Entering the European market for olive oil

Selling olive oil in Europe starts with strict rules and tests. Panels judge virgin oils by taste, while laboratories check safety and composition. Buyers expect proof of safety and correct labelling, and most also ask for GFSI food safety schemes. Bulk olive oil is imported through large brand owners. High-end oils go through specialised importers and fine-food retail. Competition from Spain, Italy and Greece is intense, and Tunisia, Morocco and Türkiye are growing competitors. Prices are linked to crop sizes.

Contents of this page

1. What requirements and certifications must olive oil meet to be allowed on the European market?

Olive oil exporters that want to enter the European market need to put their products through regular laboratory and sensory tests. Virgin olive oils are the only food sold in Europe where sensory testing is required by law to define quality. To sell virgin olive oil in the European Union (EU), a trained tasting panel must test it. This is according to the Commission Implementing Regulation (EU) 2022/2105.

What are mandatory requirements?

Olive oil sold in Europe must be tested for safety. Testing for safety includes complying with established maximum levels for harmful contaminants. Olive oil product composition is very important. Olive oil must meet requirements related to acidity, content of specific chemicals and certain sensory characteristics. The product label should also show the type of olive oil.

Tariff barriers

Many countries around the Mediterranean can sell olive oil to the EU at zero duty. This if they follow the free-trade agreement rules and present proof of origin (EUR.1/EUR-MED or an origin declaration). These rules are set by the Pan-Euro-Mediterranean (PEM) system. The revised PEM Convention on preferential rules of origin entered into force in 2025.

Most olive oil producing countries are members of the Euro-Mediterranean partnership agreement. The EU also has free-trade agreements with Albania, South Africa, Palestine and some South American countries.

A specific tariff quota is used for Tunisian olive oil. The EU allows imports of 56,700 tonnes per year of virgin Tunisian olive oil duty free under TRQ 09.4032. This quota is managed with import licences under EU rules. Amounts above this pay the normal ‘erga omnes’ duty of €124.50 per 100 kg. For all imports, TARIC is the official database for the EU customs tariff and trade policy measures.

European importers must also have import licences to get reduced tariff rates under the tariff quotas. Currently, most olive oil importers with licences to import within a given quota are big olive oil blending companies from Spain, Italy, France and Belgium.

The United Kingdom (UK) has a separate Tunisian quota. For 2025, the official notice shows 6.64 million kg at zero duty, also managed by licences.

Olive oil from the Western Balkans usually enters the EU at 0% duty under EU autonomous trade preferences. The EU-Türkiye customs union covers industrial goods. Agricultural products (including olive oil) are outside the customs union’s tariff-free regime.

Mineral oil hydrocarbons

Mineral oil hydrocarbons (MOSH and MOAH) are contaminants sometimes found in olive oil. In 2023, a French consumer test of 24 olive oils found MOSH/MOAH in many samples. Although there are no official limits yet, more research into their impact on human health is expected. Between 2020 and 2024, 8 alerts about mineral oil hydrocarbons were submitted to the EU’s Rapid Alert System for Food and Feed (RASFF).

Pesticide residues

The EU has set maximum residue levels (MRLs) for pesticides in and on food products. The EU regularly publishes a list of approved pesticides that are authorised for use. Although high levels of pesticide residues are not very common in olive oil, some European importers do request detailed tests.

Between 2020 and 2024, 7 incidents involvinghigh levels of pesticide residues in olive oil were reported to RASFF.

Other contaminants

Other commonly requested contaminant controls for olive oil are related to the presence of heavy metals, irradiation and polycyclic aromatic hydrocarbons (PAHs). Commonly tested heavy metals include cadmium, lead and mercury. The presence of PAHs can be connected to the production of olive pomace and smoked oils.

Tips:

- Perform laboratory tests only in ISO/IEC 17025:2017 accredited laboratories.

- To prepare for potential new MRL changes, read the ongoing EU reviews of MRLs.

Olive oil composition

EU olive oil legislation defines 8 different categories of olive oil, as well as the relevant methods of analyses that member states should use.

The sale of fake or falsely declared olive oil in Europe is prevented through regular controls. Each European country must perform a certain number of controls to ensure that marketing standards for olive oils are respected. Despite frequent controls, irregularities are still found.

Common fraud methods are adding cheaper seed oils, mixing in refined or pomace oil, and making false claims about quality grade, organic status and origin. Major authenticity tests include:

- Waxes: Presence can reveal pomace oil in a blend;

- 2-glyceryl monopalmitate (2-GMP): Presence can reveal re-esterified (reconstituted) oils;

- Stigmastadienes: Indicates refined oil added to virgin oil;

- ECN-42 (triacylglycerols): Helps detect seed oil additions;

- Fatty-acid profile (and sterols): Serves to check if an oil fits olive oil or blend ranges.

There are other International Olive Council (IOC) tests that are used to confirm authenticity.

Quality requirements

The different categories of olive oils are graded based on quality parameters on the physical and chemical features. They are also graded based on the organoleptic (sensory) aspects. High-quality olive oil has low acidity, a highamount of polyphenols and good flavour.

The main chemical features related to quality are the acidity level, peroxide index, level of oxidation, fatty acid content and sterols composition. Chemical composition of olive oil depends mainly on olive cultivars, production region, olive health, freshness and production process. Acidity increases when olives are too mature (when it starts to ferment), when temperature during crushing is too high, and when the time between harvesting and pressing is too long. Storage time also increases acidity.

Additional sensory testing is necessary to define characteristics such as fruitiness and the absence of organoleptic defects. Sensory tests are required only for virgin olive oils, and they are performed by a team (panel group) of 8–12 qualified assessors. Officially recognised assessors must participate every year in proficiency tests to prove their competence.

Tips:

- To avoid fermentation, do not store olives in big piles for a long time.

- Separate unfiltered oil from any sediment and water after extraction as soon as possible to avoid the appearance of sensory defects. Repeat this process a few times before bottling.

- Train employees in your company to perform in-company sensory tests for the regular monitoring of olive oil quality. Follow the ISO 8586:2023 training guidelines for sensory assessors.

Packaging requirements

In the EU, olive oil sold to final consumers must be in containers of 5 L or less with an opening that cannot be re-sealed after first use. Countries may allow bigger containers for restaurants and other collective kitchens. These rules are set out in Regulation (EU) 2022/2104. There is no size limit for bulk oil for business use, but it is still covered by the EU marketing standard and official checks.

Phthalates are chemicals that may be found in samples of olive oil. They can get into the oil through the plastic packaging but also from processing equipment. Limits are set in the European regulation on plastic materials and articles intended to come into contact with food. In December 2024, the European Commission adopted a ban of bisphenol A (BPA) in food contact materials.

Labelling requirements

The European olive oil marketing regulation regulates the information that must be placed on the retail label and what optional information can be included. Mandatory information includes the following:

- Category of olive oils (either EVOO, virgin, olive oil composed of refined olive oils and virgin olive oils, or olive-pomace oil) and a category description;

- Storage conditions: must be stored away from light and heat;

- Place of origin: obligatory for extra virgin olive oil (EVOO) and virgin olive oil. If olives are harvested in one country but processed in another this must be also indicated on the label. For example, 'extra virgin olive oil obtained in Italy from olives harvested in Greece';

- Packaging plant number.

Optional labelling on EVOO can include special quality characteristics such as "first cold pressing", "cold extraction" and special sensory characteristics. These are allowed only under strict conditions. EVOO labelling can also include maximum acidity expected by expiry date and harvesting year.

Tips:

- Read more about the transport and storage conditions for olive oil on the websites of Transport Information Service and Cargo Handbook.

- Read the CBI study about buyer requirements for processed fruit and vegetables for a general overview of buyer requirements in Europe.

What additional requirements do buyers often have?

Some specific buyer requests have become equally important. These include compliance with food safety, quality and sustainability standards.

Specific quality characteristics

Buyers may have special quality preferences for olive oils in terms of intensity and olive ripeness. Regarding intensity, all olive oils can be classified as intense (robust), medium or light (delicate).

Some buyers specialise in premium olive oils. Premium olive oils usually have an extremely low acidity level: if possible, less than 0.3g per 100g.

Trading packaging requirements

A large amount of olive oil is exported as bulk. Olive oil is often shipped in bulk in 200 L drums, 1,000 L intermediate bulk containers (IBCs), flexitanks (20-24 tonnes) or tank trucks. These are recognised in the Codex Alimentarius code of practice for edible oils. For the food service sector, most pack sizes vary between 5 L and 25 L and often tin cans or bag-in-box are used.

The most common sizes of retail olive oil bottles in Europe are between 0.5 and 1 L. Premium oils are often 0.50 L or 0.75 L, while 100 ml and 250 ml are also used for catering.

Dark glass bottles and metal cans protect olive oil from light. Bag-in-box packaging helps reduce contact with air, and plastic bottles made of polyethylene terephthalate (PET) are also used.

Food safety certification

Most established European importers will not work with you if you cannot provide some type of food safety certification.

European buyers mostly ask for Global Food Safety Initiative (GFSI) recognised certification. For olive oil, the most popular certification programmes recognised by GFSI are:

- International Featured Standards (IFS);

- Brand Reputation through Compliance Global Standards (BRCGS);

- Food Safety System Certification (FSSC 22000).

Note that food safety certification is only a basis to start exporting to Europe. Serious buyers will usually visit or audit your production facilities before buying.

Sustainability requirements

There is an increasing demand for sustainably-sourced food in Europe. To help consumers make more ecological choices, new labelling systems have appeared such as Eco-Score, Planet Score and Enviroscore. For example, the Italian producer Monini promotes its brands Classico and Delicato as CO2 neutral. Along with requirements related to environmental impact, there is an increasing demand for a more transparent and fair supply chain.

One way to show that you take care of farmers and workers is to get certified with standards such as Fairtrade, Fair for Life and Rainforest Alliance. Fairtrade is the most used ethical certification for olive oil, especially for olive oil from Palestine and Syria. Fairtrade International has minimum prices and premiums for olive oil classified by origin, as well as by category (organic or conventional, and extra virgin or virgin).

Some buyers want suppliers to follow their code of conduct. Other companies require suppliers to adopt one or more common standards. Examples include independent audits such as the SMETA audit (by Sedex), the ETI Base Code (by the Ethical Trading Initiative) and the amfori BSCI code (by amfori). If olive oil is intended for direct retail sales, suppliers will have to follow a specific code of conduct developed by retailers.

Wastewater generated by olive mills contains high concentrations of phenols, which can contaminate water if released untreated.

Tips:

- Read CBI tips to go green and CBI tips to become a socially responsible supplier to become familiar with market requests on environmentally friendly operations and sustainability;

- Read the CBI study on trends in the European processed fruit and vegetables market for an overview of developments regarding sustainability in Europe.

What are the requirements for niche markets?

Organic olive oil

To market olive oil as organic in Europe, olives must be grown using organic production methods. Growing and processing facilities must be audited by an accredited certifier before exporters can place the EU’s organic logo on the packaging. This is also necessary before you can add the logo of the standard holder: for example, Soil Association in the UK and Naturland in Germany.

Regulation (EU) 2018/848 sets the rules for organic production and the labelling of organic products in the EU. Besides this, Regulation (EU) 2021/1165 authorises certain products and substances for use in organic production. Finally, Regulation (EU) 2021/2307 provides rules on documents and notifications that are necessary for imports of organic products.

Halal or kosher certification

The Islamic dietary laws (halal) and the Jewish dietary laws (kosher) impose specific dietary restrictions. If you want to focus on Jewish or Islamic ethnic niche markets, you should consider implementing halal certification or kosher certification schemes.

Tip:

- Consult the Sustainability Map database for information on a wide range of sustainability labels and standards.

2. Through which channels can you get olive oil on the European market?

If you want to offer olive oil of standard quality in big volumes, European olive oil producing, blending and bottling companies are good entry points. However, independent specialised olive oil importers are also an important channel. This is especially for food service or high-end market segments.

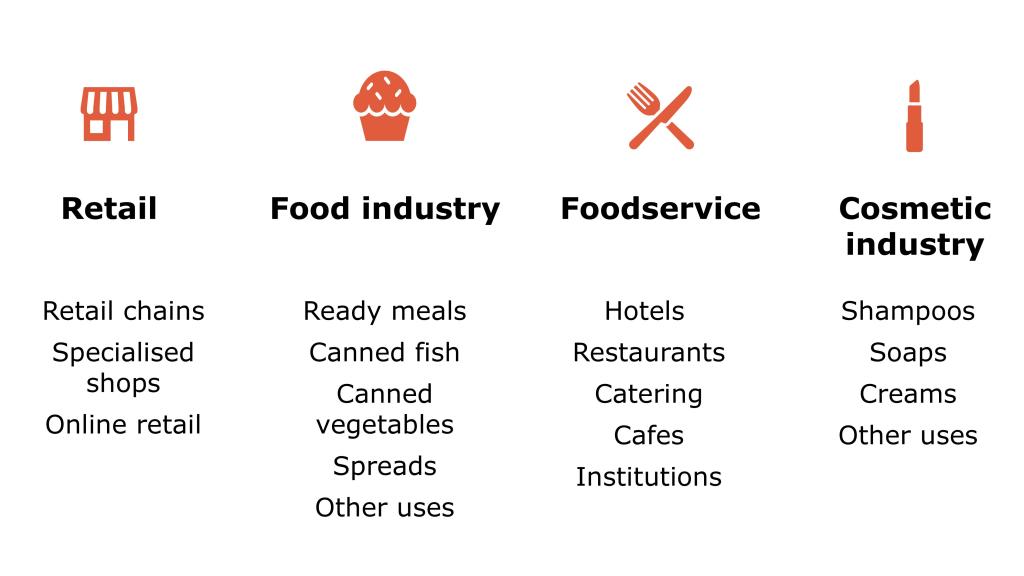

How is the end-market segmented?

Olive oil in Europe is mostly used for home consumption, so retail sales have the largest share. Olive oil is also used by the food processing industry and by foodservice. The retail segment represents approximately 60% of the European olive oil market. Within this segment, the largest volumes are sold through supermarkets.

Figure 1: End-market segments for olive oil in Europe

Source: Autentika Global, 2025

Retail

Retailers mostly buy products through intermediaries, such as specialised distributors. Online retail sales of olive oil currently account for a small share of the market, but they are growing.

Major sub-segments of the olive oil retail market in Europe include:

- Retail chains: These are the main outlet for olive oil sales. Mainstream retailers are selling more olive oils, including organic and higher quality oils under private labels;

- Specialised olive oil shops: Relevant for high-quality and single-origin EVOO sales. Oil & Vinegar from the Netherlands is a specialised shop that started in the Netherlands. It now has stores in several European countries. Some national chains also specialise in olive oil, such as Oliviers & Co in France;

- Specialised ‘fine food’ stores: These shops sell a wider range of food and premium olive oils. Some are luxury food department stores such as Fortnum & Mason in the UK. They can also exist as food corners in shopping malls or in luxury department stores such as La Grande Épicerie in France and De Bijenkorf in the Netherlands;

- Specialised organic and health food shops: Important for suppliers of certified organic olive oils. Many organic shops are part of specialised organic food retail chains. Some European shops selling organic olive oil are also drugstores (for example, dm and Rossmann), variety shops (such as HEMA) or food supplement stores (such as Holland & Barrett);

- Specialised ethnic shops: These shops provide opportunities to enter the market without competing directly with the leading retail brands;

- Specialised ethical shops: This is a niche segment that provides opportunities for fair trade and ethical certified suppliers;

- Online retailers: Online-only retailers usually sell premium olive oils, often from specific origins or from single producers.

Food industry

Most food industry processors rarely use EVOO as an ingredient. However, the number of products with EVOO as an ingredient, is on the rise. Adding olive oil to food products improves the consumer’s image of the product. Most food industry companies are supplied through wholesalers and do not import olive oil directly. The biggest users of olive oil in the European food industry include:

- Ready meals: Producers of chilled, canned and frozen ready meals use olive oil as an ingredient. Most of those products include Italian style products, such as pizzas, pastas and pesto sauce, or Spanish style products, such as frozen paella. Mediterranean style ready meals also using olive oil as an ingredient are appearing on the market, such as Greek style salads and pita breads, and Middle Eastern tabbouleh salads;

- Canned fish: Producers of canned fish use oil in most of their products.;

- Canned vegetables: This includes processed and canned vegetables, such as grilled artichokes, grilled peppers, chopped garlic and canned pasta sauces;

- Spreads: Many spreads include olive oil as a healthy ingredient that also improves flavour;

- Other food industry products: These include dips, sauces, condiments, table olives, dressings and bakery snacks.

Food service

The food service segment (hotels, restaurants, catering and public organisations) is usually supplied by specialised wholesalers and distributors. Most demand comes from Mediterranean food restaurants and fast-food chains, such as pizzerias and tapas bars. High-end restaurants serve premium olive oil as well.

The food service segment is quite large in Europe, in terms of olive oil use. In order to reach end buyers in this segment, it is necessary to use specialised distributors and specific packaging, such as 5L tin cans.

Most olive oil used for food preparation in restaurants is not virgin. However, olive oil served together with dishes is mostly EVOO.

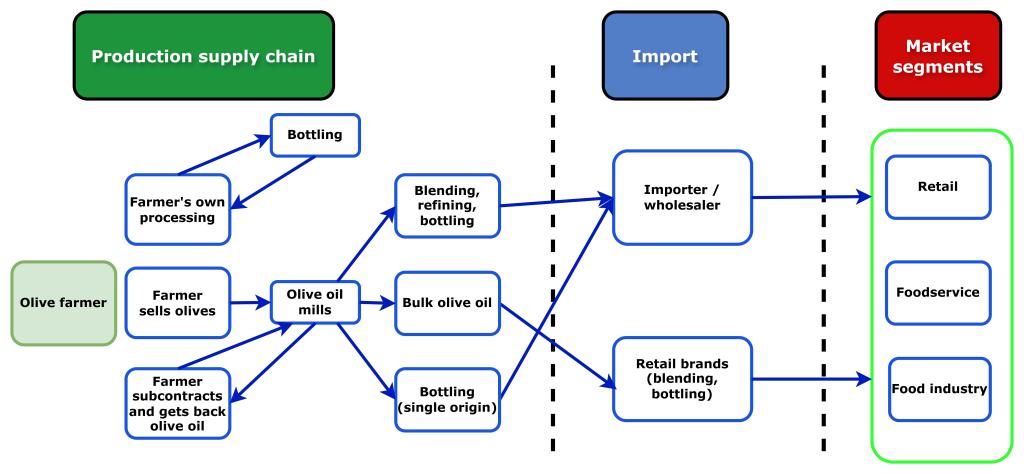

Through which channels does olive oil end up on the end-market?

The most important channels for placing olive oil in Europe are large producing and bottling companies. They import bulk olive oil for blending and production of their own retail brands. However, independent, specialised olive oil importers are also an important channel, especially for companies willing to enter high-end segments in the European market.

Figure 2: European market channels for olive oil

Source: Autentika Global, 2025

Importers (Wholesalers)

Unlike many other food sectors in Europe, in the olive oil sector the largest importers are not traditional wholesalers. Instead, the largest importers arefirms that market olive oil under famous retail brands. These companies import bulk olive oil from their own production locations to different destinations in Europe.

Specialised importers, in turn, import either bulk or bottled olive oil and sell it to the food service segment or to specialised shops. Some specialised importers are also exclusive distributors for certain olive oil brands.

For new suppliers, it is hard to establish long-term relationships with leading brands that already work with selected suppliers. You often need to offer the same quality, but at better prices than your competitors. On the other hand, specialised importers of premium olive oil offer better prices, but ask for exceptional quality, new flavour profiles and interesting stories behind your product or brand.

The most important types of olive oil importers are the following:

- Leading retail brand producing companies: These are companies that buy most of the olive oil in the world. They are relevant for bulk exporters, but less relevant for suppliers of bottled oils. Examples include Deoleo, SOVENA, Migasa, Salov and Acesur;

- Retail bottling companies and brand distributors: These companies are often bottlers of different types of edible oils. Some are multinational companies selling many different products and international brands. They can be interesting for bulk olive oil exporters. Some examples are Avril Group, Unilever, Princes Group, and Di Luca & Di Luca;

- Specialised olive oil importers: Some of them act as bulk wholesalers, while some are specialised in trading premium olive oil and supplying olive oil shops. Examples include The Oil Merchant, Artisanal Olive Oil Company, Assisi (Oil & Vinegar brand), Henry Lamotte Oils, the gift of oil, Meyer & Co and Imex Delikatessen;

- Specialised natural and organic food importers: Examples are Le Temps des Oliviers, Bio Planète, Naturata, Raw Living, and Gebana;

- Other importers: Some importers provide opportunities for niche markets. They include single-origin olive oil importers, fair-trade and sustainable product importers, and ethnic food importers.

What is the most interesting channel for you?

Specialised olive oil and vegetable oil importers are the best contacts for exporting olive oil to the European market. This is particularly so for new suppliers willing to reach the retail segment more easily.

Specialised importers usually have a good knowledge of the European market and monitor the situation in olive oil producing countries closely. On the other hand, large-scale producers willing to provide standard quality and competitive prices can also consider working with the larger producing and bottling companies.

Tips:

- Study the exhibitor lists of large trade fairs, such as Anuga, SIAL, Alimentaria and PLMA to find potential buyers for your olive oil.

- To reach buyers in the food service segment, look for suppliers at specialised food service events, such as SIRHA and Internorga.

- If you are producing premium olive oil, enter your product in international competitions to attract potential buyers. Also consider exhibiting at specialised fine food exhibitions, such as the International Food & Drink Event and Speciality & Fine Food Fair.

3. What competition do you face on the European olive oil market?

As most of the olive oil in the world is produced in Europe, you can expect fierce competition from Spain, Italy and Greece. Suppliers from Tunisia, Morocco and Türkiye are also strong competitors.

Which countries are you competing with?

The main competitors for emerging olive oil suppliers are in Europe, namely Spain, Italy, Portugal and Greece. Tunisia is the main non-European supplier, followed by Morocco and Türkiye. Spain is characterised by large-scale production and a price-competitive assortment. In Italy and Greece, many small-scale producers produce high-quality olive oil, while Tunisia has the strongest organic product range.

Source: Autentika Global, ITC, Eurostat, 2025

Europe: The leading world supplier of olive oil

Spain is the leading olive oil producing country in the world, and the largest supplier to other European countries. Spain is expected to produce 1.28 million tonnes of olive oil in 2024/2025, up from 854,000 tonnes in the previous season. In 2024, Spain exported 517,944 tonnes of olive oil to other European countries, at a value of €3.53 billion. Export volumes to European countries decreased by 9% per year between 2020 and 2024. However, export values increased by 21% annually in the same period. Most of the olive oil exported from Spain is EVOO (68%), followed by refined and blended oils (27%).

The largest share of olive oil production is in Andalusia (80%) followed by Castilla-La Mancha (8%), Extremadura (5%) and Catalonia (3%).

Spain grows 260 different olive cultivars, but the most important is Picual.

In 2024/2025, Greece was the second-largest European olive oil producer with 250,000 tonnes. This was up from 175,000 tonnes a year earlier. However, on average, Greece produces less olive oil than Italy. In 2024, Greece exported 128,357 tonnes of olive oil to Europe at a value of €882 million. Export volumes to Europe decreased by 10% annually while export values increased by 19% annually between 2020 and 2024.

Greek production is focused on high quality olive oil and EVOO represents a large share of the produced output. Greece is also the leading world exporter of crude olive pomace oil, which is mostly exported to Italy and Spain for further refining.

Most olive oil production in Greece is concentrated in Peloponnese (Messenia and Ilia), Crete (Iraklion and Chania), Mitilíni and on the Ionian Islands (Corfu).

In 2024/2025, Italy exported 157,403 tonnes of olive oil to Europe, valued at €1.35 billion. Italian domestic production is not sufficient for exports, so the country imports more olive oil than it exports. More than 72% of Italian olive exports is EVOO.

Italian production is concentrated in the south, with Puglia as the leading producing area, followed by Calabria and Sicily. The most common variety is Coratina (especially in Puglia).

Portuguese exports of olive oil to Europe increased by 13% in volume annually over the past 5 years to 215,225 tonnes in 2024. In value, these exports increased by 39% annually to €1.12 billion in 2024. Portugal shows continuous olive oil export growth. Around 66% of Portuguese olive oil exports is EVOO, followed by refined and blended olive oil (12%).

Source: Autentika Global, ITC, Eurostat, 2025

Tunisia: The leading exporter of organic olive oil to Europe

Tunisia is the second-largest olive oil producing country outside of Europe. In the 2024/2025 season, Tunisian olive oil production was estimated at 340,000 tonnes. Tunisia is a major exporter of organic olive oil. The country exported 48,900 tonnes of organic olive oil in the first 10 months of the 2024/2025 season, which started in November 2024. Europe is Tunisia’s main export target for olive oil, accounting for around 57% of total exports, with Italy being the largest importer.

Tunisia exported 152,086 tonnes of olive oil to Europe in 2024, valued at €825 million. Export volumes to Europe increased by 6% per year, while export values increased by 33% per year between 2020 and 2024. More than 64% of Tunisia’s olive oil exports consist of virgin olive oil, while 19% of exports are EVOO. Most of the olive oil is exported as bulk.

In 2024, Spain was the largest importer of Tunisian olive oil in Europe, with 94,952 tonnes, followed by Italy (47,649 tonnes). The European Commission publishes Tunisian olive oil quotas.

The spike in Tunisian exports in 2021 is linked to EU import rules and US tariffs. Tunisia has a 56,700-tonne duty-free quota. After this is used up, EU operators can still import Tunisian olive oil in bulk under the Inward Processing Regime (IPR). This avoids entry tariffs as long as the oil is re-exported after bottling or further processing.

The US imposed a 25% tariff on bottled Spanish olive oil from October 2019 in the Airbus dispute, which caused exports of Spanish olive oil to the US to drop sharply. To keep their brands in the US market, Spanish companies began importing more oil from Tunisia and bottling it in Spain before re-exporting it.

Morocco: Supplier of processors in Europe

Morocco is the fourth-largest olive oil producing country outside Europe, after Türkiye, Tunisia and Syria. In 2024, Morocco exported 11,540 tonnes of olive oil to Europe at a value of €42 million. A 44% share of Morocco’s exported olive oil in 2024 was crude pomace olive oil, followed by EVOO (40%).

In 2024, the leading export destination for Moroccan olive oil was Spain (69%), followed by the United States (21%).

The leading olive variety in Morocco is Picholine Marocaine, used in more than 96% of the country’s olive oil production.

Türkiye: The fastest growing supplier to Europe

Türkiye is the largest olive oil producing country outside of Europe. In 2024/2025, Turkish olive oil production was estimated at 450,000 tonnes.

Türkiye exported 30,587 tonnes worth €184 million to Europe in 2024. Export volumes to Europe increased by 39% per year between 2020 and 2024, while export values increased by 85% per year. More than 36% of Türkiye’s global olive oil exports consist of EVOO olive oil, while 26% are virgin olive oil.

The export increase was fuelled by a record-breaking table olive and olive oil harvest in 2024/2025. Turkish olive oil exporters are making inroads in the US market. The Aegean Olive and Olive Oil Exports’ Association (EZZIB) represents the interests of the country’s olive oil industry.

The US is the largest importer of Turkish olive with a 31% share (35,136 tonnes), followed by Spain with 17,259 tonnes and Italy with 8,580 tonnes.

Which companies are you competing with?

Many olive growers, grower cooperatives, olive oil mills, refineries, blending and bottling companies supply European markets, each of them with their own export strategies. The number of small farmers and oil mills is decreasing while large-scale production and processing is increasing. An estimated 50% of olive oil retail sales in the world is bottled by only 5 or 6 large companies.

European companies

Spain’s autonomous community Andalusia has the largest number of olive oil processors, and the largest olive mills in terms of capacity, some of which can process 2,500 tonnes per month. Most Spanish mills use two-phase decanter centrifuges and do not operate independently, but are related to packing facilities.

Despite the large number of olive mills, up to 50% of Spain’s producing cooperatives belong to large cooperatives that gather operations such as growing, processing, packing and exporting. Some of the largest Spanish olive oil cooperatives are Dcoop, Jaencoop, Almazaras de la Subbética, Oleoestepa, Interoleo, Oleotoledo, and Montes Norte. The largest individual olive oil processor in Spain, and in the world, is La Cooperativa Nuestra Señora del Pilar with 14 production lines (member of Jaencoop).

Other larger individual processors in Spain include Nuestra Señora de los Remedios, San Isidro de Loja, Fertinez and Bravoleum. The largest olive oil bottling and blending companies in Spain are Deoleo, Sovena, Migasa, Acesur, Borges and Maeva.

The following two stand out:

- Dcoop: The largest olive oil producer in the world, Dcoop currently produces approximately 7% of the world’s olive oil, and exports to almost 70 countries;

- Deoleo: The world’s largest olive oil bottler, with factories in Spain and Italy and subsidiaries in 15 other countries.

Italian production is characterised by the presence of a larger number of small-scale olive mills. Approximately 17% of Italy’s olive mills are in Puglia, 17% are in Calabria and 14% are in Sicily. Most of these olive mils belong to individuals and only roughly 20% of them are operated by cooperatives, mostly in Puglia and Toscana.

Large bulk olive oil producers, storage companies and refining companies in Italy include Castel del Chianti, Oleificio Zucchi, Valpesana, Casa Olearia Italiana, Fiorentini Firenze and Montalbano Agricola Alimentare Toscana.

Several large Italian bottling companies also own oil mills, such as Salov (Filippo Berio and Sagra brands), Monini, Fratelli Carli (Olio Carli), Olio Dante (Dante), de Cecco, Farchioni, Pietro Coricelli, Olitalia, Basso, Desantis and Rubino.

Notable Greek producers, traders and exporters include Terra Creta, Nutria, Olicobrokers, and ABEA. Many small mills produce PDO olive oils. Approximately 90% of Greece’s olive oil exports are in bulk and 10% under branded names of many different companies.

The leading exporters are Nutria, Gaea, Minerva and Upfield.

The largest Portuguese independent player is SOVENA group owned by Nutrinveste. It owns brands such as Andorinha, Olivari, Fontoliva, Soleada and Flor de Olivo. SOVENA organises production through their company Oliveira da Serra, on more than 10,000 ha.

Tunisia

A large share of processing in Tunisia is still done by traditional presses and mills. The largest number of mills is located in Sfax and Sahel. There are more than 40 olive oil packing facilities in Tunisia.

Notable export-oriented companies include CHO Group, Sadira, Huilerie Loued, Sarra Huiles, Barhoumi, and Fermes Ali Sfar.

CHO Group controls 20% of Tunisia’s production and has subsidiaries in several countries. The company is an exporter of bulk olive oil and organic olive oil but also produces the brand Terra Delyssa. It has subsidiaries in Europe and the United States.

Morocco

A leading olive oil producer is Lesieur Cristal, but there are many olive oil producers and exporters in Morocco. A leading company is Atlas Olive Oils, which cultivates more than 1 million olive trees on 3 estates at the foot of the Atlas mountains. Two of their premium brands — Les Terroirs de Marrakech and Desert Miracle — have won awards in international competitions. Lesieur Cristal is part of France’s Avril Group. It produces olive oil under its leading brands Jawhara and Mabrouka.

Türkiye

Notable Turkish olive oil exporters include Verde Yağ (owned by TRK Group) and one of Türkiye’s largest edible-oil groups, Savola Gıda Türkiye, with its Yudum, Egemden and Komili brands. Kristal Yağları is one of Türkiye’s oldest bottlers and the company is now expanding its branded olive oil exports from İzmir to Europe. Poyraz Zeytinyağı is also positioning itself as a value-added, branded olive exporter.

Tips:

- To learn more about the Spanish olive oil industry, consult the Spanish Olive Oil Interprofessional, Spanish Olive Oil & Pomace Olive Oil Exporters Association (ASOLIVA), Spanish Federation of Industrial Producers of Olive Oil (Infaoliva) and National Association of Industrial Packagers and Refiners of Edible Oils (ANEIRAC).

- Learn more about the Italian olive oil industry from the Association of Italian olive oil producers (ASSITOL), Italian Olive Consortium (UNAPROL) and Institute for Agricultural Market Services (ISMEA).

- Visit leading European trade fairs, such as Anuga, SIAL and BIOFACH (for organic) to meet potential clients and see what the competition is doing.

Which products are you competing with?

The main substitutes for olive oil are other vegetable oils and butter. The most produced oil in Europe is rapeseed oil, followed by sunflower and soybean oil. Sunflower oil is also the most imported type of vegetable oil in Europe.

Olive oil is considered a high-value product. It is important to offer high-quality olive oil to final consumers.

Argan oil, avocado oil, jojoba oil and macadamia oil also belong in the premium segment, but they are used more as cosmetic ingredients.

Tip:

- Visit the websites of the Federation of European Vegetable Oils Industry (FEDIOL) and the European Association of Dairy Trade (Eucolait) to better understand the competition to your product.

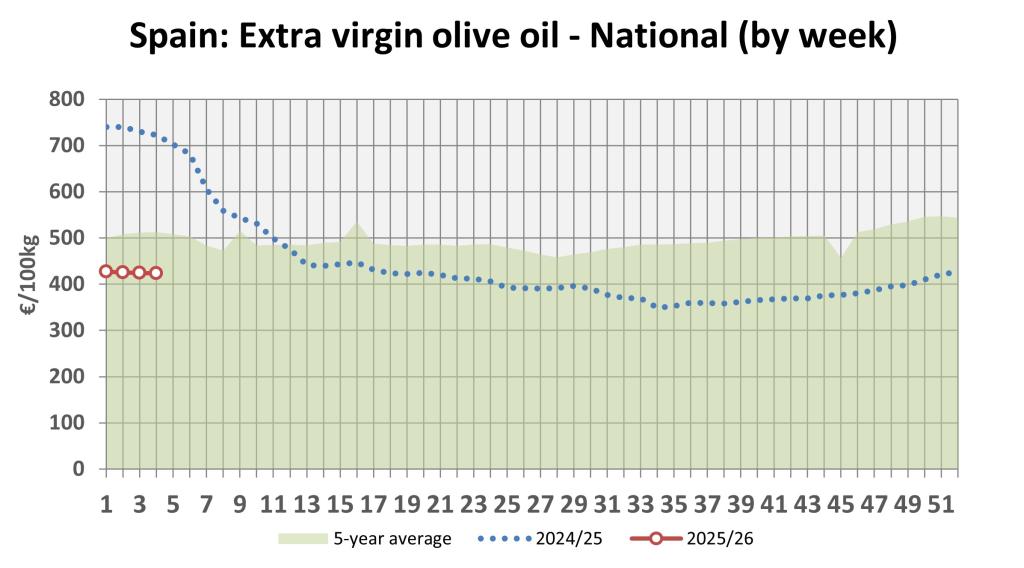

4. What are the prices for olive oil on the European market?

Prices of olive oil vary according to the type of olive oil. The cheapest olive oils are lampante and olive pomace oil, and the most expensive are EVOO premium oils. Bottled olive oils reach the highest export prices. But most of the European trade consists of bulk olive oil.

Italian olive oil is sold for far higher prices than Spanish, Portuguese and Greek oils.

In mid-2025, producer prices for EVOO were very different by country. Prices in Spain fell to about €3.9/kg in August. Italy stayed near €9.7/kg. Protected Designation of Origin (PDO) olive oil prices are higher. Brisighella PDO was about €19/kg and Bruzio PDO was €9.70/kg in September 2025. In final retail sales, a litre of Brisighella oil can sell for €40-50.

Figure 5: Average weekly prices of EVOO from Spain:

Source: Autentika Global, European Commission, 2025

The price breakdown below is a rough indication, as many different factors affect production costs.

Table 1: Olive oil retail price breakdown

| Export process steps | Type of price | Price breakdown | EVOO price per litre (example) |

|---|---|---|---|

| Production of olives | Raw material price | 5%–6% | €0.66/kg for olives, based on the assumption that the price of 100 kg of olives is €120 and that producing 1L of oil requires 5 kg of olives. |

| Crushing and production of bulk oil | FOB or EXW price | 50% | €6 |

| Import, shipping, handling and storing | CIF price | 58% | €7 |

| Bottling | Wholesale price (value-added tax included) | 60%-70% | €8 |

| Retail sales of the final packed product | Retail price | 100% | €12 |

Source: Autentika Global, 2025

Tip:

- Check prices in the leading producing countries on the websites of Precio Aceite de Oliva, ISMEA, Certified Origins and the IOC.

Autentika Global carried out this study on behalf of CBI.

Please review our market information disclaimer.

Search

Enter search terms to find market research