Which trends offer opportunities or pose threats in the European coffee market?

The European coffee market is changing. Because they want convenience, customisation, and product innovation, young consumers drink their coffee differently from older generations. These and other factors increase demand for ready-to-drink coffee and shift focus towards healthy coffee consumption and high-quality (specialty) coffee.

Sustainability concerns are a main driver for other trends. The EU pushes new laws and directives to make soft commodity supply chains more sustainable. However, companies are also taking the initiative. Companies are adopting private standards, and regenerative agriculture is gaining importance.

All of this is happening in a context where prices are changing constantly. Increasing prices force players in the coffee market to adapt. Lastly, technological progress, especially artificial intelligence (AI), is changing how firms run their processes.

Contents of this page

- The ready-to-drink market grows

- Health concerns change consumer behaviour

- The specialty coffee segment continues to grow

- Coffee prices are increasing

- Mandatory sustainability rules are reshaping the coffee sector

- Regenerative agriculture is gaining ground

- Company standards gain importance

- Artificial intelligence will transform the coffee sector

1. The ready-to-drink market grows

The ready-to-drink (RTD) coffee market has grown a lot in recent years. Consumers want convenience, premium quality, perceived health benefits and variety. This results in greater availability of RTD options. These range from iced coffee in bottles and cans to premium cold brew and nitro variants.

Convenience drinks, like bottled and canned coffee drinks, have become popular alongside at-home brewing. The broader ‘Specialty Coffee Beverages’ category includes RTD coffee. Examples in the RTD category include Starbucks’ chilled bottled Frappuccino, Wakuli’s Nitro Cold Brews, Costa Coffee’s canned lattes, and Chameleon Organic's cold brew concentrates and bottles. Coca-Cola (including Costa Coffee) is the largest player in the RTD sector, closely followed by Starbucks and Nestlé. Germany is Europe’s main RTD coffee market.

The future of the European ready-to-drink market

Currently, the RTD market is much larger in the United States. As Europe follows the United States in many consumer trends, the European RTS market will likely grow in the next one to three years. In the long term, RTD coffee will keep expanding, driven by the growing Generation Z (Gen Z) market. Gen Z shows a high willingness to purchase innovative coffees.

According to a study by Global Data, the RTD market is growing more in value than in volume. This means RTD coffees will become more expensive. The main European growth markets are Hungary, Portugal and Austria.

It is uncertain whether the European RTD market will ever reach US levels. Local habits and preferences might limit how big the market can get. Europe’s strong cafe culture may keep the market smaller than in America. Many Europeans prefer drinking in cafes. This especially applies to Southern European countries like Italy, France and Spain. This limits the RTD market, which is mainly sold in supermarkets. Europeans also have a higher preference for hot coffee. In Europe, coffee consumption is a cultural habit. Older generations in particular will not change these habits easily.

2. Health concerns change consumer behaviour

Consumers more and more seek beverages that align with their wellness goals. Awareness of coffee’s potential health benefits and product innovations drive this trend. Health concerns will likely continue to gain importance in the coming years. Gen Z, entering the consumer market, drives this trend.

Popular products enriched with functional ingredients include:

- Coffee with vitamins, such as Nespresso’s Coffee+ range;

- Coffee with mushrooms extracts, such as Super Foodies functional coffee;

- Coffee with proteins, such as Melkunie’s Protein coffee latte.

These ingredients are often added to RTD coffee, including a marketing story. Many consumers also seek milk alternatives for their coffees. Alongside interest in coffee with added ingredients, there is also a notable preference for lower caffeine intake. This offers market opportunities for reduced-caffeine blends, half-caffeine and decaffeinated varieties. Decaffeinated (decaf) coffee is being rebranded as a mindful choice. Many Europeans also limit their coffee consumption to reduce their caffeine intake.

This trend only offers opportunities for some coffee exporters, active in specific niche markets. This means exporters of decaffeinated coffee, or coffee varieties such as Laurina, which are low in caffeine. Exporters of roasted coffee can tap into this market by adding extra ingredients to their coffee.

Some examples of companies tapping into this trend are:

- El Quetzal is a roaster of green and roasted coffee. The company also sells Laurina coffee, which is low in caffeine.

- Juan Valdez is a Colombian company that produces decaffeinated coffee.

Tips:

- Read our studies on roasted coffee to learn more about these markets.

- If you export large quantities of standard-quality coffees, identify European roasters that manufacture private-label packaging, single origins, coffee blends, ready-to-drink products (RTD), pods, capsules or importers that supply these roasters. Approach these companies to sell your green coffee directly. Many single-serve manufacturers use bulk coffee, which is often Rainforest Alliance certified.

- Read our study on how to find buyers in the European coffee market for more information.

- Learn about low-caffeine coffee varieties (e.g. Laurina and Aramosa).

3. The specialty coffee segment continues to grow

The European specialty coffee market has grown for years and continues to do so. Consumers want high-quality, unique coffee experiences. Some consumers are willing to pay more for coffees with good origin stories. Globally, younger generations are driving this trend due to their interest in sustainability and ethical sourcing.

Demand for specialty coffee is rising across various channels, with an increase in independent specialty coffee roasters and cafés. The rise of e-commerce also contributes to this trend. It provides better access to specialty coffee. The continued expansion of e-commerce platforms and collaborations between supermarkets and local roasters indicate that specialty coffee is becoming more mainstream.

In the coming years, many different coffee blends for wider taste profiles will enter the market. These blends range from single-origin beans to drinks flavoured with local ingredients. This creates opportunities for suppliers of high-quality coffee to expand. Some relevant developments and concepts within the specialty coffee market are given below.

Signature blends

These are carefully selected coffees from different origins. They have unique taste profiles. Examples include blends by Coffee Masters (United Kingdom), Taf (Greece) and Flying Roasters (Germany).

Single origin and geographical indicators

Single origin is associated with high quality and uniqueness from a certain region or country. Growers from Ethiopia, for example, rely on the uniqueness of their origins, which is considered the birthplace of coffee. Peruvian producers also promote their origins, with their national coffee brand Cafés del Peru. This was launched in 2019. Other examples of single origins are Jamaican Blue Mountain, Hawaii Kona, Kenya AA and Guatemala Antigua.

Single farm or estate

Coffee sourced from a single farm is called single farm or single estate. Examples include Tanzanian Kifaru Coffee and the Salvadorian Finca el Cerro.

Micro lots and nano lots

The specialty coffee market sees an increase in micro and nano lots. These lots consist of extremely high-quality coffee beans, which are sold for very high prices. Micro lots usually consist of 10–75 bags. Nano lots are smaller. They consist of fewer than five bags of coffee of exclusive quality. Micro and nano lots allow more direct relations between producers and smaller buyers, such as specialised traders and small-scale roasters. This opens an interesting opportunity for top-quality and value-added coffees. However, volumes are low, and the costs for preparing these lots for export and the logistical expenses are high. Micro and nano lot coffees usually do not represent a coffee producer’s core business. They are mainly used to boost the producer’s reputation as it shows they have the skills to produce and process interesting varieties.

Infused coffee

Infused coffees offer complex and new flavours. Infusion can occur at different stages of the coffee-making process. This can occur before or after roasting, or even when the coffee is ground. In response to the growing demand for complex flavours, coffee producers are exploring new methods. They have started using techniques like anaerobic fermentation and carbonic maceration. This involves fermenting coffee in pressurised tanks. It differs from traditional methods such as washing, honey or natural processing. Some producers take these methods even further and experiment with different flavours. During fermentation, non-coffee materials like fruit pulp, aged beans and essential oils can be infused. Infusion can also occur during drying or storage. However, the most common stage for infusion is during fermentation.

Which companies are exporting specialty coffee?

Large trading companies are expanding their portfolios with specialty coffees. This shows how the segment is growing in importance. InterAmerican Coffee, owned by Neumann Kaffee Gruppe, was one of the first large players to set up a group to source specialty coffees. Other recent examples include Rehm & Co (owned by Benecke Coffee) and Sucafina Specialty. Covoya (previously Olam Specialty Coffee) expanded its brand and e-commerce platform from the US to Europe in 2022.

Although multinational coffee traders are increasingly engaged in the specialty market, there are also many specialised independent trading companies in Europe. These companies focus on importing small volumes of high-quality or single-origin coffees, for which they pay competitive premiums. Examples include Coffee Quest, Trabocca, This Side Up (the Netherlands), Belco (France), Falcon Coffees (United Kingdom) and Nordic Approach (Norway).

Tips:

- Read our study on the specialty coffee market in Europe to learn more about trends and market opportunities for coffee exporters.

- Read this article on how to limit risk and improve quality on your micro lot.

- Check the Specialty Coffee Association (SCA) website to learn more about coffee cupping and protocols.

- Refer to the Cup of Excellence platform to connect with other industry players and potential buyers.

- Learn more about the rise of ecommerce and what the future holds for coffee in ecommerce.

- Learn more about the art of online sales for specialty coffee roasters.

4. Coffee prices are increasing

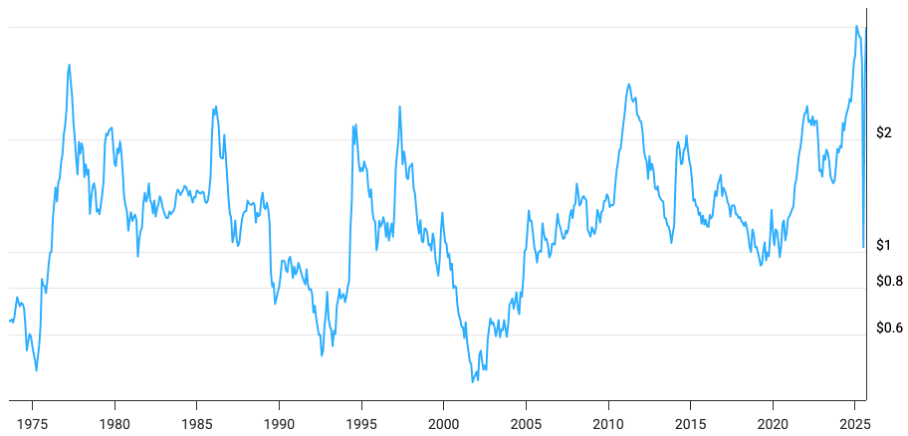

Coffee prices have surged in recent years. Average yearly prices increased from $1.11 (USD) in 2020 to $2.35 in 2024. Prices increased even further into 2025 (as of September), reaching $3.30.

There are several explanations for the increased prices. The main reason is a global coffee shortage due to lower supply and increasing demand. Bad weather affected the main coffee-producing countries cutting yields. Brazil suffered multiple poor harvests in a row, affecting coffee production. Drought in Vietnam, the second-largest coffee producer, reduced coffee yields by about 20% in the 2023/2024 and 2024/2025 seasons. At the same time, demand for coffee kept climbing, especially in Asia.

There were other reasons for coffee prices rising. Higher labour and energy costs raised production and transportation expenses. Speculation on the commodity market accelerated market volatility and price increases.

Effects on producers

Some producers and exporters benefit from these price increases. However, many smallholders do not get the full advantages. Complex supply chains, intermediaries, higher farm costs and liquidity constraints (pre‑financing) mean farmgate gains are uneven. In some countries, such as Guatemala and Honduras, farmgate prices have tracked coffee prices closely. In others, such as Ethiopia, prices lag while production costs increase.

For many farmers, higher prices do not fully compensate for lower volumes resulting from poor harvests or increases in input and harvesting costs. The high price swings (volatility) also reduce their ability to invest in long‑term improvements.

Effects along the supply chain

The volatility and higher spot prices reduce exporters’ working capital and pre‑financing. This makes it harder to honour forward contracts. This raises the risk of defaults and contract renegotiations.

Many roasters and importers face thinner margins. They pass higher costs to retailers, which changes consumer behaviour. Importers also encounter sourcing difficulties. Increased prices lead to more frequent renegotiations and make shorter contracts and spot purchases to manage risk more common. They also lead to tough price negotiations between traders, roasters and retailers.

Higher retail prices change consumption patterns. They lead to more at‑home brewing. A shift toward lower‑priced formats or blends is likely.

Future impact on increasing prices

Coffee prices are high compared to a few years ago. Price volatility has always defined the coffee market. As a global commodity, coffee prices often rise and fall sharply. Several peaks have occurred over the last 50 years; in 2011, 1997, 1994, 1986, 1979 and 1977. Each of these spikes was followed by a decline, with no lasting shift in how value was shared in the supply chain. The current increase may follow the same pattern.

Figure 1: Coffee price development, between August 1973 and August 2025

Source: Macrotrends.net

It is worth asking if prices are truly ‘high’. Many consumers and retailers think so, but two key facts matter. First, green coffee prices have long been below the level most farmers need to earn a living income. Even now, many farmers remain far below that threshold. Second, large roasters, such as JDE Peet’s and Lavazza, reported strong profits during this period. This suggests that downstream players, not producers, have been able to capture much of the price increase. No structural changes are expected to improve value distribution in the sector.

In the short term, prices may fall if production recovers in some regions. Climate change will continue to disrupt production, while rising incomes in Asia keep high pressure on the demand side. This combination points to a future of sharper and more frequent price spikes.

Tips:

- Sell in parts. Avoid selling your whole crop at one fixed price. Spread sales over time to reduce risk.

- Join a cooperative or work with your neighbours to sell together and get better prices and finance opportunities.

- Build long-term relationships with buyers that support you. Stronger, longer relationships with buyers can enable pre-finance and stable orders.

- Stay informed about coffee price drivers like overproduction, weather events, supermarket price wars, trade turmoil and shifting regulations. Some useful sources include the Trading Economics, the Markets Insider and ICO’s monthly coffee market reports, Perfect Daily Grind, Daily Coffee News and The Pourover.

- The global coffee market is shaped by supply and demand. Arabica coffees are traded on the New York Stock Exchange and Robusta on the London Stock Exchange. These markets often rely on futures contracts. These allow buyers to secure future coffee shipments at lower prices, creating market liquidity. However, this system can lock producers into prices that do not reflect their coffee’s true value. Learn more about coffee hedging and global coffee prices on the Perfect Daily Grind website.

5. Mandatory sustainability rules are reshaping the coffee sector

The EU is introducing new sustainability laws that coffee exporters must meet to sell in Europe. These rules cover environmental protection, human rights and fair labour standards. They are part of the EU’s Green Deal and linked strategies. They aim to make soft commodity supply chains fairer and greener. Their impact, however, is still uncertain. Timelines, enforcement methods and readiness in the EU and producing countries vary. This has resulted in regulatory uncertainty and faltering political will to drive sustainability transformation.

Current legislation

The EU has adopted many pieces of legislation, directives and plans to improve sustainability across supply chains. This section provides a short overview of the pieces of legislation and directives that have the largest impact on coffee exporters. At the same time, many of them are subject to change. This makes this trend very uncertain.

EU Deforestation Regulation (EUDR)

The EUDR entered into force on 29 June 2023. A key requirement is that coffee placed on the EU market must originate from land not deforested after 31 December 2020. European buyers must verify legal origin and trace products to the farm plot with geolocation data and conduct due diligence.

At the time of writing (October 2025), the EUDR deadlines were open for discussion. The deadline for large companies, December 2025, was likely to be postponed. This would be the regulation’s second delay. You can find more information on the EUDR and how to comply with it in our tips on how to become EUDR compliant in coffee and our webinar on how to meet EUDR requirements.

Corporate Sustainability Due Diligence Directive (CSDDD)

The CSDDD was formally adopted in 2024. It forces large companies to prevent and address adverse human rights and environmental impacts across their supply chains and prepare transition plans aligned with the Paris Agreement. The rules apply in phases:

- From 2027, for companies with 5,000+ employees or €1.5 billion turnover;

- From 2028, for companies with 3,000+ employees or €900 million turnover;

- From 2029, for companies with 1,000+ employees or €450 million turnover.

You can find much more information on the CSDDD and how to comply with it in our study on requirements for the European coffee market.

EU Forced Labour Regulation (EFLR)

The objective of the Forced Labour Regulation is to ban the production or trade of any product made using forced labour. Based on risk assessments, companies based in the EU must ensure that no forced labour occurs within their supply chains. In April 2024, the EU Parliament gave its final approval to the legislation. Companies should be prepared to comply with the Regulation’s requirements from mid-2027. Non-compliant European companies will be fined. National authorities will have the power to investigate, remove goods or fine non-compliant companies.

The full effect of the Forced Labour Regulation on exporting companies is still unclear, but the European Commission will issue more guidance later. However, European buyers will require more information from their suppliers.

Empowering consumers for the green transition

Directive 2024/825 entered into force in May 2024. It aims to ensure that consumers receive better information on some sustainable practices. Green or environmentally friendly claims can only be made with sufficient proof. This also affects using company standards. Using logos from company standards is only allowed if an independent authorised third party verifies them. This directive will enter into force through national legislation by 27 September 2026.

Future outlook

While these laws are in place, the political debate is shifting. In February 2025, the European Commission (EC) proposed the ‘Omnibus approach’. The EC wants to consolidate the CSDDD, the Corporate Sustainability Reporting Directive (CSRD) and the EU taxonomy. The EU wants to simplify compliance to reduce the burden on companies.

The proposed Omnibus weakens the CSDDD. The directive would apply to fewer companies and limit the obligations to only their direct suppliers. It also removes obligations for climate transition plans and reduces the penalties.

In the short term, expect uncertainty. Your buyer will likely come with new or short-term information requests. As such, it is crucial to have well-recorded business information. In the long term, EU regulation is likely to set higher sustainability standards for supply chains.

Stricter legislation may also lead to more divided trade flows. Some European importers have already shifted imports from ‘risky countries’ to ‘less risky countries’ to reduce the chance of not complying with EUDR standards. From an exporter's perspective, some companies will likely invest in legislative compliance, while others will shift towards new markets. In countries with better national support, such as Brazil and Colombia, companies are more likely to keep exporting to Europe. On the other hand, cooperatives with many remote smallholders in ‘risky countries’ may seek new buyers elsewhere.

Tips:

- Ensure that your suppliers follow responsible business practices. Many social and environmental issues arise at the farm level, which may not be a part of your direct handling and processing activities.

- Demonstrate how you work to reduce your carbon footprint. For example, you could show how you are replacing chemical fertilisers with natural alternatives. This could help you position yourself as a preferred supplier to European importers and companies.

- Read our tips to go green and tips on how to become more socially responsible in the coffee sector. These suggestions include practical actions to enhance sustainability within the coffee industry.

- Follow the European Commission news to stay up to date on the EUDR and other regulations that may have affect your export business.

6. Regenerative agriculture is gaining ground

Regenerative agriculture is a way of farming that focuses on improving soil health, increasing biodiversity and using natural practices. These practices can include compost, cover crops, agroforestry, reduced tilling and integrating animals to create healthier soils and crops. International attention, such as from the United Nations climate conference, has helped put sustainable and regenerative farming into policy conversations.

Regenerative agriculture does not have a single, fixed set of rules. This makes the concept unclear: different certifiers and groups define it differently. Some allow certain synthetic inputs. Others, such as Regenerative Organic Alliance, follow stricter organic rules. As such, it can be hard to know exactly what a ‘regenerative’ label means.

Multi-stakeholder initiatives are working on creating clearer standards. Regenerative Organic Alliance works with A Greener World, BioAgricert and Regenified on clear standards. The Global Coffee Platform published the GCP RegenCoffee Guidance. It offers a framework for regenerative agriculture.

Regenerative farming is growing. Producers are dealing with climate shocks, soil loss and lower profits. They need ways to make farms more resilient and productive. A farm working according to the regenerative farming principles is Finca el Suelo in Colombia. Large roasters, such as Lavazza, Nestlé, Starbucks and Illycaffè, invest in regenerative practices to secure supply. Regenerative farming has also caught the attention of small specialty roasters, such as the Dutch Wakuli. Many sustainability programmes, such as Technoserve’s coffee portfolio and IDH’s Coffee Farmer Income Resilience Program, lean on regenerative practices.

In the short term, adoption will rise. Farms can improve soil, hold water and reduce input costs over time. Certification may add value through market access and trust. In the long term, standards will need fair financing and clearer measurements (e.g. soil organic carbon, water retention and biodiversity indicators).

Tips:

- Learn about regenerative farming. For instance, start by reading the Alliance Biodiversity & Ciat blog. It gives an interesting overview of the advantages.

- Get inspired by Finca el Suelo’s video where they explain how they work according to regenerative agriculture principles.

- Regenerative farming overlaps with organic farming. Read more on the opportunities and threads in this field in our study on Exporting organic coffee to Europe.

- Read more about climate-friendly coffee production in our tips to go green in the coffee sector.

7. Company standards gain importance

In recent years, many major coffee companies have created in-house sustainability standards. These are separate from independent third-party certification schemes, such as Fairtrade, Rainforest Alliance, Organic and 4C. Company standards are usually developed and managed in-house. They may use elements of existing certification systems. However, companies retain full control over how they apply, promote and measure them.

Most company standards are not audited by independent organisations. This can make them less transparent and less complex than third-party systems. For companies, in-house standards offer flexibility. They align sustainability goals with supply chain control and branding strategies. Examples include:

- AAA Program (Nespresso)

- AtSource (Ofi)

- Bloom (Neumann Kaffee Gruppe (NKG))

- C.A.F.E. Practices (Starbucks)

- IMPACT (Sucafina)

- LIFT (Mercon Coffee Group)

- Sustainability Management Services (ECOM)

- The Volcafé Way (Volcafé)

Company-programme sustainable coffee is growing. In 2020, only 4.4% of coffee sourced by members of the Global Coffee Platform (GCP) was covered by a company standard. By 2023, this figure had grown to 21%. Note that GCP members do not represent the whole market.

Starbucks’ C.A.F.E. Practices, for example, has become a central part of the company’s global brand identity. The programme focuses on sustainable sourcing, supporting farming communities and addressing climate change. Nespresso’s AAA programme has reached over 90% of its sourcing, aiming to improve productivity, quality and farmer livelihoods. JDE Peet’s has also integrated sustainability into its sourcing targets, aiming for 100% responsibly sourced coffee by 2025, verified under Enveritas Green standards.

Smaller and mid-sized industry players are also involved in projects directly at origin. For instance, check the websites of the Dutch trader Trabocca and UK trader Falcon to get an idea of the type of projects origin traders are engaged in. Retailers develop codes of conduct to contribute to sustainability concerns and requirements. Examples include those developed by REWE (Germany), Ahold Delhaize (Netherlands) and Carrefour (France).

This trend requires producers and exporters to be well-aware of the landscape they operate in. Although many standards are similar, they all have their own requirements. Compliance to multiple standards gives you better market access, but it also costs more. Therefore, it is key to know which standards your potential buyers maintain, and what they want for the future. Not all buyers, and therefore not all standards, are active in every country. The GCP sustainability report 2023 (p. 23) provides an overview of the certification schemes active in the largest coffee-producing countries.

Future Outlook

The growth of company-created schemes will likely continue. In 2024, 19 new sustainability schemes were recognised as equivalent to the Coffee Sustainability Reference Code (CSRC). The CSRC sets minimum standards for certification schemes to become recognised by the GCP. Company sustainability standards will likely become more common, data-driven and closely tied to regulatory compliance, such as the EUDR.

Tips:

- Read our studies on certified coffee and multi-certified coffee to learn more about this topic.

- Screen your suppliers. Ensure they have strong environmental and social practices. Many risks occur at farm level.

- Know your buyers’ standards. Understand whether your buyers use a company standard, an independent certification or both.

- Demonstrate how you reduce your carbon emissions, for instance, by replacing chemical fertilisers with organic inputs. This can help you to position yourself as a preferred supplier to European importers and companies.

- Read our tips to go green and tips to become more socially responsible in the coffee sector. The latter covers practical actions to enhance sustainability in coffee.

8. Artificial intelligence will transform the coffee sector

Artificial Intelligence (AI) is transforming the coffee market. It improves production, trade and roasting while reducing waste. It enables data-driven decisions, reduces human error and improves quality control. However, it also raises questions about data ownership and equitable access for smaller actors.

AI tools can help farmers monitor crop health, predict yields and adapt to climate conditions. Examples of such tools are WSeeds, Almanac and Cropster. These tools can enable better harvest planning and resource use. Exporters can use quality control tools to assess bean quality, such as Agrivero and Demetria. Other AI tools help them with their logistics, such as Project44.

Importers benefit from predictive analytics tools that match supply to demand and monitor logistics in real time. This improves quality during transport. Solutions like blockchain-enabled traceability systems, such as IBM Food Trust, can verify origin and sustainability claims. Acclym can help importers with their sustainability reporting.

Roasters can use AI-assisted equipment. Examples include IMF Roasters’ systems, Aillio’s AiO roaster and Ansa’s Variety e23. These systems use sensors and machine learning to adjust temperature, airflow and drum speed automatically. This leads to more consistent flavour profiles, batch after batch.

The Coffee Gardens is a producer in Uganda. The company uses different AI tools to increase efficiency. In their day-to-day activities, they utilise tools like ChatGPT to write code in Salesforce and quickly convert geographic information into area measurements. They also use Zapier (with AI components) to connect their databases with other sources, streamlining data processing. Artificial intelligence is used to verify if farmers have completed their training, by analysing photos submitted as evidence.

Looking ahead, the company expects to expand its use of AI with a chatbot designed specifically for their staff, and potentially for other companies in the future. With the chatbot, the company aims to make good farming practices accessible to their farmers. They provide trainers with accessible information based on specific needs, rather than expecting staff to read and memorise dense manuals.

Future Outlook

AI use in the coffee sector will likely expand rapidly in the short term through greater adoption. Robotic baristas, automated roasting systems, real-time farm monitoring and blockchain-based traceability will likely become more common.

For producers and exporters, relatively small, demarcated tasks will likely become automatable in the short term. One example is using a note keeper during meetings, such as Fireflies. For more integrated use in the supply chain, having good administration for your business processes is key. Be aware that many AI tools are only helpful if you can provide them with high-quality input.

In the long run, advances in machine learning and integrated supply chain optimisation could lead to fully data-driven coffee production and trade. AI systems will likely link farm-level environmental data, processing conditions, logistics and market analytics to adjust strategies in near real time.

Tips:

- Work on your business’s traceability and bookkeeping. AI tools can enhance your business performance better if you provide them with high-value input. AI tools have even more effect if integrated into your current IT systems.

- Inform yourself on how AI is used in coffee. Read about the tools, but also talk with buyers, suppliers and other market players about digital options.

- Explore online trading platforms such as Algrano, Beyco, TYPICA and Almacena Platform to connect to roasters in Europe and elsewhere.

- Read the CBI’s Tips to go digital in the coffee sector, Tips on finding buyers for coffee and Tips for doing business in Europe.

Molgo Research carried out this study on behalf of CBI.

Please review our market information disclaimer.

Search

Enter search terms to find market research

Do you have questions about this research?

The ready-to-drink market is only getting started in Europe and will likely continue to grow in the coming years, especially as it enters the specialty coffee segment, creating opportunities for direct trade and better contracts for high-quality, sustainability-focused suppliers.

Eline Ferket, Market development at 25GRAMS

AI has the potential to improve the operations of coffee producers and exporters. However, for optimal results, companies need to provide adequate data inputs. This requires maintaining accurate information on various aspects of their business, such as accounting and product flow.

Elisa Criscione, Founder & CEO at Digital Coffee Future