The United Kingdom’s market potential for coffee

The United Kingdom ranks among the largest European coffee-consuming markets. Within Europe, the United Kingdom is a key market for certified coffees. British in-home consumption is still dominated by the sale of instant coffees, but higher-quality coffee pods and ground coffee are gaining popularity. The popularity of higher-quality and specialty coffees is also driven by the enormous coffee shop market in the country.

Contents of this page

1. Product description

Harmonised System (HS) codes are used to classify products and to calculate international trade statistics, such as imports and exports. The focus in this study is on green coffee beans, which are classified in HS codes 090111 (coffee, not roasted, not decaffeinated) and 090112 (coffee, not roasted, decaffeinated). The available data do not distinguish between bulk, high-quality and specialty coffees.

Approximately 124 coffee species exist in the wild, of which only a few are commercially relevant. The two most important species on the market are:

- Coffea Arabica (Arabica): Referred to as a highland coffee, because it grows best at altitudes between 600 and 2,000 metres, Arabica is the most dominant species in the coffee market, representing about 75% of global coffee production. Each coffee tree yields an average of two to four kilos of cherries. Arabica beans are fairly flat and elongated. Arabica coffee beans have a smoother, more aromatic and more flavourful taste compared to Robusta. Arabica beans have a caffeine content of approximately 1.5%.

The main sub-varieties of Arabica are the Yemen accession, which branches out into Typica and Bourbon coffee lineages and the Ethiopia/Sudan accession.

Examples of Typica cultivars are the Hawaiian Kona, Jamaican Blue Mountain, SL14 and Maragogipe. Examples of the Bourbon cultivars that are found mostly in Latin America are Caturra, Villa Sarchi and Pacas. Examples of Bourbon cultivars found in East Africa are Jackson, K7, SL28 and SL34.

Examples of the Ethiopian and Sudanese cultivars are Geisha, Java, Sudan Rume and Tafari Kela. - Coffea Canephora (Robusta): Robusta coffee can be considered a lowland coffee, as it grows best at altitudes below 600 metres. Robusta accounts for around 25% of global coffee production. Its beans have a caffeine content of approximately 2.7%. Robusta is less susceptible to pests and diseases than Arabica. Its beans are smaller and rounder than Arabica beans. When roasted, Robusta beans generally have a stronger and harsher taste than Arabica, and it is often described as bitter. Robusta beans are often used in coffee blends and instant coffee.

Examples of crossbreeds of the Arabica and Robusta species are Catimor, Castillo (the most commonly coffee plant grown in Colombia), IHCAFE90, Ruiru 11 and Sarchimor.

2. What makes the United Kingdom an interesting market for coffee?

Although per capita coffee consumption in the United Kingdom is relatively low, the country ranks among the largest European coffee-consuming markets. Out-of-home consumption is an important segment for coffee sales in the United Kingdom and is an important driver for the growing interest in specialty coffees. The largest European branded coffee shop market can be found in the United Kingdom.

United Kingdom is among Europe’s largest importers of green coffee

The United Kingdom imported about 148,000 tonnes in 2021, making it Europe’s eighth-largest green-coffee importer. About 96% of British green coffee imports are sourced directly from producing countries, making up 4.1% of Europe’s total imports in 2021. Between 2017 and 2021, the United Kingdom’s direct import volumes decreased by 2% per year, on average.

Green coffee beans enter the United Kingdom mainly through the Port of Tilbury and the Port of Liverpool. Examples of large-scale importers in the United Kingdom include ED&F Man Volcafe, Olam Food Ingredients and ECOM. Examples of specialty coffee importers include Mercanta The Coffee Hunters, Olam Specialty Coffee (Schluter), DR Wakefield and Falcon Coffees.

The decrease in imports since 2019 is related to the effects of the COVID-19 pandemic. See the trend section below to read more about the impact of Brexit on green coffee imports by the UK, which has been limited.

The United Kingdom is Europe’s fifth-largest coffee market

Once known as a traditional tea-drinking nation, the United Kingdom has become one of the largest coffee consuming countries in Europe in recent years. The United Kingdom is among the larger coffee markets in Europe; other large coffee markets in Europe are Germany, Italy, France and Spain. The British coffee market consumed nearly 175,000 tonnes from June 2020 to June 2021. Between June 2017 and June 2021, the coffee market in the United Kingdom annually decreased by 6.3%.

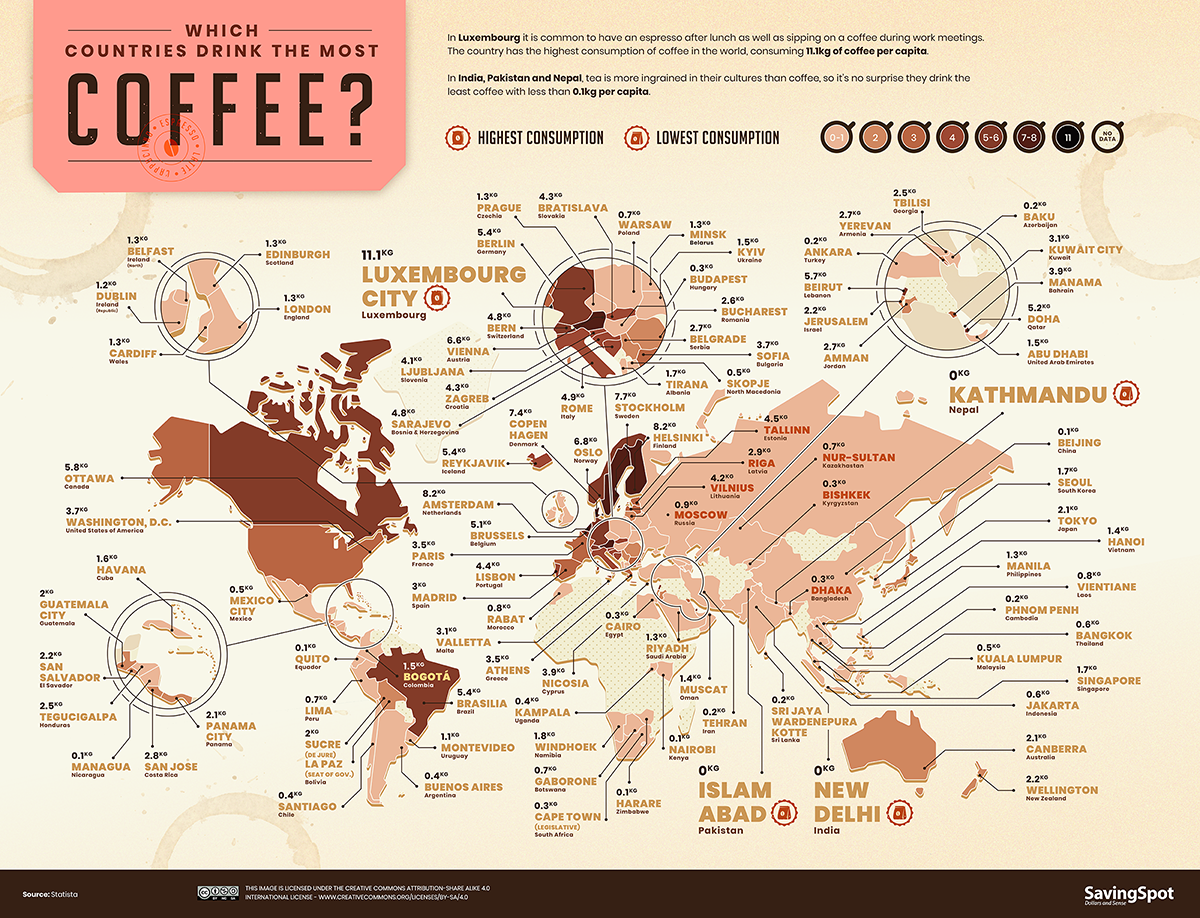

According to the British Coffee Association, British consumers drank approximately 98 million cups of coffee per day in 2021, which marks an increase of 28 million compared to 2008. A survey from 2021 showed that 70% of British consumers drink at least two cups of coffee per day. Despite the size of the market, per capita consumption of coffee in the United Kingdom is relatively low, at around 1.3 kg - 2.9 kg of coffee per year. This is much lower than the European Union’s average of 5.2 kg per year.

{kind=link}

The United Kingdom has an enormous coffee shop market

The total number of coffee shops in the United Kingdom totalled 9,540 outlets across the branded segments, and registered a growth rate of 3.5% in 2021. This makes the United Kingdom Europe’s largest branded coffee shop market, followed by Germany. In 2021, the leading coffee shop brand in the United Kingdom was Costa Coffee, with 2,791 shops, followed by Greggs with 2,176 shops, and Starbucks with 1,089 shops. Within the United Kingdom, the coffee shop segment is considered one of the most resilient economies in the country.

In 2020, due to the global COVID-19 crisis, the British branded coffee shop market declined at a rate of nearly 40%. The crisis has mainly impacted out-of-home coffee segments worldwide, and in the United Kingdom many consumers prefer to drink tea at home, which explains this sharp decline. However, demand in the coffee market has picked up again now that the worst effects of the crisis have passed. The British brand coffee shop market grew by 43% in 2021, reaching 87% of its value before the global COVID-19 crisis. Allegra World Coffee Portal forecasts that the long-term outlook for British coffee shops remains positive, with pre-pandemic sales likely to be surpassed by the end of 2023.

The World Coffee Portal expects the branded coffee shop market to grow at an average annual rate of 5.8% until 2026. In its shift from a tea to coffee-consuming country, the United Kingdom has seen a growth in coffee shops for several years. In recent years, market leaders such as Costa Coffee and Starbucks have opened drive-through stores. The number of outlets is expected to exceed 10,500 by 2026.

Growth rates for the independent coffee shop market were predicted to be slightly higher, with the value expected to rise by 25% in 2022. This is driven by the growth in hybrid working. Furthermore, a survey from 2021 showed that 65% of consumers would visit an independent coffee store to support them after the COVID-19 crisis, and also because of the quality of their products. The segment value of independent coffee shops is expected to reach £1.6 billion (approximately €1.9) in 2022.

The size and growth of the coffee shop market drives the growth of the specialty coffee market in the United Kingdom. Read more about this in the trend section below.

Tips:

- Activate the “Translation” function of your browser to make the studies available in your native language.

- See the website of the British Coffee Association for more information about the coffee industry in the United Kingdom.

- Access EU Access2Markets to analyse European and British trade dynamics and to build your export strategy. By selecting the United Kingdom as your reporting country, you will be able to follow developments such as trade flows with established suppliers, the emergence of new suppliers and changing patterns in direct and indirect imports.

- See our study of trade statistics for coffee for more detailed information about the European trade in green coffee beans.

- Refer to this list of coffee roasters in the United Kingdom and Ireland, as it gives a good idea of the profiles of British coffee roasters.

- Refer to Allegra World Coffee Portal to read more about the coffee market in the United Kingdom.

3. Which trends offer opportunities in the British market?

Sustainability is a leading consumer trend in the United Kingdom, as the country is an important market for certified coffees. The United Kingdom is a leading European market for both Rainforest Alliance and Fairtrade-certifications. Although in-home coffee consumption is still largely dominated by the sale of instant coffee, coffee pods and ground coffee are gaining ground. This trend is mainly driven by the younger generations, which are increasingly interested in higher-quality coffees. Specialty and ready-to-drink coffees are gaining popularity for out-of-home consumption.

Sustainability plays a major role in the British coffee sector

Sustainability concerns are seen as the most important consumer trend affecting the British coffee sector in 2021. Environmental sustainability, recyclable packaging materials and utensils, and traceability are listed as main concerns of British coffee consumers.

It is no surprise that sustainability certifications are well-established on the British market. The United Kingdom has the largest number of Rainforest Alliance/UTZ coffee retailers in Europe, including Costa Coffee, JD Wetherspoon, Benugo, as well as retailers Tesco, Marks & Spencer and ASDA.

The United Kingdom is also one of the largest markets for Fairtrade-certified products and coffee. Almost 25% of total coffee sales in the United Kingdom is Fairtrade certified coffee. Sainsbury’s, Waitrose and Marks & Spencer are examples of British retailers that converted their entire private label coffee lines to 100% Fairtrade. Greggs, the largest bakery chain in the United Kingdom, drove up growth in Fairtrade coffee sales in the out-of-home segment.

In 2020, the volume of Fairtrade coffee decreased by 28%. However, Fairtrade coffee sales in the United Kingdom still helped to generate over £6.7 million Fairtrade Premiums for certified coffee producers, which was around 4% of the total worldwide Fairtrade Premiums received by producers. Fairtrade Premiums are invested in farmer services and community projects in coffee producing countries.

The United Kingdom also offers a large market for organic coffee. The United Kingdom is the fifth-largest market for organic foods in Europe. The organic market amounted to £2.8 billion in 2021, registering 12.6% market growth from 2020. Companies in the United Kingdom dealing exclusively in organic coffee include Beanberry Coffee Company and Green Bridge Organics.

The British market is also open to lesser-known certification schemes such as Bird Friendly-certified coffee. British Bird-Friendly certified coffee roasters include Bird & Wild, Cafeology and Masteroast. Note that Bird Friendly-certified coffees belong to a very small niche market.

Examples of coffee exporters that clearly communicate on the sustainability practices of their business are O’Coffee (Brazil) and Cedro Alto (Colombia). Another example is Peruvian company Rainforest Trading, which offers coffees certified by various schemes, including Bird-Friendly.

The United Kingdom is a booming specialty coffee market

Both branded and independent coffee shops and roasters define the specialty market in the United Kingdom, as such the specialty coffee market is highly influenced by out-of-home consumption. Pre-COVID levels of out-of-home consumption accounted for 39% of total coffee consumption, leaving the other 61% to drinking at home. The value of out-of-home consumption in the United Kingdom has fallen by 43% due to COVID. By comparison, the European average for out-of-home consumption sales fell by 56% in 2020.

About 15% of out-of-home coffee consumption is estimated to be specialty graded. In 2019, the United Kingdom counted a total of 25,892 coffee shops, of which 1,400 were categorised as specialty coffee shops. Examples of these shops include Small Batch Coffee Roasters, Union Brew Lab, Caravan Coffee Roasters, Wood Street Coffee and Redemption Roasters. These shops roast and serve their own specialty coffees.

Although London hosts one of the United Kingdom’s main coffee festivals, and is said to have become the European heart of specialty coffee, the British specialty market reaches far beyond the country’s capital. Many other cities host coffee festivals, which have become an important platform for specialty coffee houses and roasters, including Manchester, Edinburgh, Glasgow, Birmingham and Kent. There is also a nationwide coffee festival: the UK Coffee Week.

Growth of single-serve coffee pods, but instant coffee still popular

Compared to most other European countries, British coffee consumers drink relatively large amounts of instant coffee. A recent survey stated that up to 73% of British households prefer instant coffee for in-home consumption in 2021, particularly older generations. In 2018, the volume share of instant coffee even reached 41% of the entire British market. To compare, the average volume market share of instant coffee in Europe is 17%. The instant coffee market in the United Kingdom is expected to grow in value by 7.2% each year until 2025.

On the other hand, single-serve pods are gaining popularity on the British coffee market. The United Kingdom has the largest single-serve pods market share after Switzerland and Germany. In 2018, coffee pods made up 13% of the entire British coffee market, a 3% increase from 2016. An estimated 12.6 million British households owned a coffee pod machine in 2018, amounting to 46% of total households in the United Kingdom that year. Research has indicated that there is still ample room for coffee pods growth in the United Kingdom.

The growing sales for coffee pods is largely driven by Gen Z and Millennials that are willing to spend more on more expensive coffee products, like pods. The ease-of-use of these products, the strong marketing and the wide variety of flavours have contributed to the growing sales of this segment. Within the single-serve market there is also a growing offer of specialty coffee capsules. Examples in the United Kingdom include Sendero Specialty Coffee, Colonna Coffee and Halo Coffee.

On the other hand, the downside of coffee pods is the negative environmental impact. As environmental concerns are a main trend driving the British coffee industry, several United Kingdom-based coffee companies have introduced recyclable and compostable solutions and alternatives. Examples include Roar Gill, Cru Kafe and Grind.

Ready-to-drink coffees are growing in popularity in the United Kingdom

Ready-to-drink (RTD) coffees have become increasingly popular across the United Kingdom. In 2021, the British ready-to-drink coffee market increased in value by 37%. Today, RTD coffees are widely for sale in branded coffee chains, independent coffee houses and supermarkets. The convenience of RTD coffees and their perceived health aspects (as an alternative to sodas) are driving this trend.

The RTD market in the United Kingdom is quite consolidated, with large players such as Starbucks, Coca-Cola (which owns Costa Coffee), Caffé Nero and Lavazza dominating the segment. The British RTD coffee market is expected to see annual growth of 2.4% from 2022 to 2027.

Within the RTD segment, cold brewed coffee is gaining popularity. British brands offering cold brew RTD include Sandows, Union Hand Roasted Coffee and Minor Figures. Also, plant-based RTD coffees have been introduced by brands like Starbucks and Califia Farms, to meet growing consumer demand for vegan alternatives

Brexit has affected the British coffee industry in many ways, but not its direct imports

The United Kingdom's decision to leave the European Union has had an impact on the national coffee sector. Trade relations with the European Union have weakened and trade obstacles have emerged as British companies now face a series of lengthy customs procedures, extra paperwork and administrative costs before their products can enter the EU.

However, the impact on coffee-growing nations is less direct, as UK-based importers have strong relationships with coffee-producing countries. This means that UK importers do not rely on the EU to access supplies. In 2021, about 96% of British green coffee imports were sourced directly from producing countries. In comparison to the pre-Brexit situation, import levels have not changed much. Brexit might even further strengthen direct trade relations between UK-based importers and roasters and exporters in producing countries.

Tips:

- See our study on trends in coffee to learn more about current trends in the European market.

- Promote the sustainable and ethical aspects of your production process and support these claims through certification.

- Before engaging in a certification programme, make sure to check that a label has sufficient demand in your target market and whether it will be cost-beneficial for your product, always in consultation with your potential buyer.

- Find potential business partners in the United Kingdom for certified coffee by checking the lists of Fairtrade-certified operators, Rainforest Alliance/UTZ certified coffee supply chain actors and British organic coffee importers.

- See our study on doing business with European coffee buyers for more tips on marketing and promoting coffee.

- Are you interested in exporting high-quality coffee? Learn more about cupping scores on the website of the Specialty Coffee Association (SCA). You can also consider getting a Q-grader or R-grader certificate to be able to cup and score your Arabica and/or Robusta coffee according to international standards.

- Follow the updates of the British Coffee Association and refer to this BBC blog to keep up to date about Brexit and its impact on the United Kingdom’s coffee industry.

Gustavo Ferro and Lisanne Groothuis of ProFound – Advisers In Development carried out this study on behalf of CBI.

Please review our market information disclaimer.

Search

Enter search terms to find market research

Do you have questions about this research?

From a global perspective, the EU and UK coffee markets are enormous. The amount of green beans purchased is large, and direct trade is also actively carried out. Furthermore, there is considerable room for expansion of the market for premium quality coffee enjoyed as a luxury item, in addition to coffee for casual consumption. The time will come when coffee producers and roasters cooperate and do coffee business together. Direct trade plays an important role as its base.

Ayane Yamada: Founder of TYPICA