The European market potential for essential oils

Essential oils are relevant 'active' ingredients in the European cosmetics and wellness markets, valued for their natural origin, therapeutic properties and sensory appeal. In 2025, the European market has continued to grow, but exporters face increasing regulatory scrutiny driven by the EU Green Deal, the Chemical Strategy for Sustainability and revised classification policies. The cosmetics sector relies heavily on essential oils as fragrance components and active ingredients, especially in aromatherapy, skincare and clean beauty. However, new regulations on fragrance allergens, hazard classification and essential use criteria are reshaping market access and labelling requirements.

Contents of this page

1. Product description: essential oils

Essential oils are complex natural substances typically produced by steam distillation of leaves, stems, bark, flowers, wood, and resins. More than 300 essential oils are used in the fragrance and flavour industry.

Essential oils are concentrated chemicals and usually must be diluted before use otherwise they can cause skin and eye irritations and other undesirable effects. At the same time, they have a long history of use in traditional medicine and aromatherapy. Essential oils should never be consumed except under qualified medical supervision.

In cosmetic products, essential oils can be added directly to products such as creams, lotions, soaps, and massage oils. In all cosmetic products the perfume or fragrance is an important aspect. Most typically, but not always, the fragrances are made from a blend of synthetic aromas, and the natural substances derived from essential oils.

Some oils, such as patchouli, lavender and rose, are more and more used in their whole oil form, especially in natural or clean beauty formulations, reflecting consumer preferences for botanical purity. In perfumery, it is still more typical to use isolated components of essential oils, which offer consistency and cost control. In aromatherapy, essential oils are grouped either by aroma profile (such as spicy, woody or floral) or by their claimed emotional or physiological effects, including through relaxing, uplifting and balancing properties.

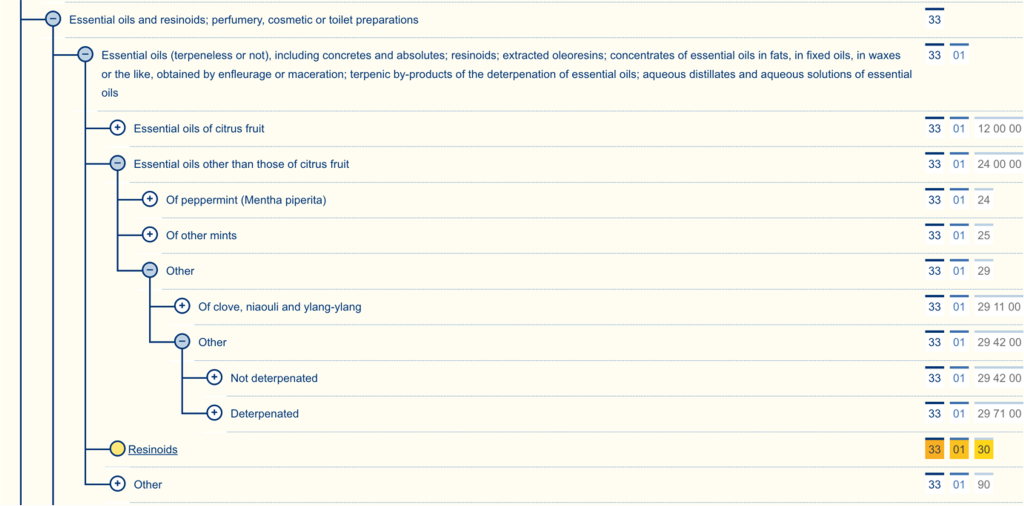

The Harmonised System (HS) classification for essential oils is shown in the figure below:

Figure 1: HS codes for essential oils

Source: Access2Markets, 2025

Essential oils are classified under HS Chapter 33.01, which covers:

- Citrus oils (orange, lemon): 3301.12–19;

- Peppermint and other mints: 3301.24–25; and

- Other single oils (rose, ylang-ylang, patchouli, tea tree, frankincense): 3301.29.

The most commonly traded essential oils, such as citrus and peppermint, have their own dedicated subheadings and are primarily used in the food and beverage industry. However, most essential oils used in fragrances and cosmetics – such as tea tree, frankincense, patchouli, ylang-ylang, vetiver and clove – fall under the broader category HS 330129.

Two examples of essential oils that we discuss in more detail in this study are frankincense and patchouli essential oils. Both of these essential oils are classified under HS code 330129.

Frankincense essential oil

Frankincense essential oil is extracted from the gum exudate of the Boswellia carterii tree, which is found in many countries across Africa, the Middle East and Asia. There are various species of Boswellia. However, the one that is used in cosmetics is Boswellia carterii. Steam distillation is used to extract the essential oil from the gum resin. It is used in cosmetics and aromatherapy, and traditionally it is also burned as incense, especially in religious ceremonies.

In aromatherapy, frankincense oil is used for its calming and meditative properties. Like all essential oils, it should not be used undiluted on the skin. There are reported health benefits for frankincense oil. However, these fall outside the scope of the cosmetics sector. Different legislation applies to substances that have medicinal properties or when they are used in therapeutic concentrations. In perfumes, frankincense oil is used as a fixative. It evaporates slowly and fixes the perfume, making it last longer.

All ingredients used in European cosmetics are typically referred to by their INCI name. INCI stands for the International Nomenclature for Cosmetic Ingredients. CosIng is the official cosmetic ingredient database of the European Commission, which is derived from the INCI database that is maintained by the Personal Care Product Council. CosIng lists more than 15,000 ingredients used in the manufacturing of cosmetics and gives information on permitted, restricted, and banned substances. In the CosIng database, you can review the cosmetic ingredients with INCI names.

In CosIng, frankincense oil is labelled as Boswellia carterii oil.

In addition to INCI, the other important reference for a cosmetic ingredient is the CAS number. CAS stands for Chemical Abstracts Service. CAS is a division of the American Chemical Society (ACS). CAS numbers are universally used to provide a unique, unmistakable identifier for chemical substances. They are especially relevant when there are many possible systematic, generic, proprietary or trivial names for the same substance. In recognition of the importance of CAS numbers, the CosIng database records include CAS numbers where these are available.

The CAS numbers for frankincense oil are 89957-98-2 / 8050-07-5. (see table 1 below)

Table 1: Frankincense essential oil record on CosIng

| INCI Name | BOSWELLIA CARTERII OIL |

|---|---|

| Description | Boswellia Carterii Oil is the volatile oil obtained from the Boswellia carterii, Burseraceae |

| INN Name | - |

| Ph. Eur. Name | - |

| CAS # | 89957-98-2 / 8050-07-5 |

| EC # | 289-620-2 / 232-474-1 |

| Chemical/IUPAC Name | - |

| Cosmetic Restriction | - |

| Other Restriction(s) | - |

| Functions |

Source: CosIng, 2025

Table 1 shows that the INCI name and CAS number of frankincense oil can be found in the CosIng database, which also provides a description and the typical functions of the ingredient. This information is essential when preparing a technical dossier for the cosmetic ingredient. However, it is important to note that the INCI name is not always searchable by common name in the CosIng database.

For example, frankincense oil cannot be located by searching the word 'frankincense', as this is not included in the INCI name or the description. Instead, the correct INCI name (Boswellia carterii oil) must be used to retrieve the relevant data.

Another useful reference for essential oils are the ISO (International Organization for Standardization) standards. These are discussed in more detail in the market entry study. While there is currently no ISO standard specifically for frankincense essential oil, the ISO 4720:2018 standard provides guidance on recommended naming conventions for essential oils, which can help ensure consistency in labelling and documentation.

Patchouli essential oil

Patchouli essential oil comes from a plant species in the Lamiaceae family. The Lamiaceae family includes many fragrant plant species, including mint and lavender. There are also many species of patchouli. However, Pogostemon cablin is the one cultivated for its essential oil because of its superior properties and yields. It originated in Indonesia, and today, 90% of all the patchouli used worldwide is supplied from Indonesia.

Patchouli is a bushy herb grown in the tropical regions of Asia. It has a heavy and strong scent. It is usually extracted by steam distillation of the shade-dried leaves. Initially, patchouli was used in the perfume industry, but it is also used in aromatherapy. In cosmetics, patchouli oil is used in products such as:

- Haircare (shampoos, scalp tonics);

- Skincare (lotions, creams, anti-acne products); and

- Personal care (deodorants and soaps).

In perfumery, patchouli oil is the most widely used raw material except for citrus fragrances. It is especially used as a base note and as a fixative. In his book 'The Essential Oils', Ernest Guenther described patchouli oil as "one of the most important and valuable perfumers' raw materials".

In the EU CosIng database, the INCI name for patchouli oil is Pogostemon Cablin Leaf Oil, CAS number: 8014-09-3 / 84238-39-1, function: fragrance. Table 2 shows the entry for patchouli oil in the CosIng database. The ISO standard for patchouli essential oil, ISO 3757:2002, defines the specifications for Pogostemon cablin oil used in perfumery.

Table 2: Patchouli essential oil record on CosIng

| INCI Name | POGOSTEMON CABLIN LEAF OIL |

|---|---|

| Description | Pogostemon Cablin Leaf Oil is the volatile oil obtained from the leaves of the Patchouli, Pogostemon cablin, Labiatae |

| INN Name | - |

| Ph. Eur. Name | - |

| CAS # | 8014-09-3 / 84238-39-1 |

| EC # | - / 282-493-4 |

| Chemical/IUPAC Name | - |

| Cosmetic Restriction | - |

| Other Restriction(s) | - |

| Functions |

Source: CosIng, 2025

Tips:

- Make sure your product descriptions and claims are aligned with legal and commercial expectations. Always provide accurate technical documentation including the INCI name, CAS number, allergen content and GC-MS profile.

- Familiarise yourself with the beneficial properties of your essential oils. Study aromatherapy websites such as Tisserand and Neal's Yard Remedies to find out how essential oils are marketed to consumers.

- Monitor your competitors’ websites to stay informed on how they present and position their essential oils in the European market.

2. What makes Europe an interesting market for essential oils?

The European cosmetics and wellness market remains an attractive destination for exporters of essential oils from low- and middle-income countries (LMICs). There is growing demand for natural, niche and ethically sourced oils, especially in the fragrance, aromatherapy and clean beauty sectors. European consumers are more and more focused on transparency, well-being and environmental sustainability, creating opportunities for suppliers who can meet high standards of quality, traceability and regulatory compliance.

The European Union imported approximately €400 million worth of essential oils under HS code 330129 in 2023, about 4,600 tonnes. Imports have shown steady growth in both value and volume over the past 5 years. Nearly 48% of the import value, around €192 million, was sourced from LMICs, including key exporters such as India, Indonesia, Egypt, Morocco, and China.

France was the largest EU importer of HS 330129 essential oils in 2023, with a value of around €291 million, of which more than two-thirds came from LMIC suppliers.

Table 3: Overview of EU imports of essential oils in 2024

| HS code | Essential oil | EU imports 2024 € | Main exporters to the EU | Imports from Africa 2024 € | Main African exporters to the EU |

|---|---|---|---|---|---|

| 330129 | Clove, niaouli, ylang-ylang and other essential oils | 947,783,000 | Indonesia, China, India | 99,387,000 | Morocco, Egypt, Madagascar |

| 330112 | Orange essential oil | 447,880,000 | Brazil, USA, Mexico | 7,997,000 | Egypt, Tunisia, South Africa |

| 330119 | Other citrus essential oils | 319,914,000 | Mexico, Peru, USA, | 4,359,000 | South Africa, Egypt, Algeria |

| 330113 | Lemon essential oil | 194,472,000 | Argentina, Uruguay, South Africa | 10,569,000 | South Africa, Egypt, Morocco |

| 330125 | Other mint oils | 25,717,000 | USA, Türkiye, United Arab Emirates | 1,196,000 | South Africa, Nigeria, Egypt |

| 330124 | Peppermint oil | 29,164,000 | Malaysia, Japan, USA | 97,000 | South Africa, Nigeria, Morocco |

Source: ITC Trade Map 2024

Demand for essential oils in cosmetics, including aromatherapy, has continued to grow more strongly than demand for traditional perfumes and fragrances. This reflects a shift towards wellness-focused and natural products in personal care. In 2024, the European cosmetics and personal care market reached a retail value of €104 billion, marking a significant milestone in industry recovery and expansion. By contrast, although fragrance and perfume sales are recovering, their value was around €13.2 billion, showing that the natural beauty trend is surpassing conventional scents.

Despite the slower growth in fragrance sales, essential oil imports have climbed steadily. According to the ITC Trade Map, the EU imported approximately €947 million worth of HS code 330129 essential oils in 2024, with a total volume of 20,520 tonnes, excluding mint and citrus oils. This ongoing rise in essential oil imports suggests that manufacturers are integrating these natural ingredients across a wider range of product formulations, including skincare, haircare, aromatherapy and clean beauty portfolios.

Source: L’Oreal Annual Report 2024

The market for artisanal and niche fragrances is resisting the broader slowdown in mainstream perfumes and fragrances. Though still a small segment, niche fragrances are gaining attention for their higher quality, symbolic exclusivity and natural ingredient concentrations. These attributes are more and more valued by European consumers. Valued at US$3.8 billion in 2023, natural fragrances are growing robustly. They are projected to reach a value of US$ 7.3 billion by 2030, with a 9.8% annual growth rate. The global natural fragrance market, which includes essential-oil-based scents, is expected to grow at a 7.5% CAGR from 2024 to 2032, reaching a total market value of US$48 billion by 2032. The market for artisanal small-batch perfumes, which often use rare natural extracts, is growing faster than the market for mainstream fragrances (2.8% annually through 2035).

Source: ITC Trade Map, 2025

The import value of essential oils in the HS code 330129 category reached approximately €947 million in 2024, showing a steady upward trend since 2021, when the value stood at around €963 million. Although there was a temporary slowdown during the COVID-19 pandemic, imports have now rebounded. Over the last 6 years, this category has seen an overall growth of more than 10%, driven by strong demand for natural ingredients in the perfume, personal care and aromatherapy sectors.

This HS category includes many of the higher-value essential oils used in fine fragrance and cosmetic formulations. According to the European Federation of Essential Oils (EFEO), approximately one-third of the global demand for essential oils comes from the fragrance and cosmetic industry, including aromatherapy applications.

The European market is expected to keep growing, driven by a stronger consumer preference for natural, traceable and sustainably sourced ingredients. Countries such as France, Germany, the Netherlands, the UK and Ireland remain the top importers in the region.

Tips:

- Refer to current market trends in your promotional materials. One effective approach is to publish short posts or articles on social media, clearly referencing your data sources. (EFEO, ITC Trade Map, Cosmetics Europe).

- Target buyers who work with a broad portfolio of essential oils. These companies often serve small and medium-sized perfumers who value niche oils and are willing to pay a premium for quality and story.

- Ensure you understand your full supply chain and communicate clearly about traceability—from plant source to finished product.

- Attend international trade shows to meet potential clients like InCosmetics and Biofach, these events attract buyers from across Europe and beyond.

- See our CBI study on tips for finding buyers in the European cosmetics market for useful information and guidance on finding buyers in channels you can use to enter the European market.

3. Which European countries offer the best opportunities for essential oils?

France, Germany, the UK, the Netherlands, Spain and Ireland offer the best opportunities for suppliers of essential oils. These countries are the largest importers of essential oils under HS code 330129. France, Germany, the UK and Switzerland also have the largest consumer markets in Europe for all cosmetic product segments, including skincare, haircare, toiletries, decorative cosmetics and fragrances.

Source: ITC Trade Map, 2025

France continues to be by far the largest European importer of essential oils. In 2024, French imports reached €303.8 million, confirming the country’s leading position. Germany followed with €134 million, while the UK recorded €116.8 million in imports. Switzerland (€116 million) and Spain (€111.9 million) also saw significant growth, strengthening their roles as key markets. Although the Netherlands has shown a declining trend in the last two years, it still imported over €72.4 million in 2024, maintaining its relevance.

The upward trend in most of these countries confirms the increasing role of essential oils across various cosmetic applications. It also highlights the importance of these countries as stable and strategic destinations for exporters from LMICs.

France

France continues to be the largest European importer of essential oils classified under HS code 330129. It has held this position for at least the last 5 years. In 2024, France imported over €304 million worth of these essential oils, confirming its status as a key entry point into the European cosmetics and fragrance markets.

Source: ITC Trade Map, 2025

The top 5 suppliers to France in 2024 were Indonesia (€34.9 million), India (€33.3 million), Türkiye (€29.9 million), Bulgaria (€19.9 million) and China (€19.6 million). These relatively balanced shares suggest that each country offers a focused and specialised range of essential oils. For instance, Indonesia is recognised as a leading supplier of patchouli oil and other high-value oils such as clove, vetiver and nutmeg. This supports the view that France values origin and specificity over volume when sourcing essential oils.

African countries remain important partners for France, supplying a total of €59.7 million in 2024. The main African exporters were Morocco (€17.3 million), Madagascar (€15.7 million), Egypt (€14.8 million), Tunisia (€6.5 million) and South Africa (€5.4 million). Although total imports from the continent have decreased from around €80 million in 2020 to just under €60 million in 2024, key players like Madagascar continue to offer value. In particular, the country has diversified beyond traditional exports such as ylang-ylang, palmarosa and clove, and it is more often shipping newer oils like geranium, niaouli and helichrysum. Interestingly, while the import volumes from Madagascar have declined over the past few years, import value has remained relatively stable. This could be a reflection of improved quality or higher market prices.

France remains a highly attractive market for suppliers from LMICs, as it is home to a significant number of SMEs active in cosmetics, perfumery and aromatherapy. This makes it a dynamic hub for essential oil sourcing. Companies involved in the import, distribution and processing of essential oils are members of Prodarom, the National Association for Manufacturers of Aromatic Products. They are also members of the French chapter of IFRA, the international fragrance association. This organisation is headquartered in Grasse, France, the heart of the French fragrance and flavour industry.

Germany

Germany remains the second-largest European importer of essential oils. In 2024, the country’s essential oil imports were valued at €134 million. This marks a recovery from €108 million in 2023 and shows resilience despite moderate year-to-year fluctuations over the past 5 years. Quantities have followed a similar trend, showing stable demand across this period.

Source: ITC Trade Map, 2025

The top 5 suppliers to Germany in 2024 were France (€29.49 million), China (€15.40 million), the US (€14.96 million), Indonesia (€11.71 million) and India (€7.60 million). The top 3 suppliers, France, China and the US, accounted for nearly 45% of the total imports, highlighting a concentrated sourcing pattern that differs from France’s more fragmented supply chain. However, the overall range of supplying countries remains mostly similar. This suggests opportunities for new suppliers to enter the German market, provided they offer a competitive mix of quality, pricing and delivery reliability.

Among the African countries, Egypt, Madagascar, Morocco, South Africa and Tunisia remain the primary suppliers of essential oils to Germany. However, their combined share is still modest. In 2024, African suppliers represented around 7% of Germany’s total imports under this HS code, slightly lower than in previous years. Madagascar and South Africa saw minor reductions in volume and value, while Morocco and Egypt have maintained stable export levels to Germany.

Germany remains an important and reliable destination for essential oils from LMICs, particularly for exporters who can offer consistent supply, traceability and alignment with sustainability expectations. While the market is competitive, niche oils and co-creation with buyers can offer viable entry points.

Some of the well-known importers of essential oils in Germany are Axxence, Frey&Lau, Symrise, Ter Ingredients and Voegele.

The United Kingdom

The UK continues to be the third most important importer of essential oils under HS code 330129. In 2024, the UK imported approximately €116.8 million of these essential oils, showing a slight recovery after a dip in 2023 (€96.6 million). Although overall import values have varied over the 5-year period, the trend in import volumes continues to rise, indicating stable demand from British manufacturers and retailers.

Source: ITC Trade Map, 2025

The top 5 suppliers to the UK by value in 2024 were China (€29.6 million), France (€19.8 million), Indonesia (€8.5 million), India (€6.5 million) and Hungary (€5.4 million). These suppliers were responsible for over 60% of the UK’s total imports of essential oils under this classification. While France and China have consistently been the top two suppliers, China has steadily increased its lead over the period, becoming the UK’s largest source in terms of value. On the other hand, imports from the US dropped significantly, from €13.7 million in 2020 to just €4.9m in 2024.

This shift may reflect changes in supply chain preferences or pricing strategies among UK importers. Imports from Indonesia and India have grown a bit, showing increased interest in niche or sustainably sourced essential oils from these regions.

While values for most African countries are still fairly low, Egypt and South Africa remain relevant suppliers, followed by Tunisia, Morocco and the Comoros. Together, these countries account for a small but stable share of the UK market.

In the UK, there are many well-known companies that use natural ingredients in their products, including essential oils. These include The Body Shop, Lush, Neal’s Yard Remedies and Tisserand. There are also many companies that produce fragrances and fragrance components. You can find a list of these on the IFRA UK website. Well-known UK importers include Treatt, Augustus Oils, O&3 and Naissance, and many small and medium-sized companies exist. You can also find a list of UK traders for HS code 330129 on the UK Trade data website.

Switzerland

Switzerland is the fourth most important European importer of essential oils. Over the last 5 years, imports have grown steadily, reaching €116 million in 2024, up from €79.8 million in 2020. This represents a 45% increase in value, underlining Switzerland’s rising importance as a destination market for essential oils used in cosmetics, fragrances and wellness products.

Source: ITC Trade Map, 2025

France remains the top supplier to Switzerland by value, with imports reaching €28 million in 2024. Indonesia followed closely at €23.5 million, maintaining its position as a leading supplier thanks to key essential oils such as patchouli and vetiver. The US is also a strong supplier, with values rising to €17.5 million in 2024. The top 5 suppliers by value in 2024 were France, Indonesia, the US, Haiti (€7.7 million) and India (€5.5 million), accounting for more than 70% of all Swiss imports of HS 330129 essential oils.

Haiti, though smaller in overall value, has shown notable growth. Imports from Haiti nearly doubled from €4.1 million in 2020 to €7.7 million in 2024, likely driven by high-value oils such as vetiver. China, while still relevant, has seen a slight decline in value, with imports decreasing from €6.3 million in 2020 to €4.7 million in 2024.

Imports from African countries account for around 8-10% of Switzerland’s total imports of this product group. Key African suppliers include Egypt, Madagascar, South Africa, Morocco and Tunisia. South Africa stands out for its stable growth, placing itself as a consistent source of competitive and high-quality essential oils for Swiss buyers.

Switzerland is home to Firmenich, the biggest privately owned fragrance and flavour company in the world. It is therefore not surprising that Switzerland is in the top 6 most important importers of HS330129 essential oils, when, in terms of its population size, it is the 15th largest country in Europe. Firmenich is also a leader in developing sustainable supplies of essential oils and traceability in the supply chain. This is creating a ripple effect across the whole industry. Also, Firmenich, like many of the major flavour and fragrance companies, has offices in the major supplying countries such as Indonesia, India, Colombia, and Mexico.

The members of the Swiss Flavour and Fragrance Industry Association are all the major flavour and fragrance companies in Switzerland. Other well-known Swiss traders of essential oils include Damascena and Ecsa Chemicals.

Spain

Spain continues to be the fifth most important European importer. Over the last 5 years, the country’s imports have steadily increased, reaching a record value of €111.9 million in 2024, up from €85.4 million in 2020. This growth reflects Spain’s increasing relevance as a destination market for essential oils used in cosmetics, aromatherapy and wellness applications.

Source: ITC Trade Map, 2025

Indonesia remains Spain’s leading supplier of essential oils, with exports reaching €28.5 million in 2024, accounting for more than 25% of Spain’s total imports. Indonesia’s dominance is driven by its strong supply of patchouli, clove and nutmeg oils, which continue to be in high demand among Spanish manufacturers and distributors.

Other key exporters in 2024 included France (€18.3 million), China (€11.2 million), India (€6.3 million) and Haiti (€4.2 million). Together, these top 5 suppliers accounted for more than 60% of Spain’s total imports of essential oils, showing a relatively concentrated supplier base.

Spain also sources a significant share of its essential oils from African countries. In 2024, African suppliers such as Tunisia, Egypt, Morocco, South Africa and Madagascar contributed around 10% of Spain’s total imports by value. This represents one of the highest percentages of African-origin essential oils among major European importers. For comparison, the volume of imports from Indonesia continues to exceed that of all African countries combined, highlighting not only Indonesia’s production scale but also Spain’s specific demand for Indonesian-origin oils.

Spain’s importance as an importer is linked to its robust manufacturing sector for cosmetics and fragrances, including several companies known for blending essential oils into skincare and haircare formulations. Its proximity to North Africa also facilitates strong trade flows and logistics for natural ingredients sourced from the Mediterranean and Sahel regions.

The Spanish market is an important market for suppliers of essential oils. Spain has a thriving fragrance and flavour industry, as represented by the Spanish Association for Fragrance and Food Flavourings (AEFAA). The members of this association are important potential customers for suppliers of essential oils. Important traders of essential oils include Indukern, Lluch, and Ventos.

The Netherlands

The Netherlands is currently the sixth-largest importer of essential oils in Europe. While its rank has fallen slightly in recent years, the country remains a key player in the European trade of essential oils, especially as a re-export and distribution hub. In 2024, imports reached €72.5 million, reflecting a decline compared to €101.1 million in 2020. This marks a 29% decrease over 5 years, with a sharper drop observed in the last two years.

Source: ITC Trade Map, 2025

Despite the decline in value, the Netherlands continues to source essential oils from a relatively concentrated supplier base. In 2024, the top exporters by value were the US (€19.8 million), France (€18.5 million), China (€6.6 million), Indonesia (€5.1 million) and the UK (€3.2 million). Together, these 5 countries accounted for 75% of total imports, highlighting a high level of supplier concentration compared to other European countries.

Imports from African countries remain limited, with total values below 1% of the Netherlands' essential oil imports. Key African suppliers include South Africa, Egypt, Morocco, Tunisia and Ghana, but volumes remain marginal. In 2024, imports from Africa were estimated at around €500,000-€800,000, reflecting limited demand. One of the reasons for this could be that the Netherlands has a smaller domestic cosmetic production base than France, Germany and Spain. Moreover, European buyers can directly import essential oils from their countries of origin rather than relying on intermediary trading via the Dutch market.

Still, the Netherlands plays an important role in the logistics and redistribution of essential oils across Europe, thanks to the advanced infrastructure of ports such as Rotterdam and strong position as a trade gateway. It remains a relevant entry point for exporters aiming to reach broader European markets, particularly for those working with specialised traders and distributors.

Therefore, it is still important to include Dutch buyers in your marketing activities. Two well-known Dutch companies that trade in essential oils are De Lange and IMCD. The members of The Netherlands Flavour and Fragrance Association (NEA) may also import certain essential oils from the 330129 category.

Tips:

- Develop lists of potential buyers in at least the six countries above.

- Keep up to date with industry developments by regularly checking the IFEAT and IFRA websites.

- Keep up to date with what the major companies and company associations are talking about and reporting, especially with regard to sustainability.

- Have a look at our CBI report What is the demand for natural ingredients for cosmetics on the European market? to read about the potential demand of the European market.

Video 1: The fragrance journey – discover how the IFRA Standards help you to enjoy fragrance with confidence

Source: IFRA – The International Fragrance Association, 2022

4. Which trends offer opportunities or pose threats in the European essential oils market?

There is a growing demand for essential oils that meet high sustainability standards. This does not necessarily mean that you need certification. Still, you will need to document your activities, especially with regard to environmental impact, and be able to offer traceability back to the origin of the raw materials.

Growing importance of sustainable production

Sustainable and traceable supply chains are becoming a key requirement in the cosmetics industry. This is driven by regulation, consumer awareness, environmental concerns and brand commitments to responsible sourcing. For essential oils like frankincense and patchouli, sustainability issues are particularly relevant.

Frankincense essential oil (Boswellia carterii) is under pressure due to unsustainable harvesting. Because this production is the main source of income for some rural communities in the mountainous regions of Somalia, trees are often over-tapped without allowing a sufficient one-year resting period. This depletes their health and makes them more vulnerable to insect damage and low germination rates. As demand grows, producers in regions like Somalia and Ethiopia face economic pressure to extract more resin than is ecologically viable.

Certification schemes like FairWild and Cosmos Organic offer frameworks to support sustainable production, but implementation challenges remain, particularly in remote rural areas. FairWild, for example, requires ongoing documentation and monitoring. Organic certification can still improve practices and enhance market credibility.

Patchouli producers also face sustainability issues linked to soil degradation, climate variability and inconsistent agricultural practices. Leading fragrance companies such as Firmenich, Givaudan and Symrise are working with sourcing partners like Indesso in Indonesia to implement regenerative agriculture, farmer support and responsible sourcing standards. These partnerships serve as models for long-term collaboration with producers in LMICs.

Video 2: Indesso, Indonesia – sustainable practices and company profile

Sustainability in the essential oil industry will become even more important in the coming years as brands seek full supply chain visibility and compliance with evolving EU environmental regulations.

Tips:

- Invest in sustainability practices when supplying frankincense, patchouli, and other essential oils. European buyers often prioritise partners that follow good agricultural and collection practices (GACP) and traceable, responsible sourcing.

- Read our tips on going green with natural ingredients for cosmetics.

- Review the Responsible Sourcing Practices of Firmenich, Givaudan and other major companies. Implement their requirements as much as you can.

- Consider adopting sustainability standards such as FairWild and/or Organic. Having your essential oils certified adds credibility to your products, allowing you to charge a premium. Make sure that you present all your certifications in your marketing materials.

- Have a look at our CBI study on Entering the European market for essential oils.

Increasing demand for personalised and niche fragrances

In recent years, there has been a clear trend towards the personalisation of fragrances. This movement continues to gain traction in 2025, particularly among millennials and Gen Z consumers, who want deeper emotional and sensory connections with their cosmetic choices. Personalised fragrances allow them to express their identity and values while enjoying a more tailored product experience.

The niche fragrance market remains the fastest-growing segment within the global fragrance industry. As mainstream markets become crowded, niche perfumery offers customised scent profiles, creative freedom and stories linked to origin or experience. Critical consumers are also willing to pay premium prices for exclusive, high-quality fragrances made with natural and traceable ingredients.

Scents are now being created with non-traditional essential oils, including botanical, fermented and wild-harvested raw materials. These ingredients are valued for their ability to evoke emotions, memories and places, adding a unique smell signature. Retailers more and more use fragrance to enhance customer engagement, especially through dedicated perfume shops and in-store customisation counters.

For example, the British personal care company Lush created a range of personal care products containing Indonesian patchouli oil. The patchouli scent evokes a strong cultural identity and is often associated with natural lifestyles and freedom, originally linked to the hippie movement of the 1960s.

The personalisation trend is also helping brands build stronger consumer loyalty. With rising interest in sustainability and wellness, and higher disposable incomes, the European fragrance market offers great potential for suppliers of niche essential oils.

The Fragrance Foundation plays an interesting role in promoting the fragrance sector internationally, supporting innovation, education and cultural engagement in perfumery. It encourages connections between producers, brands and institutions, helping to promote niche and artisanal fragrance creators. Exporters of natural ingredients can benefit from keeping an eye on the Foundation’s international activities, awards and trade events. This helps you better understand industry developments and opportunities within the French and wider European fragrance market.

Producers from LMICs can use this trend by offering unique oils with strong origin stories and high aromatic quality. Unlike in bulk markets, such as those for orange, lemon and peppermint oils, European buyers sourcing niche essential oils are more open to working with smaller suppliers and placing smaller minimum orders.

Tips:

- Familiarise yourself with fragrance and beauty trends. Good sources of information include Cosmetics Business, Premium Beauty News and perfumery blogs.

- Have a look at our CBI study on natural ingredient trends in the cosmetics sector to understand how suppliers from LMICs can position themselves successfully in the European market.

ProFound – Advisers in Development carried out this study on behalf of CBI.

Please review our market information disclaimer.

Search

Enter search terms to find market research

Do you have questions about this research?

We face a challenging period for the essential oils industry in Europe. Regulations are evolving, but so is our collective capacity to respond. By working together – producers, exporters, traders and associations actively participating in the dialogue with EU authorities – we can ensure that the unique value of natural essential oils is understood and protected with scientific collaboration and active engagement.

Andrey Mitov, President of the European Federation of Essential Oils (EFEO)

Webinar recording

Regulatory developments for essential oils in the European Union

27 February 2025