The Belgian market potential for coffee

Belgium is a major importer of green coffee. Most of this coffee is re-exported to other European countries, especially France and the Netherlands. Belgium offers many opportunities for certified coffee. While organic imports decreased in 2024, Rainforest Alliance imports increased. Belgium is a saturated consumer market. Most growth comes from premiumisation and, though not as much, sustainability initiatives.

Contents of this page

1. Country description: Belgium

Belgium is a country in Western Europe. It borders the Netherlands, Germany, Luxembourg and France. It is a relatively small country with a population of approximately 12 million. However, Belgians are wealthy, with an average gross domestic product (GDP) of €38,600. This is above the European average.

Belgium has three regions that have political, economic and cultural differences. With almost 7 million citizens, Flanders is the largest. The Flemish speak Dutch, and the region borders the Netherlands. Flanders is the richest region of Belgium and home to most coffee companies. Wallonia is the second-largest, with almost 4 million citizens who speak French. Brussels, the third region, is the capital of Belgium and the European Union. Although located in the Dutch-speaking Flanders, Brussels’ main language is French.

Figure 1: Regions of Belgium

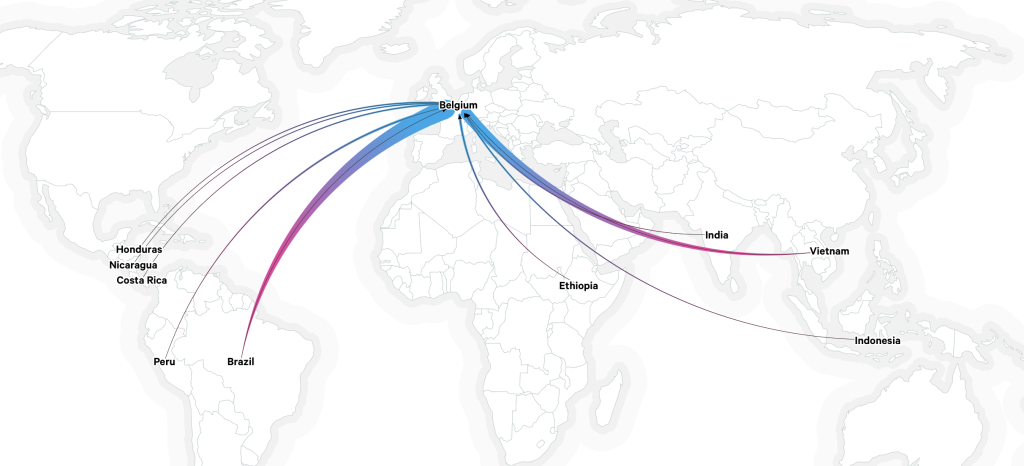

Belgium is one of Europe’s main importers of green coffee. Antwerp is one of Europe’s largest harbours and serves as a main entry point into Europe. Belgium is also an important consumer market. Coffee is an important part of Belgian culture, with a large out-of-home segment. Figure 2 shows the largest green coffee trade flows into Belgium. Broader arrows indicate larger trade flows.

Figure 2: Main trade flows of green coffee into Belgium

Source: Resource trade

Tips:

- Find out which coffee companies operate in Belgium to target potential business partners. You can find lists of coffee companies on the websites of the European coffee trip and Company data. Javry offers a list of roasters per region. You can find a list of coffee shops on Enjoytravel.

- Find more information on the Koffiecafe (Belgian Coffee Association) website . The association publishes sector news and information about national events.

- Learn about the main European markets by reading the CBI country studies. These cover the Spanish, German, French, Swiss and Scandinavian markets, and many others.

- Check out the website of Belgium’s largest port, the Port of Antwerp Bruges. On this website, you can learn about these key trade hubs and discover potential business partners.

- Use your browser's translation function to read studies in your language. Since many resources are in Dutch or French, this will help you to understand the information better. For instructions on how to do this in Chrome, visit the Google Support website.

2. What makes Belgium an interesting market for coffee?

Belgium is one of Europe’s main ports. About two-thirds of its coffee imports are re-exported to other European countries. Almost 90% of its green coffee is sourced from producing countries directly. At the same time, Belgium has an interesting consumer market, with a large out-of-home market and a high focus on quality.

Belgium is Europe’s fourth largest green coffee importer

In 2024, Belgium imported 282,000 tonnes of green coffee. Of this, 248,000 tonnes (88%), came directly from producing countries. This is slightly less than Spain’s imports (273,000 tonnes). It represents about one-quarter of German imports, Europe’s largest importer. Over the last decade, Belgium’s imports volume have gone up and down between 280,000 and 310,000 tonnes. 2020 and 2021 imports were particularly high.

Source: Eurostat, 2025

Tip:

- Read our study on coffee demand for detailed information about the European green coffee bean trade.

Belgium and Germany are Europe’s largest trade hubs

Belgium is the largest European re-exporter of green coffee. In 2024, 184,000 tonnes of green coffee were exported to other countries. This represents around two-thirds of its imports (66%). Belgium re-exports slightly more green coffee than Germany. Germany re-exported 179,000 tonnes of unaltered green coffee in the same period.

However, a significant portion of Germany’s green coffee imports, 141,000 tonnes, was decaffeinated before export. Since this processing adds value, these exports are not classified as simple re-exports. If we combine Germany’s re-exports with its decaffeinated green coffee exports, Germany exports much more than Belgium overall (321,000 tonnes compared to Belgium’s 185,000 tonnes).

Belgium mainly re-exports green coffee to other European countries: France (76,000 tonnes), the Netherlands (43,000 tonnes), Spain (14,000 tonnes), Germany (11,000 tonnes) and Poland (11,000 tonnes).

Before re-exporting, most coffee is stocked at the port of Antwerp. Antwerp is Europe’s largest harbour in terms of stocking capacity. Specialised companies take care of warehousing. This means offering special services, such as quality checks, among other responsibilities. Molenbergnatie is the largest warehousing company in Antwerp.

As a trade hub, Belgian imports fluctuate a lot based on availability. In recent years, weather conditions have heavily influenced Brazilian (mainly Arabica) and Vietnamese (mainly Robusta) production. This has influenced import figures significantly. For example, the share of Robusta decreased from 30% in 2023 to 18% in 2024.

Belgium offers a very large consumption market

Coffee is part of Belgian culture. This is true of all regions. Flemish consumers prefer lighter roasts while Walloons like their coffee darker. On average, Belgians drink 5.7 kg of roasted coffee per year, which is more than Italians. Almost 87% of Belgians drinks coffee every day, averaging four cups per person. Most coffee is consumed in the morning. Over half of Belgians say they need to start the day with a cup of coffee.

According to Tchibo, each Belgian consumer spent about €281 per year on coffee in 2022. For 2025, this was expected to rise to €349 (+24%). In the same period, German spending rose only 9%, from €232 to €252. Growth in Belgium comes from premiumisation (spending on more expensive products) and volume growth. Spending was predicted to increase by 24% while volumes were expected to grow 13%.

Belgium has a large out-of-home coffee market. A lot of coffee is consumed at the office. This is especially of the services sector, where 84% of employees drink coffee daily. In the technology and IT sector, over 50% of employees drink at least three cups of coffee every day.

Over 50% of Belgian coffee consumers do not think the coffee at the office is of good quality. With at-home coffee increasing in quality, Belgians have become more demanding in terms of the coffee they get at work. As a result, there has also been more demand for higher-quality coffee in the out-of-home market in recent years.

The type of coffee consumed at the office is a bit different from coffee consumed at home. Ground coffee is most consumed both at home and at work.

Source: Alsafra et al., 2022

Based on a large survey, the taste of coffee is the most important reason for Belgian consumers to choose a particular brand, followed by the price. After taste and price, habits and fair trade aspects are also considered. Organic, health, caffeine level and packaging are less important. Local production hardly factors into decision making at all. Note that this study reports consumers’ perceptions. Marketing and unconscious influence by coffee brands are not reflected.

Younger generations are more inclined to add milk to their coffee. Slightly less than 50% state that either cappuccinos or latte macchiatos are their favourite types of coffee drinks.

Belgium sources most coffee from producing countries directly

In 2023, 91% of the coffee imports came directly from producing countries. Brazil (341,000 tonnes) is the largest supplier of green coffee to Belgium by far. Vietnam (207,000 tonnes), Honduras (76,000 tonnes), Uganda (53,000 tonnes), Colombia (40,000 tonnes) and India (34,000 tonnes) follow.

Long- and short-term projection

Belgium’s consumer market is saturated. This means the consumption volume will probably remain stable. Because the port of Antwerp is a popular destination, its position as a hub into Europe is safe. The factor with the greatest impact on the future volume is the price of coffee. Due to increased prices, many buyers emptied their stocks. If prices drop, buyers will become interested in refilling their warehouses.

In the long term, coffee imports are under pressure due to expected global shortages. Global demand for coffee will likely grow due to growing consumption, mainly in Asia. At the same time, supply will likely be lower due to climate change and aging farmer population. You can read more about this in our study on coffee demand.

Tips:

- Visit the Access2Markets website to analyse European and Belgian trade dynamics and to build your export strategy. By selecting Belgium as your reporting country, you will be able to follow developments such as the emergence of new suppliers and the decline of established ones.

- Visit the Brussels Coffee Show or the Ghent Coffee Fest to expand your network in Belgium.

- Join the World of Coffee, which is held in Brussels in 2026.

- When visiting a trade fair, prepare well. Make sure you have defined your goals, be prepared to share your story and promotion materials, and follow-up afterwards. You can read more tips in this practical guideline on how to navigate a coffee conference.

3. Which coffees offer the most opportunities for the Belgian market?

Belgian consumers value quality and sustainability. As a result, certified coffee products have a strong presence in the market. Major certifications include Rainforest Alliance, Fairtrade and organic. Many products have more than one certification.

Demand for Rainforest Alliance has grown

Despite a 5% production reduction, demand for Rainforest Alliance-certified coffee increased in 2024. Globally, Rainforest Alliance certified imports rose from 864,000 tonnes in 2023, to 1,050,000 tonnes in 2024. This growth mirrors demand in Europe. It grew from 615,000 tonnes to 751,000 thousand tonnes between 2023-2024. Belgium, being an important re-exporter, also profited from this growth. Belgian imports rose from 32,000 tonnes to 41,000 tonnes, making Belgium Europe’s fifth-largest Rainforest Alliance importer. This is just 1,200 tonnes less than the United Kingdom.

Supremo is a Belgian trader and part of Ecom. The trading company works with several certification programmes, including Rainforest Alliance, Fairtrade and organic. Coffeeteam is another Belgian trader that works with Rainforest Alliance.

Fairtrade is well-known among consumers

Fairtrade is the best-known certification standard in Belgium. 65% of Belgians recognised the logo in 2022. This is a slight decrease from 2020. Fairtrade green coffee sales amounted 2,686 tonnes in 2024. This is up 0.7% from 2023. In terms of market share, 4.4% of all coffee sales were Fairtrade certified in 2024. This is the same as 2023.

Sucafina is a global coffee trader, also based in Belgium. The company sources coffee certified according to different certification programmes, including Fairtrade. The Fairtrade sales in 2024 increased by 1.5% after a 7% decline in 2023.

Belgium follows the European trend, organic imports drop

European organic coffee imports dropped in 2024. Organic import levels were stable between 2020 and 2023, with slight fluctuations between 131,000 tonnes and 136,000 tonnes. In 2024, however, imports dropped by 12.8% to 116,000 tonnes.

The main reason for drop in European imports was the increased price of coffee. On the consumer side, many buyers opt for non-organic coffee to keep coffee available. From the supply side, a lot of organic coffee is sold as conventional coffee. Many organic producers could sell their products for similar prices as conventional coffee, with fewer obligations.

Reduced supply and demand can also be seen in the Belgian organic market. Belgian organic imports also dropped by 11.7% to 26,000 tonnes in 2024. Rucquoy is a Belgian trader that sources organic coffee.

Fairtrade organic is the most common type of multi certification

Belgium has a large market for double-certified coffee. Most multi-certified coffee is Fairtrade-Organic certified.

Many large Belgian retailers sell multi-certified coffee, like Colruyt, Delhaize and Carrefour Belgium. Delhaize and Carrefour carry their own private label coffees that are often certified by both Fairtrade and EU Organic. Colruyt only sells third-party certified coffee.

Company standards gain importance

Many major coffee companies have developed their own sustainability programmes, known as company standards. Most company standards intend to set a baseline for sustainable purchases. However, they are usually less demanding than independent third-party programmes like Rainforest Alliance and Fairtrade. Many company standards are recognised by the Global Coffee Platform, according to its equivalence mechanism. Ecom Sustainable Management Services is a company standard present in Belgium.

There are no figures on how much of Belgian coffee imports complies with coffee standards. However, globally these company standards are on the rise. In 2020, according to the Global Coffee Platform, 4.4% of all coffee sales complied with a company standard. By 2023, this had grown to 21%.

The share that complies with a company standard differs per company. The standards that are important also differ per producing country. In Brazil, Enveritas Green is the main company standard. Enveritas certifies coffee for JDE Peets. This next most important is Louis Dreyfus’ company standard.

Tips:

- Find potential organic business partners in Belgium on this list of Belgian organic coffee importers. For Rainforest Alliance, check the Belgian Rainforest Alliance-certified coffee brands.

- Look for potential buyers online if you supply certified coffee. For instance, you can find Belgian importers of Fairtrade-certified coffee on the Fairtrade Belgium website.

- Promote the sustainable and ethical aspects of your production process and support these claims with certification. Read our study on doing business with European coffee buyers for more tips on marketing and promoting your coffee.

- Before committing to a certification programme, make sure to check market demand and whether it will be cost-beneficial for your product. Always do this in consultation with your potential buyer.

- Find out which certification standards and company standards are important in your country. The Global Coffee Platform’s sustainability report is a good starting point. Alternatively, you can consult the websites of the different standards and their certification bodies.

- Read our studies on certified coffee, multi-certified coffee, organic coffee and relevant social certifications to identify more opportunities in these markets.

Belgium has a vibrant specialty coffee market

Belgium has a vibrant specialty coffee culture. Demand for specialty coffee is especially strong in large cities, such as Brussels, Antwerp and Bruges. There are no exact numbers about the size of the Belgian specialty coffee market. According to experts, this market is growing. Examples of micro roasters are Gust Coffee Roasters, De Goudvink, Parlor Coffee and MOK Specialty Coffee Roastery. All these companies serve their own specialty coffees.

Belgian companies active in the specialty segment sometimes source their coffee from producers directly. This underlines the importance of coffee origins and social impact. It makes storytelling an increasingly important aspect. One coffee exporter with particularly effective storytelling is the Brazilian Fazendas Dutra Organic Specialty Coffee. Belgian roaster Ray & Jules buys from farms directly. The company roasts coffee using solar power.

The Belgian specialty coffee market is expected to continue growing. However, the current market is very uncertain. Belgium faces an energy crisis, volatile coffee prices and global trade tensions. These factors could affect the future growth of the specialty market.

Almost all specialty coffee is Arabica. However, Robustas are entering the Belgian specialty coffee market. Robustas can be an interesting alternative in themselves or added to specialty coffee blends to reduce the price.

Tips:

- If you offer rare coffees, reach out to Belgian specialty coffee traders or specialty coffee roasters that value innovation, such as OR Coffee. Belgian specialty coffee lovers are very interested in trying new flavours.

- Invest in cupping facilities: a lab and skilled Q-graders. By better understanding the quality and value of your own product, you learn the language of the buyer and are better positioned to negotiate the right price.

4. Which trends offer opportunities or pose threats in the Belgian coffee market?

The European coffee market is changing, and the Belgian coffee market with it. Most trends apply to the whole European region. These trends are described in our study on trends in the European coffee market.

Premiumisation drives growth on the Belgian consumer market

The Belgian market is growing more in terms of value than volume. Between 2021 and 2023, coffee sales value increased from €652 million to €775 million (19%). Belgium is a wealthy country, and the market is saturated. Growth in volume mainly comes from the growing population, and Belgians are starting to consume coffee at younger ages. Most growth, however, comes from higher-priced products. Between 2021 and 2023, volume increased from 42,700 tonnes to 44,600 tonnes (4.4%).

The premiumisation of the Belgian coffee market shows in several ways. First, demand for whole-bean coffee is increasing. Coffee enthusiasts often have their own espresso machines and try to create their perfect coffee. This coffee can be specialty coffee and is often of above-average quality.

Second, the ready-to-drink (RTD) market is growing. RTD coffees are often expensive. Besides coffee, these drinks contain many other ingredients, such as milk and sugar. Many of these are iced coffees. These ready-to-drink coffees also tap into other trends, such as using plant-based milk alternatives and adding protein to their products. This creates opportunities for suppliers of lower quality coffee. As coffee is only one of many ingredients in RTDs, the quality of the coffee is less important.

While premiumisation was driven by demand for capsules and pads prior to 2020, demand for these products is declining. This particularly applies to the Belgian market. In terms of volume, the market share of capsules and pads decreased from 16% to 15% in 2023. In Belgium, this market declined from 31% to 22%.

Café de Colombia has tapped into this trend. The company launched its premium brand Juan Valdez, selling specialty ground and whole bean coffee. The company exports roasted coffee to Europe, including Belgium. Volcán Azul from Costa Rica also exports roasted specialty coffee to Europe, for sale in Belgium.

Sustainability initiatives affect the Belgian coffee sector

Like in other European countries, Belgian coffee companies work on sustainability. They do so for multiple reasons, like ethics, EU regulations, competition and high energy prices.

One way this can be seen is in the use of reusable capsules or recyclable coffee capsules and pads. Beyers, part of Sucafina, switched their production from traditional to entirely compostable pads. The company produces 1.4 billion pads every year, partly sold under private label. Juan Valdez from Colombia started producing compostable coffee pods in 2016.

Another example of increasing sustainability is reusing ground coffee. Coffee grounds are an excellent base for growing mushrooms. Belgian company Permafungi collects coffee grounds from cafes and restaurants. After harvesting, the leftover material (mushroom compost) is used to grow chicory in soil, supporting a full circular lifecycle. In terms of materials, Belgian company Orineo uses coffee grounds mixed with plant resin to create panels for flooring and furniture. Finally, textile producer S. Café uses coffee grounds to create outdoor and sports fabrics. The fibres dry quickly, control odours and provide UV protection. They are found in well-known brands like Timberland and The North Face, showing coffee’s value beyond brewing.

A third example is the electrification of the roasting facilities. Beyers Coffee aims to build a fully electric roasting facility to reduce its impact on climate change. Electric roasting is done at much lower temperatures, which also affects the roasting process. Café Compadre from Peru roasts its coffee with solar power. The company sells its coffee cups to IKEA.

Tips:

- Read more about legislation in our studies on Organising your exports and Requirement for exporting coffee and Entering the Belgian coffee market.

- Read our study on Exporting roasted coffee, to learn more about the possibilities of tapping into this market.

- Inform yourself on how to engage with sustainability trends. Read our Tips to go green, our Tips to become socially responsible, our Tips to become EUDR compliant, and our study on The green deal.

Molgo Research carried out this study on behalf of the CBI in partnership with Ethos Agriculture.

Please review our market information disclaimer.

Search

Enter search terms to find market research

Do you have questions about this research?

Do business when it makes sense. This is the time to act and look for strategic partners which serve you best in the long term.

Ali Yousefi, Operations manager at OR Coffee Roasters