The European market potential for software development services

The European market for software development services is growing. Customers are looking for software that is user-friendly, efficient, and customisable. They want software that can easily be integrated with other systems and that can be accessed from anywhere. The shortage of software developers is pushing European companies towards outsourcing. Using artificial intelligence to develop software is becoming the standard.

Contents of this page

1. Product description

Software is a set of data, instructions or programs that tell a computer what to do. The 3 main types are:

- System software – controls the computer’s core functions and allows applications to run;

- Application software – allows end-users to perform tasks; and

- Programming software – enables developers to create other software.

Regardless of the model you are using (Waterfall, Agile etcetera), software development typically involves a set of steps known as the software development life cycle (SDLC).

Figure 1: Software development life cycle

Source: Globally Cool

Providing software development services is a key segment within IT outsourcing (ITO). You can offer a complete package of SDLC services or any number of individual services. However, European companies often outsource only a part of their software development. This is usually implementation and coding, testing and maintenance, and support.

Tips:

- Look at your SDLC and software development methodology and clearly define what you can offer based on your capacity, expertise, experience, and references.

- If your focus is software testing, see our study on software testing services.

2. What makes Europe an interesting market for software development services?

Europe’s demand for software development services is driven by increasing digitisation of businesses, the rise of e-commerce, and the growing importance of data analytics, combined with a large skills shortage. Practically every European company needs software, but most do not want/need to hire an in-house software development team. Because of this, software development is among the most outsourced IT services in the world.

The European ITO market continues to grow

The global software development outsourcing market is expected to grow by a CAGR of 11.5% from 2023 to 2028. Experts believe this growth percentage also represents the European market. Surveys by Whitelane Research and partners done in 2023 among the largest European IT spending organisations show that 39% plan to outsource at the same rate and 31% plan to outsource more in 2024, while just 15% plan to outsource less.

Europe still has a software developer shortage

There is a large gap between the number of software development jobs and the number of available software developers. This gap is expected to keep growing. This has been the case for many years, and it is not expected that there will be an end to this skills shortage in the next 10 years.

Source: Eurostat

For example, in 2021, 12% of all companies in the Netherlands were looking for ICT specialists. More than 70% of the companies hiring had difficulties finding these experts. The fact that many software development buyers report that most candidates lack soft skills, further limits the availability of suitable talent.

To fill the gap, many companies in Europe try to hire software developers from abroad. An easier option, providing more flexibility, is to outsource software development tasks to offshore providers like you. The recent acceptance of working from home will only encourage this, as it blurs the distinction between in-house, nearshore and offshore teams.

Tip:

- Find the right people. Consider hiring people with the necessary talents who still need to develop the competencies needed. You can train them on the job. Also, make sure you have access to the right people to scale up operations and service clients at short notice.

European companies want to focus on their core business activities

Besides the fact that many European companies struggle to find skilled software developers, many companies do not want to employ software developers themselves. Many companies prefer to focus on their core business activities and work with outsourcing providers on their software-related projects.

Outsourcing gives European businesses access to a wide range of software development skills from around the world. This is great for handling complex projects that need specialised expertise. Outsourcing providers often specialise in the newest technologies like blockchain, AI, and IoT. This means buyers can use these technologies without needing to put a lot of effort into training their own staff. Outsourcing providers might have faced similar challenges before and can offer helpful advice to reduce risks in projects. This often leads to better project results.

The most popular programming languages at the moment are C, Java and Python, but do not forget to keep an eye out for upcoming languages such as Rust, Kotlin and Julia. There are specific programs for specific problems. For example ‘R’ is the go-to language for statistical computing and data analysis.

Tips:

- Emphasise your expertise, experience and domain knowledge in your marketing activities. This can be the deciding factor when European companies are selecting a service provider. This includes soft skills.

- Read Stack Overflow’s annual Developer Survey, which shows which developer skills are in demand and provides demographic information on software developers worldwide.

- Keep your skills and your knowledge of the latest technological developments up to date because your buyers expect that of you.

- Specialise in a few programming languages, rather than working with several that you do not fully master.

Your service is probably cheaper than hiring a software developer directly

Cost reduction remains an important reason for European companies to outsource software development. In developing countries, software developers normally cost less per hour than in Europe. The lack of software developers in Europe further increases the cost of the available specialists, who are in high demand. This is good news for outsourcing providers like you, because you can probably offer similar services at lower prices.

Be aware that if your offer is ’too cheap’, European buyers may think it must be too good to be true and assume that the quality is low.

Tips:

- Do not compete on price only. Offer competitive pricing, but do not compromise on quality.

- Be transparent in your pricing: avoid hidden costs.

- In addition to your competitive prices, promote your expertise, experience, references, capacity, flexibility, reliability, and communication capabilities.

- Read our ITO demand study to get tips on how to deal with the disadvantage of being located outside the European Union.

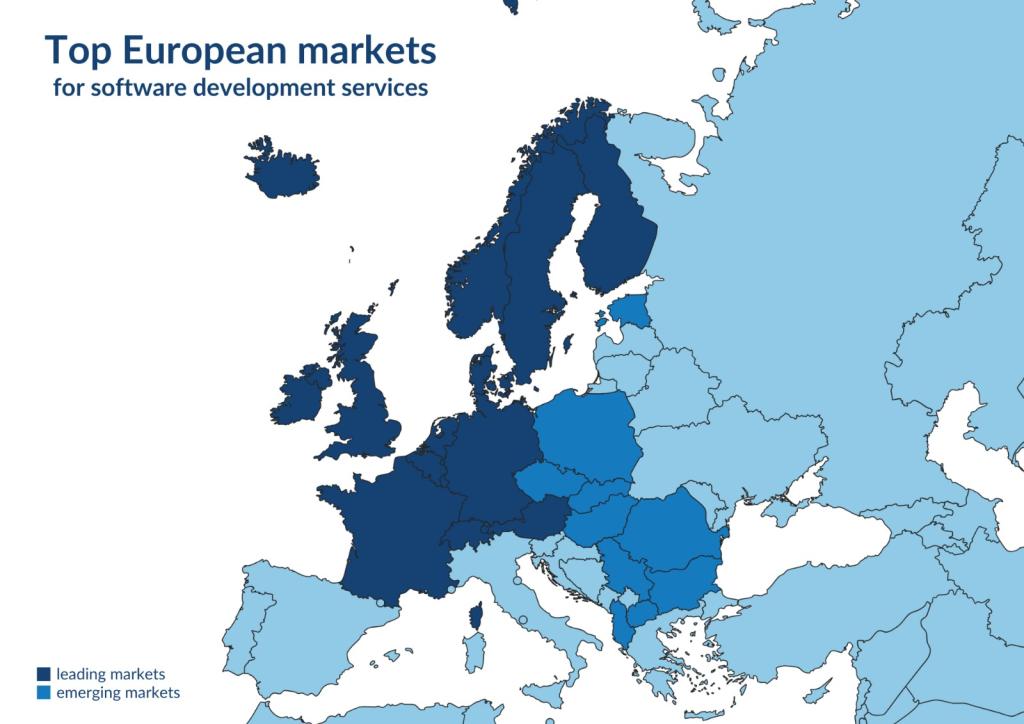

3. Which European countries offer the most opportunities for software development services?

Northern and western European countries are the biggest outsourcing markets. While the largest countries offer opportunities based on size, some smaller countries (particularly the Benelux and the Nordic countries) are key players in the software industry. In addition, central and eastern European countries (CEE region) are promising markets for partnerships with nearshore providers.

Figure 3: Leading European markets for software development services

Source: Globally Cool

Germany is Europe’s largest economy

Germany is the largest economy in Europe, home to almost 19% of the EU’s population. Its economy is widely considered the stabilising force in the EU. Germany’s main industries include the automotive, electrical and chemical sectors. They increasingly rely on software to optimise production, improve products and stay competitive.

The country is also home to some of Europe’s largest software companies, like SAP and Software AG. There are around 901,000 professional software developers in Germany. In 2019, the German software industry was projected to grow from €18 billion in 2018 to €20 billion in 2021, at an average annual rate of 2.9%. The potential effects of the pandemic were not yet included in this, but they are generally expected to boost the need for ITO.

The German market has a strong focus on industrial software.

Germany has the third-largest number of tech-related start-ups in Europe, which can be a viable target market for software development offshoring. They often cannot afford to employ a large development team, have limited budgets and need solutions fast.

Although its size makes Germany an interesting market, companies are less open to offshore outsourcing than in countries like the United Kingdom (UK) and the Netherlands. However, as German businesses continue to face skills shortages and become more experienced in offshoring, their attitude towards it is improving. In addition, the pandemic relaxed Germany’s generally stiff corporate culture and showed companies what is possible with remote working and outsourcing. This makes them more open towards outsourcing.

There could be some language barriers, as companies generally prefer to work and collaborate in German. Generally, you need an intermediary in Germany to communicate with current and potential clients for you. If you can do business in German, you could also target German-speaking companies in Austria and Switzerland.

The United Kingdom remains attractive despite Brexit

The United Kingdom is the second-largest economy in Europe. The UK is home to many industries, but their finance and banking sector is the biggest contributor to the British GDP. Software is a very important element in this sector. The UK has a thriving FinTech industry.

In 2023, British software development industry revenue was estimated to reach a value of almost €52 billion at the end of 2024. This is an annual growth rate of 4.2%.

Around 849,000 professional software developers work in the United Kingdom. The most famous British software companies include Sage, Clarivate and Darktrace. In addition, the United Kingdom is home to the largest number of tech-related start-ups in Europe.

Of all European markets, the United Kingdom is the most open to offshore outsourcing and the least cautious about doing business with developing countries. This openness is due to the nation’s cost-saving business culture and historical ties to many countries across the globe.

The effects of Brexit on software development are not entirely clear but Brexit has certainly made it harder for UK companies to hire talent from other countries. In turn, this makes the existing IT skills shortage in the UK even greater. Offshore ITO suppliers like you could benefit from this.

The Netherlands is a European IT hub

The Netherlands has the sixth-highest GDP in Europe. It is also a major IT hotspot. Major players like IBM, Microsoft, Google, NTT and Oracle have chosen the Netherlands for their European headquarters, customer services centres, research and development facilities, and more. It also has the most tech-related start-ups out of the smaller countries.

In 2023, revenue of the Dutch software development industry was estimated to reach a value of almost €52 billion by the end of 2024. This is an annual growth rate of 4.2%.

Between 2024 and 2028 revenue in the Dutch software market is expected to increase by almost €1.5 billion; that is a growth rate of almost 16%. Despite the high number of professional software developers per 1000 inhabitants, the country has one of the highest percentages of hard-to-fill IT vacancies in Europe. This could drive many companies towards outsourcing solutions, and it makes the country an interesting market, despite its size.

Companies in the Netherlands are traditionally open towards outsourcing. Research done on the Dutch market in 2024 found that the main reason for using external providers is access to resources and talent, say 56% of respondents, up from third place in 2023. Second in priority is scalability (51%), followed by a focus on core business (49%). It is very interesting that this research also found that cost reduction has seen a significant decline in importance, dropping by 16% to its lowest point to date at 23%.

Language barriers are generally not an issue, as the Dutch have excellent English language skills.

Nordic countries – Finland is in urgent need of software talent

Finland, home of open-source operating system Linux and companies like F-Secure and Nokia, is another small-sized powerhouse in IT. The Nordic countries are known for their innovation in the gaming industry. These countries offer extra opportunities if your expertise lies in the gaming industry. Another interesting segment is enterprise software.

It is also another example of a region with a shortage of software talent. Although the Finnish workforce has the highest share of IT professionals in Europe (7.6%), this is not enough to meet the fast-growing demand. This, combined with the continuous growth of the software industry, gives the current situation great opportunities for outsourcing.

Businesses in the Nordic region are increasingly looking at Eastern Europe to meet their IT needs. The demand for nearshore outsourcing, particularly to Eastern European countries, is expected to rise. Nearly 40% of organisations express their intention to include nearshore outsourcing in their outsourcing strategy.

In the Nordic countries, two-thirds of organisations plan to maintain or increase their outsourcing activities, with only 20% considering increasing outsourcing significantly. This percentage is the lowest in Europe. It is 16% lower than the European average of 36% recorded in 2022.

When companies in Nordic countries decide to homesource, their main motivation is the desire to achieve faster time-to-market and improve quality (say 60% of respondents).

Like in the Netherlands, language barriers are generally not an issue, because Finns (and the rest of the Nordics) have excellent English skills.

Poland may need offshore partners to keep up with demand

Poland is a major player in the software development industry within the central and eastern European countries (CEE region). The country is home to about 25% of the developer population in the region. This adds up to around 295,000 professional developers, in various hubs across the country. It depends on the programme, but Polish professionals are among the top 5 best developers of the world, adding to Poland’s popularity as a nearshore provider for European buyers.

Revenue in the Polish software market is expected to reach €2.1 billion in 2024 and grow to a market value of €2.6 billion in 2028, at an average rate of 4.0% per year. The country also has the highest number of tech-related start-ups in the region. To meet the demand from its flourishing software industry, Poland may increasingly need to turn to offshoring. As the country has the highest hourly rates for software development in central and eastern Europe, Polish software companies can save quite some costs by subcontracting to you.

Czechia struggles to fill IT vacancies

Czechia is another well-known software development nearshoring destination in CEE. Renowned IT brands like Avast, AVG and Socialbakers were founded there. The Czech software industry is expected to grow by a CAGR of 3.64% from 2023 to 2028. The more than 100,000 Czech software developers were rated to be in the top 10 best developers in the world.

However, in 2021, 77% of Czech companies with IT vacancies struggled to fill these positions. This was the highest rate in Europe. This drives Czech software companies towards subcontracting. Like in Poland, the relatively high hourly rates for software development in Czechia add to the benefits of offshore subcontracting for these companies.

Tips:

- Select your target market not only based on size but also by looking at factors such as cultural similarities, historical ties and shared languages.

- Use the member lists of relevant industry associations to identify potential buyers, such as Digital Europe, Bitkom, the Finnish Software and E-business Association and the Software Development Association Poland.

- Attend (online) industry events such as the EU-Startups Summit, GOTO Amsterdam, JAX London and NEXT.

- Make sure you have access to skilled professionals, for example by working with universities, setting up training courses or centres, systematically collecting and analysing CVs and having a partner network of companies and individuals.

- Emphasise your professional skills in your marketing, as well as the lower costs you offer.

4. Which trends offer opportunities or pose threats in the European market for software development services?

The biggest trend in the European software market is the increasing adoption of artificial intelligence (AI) technologies. These technologies are being used to develop software that can automate tasks, and improve efficiency and the customer experience. For developers, incorporating AI in their solutions is becoming a must-have rather than a preferred practice.

Trends in software development go fast and they will keep changing. See our study on trends for ITO/BPO for additional information, including technologies such as artificial intelligence, VR/AR, cybersecurity and big data.

Artificial Intelligence can help you to write code

A 2023 survey revealed that 70% of software developers are using or are planning to use AI tools in their development process. AI will change the ways teams design, develop, document, deliver and debug software.

This is because:

- Developers will switch from design to platform thinking. In the past, developers have built code for outcome-oriented design. Now, AI developers will focus on how platforms function in goal-oriented design. Overall, AI developers are expected to shift towards a platform thinking approach by focusing on how platforms function. They do this by achieving specific goals and objectives, using advanced AI techniques, and adopting an iterative development process to continuously optimise platform performance and effectiveness.

- AI will help draft user stories, acceptance criteria, and requirements. Developers like you will pass this information on to business analysts to ensure it aligns with their overall strategy.

- Developers will use AI for basic UI design. Human teams will do the more complex interactive design, if those are needed. After AI lays the groundwork for pages and flows, designers create a UI that helps users navigate them.

- AI can deliver continuously. Agile teams can use AI to write high volumes of code and draft PRs for teams to review. With AI assistance, you can increase your overall rate of delivery to make it feel more continuous.

- Testing will become a higher priority. Because AI produces more code, teams need to build the architecture that tests it from every angle. Test architects will evaluate end-to-end functionality and create new regression tests if issues come up.

Generative AI will drastically change the work of software developers. Especially for outsourcing service providers from developing countries. This is because in the past, the most outsourced tasks were relatively simple tasks that can now also be done by AI. But there are good opportunities for software development providers from developing countries if they learn to work with these AI tools.

Table 1: what AI can and cannot yet do

| What AI can do | What AI cannot (yet) do |

| Repeated tasks | Complex requirements |

| First drafts of code | Strategic approaches |

| Small code updates | Independent action |

Source: Globally Cool, based on information by Pluralsight

Human developers are still very much needed in software development. You need a strong team for:

- Complex coding requirements. In some projects, developers need to work on multiple requirements at the same time. Although AI is very good at responding to engineering prompts, it struggles to manage complex criteria while keeping the big picture in line with expectations.

- Context-specific results and organisational expertise. AI cannot predict the preferences of your buyer. This means AI-generated software might not align with your security and performance requirements. We still need software developers to write specific prompts or edits so the code is in line with strategic goals.

- Broader strategic approaches. AI works best with well-defined parameters. It is not good at aligning outputs with wider strategic approaches. Human developers are needed to achieve alignment between style and functionality.

- Independent action. You need to give AI input to get output. Current AI models are generative, so we need human developers to provide prompts and to think about the next steps in development.

Tips:

- Embrace generative AI for software development. There are many sources online that can help teach your staff new software development skills. One example is PluralSight. You can also read sources that help developers improve their productivity with generative AI. Another interesting article is 9 ways developer productivity gets a boost from generative AI.

- Keep in mind that AI cannot only assist in code generation but can also be used for debugging and bug detection, automated testing, QA – code review, predictive analytics, NLP to better understand requirement, automated documentation, code reuse and optimisation and predictive maintenance.

Example

KaiOS

KaiOS is headquartered in Kigali, Rwanda, and specialises in developing the KaiOS operating system, which powers feature phones with smart capabilities.

While KaiOS is primarily known for its operating system, the company also integrates AI technologies into its platform to improve user experience and provide intelligent features such as voice recognition, predictive text input, and personalised recommendations.

KaiOS Technologies is a good example of how a relatively small company is using AI to innovate and bring smart capabilities to mobile devices, contributing to digital inclusion and access to technology.

Cybersecurity is a top priority for buyers

Europe’s digital transformation and the accompanying move into the cloud, has made cybersecurity a top priority. With cybercrime on the rise, cybersecurity needs to be proactive – preventing breaches and attacks rather than reacting to them. Key to this approach is to include security throughout your SDLC (“shift left”), instead of waiting until the ‘testing’ step. Besides creating secure software, this can also save costs: the cost of fixing vulnerabilities increases from $80 in the early development process to $7,600 after they have moved into production.

There are currently 3 trends in software security:

- Automated security testing. Automated scanning tools and statistic analysis allow your developers to detect potential issues in the code during all stages of development. It is particularly interesting to quickly and efficiently identify vulnerabilities.

- Container-based software development and orchestration. These technologies offer additional layers of security by isolating applications and facilitating centralised resource management. This reduces potential attack surfaces. Examples are Docker and Kubernetes.

- Focus on DecSecOps development security. This represents a new software development approach that integrates security throughout the entire IT lifecycle. Placing security at the centre of development pipelines like this, ensures that security tests and assessments are automatically conducted during each phase of the software development life cycle.

Tips:

- Stay up to date on trends in cybercrime and software security risks.

- For more information, see our study on cybersecurity.

- While Software as a Service has become a commodity, quantum computing is so new that it is still too early to see it as a trend. Stay on top of the latest developments and identify trends and opportunities in IT via the annual Gartner Hype Cycle for Emerging Technologies. Or check blogs like Hacker Noon to stay up to date on evolving trends.

Globally Cool carried out this study in partnership with Laszlo Klucs on behalf of CBI.

Please review our market information disclaimer.

Search

Enter search terms to find market research