Entering the European market for handwoven rugs

The mid and higher-end segments of the European market for handwoven rugs offer good opportunities, but competition is strong. You need to add value to your products through design, craftsmanship, sustainability, and storytelling. Entering the European market means you need to comply with mandatory (legal) requirements, as well as any additional or niche requirements your buyers may have. Banning child labour is an especially relevant issue in the handwoven rug industry.

Contents of this page

- What requirements and certifications must handwoven rugs meet to be allowed on the European market?

- Through which channels can you get handwoven rugs on the European market?

- What competition do you face on the European handwoven rug market?

- What are the prices of handwoven rugs on the European market?

1. What requirements and certifications must handwoven rugs meet to be allowed on the European market?

The following requirements apply to handwoven rugs on the European market. For a more detailed overview, see our study on buyer requirements for home decorations and home textiles (HDHT).

What are mandatory requirements?

When exporting to Europe, you must comply with various legal requirements.

General Product Safety Regulation

The new General Product Safety Regulation (GPSR, EU 2023/988) requires that non-food products marketed in the EU are safe to use. This applies to all non-food products sold online or offline. Non-EU products can only be placed on the market if an ‘economic operator’ in the EU is responsible for their safety. For business-to-consumer (B2C) trade, you must contract an authorised representative or fulfilment service provider.

To prove your products are safe, you must do a risk analysis and write the required technical documentation. Unsafe products are rejected at the European border or withdrawn from the market. The European Union (EU) uses the Safety Gate system to list and share information about such products.

Tips:

- Read more about the GPSR, including the questions and answers (Q&A).

- Use common sense to ensure that normal use of your product does not cause any danger.

- Search the Safety Gate alerts for handwoven rugs for an idea of potential issues.

Restricted chemicals: REACH

The REACH regulation (EC 1907/2006) lists restricted chemicals in products that are marketed in Europe.

Restricted chemicals in the production of textiles include:

- Azo dyes that release prohibited aromatic amines;

- Certain flame retardants, such as TRIS, TEPA and PBBs.

Tips:

- Comply with the restrictions as laid down in REACH.

- Do not use azo dyes that release forbidden aromatic amines. Also check that your suppliers adhere to this and ask them for certified azo-free dyes.

- Follow developments in the field of flame retardants, for instance through pinfa.

- Explore information and tips from the European Chemical Agency (ECHA), like its list of all restricted chemicals (REACH Annex XVII), information for non-EU companies and questions & answers.

Intellectual property rights

When you develop products, you must not copy an existing design. Intellectual property (IP) is protected in Europe, and products that violate IP rights are banned from the market.

Tip:

- For more information, see the European Union Intellectual Property Office (EUIPO) and the World Intellectual Property Office (WIPO).

European Green Deal

The European Green Deal is the EU’s roadmap for Europe becoming a climate-neutral continent by 2050. It provides a legal component to social and environmental sustainability. One of its main building blocks is the Circular Economy Action Plan. This includes initiatives throughout products’ entire life cycles. It targets how products are designed, promotes circular economy processes and encourages sustainable consumption. The plan also aims to prevent waste and keep the resources used in the European economy for as long as possible. In this context, legislation is constantly being updated and new laws are being developed. Some will apply to you directly and some indirectly through your buyers.

Textile Regulation

The Textile Regulation (EU 1007/2011) states that products containing ≥80% textile fibres must be labelled or marked. The label must state the full fibre composition and, if applicable, the presence of non-textile parts of animal origin. It must be durable, easily legible, visible and accessible. The label should be printed in all the official national languages of the European countries where the product is sold.

There is no EU-wide legislation on symbols for washing instructions and other care aspects. To give consumers clear information, you should follow the ISO 3758:2023 standard for graphic symbols in care labelling.

The European Commission plans to revise the regulation to introduce specifications for physical and digital labelling of textiles. This includes sustainability and circularity requirements based on the new Ecodesign for Sustainable Products Regulation.

Tips:

- Read more about the Textile Regulation. Also see the FAQ.

- Find out more about textile labelling rules from Access2Markets.

- Stay updated on the revision of the Textile Regulation.

Ecodesign for Sustainable Products Regulation

The new Ecodesign for Sustainable Products Regulation (ESPR – EU 2024/1781) entered into force in 2024. It aims to ensure that products:

- Are designed to last longer;

- Are easier to reuse, repair and recycle;

- Incorporate recycled raw materials wherever possible.

The regulation also introduces Digital Product Passports with information about products’ environmental sustainability, like their durability and use of recycled materials. The Commission adopted the first working plan in April 2025, which includes textiles. The first measures could be adopted in 2027 and be applicable 18 months later.

Tips:

- Read more about the ESPR. Also see the FAQ, Q&A and factsheet.

- Stay updated on the implementation of the ESPR.

Corporate Sustainability Due Diligence Directive and Forced Labour Regulation

The Corporate Sustainability Due Diligence Directive (CSDDD – EU 2024/1760) requires larger companies to identify and prevent, end or reduce any negative impacts their activities have on human rights and the environment. This means in the company’s own operations as well as among their direct business partners. This means that the new rules may apply to you indirectly via your buyers. The European Commission plans to publish guidelines to help companies conduct due diligence.

In February 2025, the European Commission proposed an Omnibus package to simplify sustainability due diligence requirements. As part of this, the European Parliament has agreed to postpone the application dates of the CSDDD. The CSDDD will now come into force following a staggered approach: it will apply to the first group of companies on 26 July 2028 until full application on 26 July 2030.

In addition, the Forced Labour Regulation (FLR – EU 2024/3015) bans products made with forced labour. The FLR will apply from 14 December 2027.

Packaging legislation

The Packaging and Packaging Waste Directive (PPWD – 94/62/EC) aims to prevent or reduce the impact of packaging and packaging waste on the environment. Buyers may therefore ask you to minimise the use of packaging materials and/or to use sustainable (recycled) materials.

By 2030, all packaging on the European market should be reusable or recyclable in an economically viable way. To help achieve this, the new Packaging and Packaging Waste Regulation (PPWR – 2025/40) entered into force in February 2025. This regulation will apply from 12 August 2026, replacing the PPWD.

The Plant Health Law (EU 2016/2031) also sets requirements for wood packaging materials used for transport, such as packing cases and pallets. The goal is to prevent organisms that are harmful to plants or plant products from entering and spreading within the EU.

Tip:

- Read more about the EU rules on packaging and packaging waste and the requirements for wood packaging materials.

Pending: Green Claims Directive

The European Commission has proposed a Green Claims Directive to:

- Make green claims reliable, comparable and verifiable;

- Protect consumers from greenwashing (pretending you are ‘greener’ than you are);

- Contribute to a circular and green economy;

- Help establish a level playing field when it comes to the environmental performance of products.

The proposal is currently awaiting approval. If the Directive is approved, any green claim you make about your product has to meet certain requirements. These requirements will apply to how you prove and verify your environmental claims, and to how you communicate about them. The same goes for any claim your buyer makes. Until then, 2 directives already ban misleading and false environmental green claims: the Unfair Commercial Practices Directive (2005/29/EC) and the new Directive to empower consumers for the green transition (EU 2024/825), which enters into force on 27 September 2026.

Tips:

- For details, see the Q&A and factsheet.

- Stay updated on the proposed rollout of the Green Claims Directive.

- For help with communicating your sustainable performance honestly and effectively, use the Netherlands’ guidelines regarding sustainability claims and/or the British guidance for businesses on making environmental claims.

What additional requirements do buyers often have?

Buyers often have additional requirements related to sustainability, labelling, packaging, payment and delivery terms.

Sustainability

Social and environmental sustainability are becoming more important in the European market. Environmental sustainability focuses on your company’s impact on the environment, such as through raw materials and production processes. Social sustainability focuses on your company’s impact on the wellbeing of your workers and the community. Key topics include fair wages and safe working conditions.

In addition to legal compliance, a growing number of European buyers want business partners that comply with:

- Business Social Compliance Initiative (BSCI): an initiative of European retailers to improve social conditions in sourcing countries. They expect their suppliers to follow the BSCI Code of Conduct.

- Ethical Trading Initiative(ETI): an alliance of companies, trade unions and voluntary organisations. ETI aims to improve the working conditions in global supply chains through their ETI Base Code of labour practice.

- Sedex: a membership organisation striving to improve working conditions in global sourcing chains. The platform lets you share your sustainability performance based on a self-assessment. You can also get SMETA-audited.

You can learn about sustainable options from standards such as ISO 14001 and SA8000. These standards enable certification, but most buyers do not require them.

Tips:

- Optimise your sustainability performance. Study the issues included in initiatives such as BSCI and ETI to learn what to focus on.

- If you can show your sustainability performance, this may give you a competitive advantage. For example, ITC’s Green Performance Toolkit helps small textile businesses assess and track their environmental performance and identify improvement areas. You can also use a code of conduct like the ETI base code.

- For more information, see our study on sustainability in HDHT, our tips to go green and become socially responsible, and our webinars on sustainability in the European HDHT market, sustainable innovations for your HDHT business and the sustainable transition in apparel and home textiles.

- Read more about BSCI, ETI, Sedex and SA8000 in the ITC Standards Map. You can also conduct a free online self-assessment.

- Highlight your sustainable activities and policies in the ‘story’ behind your product and company. Buyers appreciate good storytelling that evokes an emotional connection.

Labelling

The information on the product’s outer packaging should correspond to the packing list sent to the importer.

External packaging labels should include:

- Name of producer;

- Name of consignee;

- Quantity;

- Size;

- Volume;

- Warning labels.

The most important information on the product labels of handwoven rugs is composition, size, origin and care labelling. Your buyer will further specify what information they need on the product labels or on the item itself, such as logos or ‘made in’ information. This is part of the order specifications. In Europe, EAN or barcodes are commonly used on the product label. For more information, please refer to the Textile Regulation.

Packaging specifications

Importer specifications

You should pack handwoven rugs according to the importer’s instructions. They have their own specific requirements for packaging materials, palletisation and stowing containers. Always ask for the importer’s order specifications, which are part of the purchase order.

Damage prevention

Handwoven rugs are transported as rolls, wrapped in plastic film and jute/hessian sacking. They are rolled up with the face inside and packaged before they are put into a container. Sometimes two rugs are rolled up together, but this may make the roll too heavy. Runners are often protected with hardboard disks at the ends, to stop them from slipping and telescoping. When in doubt, check the requirements with your buyer.

Rugs must not be handled with bag or plate hooks, as the film packaging can easily be torn. A carpet carrying mandrel should be used to handle rolled rugs.

Material

Importers are increasingly banning wooden crating and packaging. Economical and sustainable packaging materials are more popular. Using biodegradable packing materials can be a market opportunity. Some buyers may even demand it.

Tips:

- Always ask for the importer’s order specifications, including their packaging and labelling requirements.

- See Packaging Europe for more information on the latest packaging developments.

Payment and delivery terms

Payment terms are confirmed in the order contract. They vary from buyer to buyer and are related to the volume and value of the order, the type of distribution partner, whether or not an agent is involved, and what delivery terms apply.

Delivery terms, known as Incoterms, depend on the type of distribution partner. HDHT importers generally prefer Free On Board (FOB) or Free Carrier (FCA) arrangements.

Tips:

- See our tips on how to organise your exports for more information.

- Study the different Incoterms, including your and your buyer’s rights and obligations.

- See our study on terms & conditions for a more elaborate overview, how to work with them, and the benefits of having your own.

What are the requirements for niche markets?

Fair trade practices and sustainability certification are the most common niche market requirements.

Ethical rugs and carpets

Several ethical initiatives focus specifically on the rug/carpet industry:

- GoodWeave works to end child labour in global supply chains. It is particularly active in the carpet industry in Bangladesh, India and Nepal. You can search buyers per country for an indication of the relevance in your target market.

- Label STEP focuses on fair trade and the wellbeing of weavers and workers in countries like Morocco and Nepal.

- Care & Fair aims to combat illegal child labour and improve the situation of carpet-knotting families in India and Pakistan.

Tips:

- To target the ethical niche market, you need to find business partners in this niche. Study the initiatives and how they work to determine if your company would be a good match.

- Read more on GoodWeave in the ITC Standards Map.

Fair trade

The concept of fair trade supports fair pricing and improved social conditions for producers and their communities. Fair trade certification can give you a competitive advantage, especially if the production of your products is labour-intensive, like with handwoven rugs. It often includes aspects of environmental sustainability as well.

Well-known fair-trade labels are the World Fair Trade Organisation (WFTO) Guarantee System and Fair for Life certification. For most fair-trade oriented buyers in Europe however, simply complying with WFTO’s 10 principles of fair trade is enough.

Figure 1: West Elm – fair-trade handwoven rugs

Source: West Elm @ YouTube

Tips:

- Ask buyers what they are looking for. Especially in the fair-trade sector, you can use the story behind your product for marketing purposes.

- If certification is not feasible, work according to WFTO’s principles without being officially guaranteed or certified. Carefully document your company processes so you can support your story.

- Read more about Fair for Life in the ITC Standards Map.

Sustainable textiles

Buyers are increasingly interested in certification to ‘prove’ their sustainability, especially organic certification.

Popular textile certifications include:

- Global Organic Textile Standard (GOTS) – a textile-processing standard for organic fibres that ensures environmental and social responsibility throughout the production chain.

- OEKO-TEX Standard 100 – certification that guarantees textile articles are free of harmful substances.

OEKO-TEX Made in Green combines Standard 100 and STeP. Other options include the Nordic Swan eco-label (in Nordic countries) and the EU Ecolabel.

Tips:

- Explore the possibility of sourcing organic materials. Textile products containing ≥70% organic fibres can be GOTS-certified. The easiest option is to use certified yarn or fabric.

- Read more about GOTS, OEKO-TEX Standard 100 and Made in Green, and the EU Ecolabel in the ITC Standards Map.

Recycled materials

The Global Recycle Standard (GRS) is a standard for products containing recycled material, with criteria for environmentally friendly production and good working conditions. Products containing ≥20% recycled material can be GRS-certified, but only if the entire production process is certified. Additional social, environmental and chemical requirements must also be met. For consumer-facing labelling, the product must contain ≥50% recycled content. If you use GRS-certified material, you can highlight in your communication that this material is certified.

Similarly, the Recycled Claim Standard (RCS) is intended for products containing ≥5% recycled material. The RCS does not address social or environmental aspects of processing and manufacturing.

Tips:

- Check for GRS/RCS-certified versions of the materials you use, as an alternative or addition.

- Carefully check the specifications of the available certified materials. Sometimes composition changes due to the recycling process.

- When using GRS/RCS-certified materials, communicate this correctly.

- Read more about the GRS and RCS in the ITC Standards Map.

2. Through which channels can you get handwoven rugs on the European market?

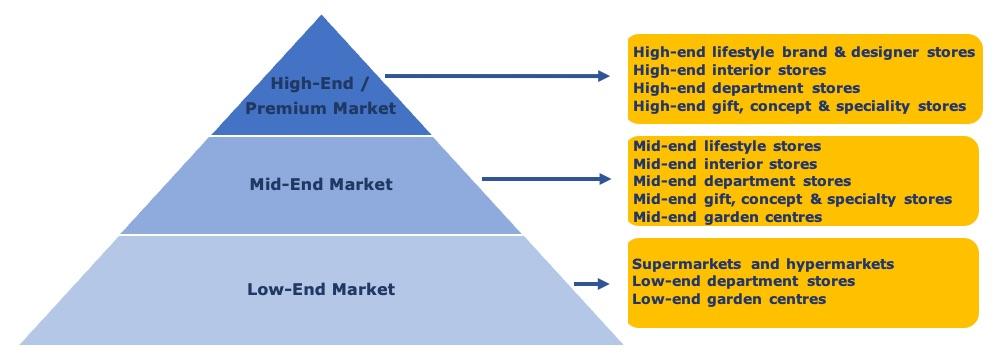

Handwoven rugs are put on the market through importers/wholesalers that supply to retailers, as well as retailers that buy directly from suppliers. The market is made up of low, mid and high-end (premium) segments.

How is the end market segmented?

Figure 2: Handwoven rug market segmentation in Europe

Source: Globally Cool, GO! GoodOpportunity & Remco Kemper

Low-end market

In the low-end segment, simple and low-priced rugs are common. They are usually small and made of inexpensive (synthetic) materials. One example of a player in this market is Aldi. Products from India, Pakistan and Bangladesh generally dominate this market. Competing with these cheap and relatively mass-produced small rugs is almost impossible. Instead, the (higher) middle and (lower) high segments offer you, as a small or medium-sized enterprise (SME), the most opportunities.

Mid-end market

The middle segment puts more emphasis on design and finish, while prices are still reasonable. H&M Home and Habitat are well-known mid-end retailers. The mid-high market responds well to local character, identity and craftsmanship. Sustainability is increasingly important to consumers in this segment. This makes the use of natural and/or recycled materials for your rugs an interesting option, as well as natural dyes.

High-end/premium market

In the high-end segment, designer quality is common and private labels are the standard. Products for this market are relatively timeless. They can also be made with high-end materials such as silk, cashmere, other high-quality wools, and blends of these fibres. Luxury brands like Woven play a role here.

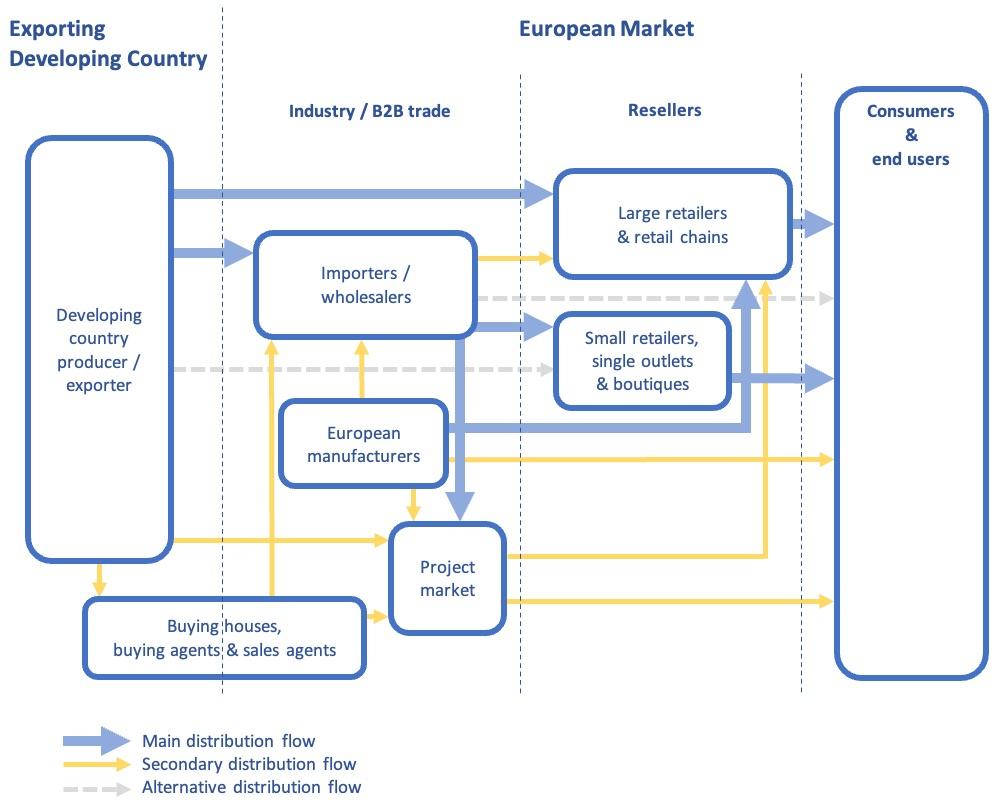

Through which channels do handwoven rugs end up on the end market?

Traditionally, the trade channels for carpets and rugs were separate from other home textile products. However, these items have now established themselves in the mainstream trade channels and have become lifestyle products. Whereas top-class kilims were previously only sold in speciality shops, they are now available at department stores. Large retail chains like IKEA now also sell handmade rugs and carpets.

This means the channels through which handwoven rugs are put on the market now also mainly use traditional patterns. Importers and wholesalers supply to retailers. Larger retail chains often bypass them and import themselves, while more and more smaller retailers have also started buying directly from suppliers. In some cases, buying agents play a role.

Figure 3: Trade channels for handwoven rugs in Europe

Source: Globally Cool, GO! GoodOpportunity & Remco Kemper

Importers/wholesalers

Importers/wholesalers sell products to retailers in their own country or region, or re-export across Europe. Supplying to buyers in the project market (such as hotels and spas) is another distribution flow for them.

These importers/wholesalers handle the import procedures. They take ownership of the goods when they buy from you (unlike agents), taking on the risk of the onward sale of the products. Developing a long-term relationship can lead to a high level of cooperation on appropriate designs for the market, new trends, use of materials, types of finishing and quality requirements.

Importing retailers

Retailers come in many sizes: large and part of a chain, or small and independent. Especially larger retail chains often import directly from their suppliers in developing countries. Many even have their own buying offices in developing countries. Others, mainly the smaller independent stores, order in Europe from wholesalers.

There is a tendency for consolidation in European retail. Large retail brands are becoming more widespread and more ‘lifestyle-centred’, offering home decoration and textiles as well as fashion accessories and furniture.

Buying agents, buying houses and sales agents

You can encounter several types of intermediaries in your dealings with European buyers:

- European buying agents represent European buyers in sourcing countries, but do not import products themselves. Sometimes they have a more limited role, such as checking product quality. They can work individually or as part of a purchasing company.

- Buying houses are comparable to buying agents, but they are based in your country and usually offer more services. These can range from raw material sourcing to design and sampling services.

- European sales agents can help you find European buyers. However, you should be careful about entering into agreements with commercial agents, because European legislation protects their position.

Agents and buying houses mostly work on commission. They may approach you, or your buyer may request an intermediary. However, you should always try to work directly with your buyer. This saves on commission and allows you to communicate directly.

E-commerce

E-commerce has grown in recent years. Your easiest way to benefit is by supplying to a European wholesaler or retailer with a strong online presence. This is usually not a separate channel. Retailers often combine online and offline channels, and the way of supplying to them is the same. Companies that only sell online also need to take stock before they can sell.

Direct business-to-consumer (B2C) sales

Selling directly to European consumers can be complicated and costly. You need an ‘economic operator’ in the EU, and you are responsible for aspects like aftersales. This is not feasible for most exporters from low- and middle-income countries.

Tips:

- To find potential buyers, search exhibitor lists or visit the main trade fairs in Europe: Ambiente, Domotex, Heimtextil and Maison&Objet.

- See our tips for finding buyers in the European HDHT market.

- For more information about trading directly with smaller retailers and e-commerce, see our study about market channels and segments.

What is the most interesting channel for you?

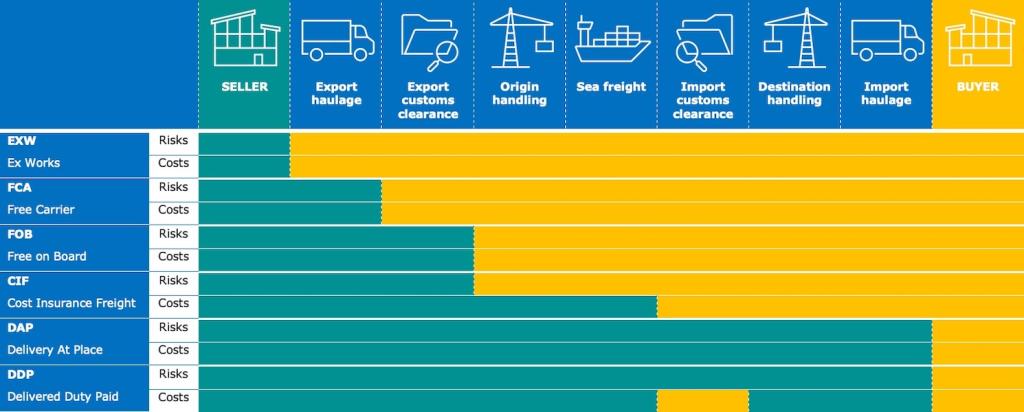

Importers and wholesalers are the main channel between exporters in low- and middle-income countries and European retailers. They are interesting if you want to develop a long-term relationship. These importers usually know the European market well, so they can provide valuable information and guidance on market preferences. They generally prefer FOB or FCA Incoterms.

Figure 4: Incoterms

Source: Globally Cool, GO! Good Opportunity & Remco Kemper

Large retailers are increasingly importing for themselves to cut out the margins of importers and wholesalers, reduce time to market and have more control over product design and finish.

Smaller, independent retailers need to differentiate from retail chains on value-added service, specialised offers and authenticity. Buying directly from producers in developing countries is an interesting way for them to do this. They usually prefer small order quantities per item, small total order volumes and delivery to their doorstep via Delivered Duty Paid (DDP) or Delivery At Place (DAP). Repeat orders are less likely. You need to calculate if this is cost-effective for you.

The trend of direct sourcing is expected to continue. This may create more opportunities for you, as a growing pool of buyers could improve your bargaining position. Because importing retailers order for their own shops, they can place orders much quicker than importers and wholesalers, who may need to show samples to their retailers before ordering.

Tips:

- Consider targeting retailers directly to improve your bargaining position and potentially close deals faster.

- Relate your offer and terms to the targeted retailer (large/small). Ask your existing buyers how they operate if you are unsure.

- Build a relationship based on mutual benefits by offering services like fast delivery and after-sales support.

- If you are interested in selling to small independent retailers, make sure you have a policy for when you participate in trade fairs. You must have appropriate terms of trading, such as low minimum order quantities.

3. What competition do you face on the European handwoven rug market?

Europe mainly imports its handwoven rugs directly from countries like India and Pakistan. To compete with these manufacturers in the mid- to high-end market, you need to add value by focusing on sustainability and using high-quality natural and/or recycled materials.

The HS code for handwoven rugs (570210) used in this study refers specifically to Kelem, Schumacks, Karamanie, and similar handwoven rugs. The main suppliers in this chapter reflect this. Different types of handwoven rugs and mats, such as sotronjis, may be registered under other HS codes that specify the materials used rather than whether they are handwoven or industrially produced.

India is Europe’s leading supplier of handwoven rugs by far. It had a direct import market share of 38% in 2024. Sweden (9.1%) was second by some distance. Next are Germany (6.9%), Denmark (6.6%), Pakistan (6.1%) and Türkiye (5.5%).

European countries have different roles in the HDHT market. Some are mainly importers and others are mainly manufacturers. Western European countries are mainly importers. Most Western European importers are re-exporters. They do not just sell their products in their own country, but distribute them across the continent.

European production mainly takes place in Eastern Europe, mostly because of relatively low transport and labour costs. This can make these countries a good alternative for European buyers to source low- to mid-end products. Western and Southern Europe also produce some high-end products from well-known premium brands with a long history.

Which countries are you competing with?

Your main competition comes from India, Pakistan, Türkiye and Morocco.

Source: UN Comtrade & Eurostat Comext, 2025

India dominates the market for handwoven rugs

India is the world’s largest exporter of handwoven rugs and Europe’s main supplier. Its exports to Europe grew from €19 million in 2020 to €22 million in 2024, peaking at €27 million in 2021. This translated to a compound annual growth rate (CAGR) of 3.4%. With a direct import market share of around 40%, India dominates the European market for handwoven rugs.

Its skilled labour and transportation at competitive costs give India a strong position. The country has a long history of carpet and rug production. The town of Bhadohi is also known as Carpet City, home to the largest handwoven/knotted carpet industry hubs in South Asia and the Indian Institute of Carpet Technology. Indian producers have easy access to a variety of natural materials and specialise in craftmanship. For example, because India is one of the biggest cotton producers in the world, its manufacturers have direct access to high-quality cotton at relatively low prices.

The combination of materials and skills allows Indian exporters to target the mid- to high-end market segments, where most handwoven rugs are sold. These strengths make the country a fierce competitor in the market for handwoven rugs.

Pakistan has a strong tradition of handwoven rug production

Handwoven rug/carpet production is one of Pakistan’s leading cottage industries, allowing weavers (often women) to work from their homes. The rugs come in various designs, styles and materials. They are mainly produced for the international market and have been exported to Europe for centuries. Exports grew from €3.1 million in 2020 to €3.5 million in 2024, with a strong peak of €5.9 million in 2022. This translated to a CAGR of 3.1%. Most of these rugs were shipped to Germany, France and Spain.

Pakistan has a large workforce and low wages. It is one of the world’s leading cotton producers, with a lot of capacity to produce textile products. This gives Pakistan a competitive edge in the production of cotton rugs. To compete with Pakistani suppliers, you can differentiate by using other natural and/or recycled materials, or high-end materials such as silk and high-quality wool (blends).

Türkiye specialises in kilim production

Türkiye is another country with a long tradition in producing (kilim) rugs, particularly in the Anatolian region. Kilim (also known as kelem, kelim, gelim and killim) rugs are flatwoven, often in colourful diagonal patterns and geometrical designs. Both vintage and modern versions are popular. They are also commonly upcycled and used to make complementary kilim cushion covers.

In addition to its expertise in handwoven rug production, the country’s strengths include its relatively low wages and its convenient location close to the European market, allowing for relatively easy and affordable transport. Türkiye’s exports of handwoven rugs to Europe grew from €2.5 million in 2020 to €3.2 million in 2024, with a peak of €3.6 million in 2022. This translated to a relatively strong CAGR of 6.8%. With that, the country’s direct import market share grew from about 5% to nearly 6%.

Morocco is known for its Berber rugs

Like most other leading suppliers, Morocco has strong rug-weaving traditions. Berber rugs are among the best-known types of rugs traditionally produced there. These rugs are made by various tribes, each with a distinct style. Beni Ouarain is a particularly popular style. The women of the tribe usually weave these fluffy tufted rugs from undyed, cream-coloured sheep wool. Each rug is uniquely decorated with black or brown geometric patterns and lines, often in asymmetrical designs.

Between 2020 and 2024, Morocco’s exports of handwoven rugs to Europe fluctuated at around €2 million. This translated to a direct import market share of about 3-4%. About a third of these rugs were exported to France. French is widely spoken in Morocco, which can make it easier for local companies to do business in France.

Which companies are you competing with?

The following companies are examples of the competition you will face in the European market for handwoven rugs.

Sharda – India

The Indian manufacturer Sharda is known for its wide variety of techniques, all by hand, and its (recycled) materials. One of the company’s strong points is an in-house design department that allows them to offer a wide range of designs and customised product development. In addition to business-to-business (B2B) sales, to further capitalise on its wide range of rugs, the company has created The Rug Republic, offering handmade rugs from stock on a B2C level. For European consumers, these online sales are conducted from the Netherlands.

Figure 6: The Rug Republic – Handloom rugs

Source: The Rug Republic @ YouTube

Sharda works with a variety of certifications and standards to verify their social and environmental performance, including BSCI, Sedex, ISO 14001, GOTS and GRS. They use biomass electricity generation and solar energy. They also control their water usage by recycling and sourcing from rainwater storage tanks. The rugs are individually bar-coded for traceability through all stages of production. Sharda also regularly organises training sessions on topics like product knowledge, communication skills, fire safety, first aid, ISO processes and quality management.

Kirkit Rugs – Türkiye

Kirkit Rugs offers restored vintage and antique rugs and contemporary rugs and kilim. Both categories have their roots in the traditional rug weaving from Anatolia, a region in Türkiye that is well known for its handmade rugs. As such, the heritage aspect of Kirkit’s products plays a major role. The company uses this as an important part of its promotion and storytelling. Kirkit is a Certified Label STEP Fair Trade Partner, guaranteeing the company’s commitment to high social and environmental standards.

IKEA – Sweden, India and Bangladesh

Even though IKEA as a company is one of the biggest players in HDHT worldwide, their approach to handwoven rugs is quite similar to other competitors in this field. You can take inspiration from the way they source raw materials, as well as the production process itself and the photography of both product and production. They work with weavers at production sites in India and Bangladesh to create designs that reflect the artisans’ skills and colourful heritage.

Figure 7: Handmade rug production in India

Source: IKEA @ YouTube

IKEA’s handmade rugs are produced in weaving centres that comply with the IKEA code of conduct. This way, IKEA can ensure good quality, care for the environment and decent working conditions. To make the handweaving industry more accessible for women, IKEA has developed a new loom that requires less physical strength. They have not patented it, so it can be available to everyone. The company aims to achieve a 50/50 gender balance among weavers across its supply base and to ensure all the wool they use for their handwoven rugs is 100% responsibly sourced.

Which products are you competing with?

Handwoven rugs mainly compete with their industrially produced, machine-made counterparts. Their main quality is decorativeness, provided by the designs, patterns, materials and techniques used to make them. The handmade aspect further adds to the story behind the rugs. All these characteristics add value and uniqueness to these products, making them more interesting for European consumers. However, if a consumer mainly needs a functional, standard rug, then these handwoven pieces cannot compete with cheap mass production.

Tips:

- Compare your products and company to the competition. You can use ITC Trademap to find exporters per country.

- Focus on design, craftsmanship, quality, your sustainable values and the story behind your products to stand out from the competition.

4. What are the prices of handwoven rugs on the European market?

Prices for handwoven rugs vary across market segments. After adding logistics costs, wholesaler and retail margins, and value-added tax (VAT), European consumer prices amount to about 4 to 6.5 times your selling price.

Table 1 gives an overview of the indicative prices of handwoven rugs in the low-, mid- and high-end market segments. ‘Indicative’ is key here, since prices for handwoven rugs vary depending on weaving technique, size, material, design, brand, and other ways of value addition, including a strong sustainable concept. Size is especially relevant, since differences in size directly influence the price.

Table 1: Indicative consumer prices of handwoven rugs in Europe

| Product type | Low-end | Mid-end | High-end/premium |

|---|---|---|---|

| Handwoven rugs (60x90 cm) | €5–25 | €25–75 | €75 or more |

| Handwoven rugs (120x180 cm) | €20–50 | €50–300 | €300 or more |

| Handwoven rugs (200x300 cm) | €50–150 | €150–900 | €900 or more |

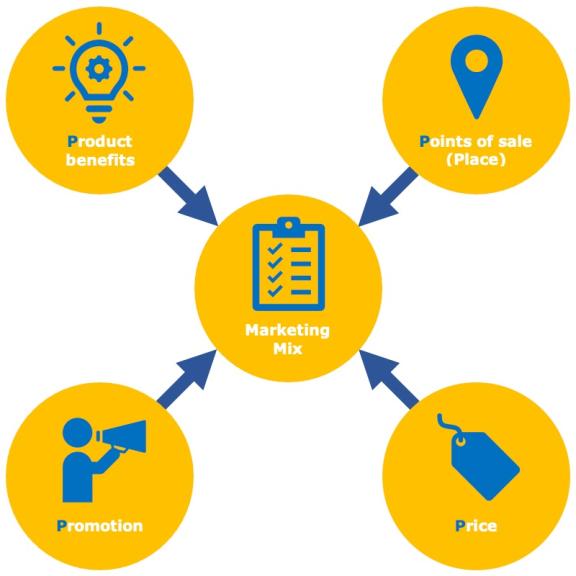

Consumer prices depend on the value perception of your product in a particular segment. This is influenced by your marketing mix.

Figure 8: Marketing mix – the 4 Ps

Source: Globally Cool, GO! Good Opportunity & Remco Kemper

Consumer prices are generally made up of:

- Your FOB price;

- Shipping, import, handling costs;

- Wholesaler margins;

- Retail margins;

- VAT – varies per country, about 20% on average.

Figure 9: Price breakdown indication for handwoven rugs in the supply chain

Source: Globally Cool, GO! Good Opportunity & Remco Kemper

The European consumer price of your rugs is about 4-6.5 times your selling (FOB) price. Besides energy, labour and transport costs, FOB prices depend heavily on the availability and cost of raw materials. For example, in recent years the price of wool has increased considerably, largely due to renewed demand from China. Occasional increases in the price of raw materials are not directly passed on to the consumer, but do put pressure on exporters’, importers’ and retailers’ margins.

For example, in Table 2 the FOB price is set at €10. Depending on the market segment your product is designed for, the consumer price ranges from €41 in the low-end market to €65.50 in the high-end market.

Table 2: Example of the price breakdown per market segment

| Price type | Low margin | Middle margin | High margin | |

|---|---|---|---|---|

| FOB price | €10.00 | €10.00 | €10.00 | Your FOB price |

| Transport, handling charges, transport insurance, banking services (20/15/15%) | +2.00 €12.00 | +1.50 €11.50 | +1.50 €11.50 | Landed price for the wholesale importer |

| Wholesalers' margins (50/75/90%) | +6.00 €18.00 | +8.60 €20.10 | +10.40 €21.90 | Selling price from the wholesale importer to the retailer |

| Retailers' margins (90/110/150%) | +16.20 €34.20 | +22.20 €42.30 | +32.70 €54.60 | Selling price excluding VAT from the retailer to the end consumer |

| Selling price incl. VAT (20%) | +6.80 €41.00 | +8.50 €50.80 | +10.90 €65.50 | Selling price including VAT from the retailer to the end consumer |

The FOB price of €10 includes your margins. These depend on your efficiency and price setting. Margins in the lower segment are generally smaller than in the middle and higher segments.

Examples of consumer prices:

- Care & Fair certified rug, 200cm diameter, Kwantum, €125

- Jute and cotton rug, 230x160cm, Sklum, ±€140

- Indoor/outdoor rug of recycled PET, 140x200cm, Fable Room, ±€215

Tips:

- Study consumer prices in your target segment to determine your price and adjust your cost accordingly. Your quality and price must match your chosen target segment.

- Calculate your prices regularly and carefully, especially if raw material prices fluctuate. If raw material prices put pressure on your margin for a longer period, consider increasing your price or finding an alternative.

- Understand your segment and offer a marketing mix that meets consumer expectations.

Globally Cool carried out this study in partnership with GO! Good Opportunity and Remco Kemper on behalf of CBI.

Please review our market information disclaimer.

Search

Enter search terms to find market research

Do you have questions about this research?

Although European customers appreciate handmade, demand for powerloom-made products is increasing. People are looking to semi-automate handmade, increase production and decrease prices. However, in the future, handwoven rugs will continue to provide high-end niche market opportunities.

Motalib Bhuiyan, Managing Director, Artisan House BD. Ltd

Our company has 17 certifications, including for recycled and organic materials. Each client and country requires different certifications. We use these to prove that we are compliant and make trading easier.

Tauhid Bin Abdus Salam, Managing Director, Classical Handmade Products BD Ltd

Webinar recording

21 January 2021