry and reforestation. These initiatives have earned the country $4.8 million in carbon credits for reducing deforestation-related emissions, with potential for much greater revenue. Farmers also benefit from increased yields and improved climate resilience.

Côte d’Ivoire is building climate resilience through projects like PROMIRE, which promotes deforestation-free cocoa production. Organisations like MyClimate are helping farmers adopt dynamic agroforestry (DAF). With DAF you plant diverse trees alongside cocoa to boost soil health, biodiversity and resistance to climate shocks. Ghana is also scaling up DAF through the Ghana Cocoa Board and projects like Sankofa 2.0. This helps farmers diversify income, restore land, and improve yields and resilience.

Private sector sustainability programmes are also working towards climate adaptation and regenerative cocoa farming. For example, Nestlé, in partnership with Barry Callebaut, is rolling out an agroforestry and income support programme across Côte d’Ivoire, Ghana and other cocoa producing countries. The initiative aims to improve cocoa farmer incomes through payments for ecosystem services while boosting biodiversity and climate resilience.

Barry Callebaut and Nestlé have also announced a partnership that will aim for net zero cocoa production in Brazil. Mars has begun investing in climate-resilient agricultural work through its cocoa for generations programme in Latin America. This relates to agroforestry systems, aerobic composting, the use of biochar and the use of low greenhouse gas (GHG) fertilisers.

Chocolate companies prefer cocoa suppliers who use farming methods that protect the environment and the climate. This creates good business opportunities for cooperatives and exporters who practice climate-smart and sustainable farming. By doing so, they become trusted partners for major chocolate brands that want to make their supply chains more responsible and environmentally friendly.

Apart from being an attractive and trusted supplier, implementing agroforestry models or regenerative cocoa systems has multiple benefits for exporters and producers. Cocoa yields can be enhanced, even in the face of challenges like drought, heat and disease. It can also lead to bean quality improvements and hence higher prices and increased interest from buyers. Cocoa farmer cooperatives can also earn carbon credits for climate-smart practices. They can explore the opportunity of carbon credit programmes like that of Verra and Gold Standard, plus become preferred suppliers for buyers who want low-carbon, resilient cocoa.

Tips:

- Learn more about regenerating cocoa here.

- Refer to Rainforest Alliance’s New Regenerative Agriculture Standard.

- Integrate shade trees, cover crops and soil fertility management into cocoa farms, document and promote your farm’s adaptation strategies.

- Explore partnerships with carbon credit or agroforestry initiatives like Verra and Gold Standard.

- Learn how carbon markets can work for small-scale farmers from Solidaridad’s Asómbrate programme in Colombia.

5. Premium chocolate segment is small but growing

The premium cocoa segment includes cocoa with higher quality or extra value, so it sells for more than standard bulk cocoa. Specialty cocoa is a part of this segment and makes up less than 10% of the market. It is often used for craft chocolate, which has grown about twice as fast as the regular cocoa market over the last 20 years. Around 49% of craft chocolate makers are in Europe, with many based in France, Italy, Germany, Austria, the UK and Switzerland. Still, the craft market is very small, at about 0.2% of global cocoa. Also, only about 4% of craft chocolate bars use cocoa from West Africa.

Globally, there is a rise in consumer preference for premium, artisanal chocolates. The demand is contributing to strong growth in the premium chocolate market. The market is projected to grow from an estimated value of US$ 7.4 billion in 2025 to a remarkable US$ 17.1 billion by 2035. This growth reflects a compound annual growth rate (CAGR) of 8.7% over the coming years.

Europe plays an important role in the global premium chocolate market with an expected cumulative annual growth rate of about 7% for 2025-2033. The growth is even stronger in regions like Belgium, France and Germany. The market is experiencing this growth because of increasing health awareness, a rising demand for ethically sourced products, and trends in luxury gifting. Germany especially has consumers gravitating towards high-quality, sustainable dark chocolate that offers health benefits and strong flavours. In addition to consumer preferences, Europe's strict sustainability regulations are influencing procurement decisions of chocolate companies. As a result, chocolate brands are adopting environmentally responsible practices that reinforce their premium positioning.

For small and medium cocoa exporters and cooperatives, this growing market offers a chance to enter high-value supply chains. European chocolate makers are looking for new origins, traceable sources and unique flavour profiles. By improving bean quality, fermentation methods and transparency, SMEs can position their cocoa as premium or specialty and access buyers who pay higher prices for ethical and flavour-rich cocoa. In the longer term, forming direct trade partnerships with bean-to-bar makers or supplying small batches for craft chocolate can help SMEs capture more value and build reputation in this expanding niche.

For more on the European speciality cocoa market, refer to our studies What is the demand for cocoa on the European market?, The European market potential for speciality cocoa and Entering the European market for speciality cocoa.

Single-origin chocolate: premium product gaining popularity

Single origin highlights cocoa from one country or region, offering distinct flavours and a stronger sense of origin that many consumers now seek. Consumer interest in the origins and quality of chocolate ingredients is driving this trend, with single-origin chocolates becoming increasingly popular for their unique flavour profiles. The chocolate flavours are unique to the origin based on variety (e.g. fine flavour cocoa types), agro-climatic factors and post-harvest handling techniques.

75% percent of consumers believe that single-origin chocolate is both more premium and sustainable than conventional varieties. Additionally, 63% of consumers perceive chocolate from specific regions as more premium than other varieties. Retailers continue to offer a wide variety of single-origin private-label chocolates, like Dutch Albert Heijn chain’s private-label brand Delicata. Delicata offers chocolates from Uganda, Peru, Costa Rica and Tanzania. Another example is the L’origine du goût chocolate collection from retailer E-Leclerc (France), made from Nicaraguan single-origin cocoa. In the UK, Waitrose offers a line of single-origin chocolates from Ecuador, Dominican Republic and Peru under its No. 1 collection.

Valrhona Inc., a renowned French chocolate producer, has been sourcing cocoa beans exclusively from the Maria Trinidad Sanchez estate (Dominican Republic). This approach ensures consistent flavour and quality for their chocolate products. Chocolate brands offering single-origin bars include Blanxart (Spain), Willie's Cacao (United Kingdom), Original Beans (the Netherlands) and Domori (Italy).

Figure 6. Single-origin bars from private label brand Kabi chocolate (Ghana)

Source: Amonarmah Consults

Single-origin products consist of three types: single-country, single-region and single-estate (Figure 7). Single-country chocolate is made using cocoa grown within a specific country. Various factors influence the sensory profile of single-country chocolate, including genetics, land conditions, and post-harvest processes like fermentation and drying. To consumers, single-country chocolate embodies the distinctive flavours and character of the country where it is produced.

Single-estate chocolate focuses on expressing the flavour of a specific farm instead of the whole country. This classification not only represents the land where the cocoa is grown but also encompasses the farm’s effort and characteristics. Single-estate chocolate reflects the farmer’s own unique essence and personality and the farm’s work culture, lifestyle and initiatives, representing the entire family behind it.

Single-estate chocolate makers like Cluizel aim to showcase the special flavours and qualities of a specific cocoa farm. They achieve this by maintaining a close and regular partnership with farmers to obtain the finest cocoa beans to craft their chocolate. This close collaboration also provides them with valuable insights into the farmers’ culture and traditions. Other single-estate examples are the lukerchocolate line and Ecuador’s Hacienda Victoria cocoa exporter.

Figure 7: Types of single-origin sources

Source: Amonarmah Consults

Exporting single-origin and single-estate cocoa or cocoa products to the European market requires strong traceability and documentation, plus sharing stories about the production context and providing assurance of the cocoa’s origin. Information related to the product’s organoleptic profile, the farmers’ profile, production and post-harvest methods, or surrounding nature and community will make your product more attractive to buyers looking for high-quality and unique cocoa.

Tips:

- Explore the possibility of obtaining legally protected geographical indications (GIs) for specific cocoa varieties. This can be an important element in your storytelling. Read the frequently asked questions on GIs on the World Intellectual Property Organization (WIPO) website, where you can find answers on applying for GI protection.

- Document and maintain the genetics of your cocoa trees. This distinguishes your unique flavour profile if you want to partner or sell your cocoa beans to single-origin chocolate makers. Learn more about harvesting and post-harvest management to improve and distinguish your cocoa bean quality.

- Connect with research institutions in your region or country. They can help you identify the varieties of cocoa trees on your farm. Some cocoa research institutes are CRIG (Ghana), CRIN (Nigeria), ICCRI (Indonesia) and UWICRC (Trinidad and Tobago). Cocoa varieties, production practices and conditions affect the quality and flavour of your cocoa beans.

- Investigate whether you qualify for industry awards, such as the International Cocoa Awards (ICA) or the Cocoa of Excellence. This can be an interesting way to profile yourself in the European market for fine flavour cocoa. ICA rewards flavour, quality and diversity of different origins.

- Read our study Exporting chocolate to Europe.

6. Storytelling: increasingly important on the cocoa and chocolate market

Consumers are increasingly interested to learn more about the origin of and story of chocolate they purchase. Most consumers (61%) are interested in learning more about the origins of their chocolate confectionery and its ingredients. This suggests that many consumers are interested in learning how cocoa production is done. Such narratives enable consumers to choose chocolate that aligns with their interest in socially and environmentally responsible cocoa.

Consumers continue to seek unique and novel chocolate experiences. This relates not just to specific flavours but also to stimulating their curiosity and sense of adventure as they taste chocolate that aligns with their values and preferences. This trend is also closely associated with an increasing emphasis on the cocoa’s origin, as well as principles of transparency and traceability.

Chocolate brands Ethiquable and Tony’s chocolonely (Figure 8) are already responding to these consumer preferences by using their packaging to tell the cocoa and cooperative story. Ghanaian craft chocolate brand Kabi Chocolate also recognises this trend by incorporating an art card with a QR code in their packaging (Figure 1) to showcase the Ghanaian story behind their chocolate, as noted in the digital traceability section.

Figure 8: Storytelling package of Tony’s chocolonely 70% dark chocolate

Source: Tony’s chocolonely

Overall, a good story helps you to market your product to specialty cocoa traders. Cocoa importers and chocolate makers can in turn use your stories in their communication with customers. By telling an appealing story, they can connect consumers to the cocoas origin and producers. This adds value to the final chocolate product.

Exporting companies sharing appealing stories about their company and history include Kokoa Kamilia (Tanzania), Lukerchocolate (Colombia), Esco Kivu (DR Congo) and Ingemann (Nicaragua).

Tips:

- Develop and express your unique selling points as a supplier of cocoa beans. Think about factors that set you apart from your competitors and create your marketing story around these features. For example, they can be related to the origin of your cocoa beans, the agro-climatic characteristics of the producing region, the culture of the producing communities, the unique quality of your product, your post-harvest techniques, or a combination of these aspects.

- Never make claims that you cannot support, for instance on the quality or production volumes of your cocoa.

- Check out the website of the specialty cocoa importer Uncommon Cacao, and see how they tell the story about the cocoa producers they source from.

- Refer to our study on going digital in the cocoa sector for tips on how to increase your market attractiveness and storytelling through digital experiences. Make sure to share your stories with a larger audience, for instance through social media and/or your website. When talking about your mission and the history of the farm or cooperative, give the story a face. Do so by providing good-quality photos of the plantations, the farmers and their families.

- Get the full report of Barry Callebaut’s Proprietary Consumer Research for 2024 and beyond chocolate trends; it will be sent to your email address.

7. Health, wellness and functional benefits increasingly influence chocolate consumers

European consumers are increasingly attentive to how chocolate contributes to their health and well-being. Beyond enjoyment, chocolate is seen as a product that can provide both physical and mental benefits. This has spurred strong demand for high-quality cocoa, sugar-free and plant-based options, and functional ingredients that align with a healthier lifestyle.

Functional chocolates enriched with ingredients like fibre, vitamins or probiotics experienced an 18% annual rise in product launches throughout Europe in 2024. Globally, the market is valued at US$ 61.8 billion in 2025 and is projected to reach about US$ 106.6 billion by 2032, at a compound annual growth rate (CAGR) of 8.1%.

One key driver is the presence of flavonoids in cocoa, which are associated with lowering blood pressure, improving blood vessel health, and reducing cholesterol. This has helped dark chocolate, which contains higher levels of flavonoids, gain popularity worldwide. Some brands, like The Good Chocolate Company (Belgium), even highlight the flavonoid content on their labels. Manufacturers are also enriching products with extra flavonoids to enhance cardiovascular and brain performance.

Dark chocolate is the fastest-growing chocolate category in Europe, with a projected 5% annual growth until 2029. In France, dark chocolate accounts for 30% of consumption, far above the 5% European average. Consumers in Switzerland also show a high preference, with over two-thirds of consumers favouring dark chocolate. Its antioxidant profile, coupled with premium positioning and sustainability credentials, makes it an interesting product of the health-and-wellness trend.

Another strong health trend is reducing or eliminating sugar. According to Barry Callebaut’s research (2024), 41% of global consumers are trying to limit sugar and 14% avoid it completely. In Europe, over 70% of consumers would like milk chocolate with more cocoa and less sugar. This is reflected in the growth of the sugar-free chocolate market (CAGR of 5.4% for 2025-2032). Companies like Stella Bernrain (Switzerland) and Klingele Chocolade (Belgium) already cater to this demand, while larger brands like Nestlé experiment with natural alternatives like cacao pulp sugar, which also creates new income streams for cocoa farmers. Explore partnerships to extract and process pulp.

With less sugar in recipes, manufacturers will depend more on cocoa for flavour and texture, boosting demand for high-cocoa beans with clean, consistent profiles. This raises the bar on quality control plus tighter specs for fermentation, drying, moisture and defects, so exporters should invest in post-harvest controls, lot segregation and cupping. Offering differentiated flavour portfolios (fruity, nutty, floral, deep cocoa) with samples and flavour notes to buyers can win business.

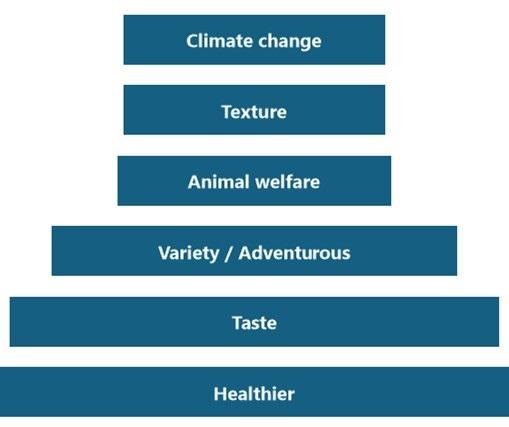

Plant-based chocolates are also gaining traction. Barry Callebaut reports that nearly half of European consumers think every chocolate brand should offer a plant-based, vegan or dairy-free option. Motivations include health, taste and adventure (see Figure 9). In recent years big players have responded to this trend: Lindt & Sprüngli expanded its dairy-free range and Nestlé launched a vegan KitKat in the UK. Younger consumers are particularly attracted to these options, which they see as both healthier and more sustainable.

For plant-based chocolates, cocoa cooperatives and exporters can focus on consistent, low-defect beans and defined flavour profiles suited to vegan milk alternatives (oat, almond, rice). This is because the vegan milk alternatives can mute or shift cocoa notes. Ensure strong sustainability and ethical credentials with certifications like organic, Rainforest Alliance and Fairtrade.

Figure 9: Key motivations to consume plant-based chocolate confectionery

Source: Barry Callebaut, 2023.

In addition, the growing popularity of cocoa nibs reflects consumer interest in nutrient-rich, ‘super food’ ingredients. The cocoa nibs market is projected to reach USD 2.9 billion by 2032. The high magnesium content supports essential body functions and helps prevent diseases like diabetes and hypertension. Cocoa nibs are increasingly used in desserts, smoothies, bakery, snacks and beverages.

Tips:

- To learn more about why chocolate is perceived as a healthy food, read this article in Vox.

- Visit the webpage of hello chocolate to learn more about the benefits of cocoa nibs. This knowledge can be a great resource for marketing your cocoa nibs.

8. Lifestyle choices are also influencing consumer preference

While health and functionality are key drivers, European consumers also make chocolate choices that reflect their values, identity and lifestyle aspirations. Here factors such as organic certification, natural ingredients and ethical sourcing play a central role.

Interest in organic chocolate continues to rise, with over half of European consumers expressing willingness to purchase organic confectionery. Europe is therefore an attractive market for organic cocoa. But organic cocoa imports have decreased considerably in recent years, partly due to high cocoa prices. Organic products are associated with purity, authenticity and environmental responsibility. A well-known example is Green & Black’s in the UK, where ‘green’ signifies organic farming and ‘black’ stands for dark chocolate.

At the same time, consumers are drawn to exotic and natural ingredients, which enhance both taste and perceived quality. Products enriched with fruits, nuts and spices are viewed as more premium by nearly 60% of European consumers. Côte d’Or (Belgium) offers bars with banana, cranberries and pecans; Paul and Mike uses real fruits, spices and floral distillates; and Lovechock (Netherlands) incorporates baobab fruit into its chocolate bars. These innovations appeal to consumers seeking novelty and authenticity in their chocolate experience.

Finally, ethical and transparent sourcing has become an important lifestyle choice. Consumers increasingly want assurance that their indulgence contributes positively to communities and the planet. Brands that highlight fair treatment of farmers, traceability and sustainability gain stronger loyalty. For many consumers, buying chocolate is no longer just about taste but about making a purposeful, values-driven choice.

Tips:

- Read our study What is the demand for cocoa on the European market? to learn more about organic cocoa export from producing countries and imports into Europe.

- Offer different types of chocolate using special healthy ingredients with unique branding. This will give your chocolate company a chance to stand out. Instead of just competing on price, you can meet people’s desires for options with additional health benefits.

- When possible, obtain certifications (organic, vegan, dairy-free) to access niche health-driven market segments.

- Introduce a ‘simple’ line of organic chocolates that exclusively feature organically sourced ingredients, from cocoa and nuts to all other components. Emphasising the cocoa percentage in the recipe will further enhance the product’s reputation for quality.

Amonarmah Consults carried out this study in partnership with Molgo Research on behalf of CBI.

Please review our market information disclaimer.

Search

Enter search terms to find market research

Do you have questions about this research?

When cocoa beans are poorly dried or contain debris, local buying companies usually spend additional time reconditioning and rebagging the beans to meet quality standards. This process often leads to bulking, which makes it difficult to maintain full traceability. Therefore exporters should partner with buyers to invest in farmer capacity-building and provide continuous support, including awareness of EU regulations such as EUDR to help farmers produce cleaner, better-quality cocoa at the source. This can reduce the need for reconditioning and safeguard traceability of cocoa beans regarding EUDR compliance.

Robert Acquah, Shipping manager at Cocoa Marketing Company