Entering the Belgian coffee market

Belgium has a huge lower-end market. This is mainly non-certified commercial coffee. Brazil and Vietnam are the main suppliers of this segment. Honduras is the main supplier of the certified coffee market. A large share of Belgian coffee is re-exported to the rest of Europe. All coffee that enters Belgium needs to meet certain standards. Most of these come from European Union legislation.

Contents of this page

1. What requirements and certifications must coffee meet to be allowed on the Belgian market?

Exporting to Belgium comes with many requirements. The European Union (EU) sets most of these. Some requirements, however, are set by the Belgian government or companies themselves. These can be divided into:

- Mandatory requirements;

- Additional company requirements to maximise success in the market;

- Requirements for niche markets.

The mandatory requirements, additional requirements and the requirements for niche markets are described below. Most requirements are the same for all European markets. For a longer and general description, read our report on requirements for the European coffee market.

What are mandatory requirements?

Requirements on food safety and hygiene

You need to follow the European Union legal requirements for coffee. These rules mainly deal with food safety, where traceability and hygiene are the most important themes. Special attention should be given to specific sources of contamination of pesticides and mycotoxins/mould, particularly Ochratoxin-A (OTA);

Tips:

- Consult the EU Pesticide Database for an overview of each pesticide's maximum residue levels (MRLs). You can search for coffee under the product or search for the active ingredient of your pesticide if you know it. This will show the MRLs of the active ingredients accepted in the EU.

- Always check with your buyers if they have additional rules regarding MRL limits or pesticide use.

- Use your browser (e.g. Google Chrome) or an AI translation to translate the information offered on Belgian websites.

Labelling requirements

Labels of green coffee exported to Belgium should be in English. They should include the following information to make sure individual batches are traceable:

- Product name

- International Coffee Organisation (ICO) identification code

- Country of origin

- Grade

- Net weight in kilograms

- For certified coffee: name and code of the inspection body and certification number

Figure 1: Example of green coffee labelling

Source: Escoffee

Payment and delivery terms

Payment is generally required when accepting the coffee, or within 30 or 45 days. This depends on the terms in your contract. Cash Against Documents is the most common type of deal when exporting coffee to Europe. You provide documents proving shipment, such as a bill of lading or invoice, and get paid in return. This ensures you receive payment for your goods.

It is important to examine these terms carefully. Generally, you will be paid earlier if you sell your coffee to a trading company than if you sell it to a roaster directly. You can read more about this in our tips on organising your coffee exports.

Packaging requirements

Green coffee beans are traditionally shipped in woven bags made from jute or hessian natural fibre. Jute bags are strong. Some specialty coffee suppliers also use other materials inside jute bags, like GrainPro and Videplast. These materials have added value over traditional packaging. They preserve bean quality, prevent post-harvest loss, reduce solid waste, reduce farmer’s net carbon footprint and help with chemical-free storage. Note that these innovative materials are mostly used for the high-end and upper-end segments.

Other packaging for transporting coffee include:

- Polypropylene super sacks for 1 tonne of coffee;

- Polyethylene liners for 21.6 tonnes;

- Vacuum-packed coffee.

These techniques increase efficiency, and maintain and preserve quality.

Figure 2: Examples of coffee packing from left to right: jute bag, container-sized flexi bag, GrainPro and Videplast liner

Sources: Raad, Bulk Logistic Solutions and GrainPro

Tips:

- Read the CBI study on buyer requirements for coffee in Europe for the full buyer requirements.

- Check EUR-Lex for more information on limits for different contaminants. For specific information on the prevention and reduction of Ochratoxin A contamination, refer to the Codex Alimentarius CXC 69-2009. Use the search tool to find the codes that contain information on Ochratoxin A, and select your preferred language.

- For information on safe storage and transport of coffee, refer to the Transport Information Service website.

- Learn more about delivery and payment terms for your green coffee exports by reading our study on organising your coffee exports to Europe.

Sustainability requirements become stricter

The main sustainability requirements are taken from the European Green Deal. Examples include the European Deforestation Regulation (EUDR) and the European Corporate Sustainability Due Diligence Directive (CSDDD).

The European Green Deal (EGD) is the European Union’s (EU) response to the global climate emergency. The EGD is a package of policies that defines Europe’s strategy to reach net zero emissions and become a resource-efficient economy by 2050. Next to the European Green Deal, the Forced Labour Regulation will also affect Coffee Suppliers that export to the EU.

The European Deforestation Regulation prohibits coffee that led to deforestation

One of the laws derived from the Green Deal is the EU Deforestation Regulation (EUDR). This legislative measure has the greatest impact on the European coffee industry.

Under the EUDR, importers must prove their coffee does not come from recently deforested land. In November 2025, the EU decided to postpone the regulation a second time, to December 30, 2026. Micro and small enterprises have six more months. This law makes traceability and technology crucial for exports to the EU market. This will have implications for the coffee industry. The EU provides an information sheet on frequently asked questions about this topic.

Belgian companies will need more information to proof due diligence in the future

Under the new CSDDD regulations, European corporations need to improve their sustainability performance throughout their supply chains. There is a lot of uncertainty surrounding the CSDDD. The European Commission has proposed simplifying the CSDDD, which would make it much weaker. The directive would then apply to 80% fewer companies. It would also limit the obligations to only direct suppliers. Itt removes obligations for climate transition plans and reduces the penalties as well. The proposal has not been accepted yet, so the final text may still change. It is unclear if and when the CSDDD will come into force.

Next to the CSDDD, the Belgian government is also working on its own proposal on mandatory value chain due diligence. The European CSDDD is only supposed to affect large companies. However, the Belgian law aims to affect all Belgian companies. The law has been adopted but it is not in force yet. It is unclear when the law will come into force. When it does, Belgian coffee traders will probably demand more information from your company.

The Forced Labour Regulation bans coffee produced with forced labour from the European market

The objective of the Forced Labour Regulation is to ban the production or export of any product made using forced labour. Based on risk assessments, companies based in the EU will need to ensure that no forced labour occurs within their supply chain. In April 2024, the EU Parliament gave its final approval on the legislation. Companies should be prepared to comply with the Regulation’s requirements from mid-2027. Non-compliant European companies will be fined.

The full effects of the Forced Labour Regulation on exporting companies is still unclear. However, it will mean that European buyers will require more information from their suppliers.

Tips:

- Increase your traceability. European sustainability requirements will become stricter. You can only provide proof of your sustainable behaviour if you know where your coffee comes from. Depending on market interest, certification could be an interesting way to do this.

- Consult your buyer if you are unsure about any requirements.

- Read more about the European Green Deal to get a better overview of the legislation.

- Learn what you can do to become more sustainable in the CBI’s coffee studies on tips to go green and tips to become socially responsible.

- Read more about national due diligence legislation across European countries.

What additional requirements and certifications do buyers often have?

Some Belgian buyers may demand extra food safety requirements in terms of processing or additional quality requirements.

Additional food safety requirements

You should expect buyers in Belgium to request extra food safety guarantees from you. Regarding production and handling processes, you should think of:

- Implementing good agricultural practices (GAP): The main standard for good agricultural practices is GLOBALG.A.P. This is a voluntary standard for certifying agricultural production processes that provide safe and traceable products. Certification organisations, such as Rainforest Alliance, often incorporate GAP into their standards. In Belgium, the Federaal Agentschap voor de Veiligheid van de Voedselketen (FAVV) is accountable for food safety.

- Implementing a quality management system (QMS): Buyers increasingly require producers to have a system based on Hazard Analysis and Critical Control Points (HACCP) as a minimum standard for green coffee production, storage and handling. The implementation of regular checking of residue levels in your green and roasted coffee could be part of this system. It is especially important to monitor Ochratoxin-A (OTA), polyaromatic hydrocarbons (PAHs) and glyphosate contamination.

Quality requirements

Green and roasted coffee usually undergo physical evaluation to determine their quality. Roasted coffee also undergoes sensory evaluations.

The quality assessment is usually based on the following criteria:

- Altitude and region;

- Botanical variety;

- Processing method – wet/washed, dry/natural, honey, pulped naturals;

- Screen size;

- Number of defects or imperfections;

- Bean density;

- Cup quality.

Moisture checks and water activity analyses are also often included in the assessment. Sample roasting is sometimes performed to assess the quality and uniformity of green coffee.

The process of quality assessment is the same for all types of green coffee beans. The exact criteria, however, differ. This means, for example, that both high-end and low-end coffee beans are checked for bean density (mass divided by volume). High-end coffees need higher bean density.

Tips:

- Know the coffee you sell. This includes information on the growing process, the processing and the flavour attributes. Fruity and chocolate are examples of flavour attributes. You should also know the quality you sell. This can help you sell part of your coffee for a higher price.

- Learn about green coffee quality assessment. The Specialty Coffee Association is the leading standard, but you can also read about other ways to assess coffee quality.

What are the requirements for niche markets?

Exporting organic coffee, specialty coffee and roasted coffee comes with additional requirements.

Requirements for organic coffee

Exporting organic coffee comes with extra requirements. To market your coffee as organic in the European market, it needs to comply with the regulations of the European Union for organic production and labelling. Regulation (EC) 2018/848 sets organic production and labelling rules.

Organic coffee is checked when it enters the EU. To import organic coffee to the European Union, the delivery needs to include an electronic certificate of inspection (e-COI). This certificate should be set up in the Trade Control and Expert System (TRACES). It must be signed by a control authority in your country before the shipment leaves the country.

When packaging, Belgian roasters can either add the EU organic label or the Biogarantie label. To gain the Biogarantie seal, Belgian companies need to be audited by Certisys, Tüv Nord Integra, FoodChain ID or Melkcomité, depending on the region of the company.

Figure 3: The Belgian Biogarantie label

Source: Biogarantie

Tips:

- Learn more about exporting certified coffee by reading our studies on organic coffee, certified coffee and multi-certified coffee.

- Find importers that specialise in organic products on the Organic-bio website. These importers may become potential buyers.

- Use this cost calculator to estimate how much it would cost for your organisation to become Fairtrade-certified. Also ask for quotations from different certifiers before you decide on which one you want to work with. Ask for timelines and an estimate of how many days would be charged. Always discuss potential certification with your buyers before you make any investment or decision.

- Try to combine audits if you have more than one certification. This will save time and money. You should also look into the possibilities for group certification with other regional producers and exporters.

Requirements for specialty coffee

Specialty coffee is graded according to its cupping profile. Fragrance, flavour, aftertaste, balance, acidity, sweetness, uniformity and cleanliness are important factors in the grading process. If you sell specialty coffee, buyers need to know your coffee's cupping score. Adding this information to the documentation of the coffee you are exporting can add value. It is very important to be aware of the quality of your coffee. You can do so through local cupping experts or become a cupping expert yourself.

Besides quality, transparency is also very important. Many buyers are interested in stories about product origins. Examples include details of your coffee farm, the coffee growers, how and where you grow your coffee, and your processing facilities. This means you should know the specifics of your coffee, from soil management to cup. You must be willing to share everything honestly.

Direct trade can also result in more frequent coffee farm visits, product assessments by your buyers and long-term business relationships.

Requirements for roasted coffee

Sensory assessment: coffee cupping

Coffee is assessed and scored by a method called ‘cupping’. Buyers will use different protocols and standards to conduct sensory assessments. However, the SCA recommends protocols and best practices for cupping coffee. The SCA’s Coffee Taster's Flavour Wheel is a widely used cupping tool. Some of the quality attributes assessed are flavour, fragrance/aroma, aftertaste, acidity, body, uniformity, balance, cleanliness, sweetness and off-notes.

Hygiene requirements for roasting

Food imported into the EU is subject to official food checks. These controls include regular inspections that can be carried out at import (at the border) or later on, once the food is in the EU. The control is meant to check whether the products meet the legal requirements.

All roasters must use a procedure based on HACCP principles. A HACCP plan is a critical element of the quality management systems of companies that want to become successful suppliers to the European market. The HACC (Hazard Analysis and Critical Control Points) principles for roasted coffee focus on keeping the coffee safe and of good quality.

The HACCP steps include checking for issues like contamination, setting up points in the process to check these issues, and ensuring the coffee meets safety standards at each point. Monitoring and keeping records are also important to ensure the coffee remains safe for consumption.

Trade tariffs

The standard duty on roasted coffee imports is 7.5%. The duty for decaffeinated roasted coffee is 9%. These duties vary depending on the exporting country. The duty depends on whether your country has a contract with the European Union. Note that the importer is responsible for paying the trade tariff, not you as an exporter.

Tips:

- Check if any trade duties apply to your country. Check the Access2Markets website.

- Read our study on exporting roasted coffee to Europe to learn more about this market.

2. Through which channels can you get coffee on the Belgian market?

The Belgian market can be divided into several segments, from the lower to the upper end. Nearly all coffee is imported through large multinational trading companies. The multinationals are mostly importers and exporters. Most coffee in Belgium is sold in supermarkets. Cafes, however, still account for a large market share. Nearly all coffee flows through multiple value chain actors before reaching the consumer.

How is the end-market segmented?

The Belgian end market for coffee can be divided into four segments: the lower, middle, high and upper end.

It is important to remember that exports to Belgium do not always end up on the Belgian market. Belgium is a large re-exporter of green coffee. Around two-thirds of its green coffee is re-exported. A large share of its roasted coffee is also shipped to other countries. Belgium is a large importer of coffee roasted in other (mainly European) countries.

Figure 4: Coffee end-market segmentation by quality

Source: Profound

Low end

Coffees in the low-end segment are mainstream, lower-quality and mainly blended. These blends are characterised by high proportions of Robusta beans. The lower-quality private label products from supermarkets belong to the low-end segment alongside some mainstream brands. Most coffee pads and instant coffee belong to this segment. Coffees in the low end of the market are mainly sold in supermarkets and through service channels, such as offices and universities.

The lower end is the largest in Belgium by far. The Belgian at-home market is very price sensitive. The lower-end market has grown due to the high global coffee prices. Belgium is home to many discount supermarkets, such as Aldi and Lidl. Both supermarkets have their own private-label roasters to supply their stores.

Mid-range

Mid-range coffees are commercial coffees with a good and consistent quality profile, such as quality espresso. This segment typically consists of blends with a higher proportion of Arabica than the low-end segment. The mid-range segment represents a stable coffee market, where sustainability certifications are important. Mid-range coffees are often sold in supermarkets and by the food service industry. Premium private label ranges of retailers typically belong to the mid-range segment.

High and upper ends

High-quality coffee mainly consists of washed Arabicas. These coffees are often single-origin and have special stories. The upper end of this segment consists of specialty coffees of excellent quality, sometimes from micro or nano lots that go through processing methods, such as naturals and honeys. These are mainly fully traceable and single-origin Arabica beans. The high and upper-end segments are a small but growing market.

Sustainability certifications are less common in this segment because sustainable practices are often considered commonplace amongst buyers. The high-and upper-end segments characterise themselves by long-term contracts between suppliers and buyers and higher prices.

Tips:

- Know the coffee quality you sell. The higher the quality, the higher your price should be. Very high-quality beans, if processed well, can also offer opportunities for direct trade. Many high-end roasters are interested in offers with a unique taste.

- Explore ways to enhance the quality of the coffee you produce. Certification, good agricultural practices and post-harvest processing can improve the perceived quality of your product.

Through which channels does coffee end up on the end-market?

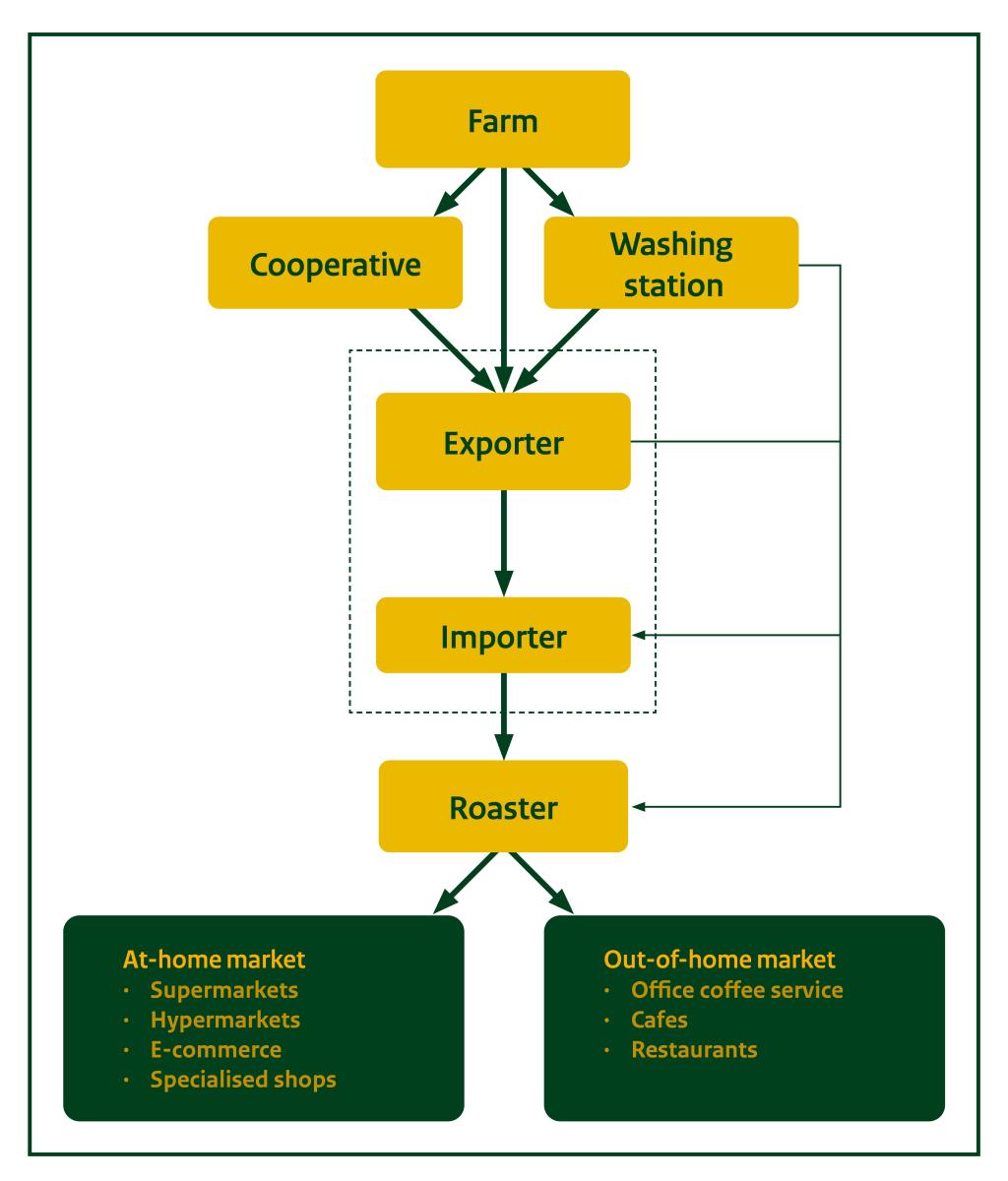

The Belgian supply chain consists of many actors, mentioned in Figure 5. Most coffee flows through all actors in the chain. However, options to get into the Belgian market more directly are arising.

Figure 5: The Belgian coffee supply chain

Source: Counter Culture Coffee

Importers play a major role in the Belgian coffee supply chain

Importers are major facilitators in Belgium’s coffee market. They bridge the gap between coffee producers around the world and Belgian roasters and retailers. They handle a wide array of essential tasks. This includes sourcing coffee, ensuring quality, managing logistics, pre-financing shipments and evaluating financial risks. Importers make sure Belgian businesses receive the types and qualities of coffee that best suit their needs. Efico and Supremo are examples of Belgian trading companies that import green coffee.

Multinational companies dominate the Belgian trade market. These include:

These companies have extensive sourcing networks. They often work directly with farmers, cooperatives and exporters. They serve the Belgian market by providing a steady, reliable supply of mainstream and specialty coffees. Sometimes they tailor offerings to local preferences. Other multinationals, such as Sucafina, focus on specialty coffee.

Online marketplaces facilitate trade

Online marketplaces are platforms that connect actors in the chain, mainly connecting farmers to roasters. Using marketplaces allows farmers or cooperatives to cut out parts of the chain. This may allow you to get better prices for your products. Only a very small share reaches Belgian roasters through marketplaces. Some of these marketplaces are:

- Algrano (Switzerland)

- Raw Material (United Kingdom)

- Beyco (Netherlands)

We did not find any Belgian marketplaces that connect farmers to roasters, but the companies mentioned work globally.

The Belgian coffee market is shaped by retailers and large international brands

Belgium’s grocery retail landscape is concentrated on a handful of major players. In Belgium, leading supermarket chains Colruyt, Delhaize, Carrefour and Aldi account for most grocery sales. Retailers play a major role in setting coffee prices, with private-label coffee occupying a strong place on supermarket shelves.

Belgium’s coffee roasting market is smaller than that of Germany, France and the Netherlands. However, it is heavily influenced by major international roasters. Most roasted coffee in Belgian supermarkets is sourced from a few large players:

- JDE Peet’s: The world’s second-largest coffee roaster and a major supplier in Belgium, which markets brands such as Douwe Egberts, Senseo and L’OR. Their products are found in most Belgian supermarkets.

- Nestlé: The world’s biggest coffee multinational, Nestlé, has a strong presence in Belgium. Nescafé and Nespresso are particularly popular amongst Belgian consumers.

- Melitta: Although not Belgian, Melitta products are sold in Belgian retailers, especially in the filter coffee segment.

- illy and Lavazza: Italian brands have a large following in Belgium, especially among espresso lovers and in hospitality channels.

- Beyers Coffee: A historic Belgian coffee brand that produces its own and private-label coffee.

Belgium is home to an active community of small coffee roasters

Large international roasters and established brands dominate Belgian supermarkets and the broader coffee market. However, Belgium also has many smaller coffee roasters.

Many smaller Belgian roasters focus on specialty coffee. They often source high-quality beans directly from producers and emphasise sustainable, ethical practices. Examples of renowned small-scale Belgian roasters include Café Capitale (Brussels), Or Coffee Roasters (Ghent) and Caffenation (Antwerp). Some, like MOK (Leuven), have earned international reputations for their innovative approach and quality.

What is the most interesting channel for you?

The best sales channel for your coffee depends on many factors. Most importantly, it depends on your unique selling point. This means you need to know your product.

- Know your coffee: to sell your coffee to Belgian buyers, your first step is to understand its specific characteristics and what sets it apart from the competition. Think about the origin of your coffee and its unique flavour notes. Consider factors like your coffee beans’ genetic profile, agroecological context, post-harvest practices, quality, and impact on communities and nature. Storytelling and traceability are also important. A good story can help connect consumers to the origin of your coffee and make their experience richer.

- Know your buyers: the second step is to learn what your (potential) buyers want. To successfully sell your coffee to European buyers, it is important to understand their taste preferences and consumption patterns. Explore specific coffee requirements like cup quality and sustainability with your buyers. Look for buyers who are willing to build long-term relationships. This can mean either approaching them directly or through an importer. You can increase your chances of success by analysing market information and identifying key buyers.

If you export green mainstream coffee, you should look into entering the Belgian market through large importing companies. These companies usually have agents or representative offices in producing countries. This can be your first point of contact.

If you have coffee with a cupping score of 80 and above, consider working with specialised traders or roasters like Efico and Supremo. One Belgian roaster that buys directly from producers is Ray and Jules. Many specialised importers prefer to work with producers and cooperatives directly.

Supplying to small roasters is interesting if you have:

- High-quality coffee;

- Micro lots;

- Sustainability certification;

- Or are willing to engage in long-term partnerships.

As the coffee market keeps changing, it is wise to explore more than one market channel.

Tips:

- Visit the World of Coffee. It will be organised in Brussels in 2026. It is a great place to meet buyers directly.

- Try online marketplaces, such as Algrano, Beyco and Raw Material. These platforms let you sell to Belgian roasters directly.

- If you have high-quality coffees and work through an importer, explore direct trade possibilities and connect with specialised roasters.

- Offer your coffee to specialised coffee importers and small coffee roasters directly. This is only possible if you are a farmer and have the financial means and technical know-how to organise export activities.

What competition do you face on the Belgian coffee market?

As a coffee supplier you operate in a global and competitive landscape. For producers and exporters, it is important to understand the market segment you operate in and the scale at which you work. By identifying these factors, you will be able to find out which countries you are competing with. Understanding the quality level, volume and positioning of your products allows you to better assess your competition and develop strategies to stand out in the global market.

Which countries are you competing with?

Competition in the Belgian coffee market is fierce. Your main competitors depend on the product you supply. Vietnam and India are Belgium’s main Robusta suppliers. Brazil, Honduras, Peru and Colombia focus more on Arabica.

In this section, we focus on the six largest competing countries: Brazil, Honduras, Vietnam, Peru, Colombia and India.

Brazil: Belgium’s largest green coffee supplier

Brazil is the world’s largest coffee producer and exporter. It produces both Arabica (around 70%) and Robusta (around 30%), although almost 80% of exports are Arabica. Brazil is also Belgium’s largest supplier. Brazilian exports to Belgium reached 97,000 tonnes in 2024. It has an average yearly increase of 3.8% since 2020.

Brazil’s coffee-producing areas are relatively flat. This has intensified the use of mechanical pickers. The use of mechanical pickers has reduced labour costs in Brazil’s coffee production. It has also led to average lower quality as machines do not distinguish between ripe and unripe cherries.

Brazil mainly produces natural and pulped natural coffees. Low-grade Brazilian Arabica is mostly used in blends. This is in high demand by roasters who focus mainly on price.

Brazilian coffee farmers are relatively successful. Factors that contribute to their success are:

- The scale they operate at;

- Mechanised cherry picking;

- Efficient infrastructure;

- Good climate (although climate change drastically affects several key producing regions).

Brazil is the only large producing country where the average farmer can generate a living income based on coffee farming.

Although Brazil is known mainly for exporting large volumes of standard quality, it also has a strong reputation as a producer of speciality coffees. The sector receives considerable institutional support through the Brazil Specialty Coffee Association (BSCA). The association aims to elevate the quality standards and enhance value in the production and marketing of Brazilian coffees.

Examples of exporters of speciality coffees in Brazil are Burgeon and Bourbon Specialty Coffees.

The 2024/2025 outlook for Brazil is positive. A 5.4% increase in production is expected.

Table 1: Brazil’s competitive profile

| Strengths | Weaknesses | Image on the coffee market |

|---|---|---|

|

|

|

Honduras: a major supplier of organic coffee

Honduras supplies a large share of organic coffee to Belgium. In 2024, Belgium imported 28,000 tonnes from Honduras. Between 2020 and 2024, green coffee imports from Honduras underwent an 7.1% yearly decline percentage. Leaf rust and domestic labour shortage led to a 24% coffee production reduction in 2023/2024.

The Honduran Coffee Institute IHCAFE has been promoting the production of value-added coffees. It did so either through certification or by actively improving quality. The country has grouped coffee production and quality specifications into six regions with different microclimates and soil composition.

Honduras has a growing reputation as a high-quality coffee supplier. Belgium is a large importer of specialty coffee. One Belgian specialty coffee trader that imports specialty coffee from Honduras is Rehm & Co.

A relatively large share of Honduras's coffee is organic. According to FiBL & IFOAM The World of organic Agriculture 2022, about 24,000 hectares were dedicated to organic coffee farming in Honduras. This is approximately 5.7% of the total planted coffee area in the country. At 24,000 tonnes, Honduras was Belgium’s largest organic coffee supplier in 2023. Honduras is followed by Peru, with 17,000 tonnes.

Certified coffee production in Honduras grew from 42% in 2018/2019 to 58% in 2022/2023. This includes Fairtrade, Rainforest Alliance, 4C and organic certification.

Examples of successful exporters in Honduras are Cafico (organic coffee) and Aruco (specialty coffee).

Table 2: Honduras’ competitive profile

| Strengths | Weaknesses | Image on the coffee market |

|---|---|---|

| High volatility due to bad weather conditions, such as leaf rust. |

|

Main source: Standard Insights

Vietnam: Belgium’s main green Robusta supplier

Vietnam is the world’s second largest coffee producer and the largest Robusta producer. Over 96% of Vietnamese coffee production consisted of Robusta coffees in 2023/2024. Vietnam’s coffee production strongly focuses on creating large volumes of standard quality coffees.

Vietnam’s total coffee exports to Belgium reached approximately 27,000 tonnes in 2023. Vietnamese exports to Belgium decreased by 55% in 2024. A drought that reduced the 2023/2024 harvest was the main cause of this reduction.

Examples of large Vietnamese coffee exporter groups include Simexco Daklak, Intimex Group, Tin Nghia Corporation and Mascopex.

The Vietnamese coffee production is expected to remain stable in the short term. High coffee prices encourage farmers to invest in the production, which cancels out the negative influences of bad weather conditions.

Table 3: Vietnam’s competitive profile

| Strengths | Weaknesses | Image on the coffee market |

|---|---|---|

|

|

|

Main source: Standard Insights

Peru: a top position in the production of sustainable coffee

In 2024, Belgium imported 19,000 tonnes of green coffee from Peru. Belgian imports have gone up and down between 2020 and 2024 between 27,000 tonnes in 2022, and 14,000 tonnes in 2023.

According to the UNDP, coffee is one of Peru’s main agricultural products. It accounts for around 25% of its agricultural income. Up to 40% of its farmland is used for coffee production. In the highlands, this figure rises to 70%. Peruvian exporters are especially important in the specialty market segment. Peru is the global leader in specialty coffee production. One example of a Peruvian specialty exporter is RainForest Trading.

Next to specialty coffee, Peru also has a dominant position as a supplier of organic coffee. It is the second largest organic coffee exporting country. It has 90,000 hectares of land dedicated to growing organic coffee.

The flavour profile of Peruvian coffees is usually nutty, chocolaty and mildly citrusy. The country’s varieties include Catimor, Pache, Bourbon, Typica and a small amount of Pacamara. Their main processing method is wet processing.

Peruvian coffee is known for its consistent quality and sustainable production. It is one the largest Fairtrade-certified coffee producing countries, and 75% of the coffee industry is owned by smallholders. Peru introduced a national coffee brand, Cafés del Peru, to the international market in 2018.

Table 4: Peru’s competitive profile

| Strengths | Weaknesses | Image on the coffee market |

|---|---|---|

|

|

|

Colombia: a strong brand of high-quality coffee

In 2024, Belgium imported 17,000 tonnes of green coffee from Colombia. Between 2020 and 2024, imports decreased by an average 2.3% every year.

Colombia is the world’s largest producer of washed Arabica. It has a strong national coffee industry that is highly technologically developed. The Colombian Coffee Growers Federation strategically promotes and markets Colombian coffee. The country is well-known for high-quality coffees. Colombian coffee is known for its chocolate, nut, herb, fruit and citrus notes. Its main processing technique is washed processing. The country’s most well-known coffee varieties are Typica, Bourbon, Caturra and Castillo.

Café de Colombia is a protected trademark. It is registered in eAmbrosia. This is the register for protected trademarks in Europe. Registration in eAmbrosia is unique among coffee-producing countries, and it protects the rights of more than 550,000 small-holder families in the country.

The Colombian coffee industry is developing quickly. Coffee companies are increasingly involved in capacity building and product quality. Colombian producers can follow coffee quality and tasting programmes to get certified. The Coffee Quality Institute (CQI) has a strong presence in Colombia. It provides courses in partnership with the National Institute of Professional Training SENA. The country’s coffee has ongoing success in competitions, such as the World Barista Championships.

Successful Colombian cooperatives or private organisations exporting coffee to the international market include Red Ecolsierra and La Maseta.

Table 5: Colombia’s competitive profile

| Strengths | Weaknesses | Image on the coffee market |

|---|---|---|

|

|

|

India: a smaller supplier with unique offerings

Belgium imported 8,700 tonnes of green coffee from India; about half of the import from Colombia. This is about the same as in 2020, when it imported 8,500 tonnes from India. Imports peaked in 2022 at 15,600 tonnes.

India’s coffee exports both Arabica and Robusta varieties to Belgium. The country is known for its Monsoon Malabar coffees. These coffees have a distinctive, mellow flavour profile. This is highly valued in specialty blends. Smallholders dominate Indian coffee production. Indian robustas are popular with roasters to add to their espresso blends.

There is a growing emphasis on both sustainability and specialty coffee production, supported by institutions like the Coffee Board of India. However, India faces significant challenges in expanding its share of the global market. These include issues related to productivity, competition from larger exporters and occasional logistical bottlenecks.

Table 6: India’s competitive profile

| Strengths | Weaknesses | Image on the coffee market |

|---|---|---|

|

|

|

Tips:

- Identify potential competitors. To be successful as an exporter, it is important to learn from them.

- Identify and promote your unique selling points. Give detailed information about your coffee-growing region or origin, the varieties, qualities, post-harvesting techniques and certification of the coffee you offer. You can also tell the history of your organisation, your coffee-growing farm and the passion and dedication of the people who work there. These are all elements that make your company unique.

- Actively promote your company on your website and at trade fairs. Quality competitions also provide good opportunities to share your story. One example is the auctions organised by the Cup of Excellence.

- If you are interested in exporting high-quality coffee, learn more about grading protocols and best practices on the website of the Specialty Coffee Association (SCA). You can also consider getting a Q Arabica or Q Robusta Grader certificate so you can cup and score your coffee through smell and taste according to international standards.

- Work with other coffee producers and exporters in your region if your company size or product volume is too small. As a group, you can promote good-quality coffee from your region and be more attractive and competitive.

- Develop long-term partnerships with your buyers. This includes always complying with their requirements and keeping your promises. See our tips on doing business with European coffee buyers for more information.

Molgo Research carried out this study in partnership with Ethos Agriculture on behalf of CBI.

Please review our market information disclaimer.

Search

Enter search terms to find market research