What is the demand for natural ingredients for health products on the European market?

Europe is one of the most promising markets for natural ingredients for health and wellness products. Consumers are choosing plant-based and alternative therapies more and more to support preventive health and overall wellbeing. Europe’s strong manufacturing foundation drives innovation in bioactive formulations and extraction technoalogy.

Demand for botanical extracts, essential oils, seaweeds, algae, turmeric and ginger continues. This reflects traditional use and scientific validation. Germany, France, Italy and the United Kingdom offer the most opportunities for exporters from developing countries. They have established self-medication cultures and large consumer markets that prefer high-quality, traceable and sustainably-sourced natural ingredients.

Contents of this page

- Sector description: Natural ingredients for health products

- What makes Europe an interesting market for natural ingredients for health products?

- Which European markets offer most opportunities for natural ingredients for health products?

- Which products from developing countries have most potential on the European market?

1. Sector description: Natural ingredients for health products

‘Health products’ refers to food supplements and herbal medicinal products. The natural ingredients that have the most potential on the European health products market are:

- Medicinal and Aromatic Plants (MAPs)

- Essential oils

- Botanical extracts

- Seaweeds and algae (spirulina and chlorella)

- Turmeric

- Ginger

Table 1: Descriptions of interesting natural ingredients for health products on the European market

| Product | Harmonised System code (used in international trade data) | Description |

|---|---|---|

| Medicinal and Aromatic plants (MAPs) | HS code 121190 | Medicinal and Aromatic Plants (MAPs) are botanical raw materials that are used in health products and cosmetic products, mostly for therapeutic and aromatic purposes. This product group excludes ginseng root, coca leaf, poppy straw and ephedra. Examples include rosemary and hibiscus. |

| Essential oils | HS code 330129 | Essential oils are extracted from plants through steam or water distillation. HS code 330129 refers to ‘other essential oils’ and excludes citrus fruit and mint oils. Essential oils traded under HS code 330129 include patchouli, frankincense and ylang-ylang. |

| Botanical extracts | HS code 130219 | Botanical extracts are derived from MAPs, herbs or spices using a solvent. The original components of the plants are not changed generally, although botanical extracts have higher concentrations of actives or nutrients. HS code 130219 excludes liquorice, hops and opium. Botanical extracts include aloe vera extract and ginseng extracts. |

| Seaweeds and other algae fit for human consumption | HS code 121221 | Seaweed refers to a number of species of macroscopic, multicellular and marine algae that grow along rocky shorelines around the world. Seaweed varies in colour from red to black. Most edible seaweed is marine seaweed, which is part of many coastal cuisines. |

| Turmeric | HS code 091030 | Turmeric (Curcuma longa) is a species of the Curcuma genus from the family of Zingiberaceae (commonly known as the ginger family of flowering plants). The active substance of turmeric, curcumin, has multiple therapeutic properties such as anti-inflammatory, antioxidant and cancer prevention. |

| Ginger | HS code 091012 (crushed ginger) | Ginger is the irregularly shaped root (rhizome) of the ginger plant (Zingiber officinale). The plant is cultivated in the tropics. Ginger is used as a spice in food and also in food supplements and herbal medicinal products. |

2. What makes Europe an interesting market for natural ingredients for health products?

Europe produces, imports and consumes a large amount of health products. It is an important market for food supplements and herbal medicinal products. The market is predicted to grow alongside consumer interest in natural health. Sustainable sourcing is becoming more and more important on the European market as part of its ever-developing requirements.

Strong and growing European demand for health products

In terms of health products, natural ingredients are mainly used in food supplements and herbal medicinal products (alternative medicine). There is only limited data on the total market size of these segments. However, available market research predicts that alternative medicine will rise in popularity in Europe and so will demand. This means opportunities for exporters of ingredients.

Food supplements

In 2024, the European market for food supplements was valued at $46 billion (USD). It is projected to reach $93.2 billion by 2033 at an annual growth rate of 8.3%. Europe is expected to become the third largest market for food supplements, after Asia-Pacific and North America.

The Food Supplements Europe sector association states that almost 9 out of 10 respondents to a 2022 study had used a food supplement at some point in their lives. 52% of respondents took supplements to maintain their overall health within the year of the study. The fastest growing product category is sports nutrition. Growth is fuelled by plant-based proteins, followed by gut health (probiotics/microbiome) and collagen/skin health (beauty-from-within).

Herbal medicine

Data on the market for herbal medicinal products is limited. Available market research also often uses different definitions for this sector, which sometimes includes herbal food supplements or cosmetic products. Globe Newswire predicts that the European herbal medicine market will reach $113 billion by 2030 and grow at a steep annual rate of 24.8% from $30 billion in 2024. It is expected to become the largest market for herbal medicine in the world, followed by Asia-Pacific. The growth of Ayurveda represents the fastest-growing segment.

Complementary and Alternative Medicine (CAM)

Europe is the largest market for complementary and alternative medicine. It had an estimated value of $59 billion in 2024. The European CAM market is expected to grow at an annual rate of almost 21% from 2025 to 2030, reaching $189 billion in 2030.

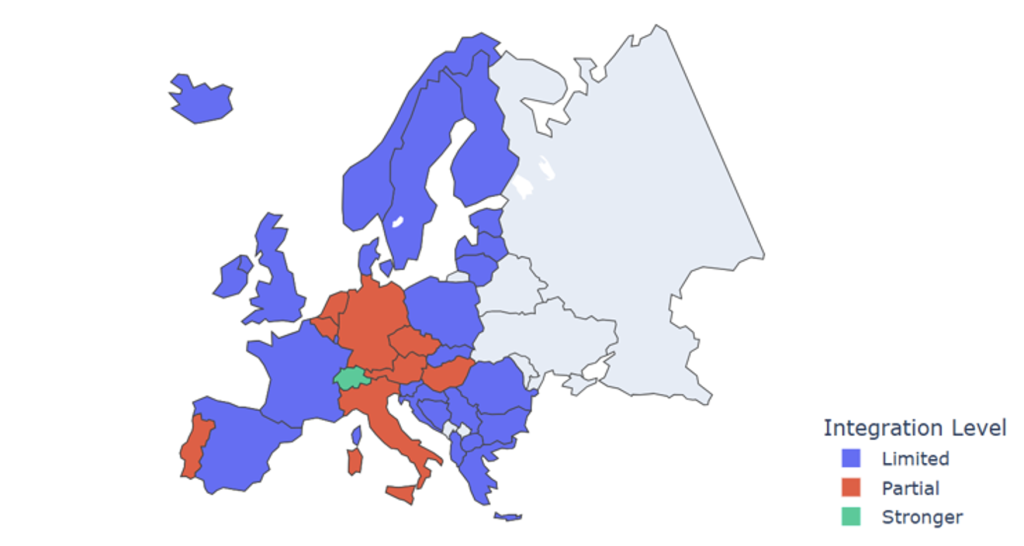

Studies have shown that CAM treatments are most popular in Germany and Switzerland. This is partly because some CAM treatments are covered by health insurance. Other reasons for the higher demand for CAM therapies include the long history of using CAM therapies in these countries, as well as positive attitudes that favour natural and holistic approaches to health. The United Kingdom is also an important CAM market.

Figure 1: Complementary and Alternative Medicine (CAM) integration in Europe

Source: ProFound, from various sources, 2025

Growing investment in innovation and R&D has made Europe an interesting market for suppliers of natural ingredients for health products.

The European herbal medicine and CAM industry are investing in new product development, extraction technologies and research into medicinal plants. Countries like Germany (Schaper & Brümmer and Dronania), the Netherlands (NutriLeads/Benicaros) and Sweden (New Nordic and Apoteum) are home to innovative health product companies.

In the coming years, the number of applications of natural ingredients in health-products is expected to grow. This growth is both through new delivery formats (like gummies) and novel bio-active extraction, formulation technologies and ingredient sourcing (for example, upcycled ingredients like fruit and vegetable pomace).

Growing European imports of natural ingredients

To meet demand from its industry and growing consumer base, Europe imports large volumes of natural ingredients. The Europe’s 2024 imports relative to global imports were as follows:

- MAPs: Europe accounted for 37% of global import value, valued at nearly €1.5 billion in 2024;

- Essential oils: Europe represented 43% of the global import value at €2.5 billion in 2024;

- Botanical extracts: Europe represented 34% of global import value, reaching €1.2 billion in 2024;

- Seaweeds: Europe accounted for 9.3% of global import value at €101 million in 2024;

- Turmeric: Europe represented 17% of global import value at €81 million in 2024;

- Ginger: Europe represented 35% of global import value at €488 million in 2024.

Total European import volumes of many natural ingredients for health products have increased over the last five years (see Figure 2). Developing countries play a large role in the supply of various ingredients, including:

- Medicinal and Aromatic Plants (49% of total European imports in 2024)

- Essential oils (51%)

- Ground ginger (66%)

- Turmeric (73%)

The Netherlands and Germany are major trade hubs from where many ingredients are distributed to other European countries.

Source: ITC Trademap (2025)

Emerging market economies are important suppliers to Europe

Emerging markets play a large role in the supply of various ingredients to Europe. This includes:

- MAPs: Europe sourced 48% of the import value from emerging markets in 2024, up from 44% in 2020. The largest emerging market suppliers to Europe were India, China, Egypt, Morocco and Kenya.

- Essential oils: About 51% of the import value came from emerging markets in 2024, up from 45% in 2020. Brazil, India, China and Indonesia were major emerging market suppliers.

- Botanical extracts: Imports from emerging markets reached 44% of the total import value in 2024. This is a notable increase from 34% in 2020. Major emerging market suppliers to Europe include China, India, Vietnam, Madagascar and Mexico.

- Seaweeds: About 51% of the import value was sourced from emerging markets in 2024, a huge jump from 35% in 2020. The largest emerging market suppliers to Europe were China, South Korea, Chile, Tanzania and Taiwan.

- Turmeric: About 73% of the import value was sourced directly from emerging markets. This share had been stable since 2020. The largest emerging market suppliers to Europe were India, Peru, Madagascar, Vietnam and China.

- Ginger: 80% of the import value came from emerging markets in 2024, an increase from 76% in 2020. Major emerging market suppliers were China, Brazil, Peru, Thailand and Nigeria.

Consumer interest in natural health options expected to grow further

For the past few years, interest in natural health products has grown in Europe. More people want to be healthier before problems appear. This has made herbal supplements, plant extracts and vitamins more popular. The Covid-19 pandemic made people more aware of their health, and this interest has continued after its end.

A 2025 scientific review confirms that more Europeans are choosing natural products to support immunity, gut health, stress relief and overall well-being. This is a lifestyle shift, not just a pandemic trend. A 2024 European study shows that people now focus more on staying healthy and avoiding illness, rather than only treating sickness. This creates more demand for natural ingredients for supplements, herbal medicines and functional foods.

Globally, more than 50% of consumers look for products with botanicals they believe will improve their immune, gut and mental health.

This is also clear when looking at other market statistics. According to Verified Market Research, the Europe vegan supplements market was valued at $2.2 billion (USD) in 2024. It is projected to reach $4.68 billion by 2032.

Recent market reports estimate that the global plant-based supplements market (covering vitamins, botanicals, plant-derived nutrients) was valued at around $11.5 billion in 2025. It is predicted to grow to $16 billion by 2032. According to a global study conducted by Mintel, the five most innovative countries for plant-based food are in Europe the UK (24% of new vegan food launches), Portugal (21.5%), the Netherlands (19.1%), Germany (18.7%) and Austria (16.9%).

Sustainable sourcing important in natural ingredients for health products

The increased adoption of healthier lifestyles boosts the sales of natural and clean label health products. Natural and organic health products are seen as safer and higher quality. A survey on behalf of Food Supplements Europe showed that 56% of respondents consider the organic, natural or non-GMO labelling to be important when purchasing supplements.

At the same time, demand for organic products is growing. The European organic food market was valued at approximately $57.48 billion (USD) (approximately €53 billion) in 2024. It is expected to grow by a lot in the coming years, with projections reaching $132.2 billion by 2033. Buyers have stated that there is almost no market for non-organic certified natural health ingredients, such as moringa and baobab.

The share of organic in the whole natural ingredients for health products market is expected to stay small. However, there are no specific statistics that confirm this. Organic certification is more common for food supplements than for herbal medicinal products, which cannot be labelled as an organic finished product. There are more opportunities for certification if a food supplement is positioned more as a food-type product, rather than as a medicinal-type product. Buyers use organic certification as a sign of quality and traceability.

Demand for sustainably-sourced ingredients is growing amongst both European consumers and buyers. Consumers are becoming more concerned about sustainability and ethical production. They want to know where their products come from. European buyers are also becoming more involved in sustainably managing resources to ensure future availability.

Many health products contain wild-harvested medicinal and aromatic plants that are at risk of overharvesting or in danger of extinction. Good practices and responsible sourcing that follow standards, such as FairWild, are essential for securing the future supply of natural ingredients for health products.

European buyers of natural ingredients for health products also struggle with a lack of quality and safety control in countries of origin. Adulteration and heavy metal contamination of medicinal plants are major issues that present serious health risks for consumers. Buyers more often demand that exporters have quality and food safety management systems in place.

Tips:

- Explore the food supplement market. In Europe, natural ingredients are used much more in the supplements sector and the complementary and alternative medicine (CAM) sector than in generic medicine, which mainly uses synthetic ingredients.

- Tell buyers how your ingredients can help consumers improve their health and wellbeing. Focus on the nutritional and health aspects of your ingredients if you supply active ingredients. Do not make medical claims. You can find more information on EU regulations regarding claims on the European Commission’s website.

- See the CBI study on buyer requirements for natural ingredients for health products for an overview of the regulations for exporting natural ingredients for health products to Europe, as well as organic certification.

- Read the CBI study on which trends offer opportunities or pose threats in the European natural ingredients for health product markets. This study provides useful information about the European health products market and information likely to increase your chances of market access.

- See the CBI studies on moringa, baobab, essential oils and turmeric for more information on the European market potential of these products.

3. Which European markets offer most opportunities for natural ingredients for health products?

Germany, France, Italy, the UK, Spain and the Netherlands are the most attractive country markets for suppliers of natural ingredients for health products.

These countries have different characteristics that make them interesting. For example, the Netherlands is an important entry point for natural ingredients. It has a high concentration of ingredient importers and distributors. The Netherlands also has robust logistics capabilities thanks to the Port of Rotterdam. These two factors are the main reasons for The Netherlands playing an important role in re-exports within Europe

Figure 3 below shows leading importers per product group included in this study.

Source: ITC Trademap (2025)

These countries have the largest processing sectors and consumer markets. Large health product manufacturers that use natural ingredients are also located there. Some of the largest producers of supplements are located in Western Europe. Table 2 provides an overview of characteristics on these main markets.

Table 2: Characteristics of leading European markets for natural ingredients for health products

| Production | Processing | Trade | Herbal medicinal products market | Food supplement market | |

|---|---|---|---|---|---|

| Germany | Large EU producer of Medicinal and Aromatic Plants (MAPs) | Largest extraction industry | Largest importer in all categories, highest share imports from developing countries | Largest market EU, also interest in aromatherapy | Large market |

| Italy | Large EU producer of MAPs | Strong extraction industry | Large importer MAPs/extracts | Medium-sized market | Largest market EU: limited herbal |

| France | Large EU producer of MAPs (use in cosmetics) | Strong extraction industry | Large importer MAPs/extracts/ | Large market EU, also interest in aromatherapy | Large market |

| UK | Small EU producer of MAPs | Strong trader in MAPs/extracts | Mid-sized market, relatively large in Ayuverda/TCM | Large market, focus on multi-herb products | |

| The Netherlands | Limited production of MAPs | Limited extraction industry | Important trade hub for natural ingredients, large share of imports from developing countries | Medium-sized market | Medium-sized market |

| Spain | Large EU producer of MAPs | Strong extraction industry | Important and growing importer of MAPs for processing industry | Medium-sized market | Small but fast-growing market |

Source: ProFound, 2025

Germany at the centre of herbal medicinal products in Europe

Germany is home to the largest consumer market in Europe and consumers are more and more health conscious. There is also growing consumer interest in plant-based products and a strong extraction industry. Because of this, the German market offers opportunities for exporters of natural ingredients for health products.

Germany is one of Europe’s largest food supplement markets, alongside Italy. The German nutritional supplements market was worth approximately $12 billion (USD) in 2024. Solid growth expected to continue until 2030. Pharmacies are still the main sales channel, but online and mail-order sales are expanding quickly.

According to consumer surveys, supplement use in Germany is rising steadily. A 2025 Pharmazeutische Zeitung article reported that 54% of consumers purchased supplements in the previous six months. A 2025 Springer Medizin review estimated that around two-thirds of adults in Germany use food supplement regularly, depending on sample and definition. This trend is expected to continue in the coming years as German consumers become more aware of these products’ benefits.

Of the food supplements consumed, herbs or herbal products make up approximately 20% of overall consumption. Herbal supplements like algae make up around 10%. Still, minerals and vitamins are particularly popular among German consumers. They make up slightly less than half of the country’s food supplements market.

Germany has a long tradition of herbal medicinal products. This is shown in the German pharmaceutical market, especially in self-medication products. The ABDA Zahlen, Daten, Fakten 2024 report shows that self-medication (non-prescription) in German pharmacies sold 483 million packages in 2023, up from 435 million in 2021.

The cultivation of MAPs has a long tradition in Germany, especially in the East. Several German MAP producers are competitive on the market, particularly when it comes to to ingredients for herbal medicinal products. This is thanks to the high quality and excellent documentation they provide. MAP producers in Germany include Pharmaplant and HEGO Heilkräuter Gorges GmbH & Co.KG.

There is strong domestic demand for raw materials and processed ingredients for industrial use to supply health products. In terms of trade, Germany dominates imports of several natural ingredients for health products, such as MAPs. These raw materials are used in Germany’s extensive processing and manufacturing industry. German importers include MartinBauer and Worlée.

France focuses on herbal health products

France is an attractive market for exporters of natural ingredients for health products. It is a large and growing consumer market where consumers value plant-based food supplements. Traditionally, French consumers rely on prescription medicines and food supplements. As a result, France is one of the largest markets for food supplements in Europe.

In 2024, the French food-supplement market generated approximately €2.9 billion, up about 5.7% year-on-year since 2018. Around 61% of French adults were estimated to have consumed a supplement between early 2022 and early 2024, compared to 59% in 2023. Around 77% of supplement users take them several times a year. Online distribution channels are seen as the main reason for this market growth. But pharmacies are still the dominant channel, making up 55% of sales.

Around 72% of French respondents in the Synadiet Observatoire 2024 survey believed food supplements to be effective. The most popular reasons for taking food supplements were to:

- Reinforce their immune system (48%);

- Stay in shape/support overall wellbeing (44%);

- Improve sleep (36%);

- Manage stress (31%).

Traditional Western herbal medicinal products dominate the French herbal medicinal product market, especially homeopathic medicines. These products focus mainly on preventive health. France is one of the largest markets for herbal medicinal products in Europe, surpassed only by Germany. The French herbal medicinal product market (OTC herbal medicines) was valued at about $4.83 billion (USD) in 2023 and is predicted to reach $23.84 billion by 2030.

France produces a large amount of MAPs, mostly for the essential oil and cosmetics industries. It is also the largest EU importer of essential oils (see Figure 2). The production of MAPs relies on strong domestic demand and large MAP valorisation., The number of producers is growing and the cultivation area is being expanded. But according to Synadiet, demand is still higher than what can be supplied agriculturally. France has a large extraction sector that supplies the herbal medicinal product, food supplement and cosmetics sectors.

French manufacturers produce high-quality consumer products at competitive prices. These are supported by documentation and market communication. Emphasis on quality ensures consumer satisfaction and trust in the products. Customer advice plays an important role in pharmacies and para-pharmacies. Para-pharmacies are retail stores that specialise in selling non-prescription or over-the-counter healthcare products.

French health product manufacturers include Laboratoires Boiron, Arkopharma and Phytea. Importers include Elementa Ingredients and Pharmanager Ingredients.

Italy is the number one food supplement market in Europe

Italy is an attractive market for exporters in developing countries. It is the largest importer of botanical extracts in Europe. They have a thriving natural health product manufacturing industry. Consumers also have a long history of using locally produced botanicals for herbal medicinal products and traditional medicine.

Italy is the largest food supplement market in Europe. Its dietary supplements market was valued at approximately $7.8 billion (USD) (€7.1 billion) in 2024. This value is predicted to reach $11.6 billion by 2030 at an annual growth rate of 7%. Pharmacies are the main distribution channel. They sell around 80% of food supplements.

According to Ipsos market research, Italian consumers use food supplements to feel fitter (87%) and because they want to take care of their bodies (84%). A study by the IRI reported that 80% of Italians took dietary and nutritional supplements in 2023.

The Italian herbal sector is stable and growing due to Italy’s strong pharmacy channel and botanical heritage. According to a report by the Italian Federation of Herbal Medicine Industries, the Italian herbal product market was valued at €2.9 billion in 2022 (latest figure available). This is around 11% of the country’s total pharmaceutical market.

However, this figure includes both herbal medicinal products and supplements. Products with natural active ingredients are used, especially for mild health issues. Popular ingredients include:

- Passionflower;

- Lemon balm;

- Propolis;

- Fermented red rice yeast;

- Arnica;

- Aloe;

- Calendula.

Italy is a large producer of medicinal and aromatic plants. The country relies less on imports of natural ingredients for health products from non-European countries than other main European countries. However, it still presents opportunities for raw materials grown in tropical climates.

Examples of Italian manufacturers of health products include Dr Taffi, Boiron and Naturando. Importers of ingredients include Carlo Sessa and Minardi.

The UK increasingly imports natural ingredients directly from developing countries

The UK is a growing market with high demand for plant-based products that support general health. It depends on imports of natural ingredients, because local production is limited. This leads to additional opportunities for you.

The UK dietary supplement market was valued around $4.15 billion (USD) in 2024. It is projected to grow to $6.52 billion by 2030. Early pandemic-related analyses showed a surge. For example, the Health Food Manufacturers’ Association reported approximately 20 million daily supplement users in 2020. However, more recent publicly-available data highlight sustained growth rather than the sharp spikes of the pandemic. Important drivers for taking food supplements include general health and wellness (60.7% of UK consumers) and to optimise health (20.4%).

UK consumers increasingly look for natural and clean products. This trend is reflected in other sectors, such as the cosmetics industry. The UK herbal supplement market generated $926 million in 2024, and is projected to reach about $2.2 billion by 2033, with an average annual growth rate of 10% from 2025 to 2033.

The UK has a strong herbal medicinal product sector. Traditional Chinese Medicine (TCM) and Ayurvedic medicine hold relatively strong positions compared to other European countries. This offers opportunities for ingredients used in these medicine practices. Aromatherapy is also popular in the UK. It is used for relaxation and preventative care rather than as a form of medication. Brands with large portfolios of aromatherapy products (essential oils) include Oshadhi and doTERRA. With limited local production, the UK relies on imports (see Figure 3).

The UK is expected to remain an important market in Europe for natural ingredients for health products in the coming years. There are a few major players that supply MAPs and/or saps and extracts to the UK market. One of these players is Organic Herb Trading Company, a member of the British Herbal Medicine Association. Another one is the Herbal Apothecary, which supplies several herbs and extracts and makes products like tinctures and capsules.

Total UK imports of botanical extracts and MAPs increased during the 2020–2024 period. This includes imports from developing countries. Similar developments can be seen for ginger and turmeric, where the UK sources them directly from developing countries more often.

The UK’s extraction industry is well developed, but a lot smaller than France, Italy and Germany. It mostly consists of small extraction companies. The UK also includes processors that import extracts from developing countries to complement their own product range. These imported extracts are sometimes reprocessed, but they can also be sold to manufacturers directly.

Spain’s gaining importance with growing supplements consumption and strong processing industry

Spain is a large processor of extracts. It imports large quantities of MAPs (see Figure 2). Their food supplement and herbal medicinal product markets are relatively small compared to other countries. But its continuous growth and growing focus on preventative health treatments offer opportunities.

The Spanish dietary supplements market generated approximately $2.4 billion (USD) (€2.2 billion) in 2024. It is expected to reach about $3,923 million by 2030, representing an annual growth of around 8.5% from 2025 to 2030.

Around 75% of Spanish consumers take nutritional supplements. This is comparable to the consumption levels of European countries with longer traditions of food supplement consumption. According to the Spanish Academy of Nutrition, consumers take supplements to improve their general health, to improve the functioning of the immune system and to have more energy. Around 29% of Spanish consumers take plant extracts, such as fibre, pollen and royal jelly.

Spain is an important European producer and processor of MAPs, serving local and international demand. Although there are several large players, the sector is fragmented and includes many SMEs that focus on processing domestic MAPs.

Spain’s extraction and natural health product industry is growing, with new companies entering the food supplements market. This leads to a diverse product portfolio and opportunities for developing country suppliers of natural ingredients. One example of a Spanish raw material distributor of food supplements is Nutrifoods. Another is Nutris, which formulates food supplements.

The Netherlands as a trade hub for natural ingredients in Europe

The Dutch market for herbal medicinal products and food supplements is smaller than other leading markets. But the Netherlands is a trade hub (see Figure 2). This creates opportunities for exporters from developing countries. The Netherlands depends on imports because local production is limited.

The Dutch food supplements market reached €860 million in 2024, up from €775 million in 2023 (+11%). About 72% of Dutch adults (17 years and older) report using supplements to support their health. Online purchases are rising: in 2024, 38% of users bought supplements online compared to 19% in 2019.

Dutch consumers mainly use supplements for prevention. Around 42% of Dutch consumers take supplements to improve their overall health. 33% of Dutch consumers use supplements to improve their immune systems.

The Netherlands is an important entry point for a range of natural ingredients from developing countries. Its botanical extract and ginger imports in 2024 were almost exclusively from developing countries. The Netherlands also mainly imports turmeric from developing countries. Dutch seaweed imports have been following the general European trend, and growing quickly in the last five years as well.

The Netherlands’ role as an entry point for ingredients into Europe is thanks to its role as a re-exporter to other European countries, strong ingredient-processing industry and the presence of importers and distributors that cover multiple countries.

The Netherlands combines technology with know-how in the processing and formulation of ingredients. This makes it an interesting destination for suppliers from developing countries. One example of a trading company present in the Netherlands is Caldic. It is active in the food, pharmaceutical, personal care and industrial formulation markets.

Other companies active in the import of MAPs and botanical extracts for the health market are Health Ingredients Trading and VNK Herbs.

Tips:

- Determine which market offers the best opportunities for your company and products. You can get market information from sector associations, online product portfolios of distributors and retailers, or by visiting trade fairs.

- Do market research. Review CBI market studies on the natural ingredients for health products sector and individual products or product groups. Alternatively, you can use online trade databases such as ITC Trademap and Access2Markets to download trade data for your product categories.

- See the CBI tips for finding buyers in the natural ingredients for health products sector. It provides practical guidance on finding buyers on the European market.

- Target health product companies in Western Europe. These countries are the largest consumers and producers of herbal medicinal products and food supplements. Consumers in these countries are also open to various types of complementary and alternative medicine.

4. Which products from developing countries have most potential on the European market?

European demand for natural ingredients for health and wellness products continues to rise. Consumers’ ongoing focus on preventive health, clean-label formulations and plant-based solutions are the main drivers for this. The Covid-19 pandemic sped up this shift, but the trend has proven permanent. Today, health-conscious consumers actively seek botanical and marine-derived ingredients that support immunity, digestion, stress relief and overall wellbeing.

Medicinal and Aromatic Plants (MAPs), essential oils, botanical extracts, seaweeds and algae products, turmeric, and ginger are popular natural ingredients on the European market. They have an important or growing role for developing country suppliers. The food supplement sector is trend-sensitive. This could present a risk that the popularity of some natural ingredients may not last. The herbal medicinal sector has stricter quality requirements. However, buyers in this sector are more likely to stay with the same supplier.

Medicinal and aromatic plants

Medicinal and Aromatic Plants (MAPs) are fundamental to Europe’s health, wellness and natural-product industries. Beyond their traditional use in herbal medicine, MAPs are important inputs for food supplements, cosmetics, aromatherapy products and natural flavourings. Globally, between 50,000 and 70,000 plant species are used in traditional medicinal practices, while about 2,000 are traded in meaningful quantities in the European Union.

In 2024, imports of MAPs into Europe reached a value of approximately €1.5 billion, up from about €1 billion in 2020. This represents a compound annual growth rate of 8.9% between 2020 and 2024. It clearly shows Europe’s continued shift toward natural and plant-based health solutions.

Developing countries are strengthening their position as Europe’s main MAP suppliers. In 2020, they accounted for 44% of the region’s total MAP import value. By 2024, this had risen to 48%, confirming their growing importance.

The largest developing-country suppliers are India, China, Egypt, Morocco, Kenya, Türkiye and Albania. Together, they represent most MAP imports from outside Europe. India and China lead in global botanical extraction capacity and export a wide range of species. Egypt, Morocco and Albania specialise in Mediterranean MAPs, such as chamomile (Matricaria chamomilla), thyme (Thymus vulgaris), rosemary (Rosmarinus officinalis) and sage (Salvia officinalis).

Within Europe, Germany is the largest importer of MAPs, followed by France, the United Kingdom, Italy and Spain. Together, these five countries accounted for over half of total European MAP import value in 2024. All five countries have strong extraction and processing industries. These serve both domestic and export markets for herbal medicinal products, food supplements and natural cosmetics. Germany, the Netherlands and France also act as major re-export hubs for MAPs and processed botanicals to other world regions.

Source: ITC Trademap (2025)

Most European demand is for the most commonly used MAPs, specifically those used in Western herbal medicinal products. However, there is some demand for less common species with interesting active properties that have technical documentation and a documented history of use. This demand mostly comes from the food supplements market. For example, spices used in food are re-evaluated for health properties (see the sections on turmeric and ginger).

The quality and microbial safety of MAPs is important to European buyers. At the same time, consumers are interested in organic certified health products that support healthy lifestyles, driving demand for organic MAPs.

Western European suppliers dominate the premium segment through documented sourcing and close buyer relationships. Eastern Meanwhile, European collectors are competitive in sustainably wild-harvested temperate species. Europe’s climate restricts the production of most tropical and subtropical plants. So there are always opportunities for developing-country exporters that offer consistent quality, organic certification and transparent traceability.

Historically, several issues affect the MAPs sector. One is the overharvesting of MAPs, which puts pressure on wild plant populations. This can lead to an increase in threatened plant species worldwide. Accurately identifying species and variation is also often a problem. Largely unregulated and non-transparent supply chains limit the growth of the MAPs sector.

Table 3: Important trade indicators for MAPS

| Indicator | 2020 | 2024 | Change 2020-2024 |

|---|---|---|---|

| Total imports of MAPs into Europe | €1 billion | €1.5 billion | +29% (14% CAGR) |

| Share from developing countries | 44% | 48% | +4% |

| Top European importers | Germany, France, Spain, Italy, United Kingdom | Germany, France, United Kingdom, Italy, Spain | - |

| Main developing-country suppliers | India, China, Morocco, Egypt, Türkiye, Albania, Kenya | India, China, Egypt, Morocco, Kenya, Türkiye, Albania | - |

Source: ITC Trademp (2025)

Tips:

- Show that you have a sustainable wild collection by conducting a resource assessment. See the CITES International standard for sustainable wild collection of medicinal and aromatic plants for more information. Use a resource management system based on the assessment’s outcomes. Document your processes to make sure your efforts can be translated to your price.

- See the European Union herbal monographs for more information on the properties and applications of medicinal and aromatic plants.

- See the CBI studies on various product categories and therapeutic areas: Ayurvedic Ingredients, Digestive Health, Immune-Boosting Botanicals and Stress and Anxiety Products for more information on MAPs and their potential.

- For more information on European herb production, take a look at the website of the European Herb Growers Association. Here you can also download the association’s Good Agricultural and Collection Practices aimed to improve quality and safety of MAPs.

Essential oils

Europe is the largest market for essential oils in the world. According to Grand View Research, the European market for essential oils is expected to reach a valuation of $27 billion (USD) by 2033, with an annual growth rate of 8.9% from 2025 to 2033. Food, beverages and cosmetics industries make up the largest share of essential oil demand. However, growing consumer interest and the awareness of aromatherapy is expected to drive demand for essential oils in the coming years too.

In Europe, essential oils for aromatherapy are often regulated as cosmetic products. Eucalyptus, tea tree, jasmine and ylang-ylang oil are popular in aromatherapy.

In 2024, imports of essential oils into Europe reached a total value of approximately €2.5 billion, up from about €1.9 billion in 2020. This represents a strong compound annual growth rate of 7.8% between 2020 and 2024. In 2020, developing countries accounted for 45% of the region’s total essential oil import value, having risen to 51% in 2024.

The top developing-country suppliers are Brazil, India, China, Indonesia, Argentina and Mexico. Together, they supplied 37% of total European essential oil imports in 2024.

Germany, France, Ireland, United Kingdom and Spain are the main European importers of essential oils. They have strong manufacturing industries, growing demand for relaxation therapies and play important roles in the import and re-export of essential oils. Note that essential oils are largely used in the cosmetic and fragrance industries, especially in France.

Source: ITC Trademap (2025)

Plants for essential oil production are grown in Europe, like rose and clary sage. Germany is the largest European producer of essential oils, followed by France. Other producers include Italy, Spain and Bulgaria. Suppliers in developing countries should focus on niche essential oils that cannot be grown in Europe, like frankincense and ylang-ylang.

Table 4: Important trade indicators for essential oils

| Indicator | 2020 | 2024 | Change 2020–2024 |

|---|---|---|---|

| Total imports of essential oils into Europe | €1.9 billion | €2.5 billion | +26% (7.8% CAGR) |

| Share from developing countries | 45% | 51% | +6% |

| Top European importers | Germany, France, United Kingdom, Ireland, Spain | Germany, France, Ireland, United Kingdom, Spain | - |

| Main developing-country suppliers | India, Argentina, China, Brazil, Indonesia, Mexico, Egypt | Brazil, India, China, Indonesia, Argentina, Mexico | - |

Source: ITC Trademp (2025)

Awareness of mental health is increasing and more people prefer natural alternative treatments to pharmaceutical drugs. These factors are expected to increase demand for aromatherapy products in Europe. Essential oils have a wide range of properties such as stress relief, anti-bacterial properties, soothing, refreshment and invigoration.

Essential oils for aromatherapy have a long tradition in China, India and Egypt. They are used for respiration, digestion, immunity and anti-oxidant purposes and to reduce stress. Aromatherapy is also used to complement treatment for psychiatric disorders and chronic diseases. However, there is limited scientific evidence for their therapeutical benefits.

Adulteration and safety concerns are common issues for the essential oils market. Essential oils are diluted with cheaper or synthetic products. Sustainable sourcing is important in essential oil production. European buyers value transparent and traceable supply chains, especially for wild-collected raw materials for essential oils.

One European company active in the essential oils sector is Alteya Organics (Bulgaria). It grows and harvests roses and lavender, distilling organic essential oils and flower waters using generations-old recipes. Their range includes organic plant extracts, oils and herbs. Their portfolio includes exotic essential oils like patchouli and ylang-ylang. Alteya Organics’ products target stress and anxiety, respiratory problems, relief from insect bites, scars and pimples, as well as others. The company supplies ingredients for the personal care, cosmetics and perfumery industries in Asia, Europe, North America and Australia.

Figure 6: Examples of essential oil products on the European market

Source: Alteya Organics

Tips:

- See the CBI studies on exporting essential oils to Europe for information on essential oils on the European health product market.

- See the CBI study on buyer requirements for natural ingredients for cosmetic products for more information on requirements for essential oils in Europe.

- Visit the website of the European Federation of Associations of Essential Oils for more information on European legislation for essential oils. The website also provides a useful overview of member associations and companies in Europe.

- Look up companies that sell aromatherapy products in Europe to see which marketing stories and health claims they use. Visit websites from companies like Puressentiel (France) and Primavera Life (Germany).

- Make your supply chain transparent for European buyers. Use appropriate tracking and tracing or other audit and certification systems to show where your ingredients come from.

Botanical extracts

MAPs are increasingly processed into extracts in the countries of origin or regional processing centres before being exported to Europe. As more healthcare companies start to bypass European processors that do not offer added value, direct demand for extracts is increasing.

The European plant extract market was valued at $3.7 billion (USD) in 2024. It is expected to reach $9.2 billion by 2033, growing at an annual rate of 10.7%. However, health products are not the only industry for these products. Extracts are used in food, beverage and cosmetic industries at considerable levels as well.

In 2024, European imports of botanical extracts amounted to €1.2 billion. Between 2020 and 2024, imports increased at an average annual rate of 3.1%. Germany, Italy, France, Spain and the Netherlands were the leading importers of extracts in Europe in 2024. Together, these countries accounted for 64% of total European extract imports.

The share of European supplies from emerging market economies grew from 34% to 44% of total imports between 2020 and 2024. Many of these supplies originated from large and well-established extract producers, such as China and India. Vietnam increased its extract exports to the European market, supplying only €393,000 in 2020, while this value reached €21 million in 2024. Another supplier that saw sharp increases in its exports to Europe between 2020 and 2024 was Indonesia, at an average annual increase of 128%.

Kenya, Rwanda, Tanzania and Uganda also saw export growth to Europe between 2020 and 2024. However, their export volumes are still smaller than to the largest countries, mentioned above.

Source: ITC Trademap (2025)

Europe has a strong extraction industry. It is concentrated in countries with strong traditions of herbal medicinal products, such as Germany, France, Italy, Switzerland, Spain and Poland. The German MAP extraction industry in particular is very large and processes and trades the largest share of MAPs in the EU.

Table 5: Important trade indicators for extracts

| Indicator | 2020 | 2024 | Change 2020–2024 |

|---|---|---|---|

| Total imports of extracts into Europe | €1.1 billion | €1.2 billion | +11% (3.1% CAGR) |

| Share from developing countries | 34% | 44% | +10% |

| Top European importers | Germany, France, Italy, Spain, Netherlands | Germany, Italy, France, Spain, Netherlands | - |

| Main developing-country suppliers | China, India, Morocco, Madagascar, Mexico, Chile | China, India, Viet Nam, Madagascar, Mexico, Kenya | - |

Source: ITC Trademp (2025)

Traditionally, the threat of new entrants is lower in extracts than for producers of raw plant materials. This is due to the high market entry requirements for processed ingredients. The number of suppliers able to provide extracts of good quality is still much lower than the number of raw material producers.

The European natural health product industry is very competitive. Combined with the demand for high-quality products and natural ingredients, it encourages innovation and research and development. For example, recent studies show the suitability of plant extracts for several future medical treatments. Velvet bean extracts could be used to treat Parkinson’s disease, and hawthorn extracts could treat cardiovascular diseases.

More and more consumers grow aware of the importance of preventive healthcare. Manufacturers use this to their advantage by marketing new products. Innovative supplement manufacturers are also looking for new extracts. These new ingredients will allow them to create distinct profiles for their products. Ingredient innovation can stem from new ingredients and traditional ingredients. For instance, RECOVERA is a branded ingredient by German plant extracts manufacturer Finzelberg. It is a prickly pear extract that combines cladode and the skins of the Opuntia ficus-indica fruit.

Tips:

- Research the efficacy of your extracts by building research partnerships. Use scientific research and data to support any claims you make, as this gives you credibility.

- Review examples of technical documentation for extracts you use. For example, see this safety data sheet for ginseng extract and this certificate of analysis for echinacea herb extract.

- Be aware which segment your extracts end up in, as there are big differences in related legislation.

Seaweeds and algae products

Edible algae is becoming more popular in Europe. It is a versatile product with high vitamin and mineral content. Edible seaweed also has antiviral, antimicrobial and antifungal properties. This, together with its high protein content, make it an attractive ingredient for health products.

Seaweeds are high in nutrients (especially in iodine), although composition differs per species. Seaweeds contain several vitamins and minerals, and dietary fibre. Seaweeds also have high levels of antioxidants. Based on these properties, European health products mainly use seaweeds for the following:

- Weight management;

- General health;

- Wellbeing;

- After-sports;

- Immune support;

- Detox;

- Digestive health.

Seaweeds for health are commonly sold as capsules and tablets that contain seaweed powder or extracts.

The global seaweed extracts market was valued at $1.26 billion (USD) in 2024, with Asia-Pacific responsible for 78% of the market. This market is expected to grow to $3.44 billion by 2032.

The EU is a relatively small producer and market in the seaweed sector. But it is one of the largest importers of algae-based products. The European Commission estimates that demand will rise to €9 billion by 2030. Imports will be used in food, cosmetics, pharmaceuticals and biofuels. Spirulina and chlorella are some of the most popular microalgae used in food supplements.

The global market for spirulina is predicted to reach $1.2 billion by 2023, growing at an average annual rate of nearly 10% between 2024 and 2032. The European spirulina market is expected to grow at an average year-on-year rate of over 13% between 2023 and 2030, reaching nearly $157 million. Approximately 70% of the world’s spirulina is produced in China, India and Taiwan. Other major producers include the United States, Thailand, Pakistan, South Africa and Myanmar.

The global chlorella market is expected to grow at an average annual rate of 7% between 2023 and 2030, reaching $336 million by 2030. The European chlorella market is expected to grow at an average annual rate of 7.2% between 2023 and 2030, amounting to $240 million by 2030.

Both chlorella and spirulina have become popular ingredients due to their nutritional benefits. They are known for their high nutritional value, high protein levels, antioxidant and anti-inflammatory properties. This makes them increasingly sought after by European food supplement manufacturers and health-conscious consumers.

Source: ITC Trademap (2025)

The total European import value of seaweeds and other algae fit for human consumption increased at an average annual growth rate of 13% between 2020 and 2024, reaching €101 million in 2024. The largest importers are the United Kingdom, Germany, Poland, the Netherlands and France, followed by Denmark, Italy and Norway.

The share of imports from emerging markets increased rapidly between 2020 and 2024. In 2020, about 35% of total imports came from these countries. This share increased to 51% in 2024. The main emerging market economy suppliers in 2024 were China, South Korea, Chile, Tanzania and Taiwan.

Table 6: Important trade indicators for seaweed

| Indicator | 2020 | 2024 | Change 2020–2024 |

|---|---|---|---|

| Total imports of seaweed into Europe | €63 billion | €101 million | +38% (13% CAGR) |

| Share from developing countries | 35% | 51% | +16% |

| Top European importers | Germany, Norway, United Kingdom, Italy, Netherlands | United Kingdom, Germany, Poland, Netherlands, France | - |

| Main developing-country suppliers | China, South Korea, Chile, Philippines, Taiwan | China, South Korea, Chile, Tanzania, Taiwan | - |

Source: ITC Trademp (2025)

Sustainability is a major issue for European consumers and companies for both cultivated and wild-collected ingredients. Buyers are becoming much more involved in the sustainable management of the natural resources they use. Consumers demand sustainable products and want to know where their products come from more often. They are more aware of the effects their purchasing behaviours have on social and environmental conditions in production countries.

Seaweeds have a good position to profit off the sustainability trend. They require no land, fertilisers or freshwater. Several seaweed species also grow very quickly. Seaweeds are better at absorbing carbon dioxide than trees, and they improve water quality by extracting nutrients like nitrogen.

Seaweed production can provide an alternative livelihood for coastal communities. With most fishery stocks depleted, seaweed cultivation can create new employment opportunities. Four interesting startups that illustrate success stories in the seaweed market are Kelp Blue (UK and Namibia), Sea6 Energy (India), Australian Seaweed Institute (Australia) and Cascadia Seaweed (Canada).The sustainability aspect of seaweed production is expected to grow in importance in the future. As European consumers look for environmentally friendly products, seaweed’s low environmental footprint will become more attractive.

Figure 9: Spirulina tablets and powder

Source: Canva

Tips:

- Target Western European importers with your seaweeds, especially Italy, Germany and the Netherlands.

- For more information on the research into seaweed’s health benefits, access scientific resources. For example, you can access Elsevier Science Direct (paid), Google Scholar and Examine.com.

- If your seaweed is not certified, promote the sustainable and ethical aspects of your production process. Buyers might ask you to support your claims with certification or documentation on your sourcing and sustainability practices. For example, the Aquaculture Stewardship Council has a sustainable seaweed standard.

- See the CBI studies on exporting seaweeds to Europe. These give more information about entering the European market and the market potential.

Turmeric

Consumer awareness of turmeric is growing and there is rising demand for immunity supporting food supplements. These have created opportunities for exporters of turmeric in developing countries. Turmeric is bacoming more and more popular as a botanical for food supplements. You are also allowed to use it for herbal medicinal products.

Turmeric roots contain different active components. The most researched one is curcumin. Turmeric root powder and its extracts are marketed for their anti-inflammatory and antioxidant properties. In European health products, turmeric is mainly used for immunity support, digestive health and joint health. Other applications include liver support, cognition, mental wellbeing and heart health. In herbal medicine, turmeric powder and extracts are authorised for relief of mild digestive problems.

The global curcumin market was worth $99 million (USD) in 2024. Europe’s market is expected to be the fastest growing in the world, with an annual predicted growth of almost 13% between 2025 and 2030. European turmeric import value amounted to €81 million in 2024. Between 2020 and 2024, imports increased at an annual growth rate of 5.6%.

Emerging market economies play a particularly large role in turmeric supplies. They account for 73% of total European imports. Supplies mainly come from India; the largest supplier of turmeric in the world. About 78% of all supplies from emerging markets are from India, while Peru (13% of total supplies from developing countries) and Madagascar (2%) export much smaller volumes to Europe.

Germany is the largest turmeric importer in Europe, followed by the Netherlands.

Source: ITC Trademap (2025)

Europe’s market share of organic turmeric is still small, but demand is growing. It is largely driven by consumer demand for organic health products. However, organic certification can also help you to stand out from the competition by showing your turmeric’s traceability.

Peru is the main supplier of organic turmeric to Europe. Other suppliers of organic turmeric include Madagascar, Indonesia, India and Myanmar. The Netherlands, Spain, Germany, the UK, France and Italy are important importers. In the future, Southeast Asian countries with tropical climates could compete too, depending on quality, price, food safety and seasonal availability.

Table 7: Important trade indicators for turmeric

| Indicator | 2020 | 2024 | Change 2020–2024 |

|---|---|---|---|

| Total imports of MAPs into Europe | €65 million | €81 million | +20% (5.6% CAGR) |

| Share from developing countries | 73% | 73% | 0% |

| Top European importers | United Kingdom, Germany, Netherlands, France, Spain | Germany, Netherlands, United Kingdom, France, Spain | - |

| Main developing-country suppliers | India, Peru, Madagascar, China, Thailand | India, Peru, Madagascar, Vietnam, China | - |

Source: ITC Trademp (2025)

With its potential in immune support, turmeric has also benefited from growing consumer demand for immunity-boosting health products. Turmeric is one of the most sought-after ingredients for health and wellness. European brands have responded to this demand by bringing immunity-supporting health products to the market. These are products such as wellness shots that support healthy digestive and immune systems.

Ingredient companies and final product manufacturers are taking advantage of its popularity. They start developing turmeric-derived ingredients with higher levels of effectiveness. For example, ingredient suppliers now produce turmeric that is more bioavailable than standard turmeric extracts.

Figure 11: Turmeric

Source: Canva

Tips:

- Determine the concentration of curcumin in your turmeric, because this is linked to turmeric’s health benefits. European buyers look for turmeric with higher curcumin content. Work with a local university or a research institute to test your product.

- Consider targeting smaller, fast growing importers of turmeric, such as importers in Eastern Europe. Although they currently import lower quantities, these can still be enough if you are a small exporter.

- For more statistics on Curcuma longa, check online sources like ITC Trademap and the Indian Spices Board. The Indian Spices Board focuses on spice production, but it also lists useful sources for turmeric exporters, such as turmeric exports from India and turmeric cultivation practices. Be aware that trade data do not distinguish between use for food or health products.

- If you target the pharmaceutical industry, make sure you can meet the high regulatory and buyer requirements for herbal medicinal products. See the CBI study Entering the European market for turmeric for more information.

- Consider getting certification that proves your turmeric meets environmental and social standards. Doing so will help you find opportunities in the European market, as the demand for certified turmeric is growing. You could consider obtaining ISO 14001:2015 Environmental management systems certification, as it shows that you uphold your environmental responsibilities.

Ginger

Europe is an interesting market for dried ginger exporters. Demand has grown by a lot in recent years. This trend is expected to continue, with an estimated annual growth of 6.3% between 2024 and 2029. While ginger is mainly used in the food industry as a spice and food ingredient, it has a lot of potential for health products as well. Globally, the pharmaceutical market is the second largest segment for ginger products.

Total European imports of ginger amounted to €488 million in 2024. Between 2020 and 2024, imports grew at an average annual rate of 3.9%. The largest importers in 2024 were the Netherlands, Germany, United Kingdom, France and Spain.

Emerging market economies play an important role in the supply of ginger. In 2024, about 80% of total imports were supplied by these markets. This is a slight increase compared to 2020, when they supplied 76% of total imports. The largest suppliers were China, Brazil, Peru, Thailand and Nigeria.

Source: ITC Trademap (2025)

Table 8: Important trade indicators for ginger

| Indicator | 2020 | 2024 | Change 2020-2024 |

|---|---|---|---|

| Total imports of MAPs into Europe | €418 million | €488 million | +14% (3.9% CAGR) |

| Share from developing countries | 76% | 80% | 4% |

| Top European importers | Netherlands, Germany, United Kingdom, France, Spain | Netherlands, Germany, United Kingdom, France, Spain | - |

| Main developing-country suppliers | China, Peru, Brazil, Nigeria, India | China, Brazil, Peru, Thailand, Nigeria | - |

Source: ITC Trademp (2025)

Ginger (Zingiber officinale) is found in a wide range of supplements (such as tablets and herbal teas). Ground ginger and ginger root extract are most common in health products.

Herbal monographs are available for dried, ground ginger. This means claims can made regarding herbal medicinal products for digestive health, and regarding nausea and motion sickness prevention. A relatively new application is for its antioxidant, antimicrobial and antibiotic properties in food supplements to support the immune system. It was used to help treat common cold and flu-like symptoms in traditional Chinese and Ayurvedic medicine.

Ginger is also used more and more in aromatherapy for which there is a growing demand. In this segment, ginger oil is used for its stimulating and warming effects. It is also used to enhance concentration and to reduce feelings of stress, anxiety and fatigue. Ginger oil is imported in the product group ‘essential oils not elsewhere specified’ (see Essential oils).

The perceived health benefits of ginger are described in a wide range of places, like blogs, vlogs and health magazines. These publications often mention that ginger consumption helps with digestive problems, colds and flu and stress. Due to its growing popularity, ginger is increasingly used as a food supplement or herbal tea.

As an ingredient for digestive health and immune support, ginger can benefit from the growing consumer demand for health products that help maintain healthy immune systems and digestion. Europe’s digestive health supplement market is predicted to grow by 7.3% every year from 2025 to 2030. The European market for immune health supplements was valued at $15 billion in 2024, growing at an annual rate of 6.2% from 2025 to 2033.

Digestive health and immunity are also linked more often. Brands are taking advantage of this by offering products that target multiple health indicators. This translates into opportunities for ginger, as it is used for both applications.

Ginger is also increasingly used in aromatherapy for which there is a growing demand. Ginger oil is used for its stimulating and warming effects, to enhance concentration and reduce feelings of stress, anxiety and fatigue.

Figure 13: Example of European food supplement that contains ginger root extract, marketed to help support healthy digestive systems and reduce feelings of travel sickness

Source: Holland & Barrett

Tips:

- Determine how feasible it is for you to meet requirements for food supplements or herbal medicinal markets. Ginger can be used in a wide variety of products, which all have different legal and buyer requirements.

- Check Open Trade Gate Sweden’s publication on the 2022 European rules regarding organic production and certification to get familiar with the requirements for supplying organic-certified products to Europe.

- Target leading Western European countries that import ginger from developing countries. The most interesting are the Netherlands, the United Kingdom and Germany. Italy and Spain could also be interesting.

- Read the CBI study on exporting dried ginger to Europe for more information on its potential as a spice.

ProFound – Advisers in Development carried out this study on behalf of CBI.

Please review our market information disclaimer.

Search

Enter search terms to find market research

Do you have questions about this research?

Although you can find good data on market trends and imports of MAPs and extracts, it can be useful to do some market research on your specific ingredients and determine how you compare to your competition. For example, find out what the major supplying countries or regions are, where and in what type of market segments your ingredients are used, and how those segments are developing. This may make it easier for you to find market opportunities and show your prospective buyers you are a credible supplier who really understands the market.

Jolanda van Hal, Editor at Nutrition Insight