Entering the European market for chia seeds

Chia enters the European market through retail packers and food processors. There are increasing opportunities for chia as an ingredient. Most chia is consumed raw, so food safety management is a very important aspect for suppliers. There is a lot of competition with growing volumes from Paraguay and emerging suppliers from Africa and India. The level of operations and certifications is also rising. This makes Europe is a difficult target market.

Contents of this page

1. What requirements and certifications must chia seeds meet to be allowed on the European market?

Chia seeds need to follow the general buyer requirements for grains, pulses and oilseeds. For an overview of the legal requirements, you can use My Trade Assistant in Access2Markets. You can view requirements for the product code for ‘other oilseeds’ (which includes chia) 12079996 or specific export and destination countries.

What are mandatory requirements?

The most important thing when exporting chia seeds to Europe is to deliver a safe, quality and residue-free product. Food safety and traceability should be the top priorities.

Food safety: traceability, hygiene and control

The most important requirement for chia seeds is that they are safe for consumption. Most chia seeds are consumed raw and unprocessed. This means you need to pay extra attention to the levels of pesticide residues, contaminants (for example, Aflatoxins) and micro-organisms (for example, Salmonella, E. coli, Listeria monocytogenes). Either there are no residues or they are within the limits of the European legislation on Maximum Residue Levels (MRLs). Organic chia should not have any residue of non-organic chemicals.

European buyers say that high microbiological plate counts and pesticide residues are common issues for chia seeds. Chia with high microbiological activity within the limits can still be used for bakery products, but retail packers rarely accept it. In most countries, seed sterilisation has become a common practice (for example, with UV-C).

The European Union detected the following issues since 2022 (as of October 2025):

- Salmonella: 3 detections;

- Pesticide: 1 detection;

- Ethylene oxide: 1 detection;

- Glass: 1 detection;

- Presence of allergen (soybean): 1 detection.

Source: EU RASSF Window (2025)

As a supplier, you need to work according to the guidelines of Hazard Analysis and Critical Control Points (HACCP). Products must be fully traceable to where they came from. If residues in chia are not under control, European authorities may increase inspections or temporarily stop imports of it from your country.

Tips:

- Find out the Maximum Residue Levels (MRLs) for pesticides relevant to chia seeds. Search for ‘buckwheat and other pseudocereals’ (code number 0500020). European authorities do not use the code for oilseeds (0401000). A general default MRL of 0.01 mg/kg applies where no pesticide is specifically mentioned.

- Make sure chia seeds are well-dried when harvested. High moisture levels will increase the risk of microbiological contamination.

- Reduce the amount of pesticides by applying integrated pest management (IPM) in your production. IPM is an agricultural pest control strategy that includes growing practices and managing chemicals to grow healthy crops and minimise pesticide use.

- Have your chia seeds tested by a recognised laboratory to check that your product complies with EU standards. Only use representative samples, preferably from the same laboratory as your client to minimise differences in testing methods.

- Stay up-to-date with regulations and legal requirements. EU regulations are updated all the time. Stay in close contact with your buyers because they have to follow the same rules.

The EU Green Deal aims for sustainable food

In 2020, the European Union implemented the European Green Deal. The Green Deal wants to make the European economy more sustainable by 2050. As part of the European Green Deal, the Farm to Fork Strategy wants to make food systems fair, healthy and environmentally friendly. This strategy includes a 50% reduction in pesticide use and an increase in the share of organic farming land to 25% by 2030. This will probably lower the allowed pesticide residue levels over the coming years. But a framework law for Sustainable Food Systems (SFS) has been delayed. There is also no set publication date.

Novel Food

Chia seeds are a Novel Food in Europe. Novel Foods are food products that were not eaten a lot by humans in the EU before 15 May 1997. The EU Novel Food status Catalogue and Regulation (EU) 2017/2470 (consolidated version 20-08-2025) give an overview of authorised Novel Foods in the European Union. It also has a list of conditions for the use of chia, the labelling requirements and product specifications for chia seeds, chia oil and partially defatted chia seed powders.

To approve new or extended uses, you must apply and prove that your product is safe to consume. The European Commission publishes a summary of submitted applications and notifications. You can also read how to submit a novel food application using the e-submission system on their website.

Table 1 describes the current conditions under which chia may be used. The use of chia seeds in heated products at or above 120°C is still limited. This is because of concerns about the formation of acrylamide during thermal processing. The use of high-fibre chia powder in certain foods, like bakery products, is restricted to the company that applied for authorisation.

In most products, the use of chia seeds is no longer limited to a maximum. These include:

- Fruit, nut and seed mixes;

- Chia seeds as they are;

- Confectionery (including chocolate and chocolate products, excluding chewing gums);

- Dairy products (including yoghurt) and analogues;

- Edible ices;

- Fruit and vegetable products (including fruit spreads, compotes with/without cereals, fruit preparations to underlay or to be mixed with dairy products, fruit desserts, mixed fruits with coconut milk for a twin pot);

- Non-alcoholic beverages (including fruit juice and fruit/vegetable blend beverages);

- Puddings that do not require heat treatment at or above 120°C in their manufacture, processing or preparation.

Table 1: Conditions under which the novel food may be used (October 2025)

| Chia seeds | Chia oil | ‘Partially defatted chia seed (Salvia hispanica) powder’ | ||

|---|---|---|---|---|

| Product name | Chia powder with high protein content | Chia powder with high fibre content | ||

| Bread products | 5% (whole or ground chia seeds) | |||

| Baked products | 10% whole chia seeds | |||

| Breakfast cereals | 10% whole chia seeds | |||

| Sterilised ready-to-eat meals based on cereal grains, pseudocereal grains and/or pulses | 5% whole chia seeds | |||

| Fats and oils | 10% | |||

| Pure chia oil | 2 g/day | |||

| Food Supplements as defined in Directive 2002/46/EC (16-3-2025) | 2 g/day | |||

| Unflavoured fermented milk products, including natural unflavoured buttermilk (excluding sterilised buttermilk), non-heat-treated after fermentation | 0.7% | |||

| Unflavoured fermented milk products, heat-treated after fermentation. | 0.7% | |||

| Flavoured fermented milk products, including heat-treated products | 0.7% | |||

| Confectionery | 10% | 4% | ||

| Fruit juices, as defined by Directive 2001/112/EC (*1), and vegetable juices | 2.5% | 2.5% | ||

| Fruit nectars, as defined by Directive 2001/112/EC, and vegetable nectars and similar products | 2.5% | 4% | ||

| Flavoured drinks | 3% | 4% | ||

| Food supplements as defined in Directive 2002/46/EC, excluding food supplements for infants and young children | 7.5 g/day | 12 g/day | ||

| Cakes and pastries* | 5 g/100 g | |||

| Processed fruit and vegetables (including vegetable-based dishes)* | 10 g/100 g | |||

| Bread and rolls* | 10 g/100 g | |||

| Pasta-based products* | 8 g/100 g | |||

| Protein products* | 10 g/100 g | |||

Source: Regulation (EU) 2017/2470 (Consolidated version 20/8/2025).

* Use of partially defatted chia seed powder with a high fibre content for these products (*) is limited. Only the Functional Products Trading Arica S.A./BENEXIA can put these on the market within the Union during the period of data protection (until 13 November 2028). New applicants must get authorisation without reference to the proprietary scientific evidence or data protected in accordance with Article 26 of Regulation (EU) 2015/2283 or with the agreement of Functional Products Trading Arica S.A./BENEXIA.

Nutrition and health claims

Chia seeds have become popular thanks to their supposed health benefits. However, you cannot promote health benefits the European Union has not approved. Nutrition and health claims should only be made in agreement with the requirements of the Health and Nutrition Claims Regulation (EC) No 1924/2006 (consolidated version 13/12/2014). General claims like ‘healthy’ or ‘superfood’ are only allowed if you pair it with a specific permitted health claim.

Tip:

- Check with the EU Register of Health Claims and the Permitted nutrition claims to see which claims are allowed to be made on the European market.

Packaging & labelling

Chia is most often packed in polypropylene or multi-layer kraft paper bags of 25 kg. Kraft paper is often preferred in the organic trade. For larger industrial users, big bags of around 1 tonne can be used. Packaging must protect the product and comply with Regulation (EC) No 1935/2004 on materials and articles intended to come into contact with food (version 27-03-2021).

When exporting chia seeds or derivatives to Europe, the product must be labelled with the correct name:

- Chia seeds (Salvia hispanica)

- Partially defatted chia seed (Salvia hispanica) powders

- Chia oil from Salvia hispanica

Tips:

- Always talk about packaging requirements and preferences with your customers.

- Check the extra requirements if your product is pre-packed for retailers. Use the Codex General Standard for the Labelling of Prepackaged Foods (PDF) or Regulation (EU) No. 1169/2011 on the provision of food information to consumers in Europe (consolidated version 01/04/2025).

What additional requirements and certifications do buyers often have?

European buyers of chia seeds look for quality and certifications to make sure the product follows EU standards.

Quality standards

There is no official quality standard for chia seeds. But European buyers value quality. Moisture content and purity levels are the main things they look at. Specific quality specifications may vary from one buyer to the next. Most importers will look for bargains on price but they will still demand the highest purity. Table 2 shows an indication of quality characteristics that buyers often require.

Table 2: General quality standards for chia seeds

| Purity | Mostly 99.5–99.95% (discuss with buyer) |

|---|---|

| Moisture | <8% |

| Colour | Buyers may reject brown seeds, which are immature. |

| Nutritional value | A specific buyer may have additional preferences, for example, protein or oil content. |

| Visual quality |

|

| Free from |

|

Source: Industry and official sources compiled by ICI Business (2025)

Tip:

- Follow quality requirements closely and deliver the quality you have agreed on with your buyer. Being careless with your standards will give buyers a reason to submit claims about quality issues.

Certifications as a guarantee

Certifications are a good indication of your compliance with food safety requirements. They assure buyers, but buyers do not rely only on certifications. Your understanding of quality and food safety is very important to gain trust. Following high-quality standards and a HACCP-based food safety standard is just as important as the certification itself.

To get certified, the best approach is to implement a standard recognised by the Global Food Safety Initiative (GFSI). These standards are widely accepted throughout Europe. Commonly used certifications include:

- FSSC 22000 (Food Safety System Certification)

- BRCGS for Food Safety (British Retail Consortium);

- IFS Food Standard (International Featured Standard).

Tip:

- Read the CBI’s tips for organising your export and the CBI buyer requirements for grains, pulses and oilseedson the CBI Market Information platform for more detailed insights into the advantages of certifications.

Organic certification

Organic chia makes up a relatively large share of total chia sales. To market organic chia in Europe, you need to comply with Regulation (EU) 2018/848 on organic production and labelling of organic products (consolidated version 25-03-2025). You can apply for an organic certificate from an accredited certifier. Smallholder farmers are certified not as individual operators but as producer groups with an internal control system (ICS). Once you are certified, you can use the EU organic logo (see Figure 1).

Because it is a sub-tropical crop, chia is not easy to produce organically. It is especially difficult in large-scale production areas where commodity crops are grown. Although a large amount of chia is sold as organic. there are still regular problems with the illicit use of pesticides and residues. The newly implemented EU regulation aims to prevent fraud, but it also makes certification costly and complex.

It is important to know that buyers will hold you responsible for residual problems. This makes it a difficult and risky market to compete in.

FiBL & IFOAM write about the practical challenges of the new EU Organic Regulation:

- Many natural pesticides that are currently permitted in third countries are expected to be banned. Many of these pesticides use local plant extracts or microorganisms.

- External organic controls have become more complex and expensive.

- Legal requirements are difficult to understand for producers and businesses in third countries as they are written from a European perspective and applied word-for-word.

- The risk of decertification has increased because of the challenges around implementing European-specific rules in tropical agricultural systems.

Source: The World of Organic Agriculture. Statistics and Emerging Trends 2025, Page 122–123

Figure 1: The EU organic logo

Source: European Commission (2025)

Tips:

- Consider organic certification, if it is possible in your situation and location. Find the list of recognised control bodies and authorities to apply for certification. Remember that starting organic production and becoming certified can be expensive.

- Check the possibilities for group certification if you are part of a small farmers' group. IFOAM Organics International offers training manuals for smallholder group certification.

- Always avoid certification fraud, even if your buyer insists. It may seem profitable in the short term, but you risk a trade blockade if you are checked by food authorities.

What are the requirements for niche markets?

European buyers are looking for sustainability and corporate social responsibility (CSR) more and more. As an exporter, you share responsibility for ensuring sustainable supply chains. Adding extra social or environmental standards can help your company stand out in the market.

Sustainability and social compliance

Buyers will often require you to fill out a set of documents and declarations before you can do business. Or they may ask you to comply with a code of conduct. Applying standards and certifications will help you meet buyers’ expectations. Initiatives or certification schemes that can help improve your CSR performance include:

- Business Social Compliance Initiative (amfori BSCI)

- Sedex Members Ethical Trade Audit (SMETA)

- GlobalG.A.P. and GlobalG.A.P. Grasp

- Ethical Trading Initiative (ETI), using the ETI Base Code

With an organic Naturland or BioSuisse certification, you can focus on organic niche markets in Germany and Switzerland.

Consumer labels for social or sustainable conduct are not common in the chia trade yet. In the future, more buyers may look for specific labels, like Fairtrade International and Rainforest Alliance.

Tips:

- Use the ITC Standards Map to learn about the different sustainability and social standards, and see which ones are available for your country.

- Implement a code of conduct like the amfori BSCI code of conduct (PDF) to show buyers you treat all actors in the supply chain and the environment well.

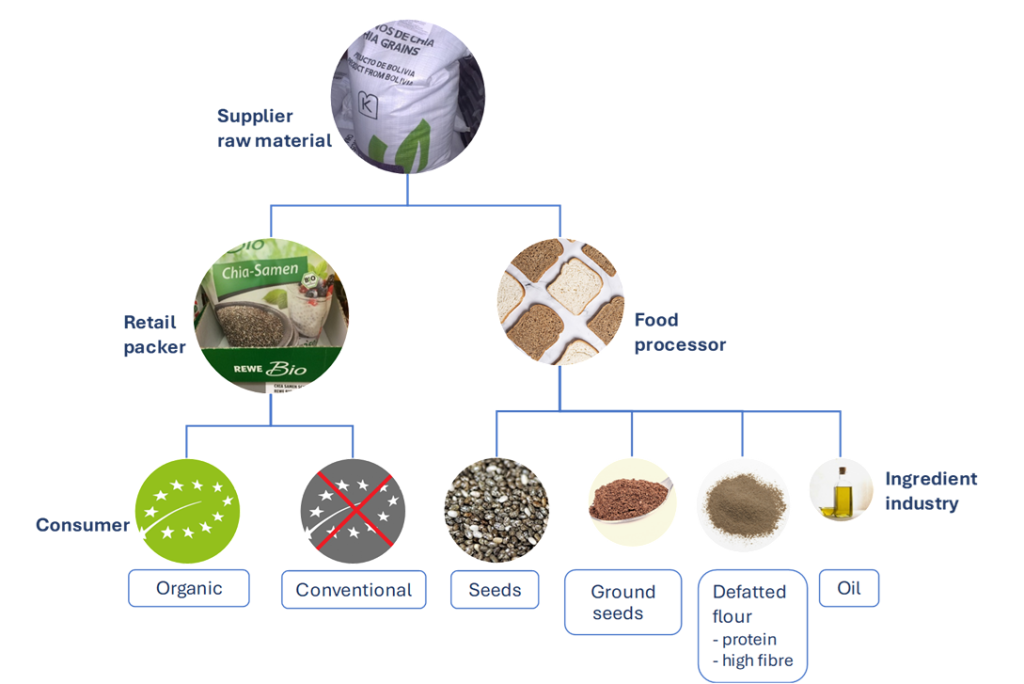

2. Through which channels can you get chia seeds on the European market?

Chia seeds are often packaged for retailers. But they also have potential as an ingredient for food brands and manufacturers. These segments are often supplied by specialised importers of natural and healthy ingredients. Because of the growing demand for chia, there could be an opportunity for new business relations.

How is the end market segmented?

The market can be roughly divided between retail packers and the processing industry.

Figure 2: Market segments for chia seeds in Europe

Source: ICI Business (2025)

Packaged for retail

Much of the bulk import is meant for retail packaging. It is a competitive segment that includes food brands and supermarket private labels.

Pre-packed chia is targeted at consumers who want a nutritious ingredient in their diet. Consumers use chia seeds in yoghurt, shakes, drinks and more. Because of the health aspect, organic certified chia has a relatively large market share.

Most pre-packed chia is sold as whole seeds and is available in general supermarkets. The few retailers that sell ground chia, chia powder and chia oil can be found online or within the specialised health food segment. Examples are Kaufland's online shop or Ölmühle Solling in Germany, Healthy Supplies and Buy Wholefoods Online in the United Kingdom and Naturitas in the Netherlands.

Food processing industry

There is a growing market for chia derivatives, like ground chia, defatted flour and oil. The use of chia seeds as an ingredient in food products is important for the future market development of chia.

The number of food brands that use chia as an ingredient seems to be growing in Europe. Baked goods and nutritious snacks are especially important, like chia charge protein bars, Semper sesame-chia crackers and Schnitzer gluten-free bread.

Demand from food manufacturers is more stable than demand from retail packers. This is because they cannot easily substitute chia as an ingredient. Price is less of a concern because food manufacturers need ingredients for production, and the percentage of chia is usually low. There is potential for both conventional and organic chia, depending on the food brand.

For food manufacturers, new ingredients like high-protein chia powder can offer new possibilities. Products like protein bars and shakes are very suitable for high-protein chia powder. These are popular with vegan consumers and athletes. High-fibre flour can be used in wholegrain foods and prebiotic drinks. Chia oil is still quite specialised. It is often marketed as an omega-3 food supplement or as a natural ingredient for cosmetics.

Figure 3: Example of a gluten-free apricot and chia oat bar in the UK

Source: factfinds from Open Food Facts (2025)

Tip:

- Analyse the available chia products in Europe by visiting supermarkets and health shops. Many outlets have their assortment online, like Rewe, Kaufland (Germany), Tesco, Holland & Barrett (United Kingdom), Albert Heijn and Ekoplaza (Netherlands). You can find a list of European supermarkets on Wikipedia.

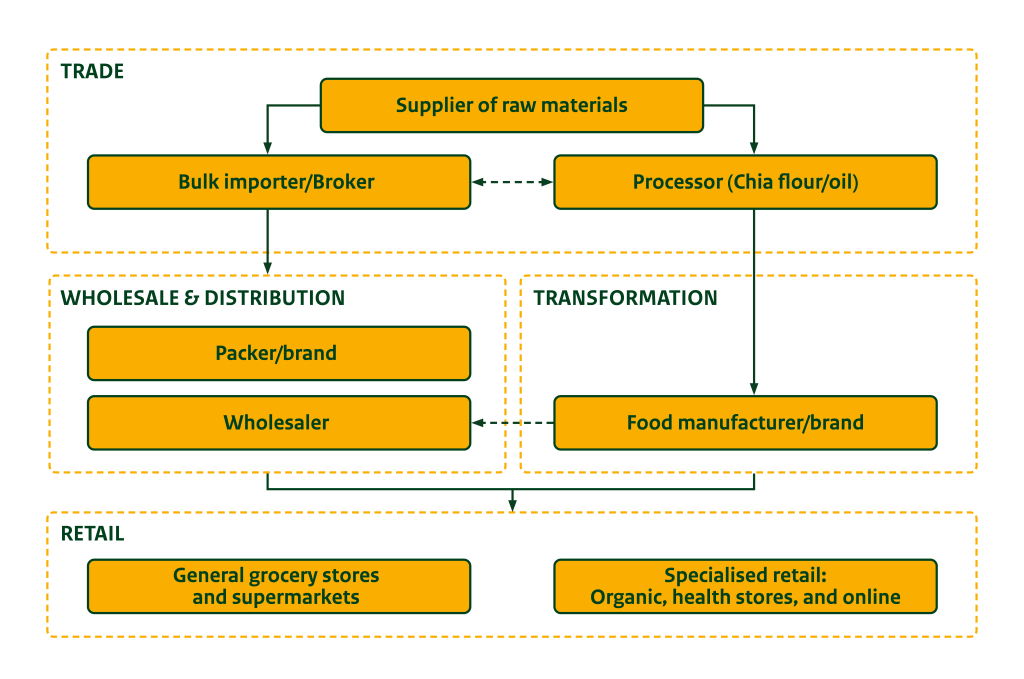

Through which channels does a product end up on the end market?

Importers of natural ingredients are the main market channel for chia seeds in Europe. They either pack for retail brands themselves or distribute chia to food manufacturers and retail packers. Food producers and larger brands may also set up their own import lines.

Figure 4: Market channels for chia seeds

Source: ICI Business (2025)

Bulk importers

Specialised importers of dry food trade most of the chia in Europe, particularly natural and health ingredients like edible seeds and nuts. Some of these companies have large assortments, and others focus on organic or functional ingredients, or chia specifically. Importers play a very important role in making sure that food safety regulations are followed and that products meet high quality standards. They distribute chia seeds to smaller users or repack chia seeds for food brands or private-label clients.

Both the chia seed industry and the businesses that import chia seeds have to deal with change. Some importers have left the chia trade over the years, but other new ones are emerging in response to the recent big rise in demand for chia. As an exporter, you must be aware of market changes and potential buyers.

Companies that focus on chia:

- Acanchia (Germany)

- Original Chia (Denmark)

- Chiabia (UK and part of Linwoods Health Foods)

Importers specialised in organic ingredients:

- Tradin Organic (the Netherlands)

- BioVeri (Poland)

Companies with a broad assortment of edible seeds, nuts or dried fruits:

- Rhumveld (the Netherlands)

- Voicevale (UK)

- Chelmer Foods (UK)

Suppliers of specialised ingredient solutions:

- Neupert Ingredients (Germany)

- Royal Ingredients (the Netherlands)

Brokers

Intermediaries or brokers can also play a role in the chia seed trade. These are often individuals or small companies that link your product to buyers in Europe and take commissions on the sales, like Seedea in Poland. Their role is purely commercial. As a supplier, you will still be responsible for most of the logistical process.

Food manufacturers/brands

Food packers, brands and manufacturers are the link with retail. They re-pack or convert chia into consumer products. Chia is a niche product for many food manufacturers, especially when chia makes up a very small percentage of a consumer food product. This is why they buy chia seeds from importers.

Only larger brands with significant interest in chia organise their own sourcing internationally. Sometimes, chia companies strengthen their position through strategic decisions. For example, the company Chiabia integrated with Linwoods Health Foods.

As the chia market continues to grow, it becomes more difficult to compete with chia brands and private-label packers. This means that more packers, including some of the first importers, are developing into added-value food companies. Original Chia has expanded its focus from chia as a raw ingredient to a number of chia products marketed under the House of Originals.

Cereal and bakery manufacturers

Gluten-free bakery brands

Plant-based food brands

- Lima Food (Belgium)

- Laboratorios Almond (Spain)

Examples of brands that pack chia seeds:

- Davert (Germany)

- Seeberger (Germany)

- Govinda (Germany)

- Biozentrale (Germany)

- Seitenbacher (Germany)

- Veríval (Austria)

- Biotona (Belgium)

- PuraSana (Belgium)

- Naturya (United Kingdom)

- TerraSana (The Netherlands)

- Pedon (Italy)

- Colfiorito (Italy)

- El Granero (Spain)

Tip:

- You can meet importers of chia seeds at large food trade fairs, like SIAL, Anuga, Biofach and Food Ingredients Europe. Use exhibitor lists or databases to search for interesting companies. For example, see exhibitor lists for Biofach and Organic-bio, the international directory of organic food wholesale and supply companies.

What is the most interesting channel for you?

Chia is part of a special ingredient market in Europe. So, importing companies are the most logical channel to enter the European market. The market is diverse enough to find new opportunities, although the largest volume is still in the hands of only a few importers. Experienced companies know the countries that supply chia very well, like Voicevale and Original Chia. Some have even integrated their businesses with suppliers, like VM Trading and Euromerc in Paraguay. Because the chia supply is not always reliable due to climate change, most importers work with more than one supplier or supply country. This can create opportunities for new exporters.

Besides connecting with the main importers, it is good to keep an eye on smaller buyers, including brand packers and food manufacturers. Food manufacturers often need smaller volumes. But they can be attractive clients because they often prefer supply security over low prices.

You can solve the issue of small volumes by maintaining your own stock in Europe. But you need to be aware that this involves competing with well-established importers and potential clients that probably have stronger positions in the market.

Tips:

- Look into your buyer’s potential in terms of volume, client networks and supply chain integration. If you find a buyer who needs a lot of chia, you could look into the possibilities of a long-term partnership. This could be good both for you and your client.

- Make sure you choose your partners strategically so you can cover different markets or segments. It is easier to build good client relationships if there is limited competition between the buyers you do business with.

3. What competition do you face on the European chia seeds market?

Paraguay is the strongest competitor in production volume and price. Buyers will also search for alternatives in other countries because they do not want to rely on a single source. Quality and certification are important if you want to stand out from your competition.

Which countries are you competing with?

Most competition for chia seeds comes from South American companies. Especially in Paraguay, where the supply has grown by a lot. In Africa, Uganda has become the most successful exporter of chia, promoting organic production. Future competition should also be expected from India.

Source: ITC Trade Map and Eurostat, calculations by ICI Business (2025)

Table 3: Indication of recent production levels 2023–2025

| Country | Production in tonnes |

|---|---|

| Paraguay | 60,000–70,000 |

| Bolivia | 7,000–15,000 |

| India | 5,000–18,000 |

| Argentina | 5,000–7,000 |

| Mexico | 5,000–6,000 |

| Uganda | 2,000–4,000 |

Source: Various sources compiled by ICI Business (2025)

Paraguay: Dominating chia supply

Paraguay is Europe’s largest supplier of chia seeds. Mechanised cultivation has turned chia into a new small commodity crop, alongside soybean and maize. Paraguay has become the most price-competitive supplier. European imports doubled between 2020 and 2024. From the 69,000 tonnes produced in 2024 plus available stock, European buyers imported around 17,300 tonnes, mainly the Netherlands and Germany.

Over the years, climatic influences, like frost and drought, have become the biggest challenges for farmers. Because Paraguay is the leading producer, dips in the harvest can greatly affect the market. For example, the 2024 harvest did not reach expected levels. The yield was 50% less than expected in 2025, leading to peak prices. On the other hand, Paraguay’s expanding production capacity means it could produce over 100,000 tonnes if the conditions are good.

Fluctuations also affect the price of organic chia. The EU imported 7,400 tonnes of organic chia seeds from Paraguay, much more than from any other producer country. But producers in Paraguay say that the country does not produce a great amount of organic chia. This raises some questions. Still, producers in Paraguay have their chemical use and maximum residue limits (MRLs) well under control.

Bolivia: Maintaining its position as a top supplier

Exports from Bolivia to Europe go up and down. Still, Bolivia has been one of the top suppliers of chia seeds since the seeds started to become more popular. Cultivation is mostly mechanical; agricultural land is relatively cheap; and there are well-developed cleaning facilities. In total, Europe imported 2,700 tonnes of chia from Bolivia in 2024. The main importers were Germany and the United Kingdom. Spain became a larger importer of Bolivian chia in 2024. Bolivia is also an important source of organic chia. The market share of organic chia imports into the European Union was an estimated 65%.

Production conditions in Bolivia are similar to those in Paraguay, but some people say that Bolivia has fewer climate issues. The country profited from recent European growth in demand in 2023 and 2024, but it has not been able to produce as much as Paraguay. For Bolivia, logistics and political unrest have been the main problems, so the country is slightly less competitive than Paraguay.

In the five years leading up to 2024, Bolivia also imported chia seeds from Paraguay and exported 2,600–5,300 tonnes of these imports to Mexico. Because Mexico had permission to export chia to China, these volumes were probably re-exported there. With the new approval for Bolivia to export chia to China, people in the industry expect that Bolivia will shift its attention to the Chinese market.

Peru: A commercial partner

Peruvian exporters combine the country’s domestic production with re-exported chia seeds from Paraguay and Bolivia. There is no exact data on the production volume, but Peru is not a big producer. Commercially, Peru is a good partner for Europe. It was the third-largest exporter, supplying 1,900 tonnes in 2024. Their main trade partner in Europe is Spain, which received approximately 1,450 tonnes of these.

With multiple smaller production initiatives, it differs from large-scale farmers in Bolivia and Paraguay. One of Peru’s main advantages is its logistical connection with various seaports. Despite some companies growing their product organically, most of the exported chia is conventional.

Uganda: Potential in organic chia

Despite several challenges, Uganda has a lot of potential. It could be a good alternative to South American chia. Until 2023, Uganda showed a growing chia trade with Europe, but this dipped below 1,000 tonnes in 2024.

European buyers see Uganda as an alternative source to make up for poor harvests in South America. They think that the number of farmers that could take part in in organic farming is Uganda’s real strength. Many areas do not make much use of agricultural chemicals. Around 86% of the chia imported by the EU was registered as organic.

Buyers also recognise the need for better organisational structures and improved seed cleaning. Production relies on large numbers of smallholder farmers. This means long supply chains and expensive logistics. When it comes to seed cleaning infrastructure, Uganda is still behind South American countries. Only a few companies manage facilities that are up to European standards and certifications.

The country has two seasons when it can produce chia seeds. But Ugandan farmers may be reluctant to produce chia because it is not a standard food for them. Lack of a stable export market has disappointed them before. On the other hand, international buyers have faced supply difficulties, including unfulfilled contracts and quality issues. These have hurt Uganda’s reputation.

Nowadays, buyers are careful when sourcing in Uganda. But they expect the country to play a larger role in the European chia market in the coming years. This may also affect production in surrounding countries, like Rwanda, Tanzania and Kenya.

India: A country to watch

India does not play a big role in the European chia trade yet. But companies in Europe are watching the developments closely because India is planting more and more chia. Estimates of Indian chia production vary from a few thousand tonnes to 18,000 tonnes. European buyers still feel some resistance to buying Indian chia because of expected quality issues and high microbiological levels.

Tips:

- Offer quality and consistency by maintaining high standards of quality control throughout the production process. To become a leading supplier of chia seeds, you need to convince buyers that you are reliable. Consistency in purity, packaging, labelling and overall product presentation is very important for building trust.

- Respect contracts and requirements. The buyer’s experience is important for the continuity of trade. Remember that one company can ruin the reputation of an entire country.

- Keep up to date with the global chia production, especially in South America and Africa. Find reliable contacts in producing countries to get first-hand information about the expected yields and production volume. When the production is not enough, it can be a good opportunity to find new clients.

Which companies are you competing with?

Innovation, compliance and certified facilities are important to being competitive in the chia business. The chia market demands well-organised suppliers who work according to Europe’s strict regulations. The best way to compete is if you have control over your quality and food safety certifications in place. Competition in leading supply countries uses organic certification, product development and innovative processing to stand out and gain goodwill from European buyers.

Paraguay: Price-competitive and compliant

Paraguay is the strongest competitor in the chia seed trade. Leading exporters in Paraguay include Agropecuaria Produza S.A., TGL Foods, Seeds Oil S.A., Super Foods Paraguay, ChiaParaguay and Healthy Grains S.A.. These exporters have invested in innovation and compliance with the high European standards. Many companies have certifications like FSSC22000, BRCGS, SMETA and EU organic. For example, Agropecuaria Produza S.A. offers a range of chia products, including premium seeds, chia oil and chia flour. TCL Organic uses ‘Thermoshock Technology’ for a chemical-free microbial reduction process.

A high degree of compliance, a large production volume and competitive pricing make companies like these very competitive.

Bolivia: Well-developed and large-scale production

In Bolivia, there are several suppliers with well-developed facilities. These include NaturalCrops, ChiaCorp, Semear Group Srl, AgroExport and Goldfoods. They have years of experience with producing and cleaning chia seeds, and they can do this on a large scale. The company Benexia, a regional group with headquarters in Chile, also has a strong presence in Bolivia. Benexia is a very innovative company and a leading chia specialist. With farms in Bolivia and Argentina, the company is also one of the largest chia-growing companies in the world. They manage more than 10,000 hectares of chia farmland. Their sister company, Productos Funcionales Delagro Srl, is the productive force behind their chia.

Peru: Commercial traders

Companies that sell chia from or through Peru often have professional marketing plans in place. They sell chia seeds together with other ingredients like quinoa, amaranth, dried fruits and cocoa. This makes them attractive suppliers of combined products. Companies that lead the chia trade from Peru include Agronegocios Wiraccocha del Perú S.A.C. and Agrofino Foods S.A.C.

Uganda: Organic chia supplier

Producers and exporters in Uganda very good at making organic products. There are several well-known and also new companies that have dedicated their resources to producing organic chia. But only a few companies can process the seeds at a level that meets European standards. This means a few companies are mostly responsible for chia processing and exports: Agri Exim, Shares Uganda and Godson Group. The challenge for these companies is to organise organic sourcing with producers, who are often large groups of smallholder farmers.

Tips:

- Keep up with your competitors’ innovations and certification levels. But do not rely only on certifications. You should also show that you understand your clients’ needs.

- Diversify your product range and do not depend on chia seeds alone. Supply and demand go up and down and are difficult to predict. This makes chia a risky business. The companies that survive in the chia export are the ones that have diversified their supply and have a long-term vision.

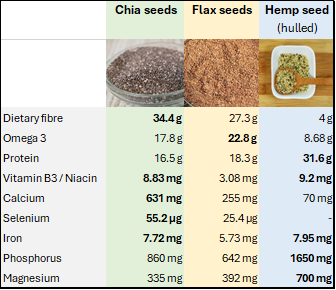

Which products are you competing with?

Food manufacturers choose ingredients based on nutritional value, marketing value and price. Chia’s combination of dietary fibre, omega-3 fatty acids and minerals give it a complete nutritional profile. But there are cheaper alternatives, like flax seeds (or linseed) and hemp seed. Flax seeds contain slightly higher doses of omega-3 fatty acids. Hemp seed has a higher protein, iron, phosphorus and magnesium content. In bakery products, sesame, sunflower, pumpkin or poppy seeds may be preferred over chia because of their taste properties.

Chia has unique characteristics, like its jelly-like substance when liquid is added. The high dietary fibre content and the ability to control viscosity and texture in food make chia seeds a functional ingredient. This gives them unique thickening properties for fruit shakes and marmalades.

Figure 6: Nutritional value of healthy seeds per 100 g

Source: USDA FoodData Central, figure by ICI Business (2025)

Tip:

- Understand the potential of chia seeds and make sure you can inform potential clients about them. Importers and food companies that already work with other healthy seeds, like flax and hemp, are likely to also purchase chia seeds.

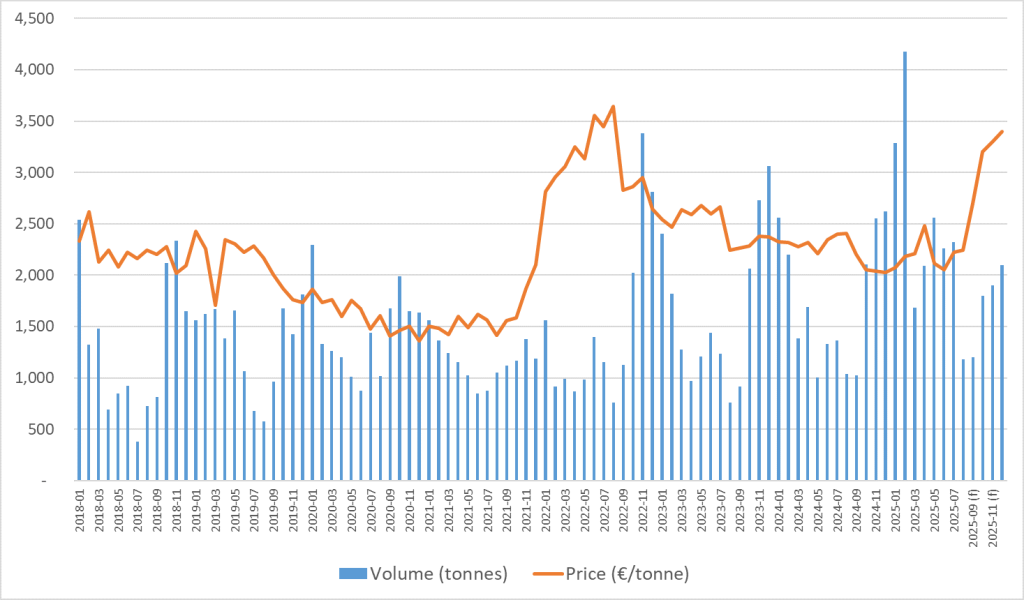

4. What are the prices of chia seeds on the European market?

Product availability is the main factor that affects trade price of chia. The climate in large producing countries can affect yields. This can lead to big changes in price. There is often a difference between the actual harvested volume and the expected production.

Common prices for European buyers are around €1,800–2,000 per tonne (FOB) for conventional chia and €2,500–2,600 per tonne (FOB) for organic-certified chia. In practice, the prices go up and down a lot. In 2021/2022, after several years of average prices below €2,000, there was a strong rise. There were price peaks of €4,000 (conventional) and €4,500 (organic) per tonne. This was mainly because of frost in Paraguay and Bolivia. The cold weather affected production and led to a market shortage. In 2025, a similar event caused prices to rise to €3,000 (conventional) and almost €4,000 (organic) per tonne.

Figure 7: Indicative price development in the EU based on trade values, in tonnes and €/tonne

Sources: Eurostat, industry sources (2025), calculations and forecast (f) by ICI Business

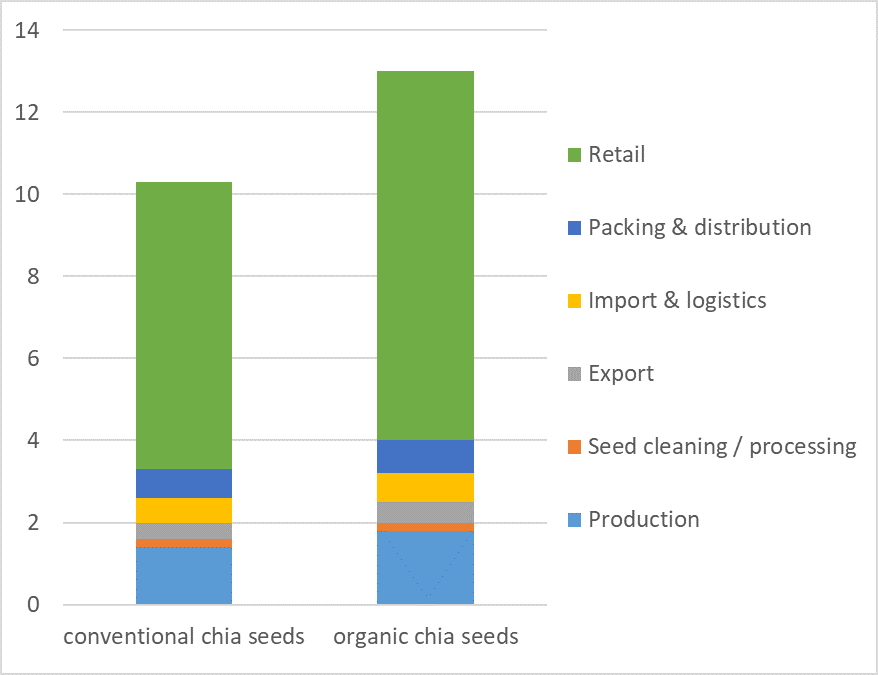

Retail prices vary and depend on the brand, retail outlet and package size. Consumers often pay an equivalent of €12–15 per kg for small packages of chia seeds. Web shops sometimes offer larger packages per kg for lower prices of €6–8 per kg. It is important to understand that retail prices are not affected much by how the trade is going. The retail price for chia seeds is pretty stable, but it may seem high compared to the trade price. The higher margin covers the risks and changes in the chia trade and covers the shelf cost of it as a turnaround product.

Figure 8: Price breakdown with indicative margins for chia seeds, in €/kg

Source: Industry sources (2025)

* Actual margins vary depending on the company and added services

Tip:

- Use your international contacts to check price developments. Online sources like Tridge may also give indications, but the best sources are still trade professionals.

ICI Business carried out this study on behalf of the CBI.

Please review our market information disclaimer.

Search

Enter search terms to find market research

Do you have questions about this research?

The chia market has become more competitive, with growing demand for certified and traceable products. Supply from Latin America is still dominant, but production challenges and climate variability are shaping a new reality where quality consistency and origin diversification are key.

Emmanuel Sanchez, Sales manager, Grains & Seeds at Royal Ingredients