Entering the European market for vases

The European market for vases offers opportunities, but competition is strong. As mass-producing countries dominate the lower ends of the market, the mid-end segment is your best option – particularly the mid-high segment. To appeal to these consumers, you need to add value to your products through design, craftsmanship and sustainability. You must meet mandatory (legal) requirements, as well as any additional requirements your buyers may have.

Contents of this page

1. What requirements must vases comply with to be allowed on the European market?

The following requirements apply to vases in the European market. For a more detailed overview, see our study on buyer requirements for Home Decorations and Home Textile (HDHT).

What are mandatory requirements?

When exporting to Europe, you must meet the following legal requirements:

- General Product Safety Directive / General Product Safety Regulation;

- Restricted chemicals: REACH;

- Packaging legislation; and

- Intellectual property rights.

General Product Safety Directive / General Product Safety Regulation

According to the General Product Safety Directive (GPSD, 2001/95/EC), all non-food products marketed in the European Union (EU) must be safe to use. In April 2023, the European Council adopted a new regulation to replace the GPSD. This General Product Safety Regulation (GPSR, EU 2023/988) will ensure that products in the EU meet the highest safety requirements, whether sold online or in traditional shops. It came into force in June 2023 and will apply from December 2024 onwards.

Unsafe products are rejected at the European border or withdrawn from the market. The EU uses the Safety Gate system to list and share information about such products.

Tips:

- Read more about the General Product Safety Directive and the new General Product Safety Regulation.

- Make sure to meet the new General Product Safety Regulation by December 2024.

- Use your common sense to ensure that normal use of your product does not cause any danger.

- Search the Safety Gate alerts for vases and other objects made of your specific material for an idea of what issues may arise.

Restricted chemicals: REACH

The REACH regulation (EC 1907/2006) lists restricted chemicals in products that are marketed in Europe.

Restricted chemicals in the production of vases include:

- Lead in the paints and glazing of ceramics; and

- Arsenic and creosotes as wood preservatives.

Tips:

- Make sure you comply with the restrictions for the use of chemicals as laid down in REACH.

- Familiarise yourself with the full list of restricted substances in products marketed in Europe via the Access2Markets platform.

- For information and tips from the European Chemical Agency (ECHA), see for instance REACH Annex XVII (a list of all restricted chemicals), information for non-EU companies and questions & answers.

Packaging legislation

The EU’s Packaging Directive (94/62/EC) aims to prevent or reduce the impact of packaging and packaging waste on the environment. Buyers may therefore ask you to minimise the use of packaging and/or to use sustainable (recycled) materials.

The EU’s Circular Economy Action Plan identifies packaging as a sector that uses the most resources, with a high potential for circularity. By 2030, all packaging on the EU market should be reusable or recyclable in an economically viable way. To help achieve this, a new Packaging and Packaging Waste Regulation (PPWR) is in the works.

Europe also has requirements for wood packaging material and dunnage (WPM) used for transport, such as packing cases and pallets. The goal is to prevent organisms that are harmful to plants or plant products from entering and spreading within the EU.

Tips:

- For more information, see the EU’s packaging and packaging waste legislation and wood packaging material factsheet.

- Stay up to date on the proposal for a new regulation.

Intellectual property rights

When you develop products for the European market, you have to make sure you do not copy an existing design. So-called intellectual property (IP) is protected in Europe, and products that violate IP rights are banned from the market. For this reason, the European Commission adopted an IP action plan that should give European companies easier access to fast, effective and affordable protection tools.

Tips:

- For more information, see the European Union Intellectual Property Office (EUIPO) and the World Intellectual Property Office (WIPO).

- Keep track of developments in Europe via the state-of-play of the implementation of the key actions mentioned in the IP action plan.

What additional requirements do buyers often have?

Buyers often have additional requirements on sustainability, crystalline silica, labelling and packaging, and payment and delivery terms.

Be (more) sustainable

Social and environmental sustainability are becoming more and more common requirements in the European HDHT market. Environmental sustainability focuses on the impact your company has on the environment. Think of aspects such as the sustainability of your raw materials and production processes. For example, you can use renewable and sustainably produced natural materials and dyes to minimise your negative impact.

Social sustainability focuses on the impact your company has on the wellbeing of your workers and the community. Issues like fair wages and safe working conditions are key topics.

You can highlight your sustainable activities and policies in the ‘story’ behind your product and company. Buyers appreciate good storytelling so that their customers can get an emotional connection with your products.

Consumers value sustainability

The increasing importance of sustainability is reflected in a recent Maison et Objet Barometer, where 62% of HDHT retailers have noticed growing interest from their customers in ethical products. They indicate that 92% of their customers think natural materials are (very) important, 77% value socially responsible production methods, and 71% care about recyclable/recycled materials.

A growing number of European buyers would like you to comply with the following schemes:

- Business Social Compliance Initiative (BSCI): an initiative of European retailers to improve social conditions in sourcing countries. They expect their suppliers to comply with the BSCI Code of Conduct.

- Ethical Trading Initiative (ETI): an alliance of companies, trade unions and voluntary organisations. ETI aims to improve the working conditions in global supply chains via their ETI Base Code of labour practice.

- Sedex: a membership organisation striving to improve working conditions in global sourcing chains. The Sedex platform lets you share your sustainable performance, based on a self-assessment.

You can learn about sustainable options from standards such as ISO 14001 and SA 8000. However, only niche market buyers demand compliance with such standards.

Avoid greenwashing – be honest about your sustainability

Being honest about your sustainability is very important. Buyers and consumers must be able to trust you. However, companies often pretend to be doing more for the environment than they really are – so-called ‘greenwashing'. In a recent European screening of websites, national consumer protection authorities had reason to believe that many green claims were exaggerated, false or deceptive. This explains why Europeans do not have much faith in sustainability claims.

Sources that can help you communicate your sustainable performance honestly and effectively include:

- the guidelines regarding sustainability claims by the Netherlands Authority for Consumers and Markets

- the guidance for businesses on making environmental claims by the British Competition and Markets Authority

Tips:

- Optimise your sustainability performance. Study the issues included in the initiatives such as BSCI and ETI to learn what to focus on.

- If you can show your sustainability performance, this may give you a competitive advantage. You can use self-assessments like the BSCI Producer Self-Assessment, or a code of conduct such as the ETI Base Code of labour practice.

- For more information, see our special study on sustainability in HDHT.

- See the ITC Standards Map for more information on BSCI, ETI, Sedex and SA8000.

- For more information on European developments in the field of human rights and sustainability, see the proposal for a Directive on corporate sustainability due diligence. This Directive requires larger companies to identify and – where necessary – prevent, end or reduce negative impacts of their activities on human rights and the environment.

Handle crystalline silica with care

Respirable Crystalline Silica (RCS) can cause lung cancer through inhalation. The ceramics industry mostly uses crystalline silica in the form of quartz and cristobalite. If you work with ceramics, you should be aware that European buyers care about worker safety and may demand good handling of crystalline silica during production.

Tip:

- See the European Network on Silica for access to materials such as a Good Practice Guide.

Label products and packaging correctly

The information on the outer packaging should match the packing list sent to the importer.

Outer packaging labels for vases should include:

- Producer name;

- Consignee name;

- Quantity;

- Size;

- Volume; and

- Caution signs.

Your buyer will specify what information they need on the product labels or on the item itself, such as logos or 'made in…' information. This is part of the order specifications. In Europe, EAN or barcodes are commonly used on the product label.

Package your products properly

Importer specifications

You should pack vases according to the importer’s instructions. They have their own specific requirements for packaging materials, filling boxes, palletisation and stowing containers. Always ask for the importer’s order specifications. These are part of the purchase order.

Damage prevention

Proper packaging minimises the risk of damage caused by shocks. How an item is packaged for export depends on how easily it can be damaged. Packaging should make sure the items inside a cardboard box cannot damage each other. It should also prevent damage to the boxes when they are stacked inside the container. Packaging therefore usually consists of inner and outer cardboard boxes. The inner boxes are filled with protective materials or clever partitioning with corrugated cardboard.

If you produce wooden vases, you need to properly dry the wood after production to prevent mould or cracks. Condensation inside the container during transport can also cause mould. This is due to humid air that becomes colder at night and warmer during the day. Good air ventilation inside the container can prevent this, so you must inspect containers for air holes before shipment. You can also place products to reduce humidity amongst the cargo. Make sure to follow the importer’s instructions.

Dimensions and weight

Packaging must be easy to handle in terms of size and weight. Standards are often related to labour regulations at the point of destination and must be specified by the buyer.

Cost reduction

Boxes are usually palletised for air or sea transport, and you have to maximise the use of pallet space. Nesting or stacking can reduce costs. Consider this when designing your products.

Packaging has to provide maximum protection, but you must also avoid using excess materials or shipping ‘air’. Waste removal is a cost for buyers.

You can reduce the amount and diversity of packing materials by:

- Partitioning inside the boxes, using folded cardboard;

- Matching inner and outer boxes by using standard sizes;

- Considering packing and logistical requirements when designing your products;

- Asking your buyer for alternatives.

Material

Importers are increasingly banning wooden crating and packaging. Economical and sustainable packaging materials are more popular. Using biodegradable packing materials can be a market opportunity. Some buyers may even demand it.

Consumer packaging

Vases can be attractive gifts. Gift boxes are an option, especially where branding is important. Retailers and brands will then either request specific packaging design or take care of that themselves at destination. This generally depends on the cost involved and the quality of packaging you can offer.

Tips:

- Always ask for the importer’s order specifications, packaging and labelling requirements.

- See Packaging Europe for more information on the latest packaging developments, including regular news articles about biodegradable packaging.

Agree upon payment and delivery terms with your buyer

Payment terms are usually agreed upon with the buyer in the order contract. They vary from buyer to buyer and are related to the volume and value of the order, the type of distribution partner, whether or not an agent is involved, and what delivery terms apply.

Delivery terms, known as Incoterms, depend on the type of distribution partner and their preferences regarding physical distribution. HDHT importers generally prefer Free On Board (FOB) or Free Carrier (FCA) arrangements.

Tips:

- See our tips to organise your export for more information on payment and delivery terms.

- Study the different types of Incoterms, including what your and your buyer’s rights and obligations are.

- See our study on terms & conditions for a more elaborate overview, how to work with them, and the benefits of having your own.

What are the requirements for niche markets?

Fair-trade practices and sustainability certification are the most common niche market requirements.

Fair trade

The concept of fair trade supports fair pricing and improved social conditions for producers and their communities. Fair-trade certification can give you a competitive advantage, especially if the production of your items is labour-intensive. This certification often includes aspects of environmental sustainability as well.

Common fair-trade certifications are issued by the World Fair Trade Organisation (WFTO) and Fair for Life. For most fair-trade-oriented buyers in Europe however, simply complying with WFTO’s 10 principles of fair trade is enough.

Tips:

- Ask buyers what they are looking for. Especially in the fair-trade sector, you can use the story behind your product for marketing purposes.

- Determine which certification programme would be the best fit for you, and apply for it if you can.

- If certification is not feasible, work according to WFTO’s principles without being officially guaranteed or certified. Carefully document your company processes so you can support your story.

- Check the ITC Standards Map database for more information on Fair for Life.

Sustainable wood

FSC (Forest Stewardship Council) certification is the most common label for sustainable wooden products, including vases. FSC chain of custody certification guarantees that a product’s source material comes from responsibly managed forests. These products are especially popular in Western European markets. Non-timber forest products like rattan and bamboo can also be certified.

PEFC (Programme for the Endorsement of Forest Certification) is another option. Like with FSC, the PEFC chain of custody certification verifies that the forest-based material in a product comes from sustainably managed forests.

Tips:

- For more information on the application process, see the five steps towards FSC certification and/or how to become PEFC Certified.

- If you use recycled wood or paper, apply for the FSC Recycled label.

- Read more about FSC and PEFC in the ITC Standards Map.

2. Through what channels can you get vases on the European market?

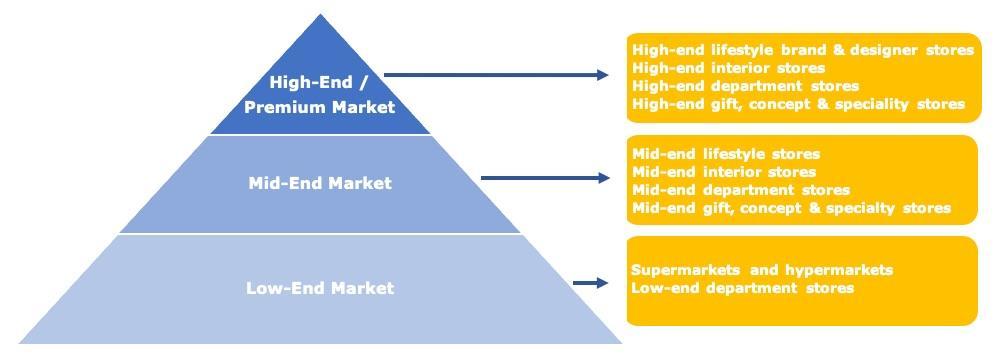

The European vase market is segmented into low-, mid- and high-end (premium) segments. The items are put on the market through the traditional channels: importers/wholesalers that supply to retailers, as well as retailers that buy directly from suppliers.

How is the end market segmented?

Figure 1: Vase market segmentation in Europe

Source: Globally Cool, GO! Good Opportunity & Remco Kemper

Low-end market

The low-end market contains everyday basics. Vases in this segment are functional, affordable and often sold in sets. They are easily available from general interior stores like IKEA and hypermarkets such as Carrefour. This market is dominated by mass-produced items from countries such as China, which are hard to compete with. Instead, the (higher) mid-end market offers you the most opportunities.

Mid-end market

Vases in the mid-end market are trendy. They come in familiar shapes at friendly prices. Designs for this segment generally focus on decorative aspects such as shape, decoration and colour. Especially in the mid-high segment, where there is a market for (semi‑) handmade items, design and craftsmanship are more prominent and innovative. Sustainable values and the story behind your products also increasingly appeal to consumers in the mid-end market. Examples of retailers in this segment are Zara Home and Habitat.

High-end/premium market

The high-end/premium segment is much smaller, as the commercial market for vases usually ends at mid-high. This luxury top segment is characterised by premium materials, such as crystal or aluminium. The vases are often handmade, using intricate techniques, with innovative shapes. Heritage brands and top-end designers play an important role in this market, which includes timeless ‘modern classics’ such as Iittala’s Aalto vases.

Figure 2: Iittala – glass Iittala x Issey Miyake and Aalto vases

Source: Iittala @ YouTube

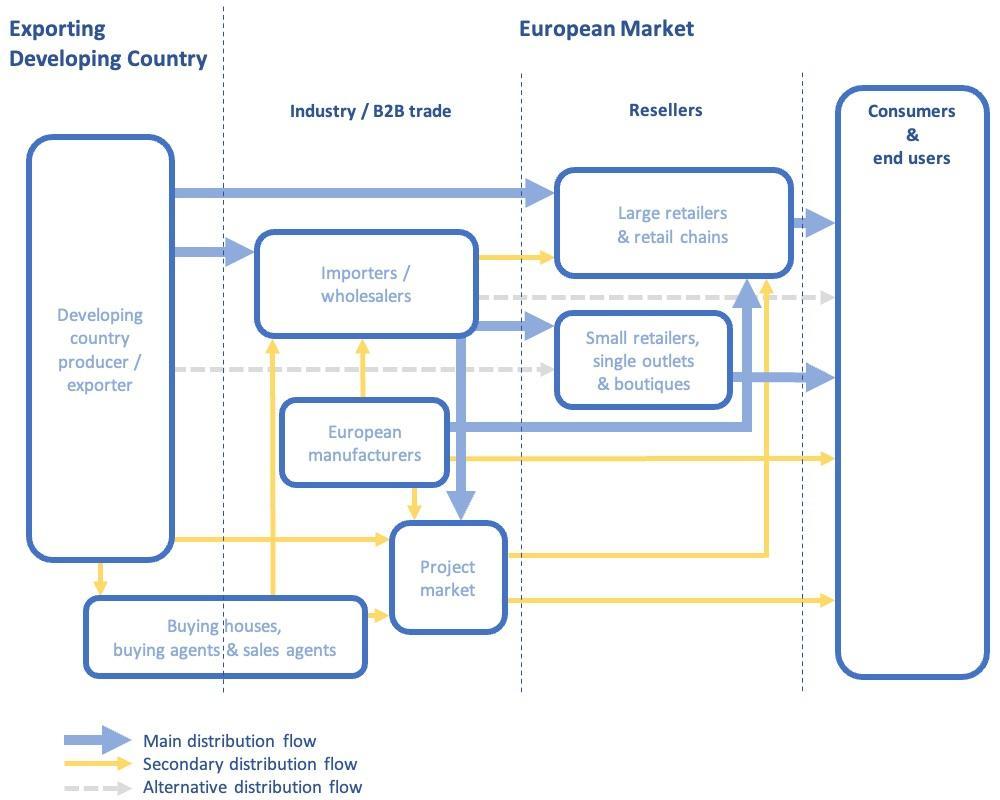

Through what channels do vases end up on the end market?

The channels through which vases are put on the market follow the traditional HDHT patterns: import takes place via importers/wholesalers that supply to retailers. Larger retail chains often bypass the importers/wholesalers and import themselves, while more and more smaller retailers have also started buying directly from the supplier. In some cases, buying agents play a role.

Figure 3: Trade channels for vases in Europe

Source: Globally Cool, GO! Good Opportunity & Remco Kemper

Importers/wholesalers

Importers/wholesalers sell products to retailers in their own country or region, or re-export across Europe. Some European markets are therefore supplied by wholesalers/importers from other European countries (internal European trade). Supplying to buyers in the project market (such as hotels and spas) can be considered as a secondary distribution flow for European importing wholesalers.

These importers/wholesalers handle the import procedures. They take ownership of the goods when they buy from you (as opposed to agents), taking on the risk of the onward sale of the products. Developing a long-term relationship can lead to a high level of cooperation on appropriate designs for the market, new trends, use of materials, type of finishing, and quality requirements.

Importing retailers

Retailers come in many sizes: large and part of a chain, or small and independent. Especially larger retail chains often import directly from their suppliers in developing countries. Many even have their own buying offices in developing countries. Others – mainly the smaller independent stores – order in Europe from wholesalers.

There is a tendency towards consolidation in European retail. Large retail brands are becoming more widespread and more ‘lifestyle-centred’, offering home decoration and textiles as well as fashion accessories and furniture.

Buying agents, buying houses and sales agents

You can encounter several types of intermediaries when doing business with European buyers:

- European buying agents represent European buyers in sourcing countries. They act as intermediaries, meaning they do not import products themselves. Sometimes they have a more limited role, such as checking the quality of the products. They can work individually or as part of a purchasing company.

- Buying houses are comparable to buying agents, but they are based in your country and usually offer more services. These can range from raw material sourcing to design and sampling services.

- European sales agents can help you find European buyers. However, you should be careful before entering into agreements with commercial agents, because European legislation protects their position.

Agents and buying houses mostly work on commission. They may approach you directly, or your buyer may indicate that they prefer to use an intermediary. However, you should always try to work directly with your buyer. This saves on commission and allows you to communicate with your buyer directly.

E-commerce

E-commerce has grown in recent years. It became particularly popular during the pandemic, which drove consumers to buy their HDHT products online. Your best way to benefit from this is by supplying to a European wholesaler or retailer with a strong online presence. For most producers, this is not a separate channel. Retailers often combine online and offline channels, but the way of supplying to them is the same. Companies that only sell online also need to take stock before they can sell.

Direct business-to-consumer (B2C) sales

Selling directly to European consumers via your own website can be complicated and costly. You are responsible for factors like aftersales obligations and payment systems for consumer use. For most exporters from developing countries, this is not feasible. In addition, according to Dutch consumer association Consumentenbond Dutch consumers buy less from non-EU web shops since new EU VAT rules were rolled out in July 2021. This makes direct online sales even less attractive.

Tips:

- To find potential buyers, search the list of exhibitors or attend the main physical or online trade fairs in Europe: Ambiente (February) in Frankfurt and Maison et Objet (January and September) in Paris.

- See our tips for finding buyers in the European HDHT market.

- For more information about trading directly with smaller retailers and e-commerce, see our study about alternative distribution channels.

What is the most interesting channel for you?

The most interesting trade channels for you are importers/wholesalers and importing retailers.

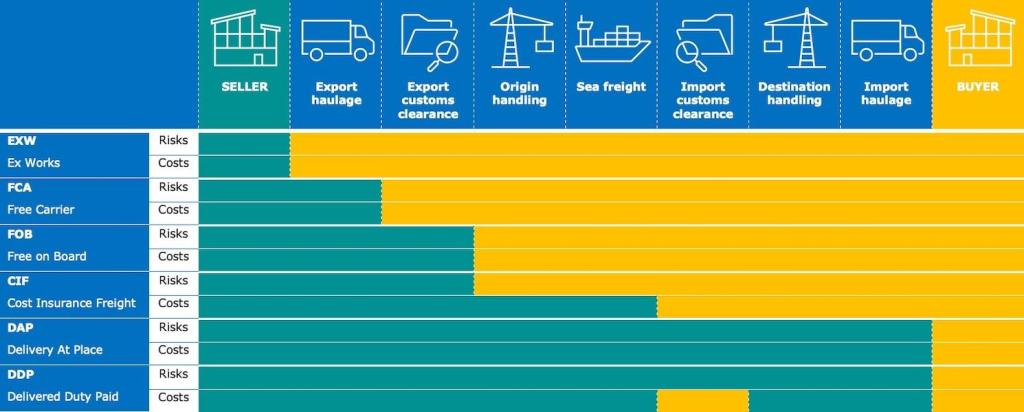

Importers/wholesalers are the main channel between exporters in developing countries and European retailers. They are interesting if you want to develop a long-term relationship. These importers usually know the European market well, so they can provide you with valuable information and guidance on market preferences. They generally prefer Free on Board (FOB) or Free Carrier (FCA) Incoterms.

Figure 4: Incoterms

Source: Globally Cool, GO! Good Opportunity & Remco Kemper

Large retailers are increasingly importing for themselves instead of through importers/wholesalers. The obvious advantages are cutting out the margins of the wholesaler and reducing delivery time to the market. In the lower-end market segments, self-importing retailers might want to drive a much harder bargain with you to keep prices as low as possible. However, price is a bit less sensitive in the mid-high segment, so that segment offers you the most opportunities.

Smaller, independent retailers continue to buy mainly from domestic importers/wholesalers. But, as in other sectors, independent HDHT retailers struggle to compete with retail chains. They need to differentiate on value-added service, specialised offers and authenticity. An interesting way for them to do so is by buying directly from producers in developing countries. They typically prefer small order quantities per item, small total order volumes and delivery to their doorstep via Delivered Duty Paid (DDP) or Delivery At Place (DAP). Repeat orders are less likely.

The trend of direct sourcing is expected to continue and may create more opportunities for you. The pool of buyers grows if more retailers become importers, which could improve your bargaining position. Importing retailers order for their own shops and can therefore place orders much more quickly than some importers/wholesalers, who may need to show samples to their retailers before ordering. You need to calculate if trading directly with (smaller) retailers is cost-effective for you.

Tips:

- Consider targeting retailers directly to improve your bargaining position and potentially close deals faster.

- Relate your offer and terms to the targeted retailer (large/small). Ask your existing buyers how they operate if you are unsure. The better informed you are, the better you will be able to set prices.

- Build a relationship based on mutual benefits by offering services such as fast delivery and after-sales support.

- If you are interested in selling to small independent retailers, make sure to have a policy for them when you participate in international (European) trade fairs. You must have appropriate terms of trading, such as low minimum order quantities or pre-stocking.

3. What competition do you face on the European vases market?

Europe’s leading supplier of the product groups that include vases is China. A lot of these supplies consist of mass-produced items for the lower-end segments. Instead of competing with these manufacturers, your best opportunities are in the (higher) mid-end market, where you can add value.

Because no specific trade data are available for vases, these statistics cover various related HS-codes for decorative objects and glassware in general.

China is by far the main supplier of the product groups that include vases to Europe, providing 49% of the imports. Germany follows at a distance with 7.6%. Next on the list are France (5.6%), the Netherlands (4.6%), Spain (4.0%) and Vietnam (3.9%).

Re-exporters or producers

European countries have different roles in the HDHT market. Some are mainly importers and others are mainly manufacturers. Western European countries are mainly importers, and most Western European importers are re-exporters. They do not just sell their products in their own country, but they distribute them across the continent.

European production mainly takes place in Eastern Europe, mostly because of relatively low transport and labour costs. This can make these countries a good alternative for European buyers to source low- to mid-end products. Western and Southern Europe also produce some high-end products from well-known premium brands with a long history.

Which countries are you competing with?

Source: UN Comtrade

China dominates the (low-end) market

China is by far the leading supplier of the product groups that include vases to Europe. Its supplies grew from €1.6 billion in 2018 to €2.3 billion in 2022. The country mainly supplies the lower-end market with low-priced vases. This is reflected in the fact it supplies nearly three-quarters of Europe’s total imports of plastic products in this group, representing about a third of China’s supplies. About a quarter of China’s supplies are ceramics. The country has become the ceramic ‘factory of the world’, handling the production of many European brands.

China is a competitive supplier of vases because of its large-scale and highly mechanised production systems, low-cost workforce, availability of raw materials, and efficient shipping to Europe compared to other Asian countries. However, the country’s rising labour costs in the last 10 years have affected its price competitiveness. In the coming years, China’s trade war with the United States and other disruptions may affect the country’s exports. European importers also want to become less dependent on China as a single supplier. This could benefit companies from other developing countries, like you.

Smaller importers increasingly look for second sources in Asia, such as Vietnam, India, Indonesia or Thailand. This also goes for those importers whose designs require some handwork. To avoid having to compete with Chinese suppliers on cost, you should stay away from mass-produced vases. Instead, focus on innovative design, sustainability, (natural) materials and the story behind your product to enter the mid-end market, where your best opportunities are.

Vietnam is another low-cost producer

Like suppliers from China, Vietnamese manufacturers are very productive and can produce at low cost. Their exports of the product groups that include vases to Europe grew from €99 million in 2018 to €182 million in 2022, at an average annual rate (CAGR) of 17%. With this, the country’s import market share increased from 2.9% to 3.9%. Most of these items are ceramics.

Vietnamese suppliers generally have a good idea of what is commercial and trendy. They effectively combine handmade and mechanised production, are well-known for their interesting ceramic and lacquerware vases and containers, and can cater to a wide range of lower- and mid-end markets. As such, they have been an effective second-sourcing alternative to suppliers from China for several years now. Vietnamese producers are also increasingly adopting environmentally sustainable practices in the production of vases.

India maintains its market share

With skilled labour and transport at competitive costs, India could be well-positioned to take a bigger share of the market. After a dip in 2020, Indian supplies of the product groups that include vases to Europe reached €138 million in 2022. This translates to a CAGR of 9.2% between 2018 and 2022, resulting in a fairly stable import market share of about 3%. These supplies mainly consist of metal items.

India has a rich craft culture, with an abundance of producers and easy access to natural materials. This allows them to target higher market segments than the mass-produced products from China. India also increasingly offers an effective combination of handmade and more mechanised production techniques. As it becomes more difficult for buyers to order short runs from China, India is becoming a popular alternative. Especially since European lifestyle buyers already source broad HDHT collections from India and are increasingly able to do one-stop shopping due to the country’s rich craft culture.

Poland keeps its position as a regional supplier

As an Eastern European country, Poland benefits from its closeness to the Western European market. This allows suppliers to offer short delivery times. At the same time, labour is relatively affordable compared to Western Europe. Suppliers have a good understanding of the European consumer and have well-established and efficient production lines. In addition, products that are ‘Made in Europe’ are increasingly popular.

Poland steadily increased its exports of the product groups that include vases to Europe, until they peaked in 2021. As a result, they grew from €76 million in 2018 to €100 million in 2022. This translates to a CAGR of 6.9%, as Poland’s share of the European import market returned to 2.2%.

Around two-fifths of Polish supplies of the product groups that include vases to Europe are made of glass, and about one-fifth are plastic items. Polish manufacturers of vases mainly compete in the more price-sensitive lower- and lower-middle ends of the market. Instead, you should focus on mid-high segments and upwards through special design value, craftsmanship, natural and sustainable materials, and interesting maker and making stories. Make sure you offer a high level of service to build strong, lasting relationships.

Portugal specialises in ceramics

Portugal’s key strengths are stoneware and earthenware. Its supply is backed by hundreds of years of experience, innovative designs and quality styling. As such, Portuguese ceramic suppliers have become key players in the more rustic, ‘country’ styles for the mid- and high-end segments of the European market. They can serve as a good example of how to use specific elements of your original (ceramics) culture such as colour, raw material and craftsmanship.

Portuguese supplies of the product groups that include vases to Europe grew from €60 million in 2018 to €73 million in 2022, at a CAGR of 5.3%. This translates to an import market share of 1.6%.

Turkey is conveniently located

Like Poland, Turkey has the advantage of being located close to the European market. Its supplies of the product groups that include vases to Europe have come back strongly after the trade disruptions of 2020. This led to an increase from €53 million in 2018 to €71 million in 2022, at a CAGR of 7.5%. This resulted in a direct import market share of 1.5%. Most of these supplies are made of glass.

The country still has to find its place in the market for vases and discover whether its positioning should be on price/volume or more on design value. To compete with this relative newcomer, you should focus on your own unique strengths and occupy the right niches before others do.

Which companies are you competing with?

Poterie Serghini – Morocco

Family business Poterie Serghini produces handmade Moroccan ceramics in Safi, a city renowned for its pottery. The company’s ceramic production is based on traditional skills that have been perfected by 8 generations of master ceramists. Their items are made from locally sourced natural clay and hand-decorated with lead-free glazes. The unique designs are “inspired by nature, the cultural symbols of Morocco, [and] the personal history of the craftsman”.

Poterie Serghini is committed to the principles of fair trade, striving to improve the quality of life in the artisan community. They offer a wide range of ceramics, from vases and planters to tableware and bathroom accessories, in traditional and modern styles. The items can be personalised, and customised in different combinations of colours, sizes and patterns.

Figure 6: Poterie Serghini – The fabulous story of Poterie Serghini

Source: Poterie Serghini @ YouTube

Artex Nam An – Vietnam

Vietnamese supplier Artex Nam An focuses on renewable natural materials that are fast-growing, biodegradable and recyclable. Their vases are made from bamboo, sometimes combined with seagrass. The company was founded in 2013, with the ambition to “make life more eco-friendly globally and better the lives of Vietnamese farmers and artisans”. Their products are ethically sourced from more than 20 local factories, most of which are BSCI-certified.

Besides its catalogue of ready-made (customisable) products, Artex Nam An offers solutions in sourcing, manufacturing, product design and development, and consulting. Their website lists a step-by-step process for each of these services.

Arfai – Portugal

A good example of your Portuguese competition is Arfai, with their mission “to produce high-end contemporary decorative ceramics items of unique added value, inspired by the art and tradition of ceramics manufacture”. The combination of traditional and modern is reflected in shapes and techniques, ranging from hand-painting to reactive glazes and metallic lustres. An R&D team keeps designs aligned with international trends. At the same time, Arfai provides bespoke private label services, from the design concept to production and the final packing and loading.

Arfai’s dedicated webpage about their commitment to sustainability conveys a good understanding of this important topic. It emphasises transparency, and the company’s efforts to be both environmentally and socially responsible. Highlights include the use of locally sourced raw materials, the company’s Waste Water Treatment Plant and Self-Consumption Production Unit for renewable energy, and several successful Sedex Members Ethical Trade Audits. Arfai’s new ‘Ecofai’ material is made from recycled ceramic waste.

Figure 7: Arfai – Sustainability

Source: Arfai @ YouTube

Which products are you competing with?

Your competition mainly comes from vases of different materials – such as glass, ceramics or natural fibre – and vases with different levels of quality and different designs. Consumers are also increasingly interested in socially or environmentally friendly produced vases.

Tips:

- Compare your products and company to the competition. You can use ITC Trade Map to find exporters per country and compare on market segment, price, quality and target countries.

- Focus on design, craftsmanship, quality and the story behind your products to stand out from your competitors.

4. What are the prices for vases on the European market?

Prices for vases vary across market segments, ranging from low-end to high-end. After adding logistics costs, wholesaler and retail margins and Value Added Tax (VAT), European consumer prices amount to about 4-6.5 times your selling price.

Table 1 gives an overview of the indicative prices of vases in the low, middle and high market segments. Be aware that these are just an indication, since prices vary depending on technique, size, material, design, brand and other ways of value addition, including a strong sustainable concept.

Table 1: Indicative consumer prices of vases in Europe

|

|

Low-end |

Mid-end |

High-end |

|

Ceramic or glass vase, 25cm high |

Up to €15 |

€15 to 50 |

€50 and over |

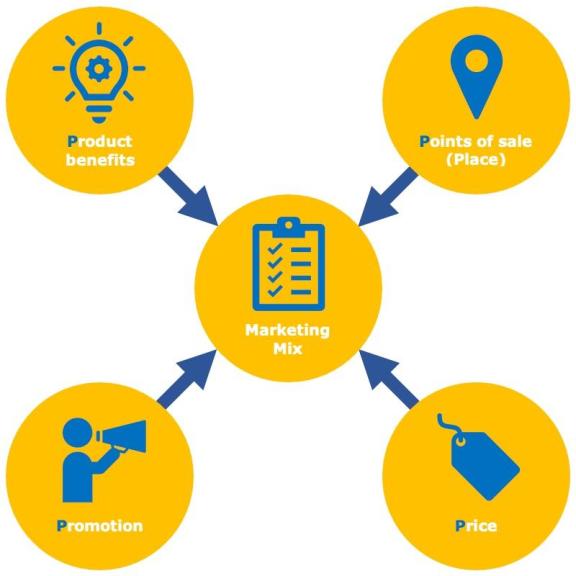

Consumer prices depend on the value perception of your product in a particular segment. This is influenced by your marketing mix.

Figure 8: Marketing mix – the 4 Ps

Source: Globally Cool, GO! Good Opportunity & Remco Kemper

The European consumer price of your product is about 4-6.5 times your FOB price. Besides energy, labour and transport costs, FOB prices depend heavily on the availability and cost of raw materials. Occasional cost increases are not directly passed on to the consumer, so they put pressure on the margins of exporters, importers and retailers. However, recent disruptions resulted in longer-term cost increases. This continuing pressure made many retailers raise their consumer prices. Now that costs like shipping rates are dropping again, consumer prices may follow.

Consumer prices generally consist of:

- Your FOB price;

- Shipping, import, handling costs;

- Wholesaler margins;

- Retail margins; and

- VAT – varies per country, about 20% on average.

Figure 9: Price breakdown indication for vases in the supply chain

Source: Globally Cool, GO! Good Opportunity & Remco Kemper

For example, in Table 2 the FOB price is set at €10. Depending on the market segment your product is designed for, the consumer price ranges from €41 in the low-end market to €65.50 in the high-end market.

Table 2: Example of the price breakdown per market segment

|

|

Low margin |

Middle margin |

High margin |

|

|

FOB price |

€10.00 |

€10.00 |

€10.00 |

Your FOB price |

|

Transport, handling charges, transport insurance, banking services (20/15/15%) |

+2.00 €12.00 |

+1.50 €11.50 |

+1.50 €11.50 |

Landed price for the wholesale importer |

|

Wholesalers' margins (50/75/90%) |

+6.00 €18.00 |

+8.60 €20.10 |

+10.40 €21.90 |

Selling price from the wholesale importer to the retailer |

|

Retailers' margins (90/110/150%) |

+16.20 €34.20 |

+22.20 €42.30 |

+32.70 €54.60 |

Selling price excluding VAT from the retailer to the end consumer |

|

Selling price incl. VAT (20%) |

+6.80 €41.00 |

+8.50 €50.80 |

+10.90 €65.50 |

Selling price including VAT from the retailer to the end consumer |

The FOB price of €10 includes your own margins as a producer. These margins depend on your efficiency and price setting. Margins in the lower segment, which deals with high volumes for low prices, are generally smaller than those in the middle and higher segments.

Some examples of vase prices across Europe are:

- recycled glass vase, HEMA, €17

- hand-carved mango wooden vase, SKLUM, £22.95

- hand-glazed stoneware vase, Motel a Miio, €69

Tips:

- Study consumer prices in your target segment to determine your price and adjust your cost accordingly. The quality and price of your vases must match what is expected in your chosen target segment.

- Calculate your prices regularly and carefully, especially if prices of your raw materials fluctuate. When raw material prices pressure your margin for a longer period, consider increasing your price or finding an alternative.

- Understand your segment. Offer a correct marketing mix to meet consumer expectations. Adapt your business model to your position in the market.

Globally Cool B.V. in collaboration with GO! GoodOpportunity carried out this study on behalf of CBI.

Please review our market information disclaimer.

Search

Enter search terms to find market research