Entering the European market for bags for work and school bags

The European market for work and school bags offers opportunities, but competition is strong. China continues to dominate the market, particularly the lower end. Instead, the higher middle segment offers the most opportunities. You can add value through design, functionality, craftsmanship, materials, sustainability and storytelling. To enter the European market, you need to comply with mandatory requirements. You also need to follow any additional or niche requirements your buyers may have.

Contents of this page

- What requirements must work and school bags meet to be allowed on the European market?

- Through which channels can you get work and school bags on the European market?

- What competition do you face on the European market for work and school bags?

- What are the prices for work and school bags on the European market?

1. What requirements must work and school bags meet to be allowed on the European market?

The following requirements apply to work and school bags on the European market. For a more detailed overview, see the CBI’s study on buyer requirements for Home Decorations and Home Textiles (HDHT).

What are mandatory requirements?

When exporting to Europe, you must comply with various legal requirements.

General Product Safety Regulation

The new General Product Safety Regulation (GPSR, EU 2023/988) requires that non-food products marketed in the EU are safe to use. This applies to all non-food products sold online or offline. Non-EU products can only be placed on the market if an ‘economic operator’ in the EU is responsible for their safety. For business-to-consumer (B2C) trade, you must contract an authorised representative or fulfilment service provider.

To prove your products are safe, you must do a risk analysis and write the required technical documentation. Unsafe products are rejected at the European border or withdrawn from the market. The European Union (EU) uses the Safety Gate system to list and share information about such products.

Tips:

- Read more about the GPSR, including the questions and answers (Q&A).

- Use common sense to ensure that normal use of your product does not cause any danger.

- Search the Safety Gate alerts for work and school bags for an idea of potential issues.

Restricted chemicals: REACH

The REACH regulation (EC 1907/2006) lists restricted chemicals in products that are marketed in Europe.

Restricted chemicals in the production of work and school bags include:

- Azo dyes that release prohibited aromatic amines;

- Certain flame retardants, such as TRIS, TEPA and PBBs;

- Chromium VI.

Tips:

- Comply with the restrictions as laid down in REACH.

- Do not use azo dyes that release forbidden aromatic amines. Also check that your suppliers adhere to this and ask them for certified azo-free dyes.

- Explore information and tips from the European Chemical Agency (ECHA), like its list of all restricted chemicals (REACH Annex XVII), information for non-EU companies and questions & answers.

Wildlife Trade Regulations

The EU’s Wildlife Trade Regulations makes sure that wildlife products only enter the EU market if they are of legal and sustainable origin. This affects leather goods, including bags. These regulations enforce the rules of the Convention on International Trade in Endangered Species of Wild Fauna and Flora (CITES). They also go beyond the CITES requirements. For example, they include more species than the standard CITES list and set stricter import conditions.

Tips:

- Check the list of protected species in Annexes A, B, C and D of the Wildlife Trade Regulations to make sure you do not use any prohibited materials.

- The Reference Guide to the Wildlife Trade Regulations is a practical tool that supports implementation.

Intellectual property rights

When you develop products, you must not copy an existing design. Intellectual property (IP) is protected in Europe, and products that violate IP rights are banned from the market.

Tip:

- For more information, see the European Union Intellectual Property Office (EUIPO) and the World Intellectual Property Office (WIPO).

European Green Deal

The European Green Deal is the EU’s roadmap for Europe becoming a climate-neutral continent by 2050. It provides a legal aspect to social and environmental sustainability. One of its main building block is the Circular Economy Action Plan. It includes initiatives throughout products’ full life cycles. It targets how products are designed, promotes circular economy processes and encourages sustainable consumption. The plan also aims to prevent waste and keep the resources used in the EU economy for as long as possible. In this context, legislation is updated and new laws are developed. Some will apply to you directly and some indirectly through your buyers.

Textile Regulation

The Textile Regulation (EU 1007/2011) states that products containing ≥80% textile fibres must be labelled or marked. The label must state the full fibre composition. If applicable, it should also mention the presence of non-textile parts of animal origin. It must be durable, easily legible, visible and accessible. The label should be printed in all the official national languages of the European countries where the product is sold.

There is no EU-wide legislation on symbols for washing instructions and other care aspects. To give consumers clear information, you should follow the ISO 3758:2023 standard for graphic symbols in care labelling.

The European Commission plans to revise the regulation to introduce specifications for physical and digital labelling of textiles, including sustainability and circularity parameters based on the new Ecodesign for Sustainable Products Regulation.

Tips:

- Read more about the Textile Regulation. Also see the FAQ.

- Find out more about textile labelling rules from Access2Markets.

- Stay updated on the revision of the Textile Regulation.

Ecodesign for Sustainable Products Regulation

The new Ecodesign for Sustainable Products Regulation (ESPR – EU 2024/1781) entered into force in 2024. It aims to ensure that products:

- Are designed to last longer;

- Are easier to reuse, repair and recycle;

- Incorporate recycled raw materials wherever possible.

The regulation also introduces Digital Product Passports with information about products’ environmental sustainability. This includes their durability and use of recycled materials. The Commission adopted the first working plan in April 2025, which includes textiles. The first measures could be adopted in 2027 and be applicable 18 months later.

Tips:

- Read more about the ESPR. Also see the FAQ, Q&A and factsheet.

- Stay updated on the implementation of the ESPR.

Deforestation Regulation

You should know that the new Deforestation Regulation (EUDR – EU 2023/1115) does not currently apply to any leather bags exported to Europe. This regulation aims to reduce the EU’s impact on global deforestation and forest degradation. It applies to cattle and derived products, such as leather. This is because many trees are cut to create space to raise cattle. However, it does not cover finished products like leather bags.

Corporate Sustainability Due Diligence Directive and Forced Labour Regulation

The Corporate Sustainability Due Diligence Directive (CSDDD – EU 2024/1760) requires larger companies to identify and prevent, end or reduce any negative impacts of their activities on human rights and the environment. The CSDDD applies to both the company’s own operations and its direct business partners. This means that the new rules may apply to you indirectly via your buyers. The European Commission plans to publish guidelines to help companies conduct due diligence.

In February 2025, the European Commission proposed an Omnibus package to simplify sustainability due diligence requirements. As part of this, the European Parliament has agreed to postpone the application dates of the CSDDD. The CSDDD is now set to apply following a staggered approach. It will apply to the first group of companies from 26 July 2028 until full application on 26 July 2030.

Besides that, the Forced Labour Regulation (FLR – EU 2024/3015) bans products made with forced labour. The FLR will apply from 14 December 2027.

Packaging legislation

The Packaging and Packaging Waste Directive (PPWD – 94/62/EC) aims to prevent or reduce the impact of packaging and packaging waste on the environment. Buyers may therefore ask you to minimise the use of packaging materials and/or to use sustainable (recycled) materials.

By 2030 all packaging on the European market should be reusable or recyclable in an economically viable way. To help achieve this, the new Packaging and Packaging Waste Regulation (PPWR – 2025/40) entered into force in February 2025. This regulation will apply from 12 August 2026, replacing the PPWD.

The Plant Health Law (EU 2016/2031) also sets requirements for wood packaging materials used for transport, such as packing cases and pallets. The goal is to prevent organisms that are harmful to plants or plant products from entering and spreading within the EU.

Tip:

- Read more about the EU rules on packaging and packaging waste and the requirements for wood packaging materials.

Pending: Green Claims Directive

The European Commission has proposed a Green Claims Directive to:

- Make green claims reliable, comparable and verifiable;

- Protect consumers from greenwashing;

- Contribute to a circular and green economy;

- Help create a level playing field when it comes to the environmental performance of products.

The proposal is currently awaiting approval. If the Directive is approved, any green claim you make about your product has to meet certain requirements. These requirements will apply to how you prove and verify your environmental claims, and to how you communicate about them. The same goes for any claim your buyer makes. Until then, 2 current directives already ban misleading and false environmental green claims: the Unfair Commercial Practices Directive (2005/29/EC) and the new Directive to empower consumers for the green transition (EU 2024/825, which enters into force on 27 September 2026.

Tips:

- For details, see the Q&A and factsheet.

- Stay updated on the proposed rollout of the Green Claims Directive.

- For help with communicating your sustainable performance honestly and effectively, see the Netherlands’ guidelines regarding sustainability claims and/or the British guidance for businesses on making environmental claims.

What additional requirements do buyers often have?

Buyers often have additional requirements related to sustainability, labelling/packaging, and payment/delivery terms.

Sustainability

Social and environmental sustainability are becoming more and more important in the European market. Environmental sustainability is about your company’s impact on the environment. For example through the raw materials you use or your production processes. Social sustainability focuses on your company’s impact on the wellbeing of your workers and the community. Key topics include fair wages and safe working conditions.

In addition to legal compliance, a growing number of European buyers would like you to comply with:

- Business Social Compliance Initiative (BSCI): an initiative of European retailers to improve social conditions in sourcing countries. They expect their suppliers to follow the BSCI Code of Conduct.

- Ethical Trading Initiative (ETI): an alliance of companies, trade unions and voluntary organisations. ETI aims to improve the working conditions in global supply chains via their ETI Base Code of labour practice.

- Sedex: a membership organisation striving to improve working conditions in global sourcing chains. The platform lets you share your sustainable performance, based on a self-assessment. You can also be SMETA audited.

You can also learn about sustainable options from standards such as ISO 14001 and SA8000. These standards enable certification, but most buyers do not require this.

Tips:

- Optimise your sustainability performance. Study the issues in initiatives like BSCI and ETI to learn what to focus on.

- If you can show your sustainability performance, this may give you a competitive advantage. For example, ITC’s Green Performance Toolkit helps small textile businesses assess and track their environmental performance and identify improvement areas. You can also use a code of conduct like the ETI base code.

- For more information, see our special study on sustainability in HDHT, our tips to go green and become socially responsible, and our webinars on sustainability in the European HDHT market, sustainable innovations for your HDHT business and the sustainable transition in apparel and home textiles.

- Read more about BSCI, ETI, Sedex and SA8000 in the ITC Standards Map. You can also conduct a free online self-assessment.

- Highlight your sustainable activities and policies in the ‘stories’ behind your product and company. Buyers like good storytelling that creates an emotional connection.

Labelling

The information on the product’s outer packaging should correspond to the packing list sent to the importer.

External packaging labels should include:

- Name of producer;

- Name of consignee;

- Quantity;

- Size;

- Volume;

- Warning labels.

Your buyers will specify what information they need on product labels or on items themselves, such as logos or ‘made in…’ information. This is part of the order specifications. In Europe, EAN or barcodes are commonly used on the product label.

Packaging specifications

Importer specifications

You should pack your work and school bags according to the importer’s instructions. They have their own specific requirements for packaging materials, filling boxes, palletisation and stowing containers. Always ask for the importer’s order specifications. These are part of the purchase order.

Damage prevention

Proper packaging minimises the risk of damage through dirt, temperature or humidity. It should make sure the items inside a cardboard box cannot damage each other and prevent damage to the boxes when they are stacked inside the container. Packaging usually consists of an outer cardboard box lined with protective material, like plastic wrapping. The actual products are generally packed in polybags or bubble wrap.

Dimensions and weight

Packaging needs to be easy to handle in terms of size and weight. Standards are often related to labour regulations at the point of destination and must be specified by the buyer.

Cost reduction

Boxes are usually palletised for transport, and you have to maximise the use of pallet space. Packaging has to provide maximum protection. However, you need to avoid using excess materials or shipping ‘air’. Waste removal is a cost to buyers.

Material

Importers are increasingly banning wooden crating and packaging. Economical and sustainable packaging materials are more popular. Using biodegradable packaging materials can be a market opportunity. Some buyers may even demand it.

Consumer packaging

Retailers usually present work and school bags without any packaging. This allows consumers to try them out and feel the material. If your buyer wants consumer packaging, they will let you know.

Tips:

- Always ask for the importer’s order specifications, including their packaging and labelling requirements.

- See Packaging Europe for more information on the latest packaging developments.

Payment and delivery terms

Payment terms are confirmed in the order contract. They vary from buyer to buyer and are related to the volume and value of the order, the type of distribution partner, whether or not an agent is involved, and what delivery terms apply.

Delivery terms, known as Incoterms, depend on the type of distribution partner. HDHT importers generally prefer Free On Board (FOB) or Free Carrier (FCA) arrangements.

Tips:

- See our tips on how to organise your exports for more information.

- Study the different Incoterms, including your and your buyer’s rights and obligations.

- See our study on terms & conditions for a more elaborate overview, how to work with them, and the benefits of having your own.

What are the requirements for niche markets?

Fair-trade practices and sustainability certification are the most common niche market requirements.

Fairtrade

The concept of fair trade supports fair pricing and improved social conditions for producers and their communities. Fairtrade certification can give you a competitive advantage. This is especially if the production of your bags is labour-intensive. It often also includes aspects of environmental sustainability.

The World Fair Trade Organisation (WFTO) Guarantee System and Fair for Life certification are common fair trade labels. For most fair trade oriented buyers in Europe, however, simply complying with WFTO’s 10 principles of fair trade is enough.

Tips

- Ask buyers what they are looking for. Especially in the fair trade sector, you can use the story behind your product for marketing purposes.

- If certification is not feasible, work according to WFTO’s principles without being officially guaranteed or certified. Carefully document your company processes so you can support your story.

- Read more about Fair for Life in the ITC Standards Map.

Sustainable textiles

Buyers are increasingly interested in certification to ‘prove’ their sustainability.

Popular textile certifications include:

- Global Organic Textile Standard (GOTS) – a textile-processing standard for organic fibres that ensures environmental and social responsibility throughout the production chain.

- OEKO-TEX Standard 100 – certification that guarantees textile articles are free of harmful substances.

- OEKO-TEX Made in Green combines Standard 100 and STeP.

Other options include the Nordic Swan eco-label (in Nordic countries) and the EU Ecolabel.

Tips:

- Explore the possibility of sourcing organic materials. Textile products containing ≥70% organic fibres can be GOTS certified. The easiest option is to use certified yarn or fabric.

- Read more about GOTS, OEKO-TEX Standard 100 and Made in Green, and the EU Ecolabel in the ITC Standards Map.

Recycled materials

The Global Recycle Standard (GRS) is a standard for products containing recycled material. It has criteria for environmentally friendly production and good working conditions. Products containing ≥20% recycled material can be GRS-certified, but only if the entire production process is certified. Additional social, environmental, and chemical requirements must also be met. For consumer-facing labelling, the product must contain ≥50% recycled content. If you use GRS-certified material, you can highlight in your communication that this material is certified.

Similarly, the Recycled Claim Standard (RCS) is intended for products containing ≥5% recycled material. The RCS does not address social or environmental aspects of processing and manufacturing.

Video 1: Water-repellent backpack made from GRS-certified recycled polyester with padded laptop compartment

Source: Cabaïa Officiel

Tips:

- Check for GRS/RCS-certified versions of the materials you use, as an alternative or addition.

- Carefully check the specifications of the available certified materials. Sometimes composition changes due to the recycling process.

- When using GRS/RCS-certified materials, communicate this correctly.

- Read more about the GRS and RCS in the ITC Standards Map.

Sustainable leather

Sustainable labelling options for leather include:

- OEKO-TEX Leather Standard: certification that guarantees leather articles are free from harmful substances;

- Leather Working Group: certification standard for leather manufacturers, leather traders, commissioning manufacturers and subcontractors that covers environmentally and socially responsible leather manufacturing;

- Sustainable Leather Foundation: audit certification for facilities throughout the leather value chain.

OEKO-TEX Made in Green certification is also available for leather products.

Tips:

- Explore the possibility of sourcing certified materials.

- See the OEKO-TEX Leather Standard supplement for special articles for the certification of suitcases, bags and backpacks.

2. Through which channels can you get work and school bags on the European market?

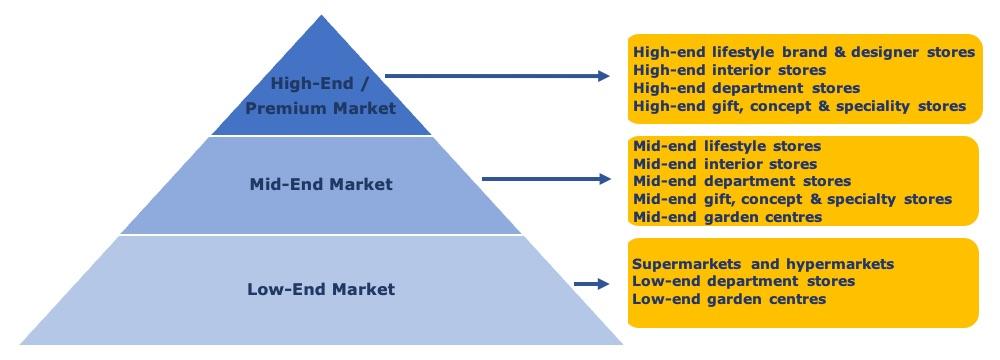

Work and school bags are put on the market through importers/wholesalers that supply to retailers, as well as retailers that buy from suppliers directly. The market consists of low, mid and high-end (premium) segments.

How is the end-market segmented?

Figure 1: Market segmentation for work and school bags in Europe

Source: Globally Cool, GO! GoodOpportunity & Remco Kemper

Low-end market

Price and functionality are most important in the low-end segment. As such, the bags made for this part of the market are simple and inexpensive. Archetypal retailers include department stores like HEMA. Value addition is hard, which means this segment offers limited possibilities to differentiate from low-cost mass production. Instead, the higher middle segment is most suitable for small or medium-sized enterprises (SMEs) from developing countries.

Mid-end market

The mid-end market follows trends at reasonable prices. It puts more emphasis on design, material and finish. Relevant players in this market include department stores like Marks & Spencer and speciality shops like Van Os.

Especially at the higher end of this segment, handmade craftsmanship and sustainable values play a larger role. As such, the mid-high segment offers you the most opportunities. To appeal to these consumers, you can add value to your bags through design, functionality, craftsmanship, materials, sustainability and storytelling.

High-end market

Trends, materials, finishing and design play a key role in the high-end market. Work and school bags in this segment often come from well-known brands and are purchased from high-end department stores like Selfridges. Top luxury brands also often have their own stores.

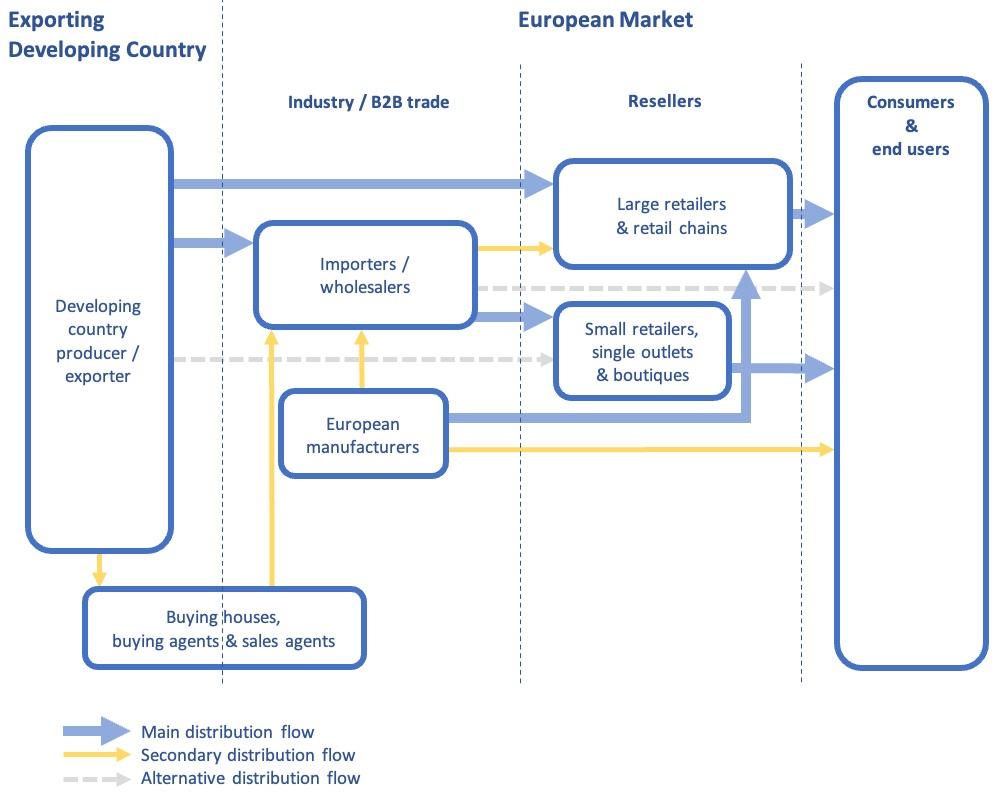

Through which channels do work and school bags end up on the end-market?

Market access channels for work and school bags mainly follow traditional patterns. Importers and wholesalers supply retailers. Larger retail chains often bypass them and import themselves. However, more smaller retailers have also started buying from suppliers directly. Buying agents can also play a role.

Figure 2: Trade channels for work and school bags in Europe

Source: Globally Cool, GO! GoodOpportunity & Remco Kemper

Importers and wholesalers

Importers and wholesalers sell products to retailers in their own countries or regions, or re-export across Europe. These importers and wholesalers handle import procedures. Unlike agents. they take ownership of the goods when they buy from you. They also take on the risk of the onward sale of the products. Developing a long-term relationship can lead to a high level of cooperation on appropriate designs for the market, new trends, use of materials, types of finishing and quality requirements.

Importing retailers

Retailers come in many sizes: large and part of a chain, or small and independent. Especially larger retail chains often import directly from their suppliers in developing countries. Many even have their own buying offices in developing countries. Others – mainly smaller independent stores – order in Europe from wholesalers.

There is a tendency for consolidation in European retail. Large retail brands are becoming more widespread and more ‘lifestyle-centred’. They offer home and office goods as well as decor, textiles and fashion accessories.

Buying agents, buying houses and sales agents

You can encounter several types of intermediaries in your dealings with European buyers:

- European buying agents: represent European buyers in sourcing countries, but do not import products themselves. Sometimes they have a more limited role, such as checking product quality. They can work individually or as part of a purchasing company.

- Buying houses: comparable to buying agents, but they are based in your country and usually offer more services. These can range from raw material sourcing to design and sampling services.

- European sales agents can help you find European buyers. However, you should be careful about entering into agreements with commercial agents, because European legislation protects their position.

Agents and buying houses mostly work on commission. They may approach you, or your buyer may request an intermediary. However, you should always try to work directly with your buyer. This saves on commission and allows you to communicate directly.

E-commerce

E-commerce has grown in recent years. Your easiest way to benefit is by supplying to a European wholesaler or retailer with a strong online presence. This is usually not a separate channel. Retailers often combine online and offline channels, and the way of supplying to them is the same. Companies that only sell online also need to take stock before they can sell.

Direct business-to-consumer (B2C) sales

Selling directly to European consumers can be complicated and costly. You need an ‘economic operator’ in the EU, and you are responsible for factors like aftersales obligations. For most exporters from developing countries, this is not feasible.

Tips:

- To find buyers, search the exhibitor lists or visit the main trade fairs in Europe: Ambiente and Maison&Objet. For leather bags, it may be useful to visit Mipel in Italy.

- See the CBI’s tips for finding buyers in the European HDHT market.

- For more information about trading directly with smaller retailers and e-commerce, see the CBI’s study on market channels and segments.

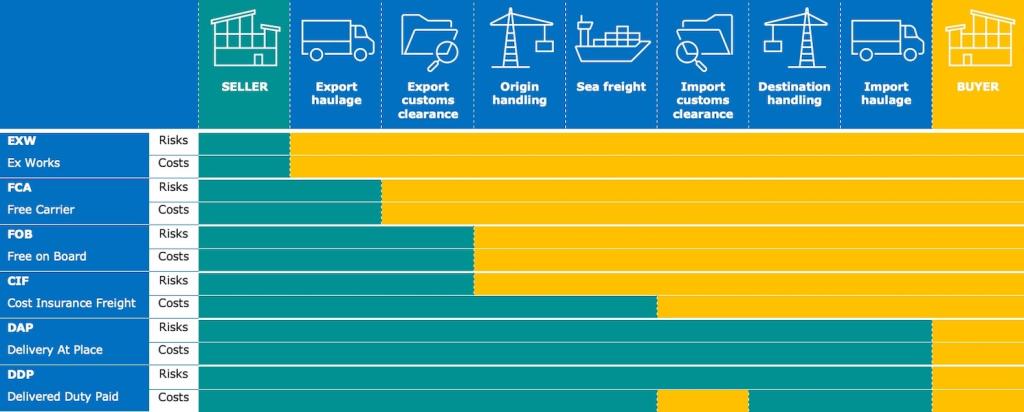

What is the most interesting channel for you?

Importers/wholesalers are the main channel between exporters in developing countries and European retailers. They are interesting if you want to develop a long-term relationship. These importers usually know the European market well, so they can provide valuable information and guidance on market preferences. They generally prefer FOB or FCA Incoterms.

Figure 3: Incoterms

Source: Globally Cool, GO! Good Opportunity & Remco Kemper

Large retailers are handling their own imports more and more. This helps them cut out the margins of importers/wholesalers, reduce time to market. It also allows them to have more control over product design and finish.

Smaller, independent retailers need to set themselves apart from retail chains. They can do so through value-added service, specialised offers and authenticity. So buying directly from producers in developing countries is interesting for them. They typically prefer small order quantities per item and small total order volumes. These retailers also want delivery to their doorstep via Delivered Duty Paid (DDP) or Delivery At Place (DAP). Repeat orders are less likely. You need to calculate if this is cost-effective for you.

The trend of direct sourcing is expected to continue. This may create more opportunities for you, as a growing pool of buyers could improve your bargaining position. Importers/wholesalers may need to show samples to their retailers before ordering. Importing retailers order for their own shop, so they can place orders much quicker.

Tips:

- Consider targeting retailers directly to improve your bargaining position and potentially close deals faster.

- Relate your offer and terms to the targeted retailer (large/small). Ask your existing buyers how they operate if you are unsure.

- Build a relationship based on mutual benefits by offering services like fast delivery and after-sales support.

- If you are interested in selling to small independent retailers, make sure you have a policy in place when you participate in trade fairs. You must have appropriate terms of trading, such as low minimum order quantities.

3. What competition do you face on the European market for work and school bags?

China is Europe’s leading supplier of work and school bags. It mainly supplies mass-produced items for the lower-end segments. Instead of competing with these manufacturers, your best opportunities are in the mid-high market, where you can add value.

China is Europe’s main supplier of work and school bags by far. It provided 36% of imports in 2024. Italy follows with 12%. The next largest are Germany (9.6%), the Netherlands (7.7%), France (5.3%) and Belgium (3.9%).

Re-exporters or producers

European countries have different roles in the HDHT market. Some are mainly importers and others are mainly manufacturers. Western European countries are mainly importers. Most Western European importers are re-exporters. They do not just sell their products in their own countries but distribute them across the continent.

European production mainly takes place in Eastern Europe.This is mostly because of relatively low transport and labour costs. This can make these countries a good alternative for European buyers to source low to mid-end products. Western and Southern Europe also produce high-end products from well-known premium brands with long histories. Italy is particularly well-known for its production of high-end leather bags, often made for Italian luxury fashion brands.

Which countries are you competing with?

Most competition comes from China, India, Czechia and Vietnam.

Source: Eurostat Comext & ITC TradeMap, 2025

China dominates the lower-end market

Chinese exports of work and school bags to Europe peaked at €284 million in 2022, before returning to €197 million in 2024. This was comparable to 2020. With this, China’s direct import market share dropped from 39% in 2022 to 36% in 2024. Nearly all of these bags were made from plastic or textile materials.

Chinese producers mainly supply the lower ends of the market with low-priced products. China’s strengths are its low-cost workforce, the availability of raw materials and efficient shipping to Europe. However, rising labour costs have affected its price competitiveness. In the coming years, China’s trade war with the United States and other disruptions may further affect exports. European importers increasingly want to diversify their collections and become less dependent on China. This could benefit suppliers from other developing countries.

To avoid having to compete with Chinese suppliers on costs, you should stay away from mass-produced bags. Focus more on your product’s design, functionality, craftsmanship, sustainability and story. This allows you to enter the mid-end market.

Unfair competition from non-compliant e-commerce platforms

Although cheap Chinese e-commerce platforms have become more popular, they are subject to product quality issues and ethical concerns. In November 2024, the European Commission urged Temu to respect EU consumer protection laws following various infringing practices. The Commission has opened formal proceedings against Temu to assess whether it breached the Digital Services Act in areas linked to the sale of illegal products, for example. Similarly, the Commission has sent several requests for information to SHEIN. In May and June 2025, the European consumer authorities established that SHEIN violated consumer protection law and filed a complaint.

To achieve a safer, more sustainable and fairer market, the European Commission published its E-commerce Communication. This toolbox for safe and sustainable e-commerce features coordinated customs controls and product safety checks. It also proposes to remove the €150 duty exemption and introduce a simplified customs duty calculation for the most common low-value goods bought from outside the EU.

India mainly exports leather bags to Europe

India has been Europe’s eighth largest supplier of work and school bags since 2022. The country generally exports about €18 million worth of work and school bags to Europe per year, with a peak of €22 million in 2022. Most of these supplies are leather bags – 84% in 2024.

A lot of India’s work and school bag exports to Europe are contract manufacturing. However, Indian brands are also becoming more established in international markets. The country specialises in craft-designed and handmade products, as opposed to mass-produced factory-made products. This allows Indian producers to compete in the mid-end segment, instead of competing on cost at the lower ends of the market.

Eastern European suppliers are conveniently located

Czechia and Poland were Europe’s ninth and tenth largest suppliers of work and school bags in 2024. Eastern European countries like these can benefit from their location, allowing for short delivery times. At the same time, labour is relatively affordable compared to Western/Northern Europe. Suppliers have a good understanding of the European consumer and have well-established efficient production lines.

However, Czechia’s exports of work and school bags to other European countries fluctuated between 2020 and 2024. Overall, they declined from €21 million to €14 million, at a compound annual growth rate (CAGR) of -9.3%. Nearly all of these bags were made from plastic or textile materials (90% in 2024). About one third were exported to Czechia’s neighbour Germany.

Poland’s exports of work and school bags to other European countries also fluctuated. Overall, they grew from €10 million in 2020 to €13 million in 2024 at a CAGR of 6.9%. This was mainly due to strong performance in Germany. It accounted for nearly 40% of Poland’s supplies to Europe in 2024. 29% of the 2024 exports were leather bags.This is comparable to average European imports.

Vietnam is another low-cost producer

Vietnam is a longstanding alternative to China. It offers outsourced contract manufacturing at attractive prices. Vietnamese suppliers are very productive and can produce at low costs. These suppliers generally have a good idea of what is commercially viable and trendy in Europe. They combine handmade and mechanised production and can cater to a wide range of lower and mid-end markets. This may allow them to benefit from potential disruptions in trade with China.

The country’s exports of work and school bags to Europe peaked strongly in 2022, when they more than doubled to €24 million. Overall, they declined from €12 million to €11 million, at a CAGR of -2.5%. Vietnam mainly exports to European trade hubs Germany and the Netherlands. In recent years, its main focus shifted between these countries. In 2020 71% of Vietnam’s supplies to Europe were destined for the Netherlands but, in 2024, 57% were exported to Germany. ≥90% of these bags were made from plastic or textile materials.

Which companies are you competing with?

The following companies are examples of the competition you will face in the European market.

reCharkha, India

reCharkha is a female-founded social enterprise, named after the traditional spinning wheel. This organisation’s identity is built around sustainability. They strive to enable livelihoods for tribal and rural women, and to conserve the environment and their local heritage. The women artisans use the traditional Charkha and handloom to hand-roll and hand-weave waste plastic into fabric. With this colourful upcycled fabric, they make products like laptop bags and sleeves, backpacks and home decorations.

Video 2: Upcycled handwoven commuter backpack

Source: My EcoSocial Planet & reCharkha-The EcoSocial Tribe

On their website, reCharkha specifies the impact of each product. For example, the commuter backpack provides 3 days of work for the tribal artisans and is made with 40 to 45 plastic bags and wrappers. The compact yet spacious multi-pocket backpack features a laptop compartment and various zip pockets. It also has a bottle holder, a key holder, and a trolley strap to attach the backpack to a suitcase. The straps and handle are cushioned. Such additional functionality is a good way to add value to the stylish bags.

WSDO, Nepal

WSDO (Women's Skills Development Organization) is a non-profit organisation that supports women who face social and economic hardships. Its goal is to improve the quality of life of women in Nepal by empowering them with new skills to be self-supportive. To achieve this, WSDO provides free training and employment opportunities throughout the production process and management. Being WFTO Guaranteed, WSDO pays fair wages and minimises its environmental impact by using local materials and eco-friendly dyes (natural/azo-free).

Video 3: WSDO - Women's Skills Development Organisation

Source: Fair Trade Connection

About 80% of WDSO’s products are exported. They are traditional and craft-based, with a contemporary touch. To make these products, the artisans process the raw materials (mainly cotton) before weaving on a backstrap loom. The fabrics they create are then made into products like laptop and tablet bags, cases, backpacks and home textiles in various styles.

Kabana, Ethiopia

Kabana is a leather goods company that cares about people and the environment. They pay their workers fair wages of about 4 times the local average. Most of their team are women. They include single mothers, refugees and women with disabilities. Kabana intentionally hires more women, “to compensate [for] the big gap created in the male-dominated manufacturing industry.” The company offers maternity leave and daycare for children. They also provide technical and soft-skills training. It has inspired some former employees to start their own businesses.

About 92% of the materials Kabana uses come from Ethiopia, including sheep and goat leather and canvas. Most of Kabana’s bags are made with vegetable-tanned leather. Their designs are classical and suitable for all seasons. For example, the Annetta laptop bag from Kabana’s timeless basics series is made from antique vegetable-tanned leather that softens over time. This simple but elegant design focuses on functionality. The Bereket backpack from the craftsmanship series, meanwhile, features soft and smooth leather that showcases the line stitch design.

Which products are you competing with?

Competition mostly comes from within the category of bags. Consumers have a wide range of options, as they can choose between different styles, designs, materials and features. Preferences can depend on personal taste, values or context. For example, some may prefer a brightly coloured recycled PET backpack. But others may opt for a more formal neutral-toned leather briefcase.

Tips:

- Compare your products and company to the competition. You can use ITC Trade Map to find exporters per country.

- Focus on design, functionality, craftsmanship, materials, your sustainable values and the story behind your products to stand out from your competitors.

4. What are the prices for work and school bags on the European market?

Prices for work and school bags vary across market segments. After adding logistics costs, wholesaler and retail margins, and Value Added Tax (VAT), European consumer prices are about 4 to 6.5 times your selling price.

Table 1 gives examples of prices across market segments. Be aware that these are just indicative, since prices vary depending on material, design, brand and other aspects of value addition, including a strong sustainable concept.

Table 1: Indicative consumer prices of work and school bags

| Low-end | Mid-end | High-end | |

|---|---|---|---|

| Briefcase | €15–30 | €30–200 | €200 or more |

| Backpack | €8–20 | €20–150 | €150 or more |

| Laptop sleeve | €3–15 | €15–100 | €100 or more |

| Crossbody bag | €10–25 | €25–125 | €125 or more |

| Messenger bag | €8–20 | €20–150 | €150 or more |

Consumer prices depend on the value perception of your product in a particular segment. This is influenced by your marketing mix.

Figure 5: Marketing mix – the 4 Ps

Source: Globally Cool, GO! Good Opportunity & Remco Kemper

The European consumer price of your bags is about 4 to 6.5 times your FOB price. Besides energy, labour and transport costs, FOB prices depend heavily on the availability and cost of raw materials. Occasional cost increases are not passed on to the consumer directly. So they put pressure on margins in the supply chain. However, disruptions have resulted in longer-term cost increases. This pressure has made many European retailers raise their consumer prices. If costs drop again, consumer prices may follow.

Consumer prices are generally made up of:

- Your FOB price;

- Shipping, import, handling costs;

- Wholesaler margins;

- Retail margins;

- VAT – varies per country, about 20% on average.

Figure 6: Price breakdown indication for work and school bags in the supply chain

Source: Globally Cool, GO! Good Opportunity & Remco Kemper

In Table 2 the FOB price is set at €10. Depending on the market segment your product is designed for, the consumer price ranges from €41 in the low-end market to €65.50 in the high-end market.

Table 2: Example of the price breakdown per market segment

| Low margin | Middle margin | High margin | ||

|---|---|---|---|---|

| FOB price | €10 | €10 | €10 | Your FOB price |

| Transport, handling charges, transport insurance, banking services (20/15/15%) | +2.00 €12.00 | +1.50 €11.50 | +1.50 €11.50 | Landed price for the wholesale importer |

| Wholesalers' margins (50/75/90%) | +6.00 €18.00 | +8.60 €20.10 | +10.40 €21.90 | Selling price from the wholesale importer to the retailer |

| Retailers' margins (90/110/150%) | +16.20 €34.20 | +22.20 €42.30 | +32.70 €54.60 | Selling price excluding VAT from the retailer to the end consumer |

| Selling price incl. VAT (20%) | +6.80 €41.00 | +8.50 €50.80 | +10.90 €65.50 | Selling price including VAT from the retailer to the end consumer |

The FOB price of €10 includes your margins. These depend on your efficiency and price setting. Margins in the lower segment are generally smaller than those in the middle and higher segments.

Examples of consumer prices:

- OEKO-TEX certified cotton children’s backpack, Søstrene Grene, €13.98

- Recycled PET backpack with laptop compartment and vegan leather details, Nortvi, €139

- Handmade leather laptop bag with metal details and cotton lining, Venice Leather, €189

Tips:

- Study consumer prices in your target segment to determine your price and adjust your cost accordingly. Your quality and price must match your chosen target segment.

- Calculate your prices regularly and carefully, especially if the prices of your raw materials fluctuate. If raw material prices put pressure on your margin for a longer period, consider increasing your price or finding an alternative.

- Understand your segment and offer a marketing mix that meets consumer expectations.

Globally Cool carried out this study in partnership with GO! GoodOpportunity and Remco Kemper on behalf of CBI

Please review our market information disclaimer.

Search

Enter search terms to find market research

Do you have questions about this research?

When it comes to leather bags, buyers mostly ask for Leather Working Group certification. Working with a certified tannery also provides traceability, which makes it easier to comply with European legislation.

Taslima Miji, Founder at Leatherina and Gootipa, Bangladesh