Entering the Swiss market for cocoa

Switzerland is known for its world-famous chocolate brands and very high chocolate consumption. This makes the country an attractive market for cocoa exporters. But it also comes with strict rules and high buyer expectations. To succeed, exporters need careful preparation, strong planning and proof of certified, sustainable cocoa. In the next sections, we explain the main requirements, trade channels and competition to help you access and grow in the Swiss cocoa market.

Contents of this page

1. What requirements and certifications must cocoa meet to be allowed on the Swiss market?

Exporters of cocoa must follow EU regulations because most Swiss chocolate is sold in EU countries, and EU buyers require compliance throughout the supply chain. For a complete overview of EU requirements, refer to our study on buyer requirements for cocoa. Also, consult the specific requirements of the Swiss Federal Food Safety and Veterinary Office.

In general, the requirements can be grouped into:

- Mandatory requirements.

- Additional requirements to keep up with the market.

- Requirements for niche markets.

What are mandatory requirements?

The EU sustainability laws to follow include the EU Deforestation Regulation (EUDR), Corporate Sustainability Reporting Directive (CSRD) and Corporate Sustainability Due Diligence Directive (CSDDD). These are in line with Switzerland’s 6 Ambitions of the Roadmap 2030 for a sustainable cocoa sector, which was set by the Swiss Chocolate Sector and updated and presented in June 2025. These regulations highlight that:

- Farmers with viable farms and good yields earn at least a living income;

- Human rights are protected: fair labour, no child labour, no forced labour;

- No deforestation from cocoa; degraded forests are restored;

- Agroforestry (shade trees mixed with cocoa) is common practice;

- Cocoa production cuts emissions in line with 2030 and 2050 climate targets;

- All cocoa entering Switzerland is fully traceable and transparent along the supply chain.

The EUDR was supposed to be enforced on 30 December 2025 (or 30 June 2026 for SMEs). However, on 23 September 2025 the European Commission proposed a one‑year delay to enforcement for high‑risk commodities such as cocoa. This means that enforcement now starts from 30 December 2026 (or 30 June 2027 for SMEs). Companies placing cocoa on the EU market must prove that their supply is deforestation‑free, legally produced, and traceable to the exact plot of land where it was grown. Exporters will need to conduct due diligence, including geolocation mapping, legal compliance checks and risk mitigation measures.

This delay, backed by the Council, is intended to give businesses more time to prepare. It also helps make sure that the EU’s central IT system is fully operational. Simplification measures are also under discussion. Only the first operator placing cocoa on the EU market would need to file a due diligence statement. Downstream traders would keep reference numbers instead of filing separate reports. Micro and small operators could submit a one‑off simplified declaration.

Besides EUDR, cocoa businesses must also align with the Corporate Sustainability Due Diligence Directive (CSDDD). This came into force in July 2024 but is now only for very large firms (5,000+ workers and €1.5B turnover). The CSDDD requires companies to prevent and address human rights and environmental risks across their supply chains. They can do this through fair pay, biodiversity protection and carbon neutrality. Focus is now risk‑based. Companies are to check their own operations and Tier 1 suppliers to make sure they follow the rule. Climate plans are no longer required.

EU Countries must put this into law by July 2028. Exporters should expect buyers to ask about labour rights, fair pay, biodiversity and environment. They can demonstrate compliance through codes of conduct covering ethics, social responsibility and environmental stewardship. Watch our cocoa webinar on meeting European market requirements (see from minute 21 onwards) to see how Bara Union from Côte d’Ivoire prevents and addresses human rights to improve sustainability in their cocoa farming community.

Meanwhile, the Corporate Sustainability Reporting Directive (CSRD), effective since January 2023, mandates standardised ESG reporting and third-party verification. The scope has been reduced to firms with 1,000-1,750 workers and €450M turnover. First reports are now due in 2028-2029. Cocoa suppliers must provide data on emissions, labour practices and resource use to help EU buyers meet their obligations.

To simplify these overlapping rules, the EU proposed an omnibus package in February 2025. The package aims to harmonise CSDDD, CSRD and the EU Taxonomy. This reform is expected to reduce administrative burdens by 25% overall and by 35% for SMEs.

Switzerland has its own sustainability laws that mirror EU standards in many ways. Article 964 of the Swiss Code of Obligations requires large companies to report on environmental and human rights risks, similarly to the CSRD. The 2024 Ordinance on Climate Disclosures also mandates climate-related reporting for public companies, banks and insurers. This is based on the framework of the Task Force on Climate-related Financial Disclosures (TCFD). A recent legal update confirms that Swiss companies are ‘indirectly affected by the CSRD and the CSDDD’ if they are part of EU supply chains or meet EU turnover thresholds.

Besides EU obligations, Switzerland has developed its own sustainability framework for cocoa through the Swiss Platform for Sustainable Cocoa (SWISSCO). SWISSCO has set a Roadmap for 2030, with goals including living income for farmers, deforestation-free sourcing and full traceability.

Also, Swiss companies are subject to legal due diligence and reporting duties on child labour risks and conflict minerals in their supply chains since 2023. These obligations are outlined in the Ordinance on Due Diligence and Transparency in relation to Minerals and Metals from Conflict-Affected Areas and Child Labour.

Other mandatory requirements for cocoa

General Food Safety

European Union regulations ensure the safety of cocoa or cocoa products entering the market. Exporters must follow the General Food Law (Regulation (EC) 178/2002). Hygiene standards, like those set out in Regulation (EU) 2017/625, are very important for maintaining food safety throughout the supply chain. These regulations aim to prevent contamination and ensure that only safe, high-quality cocoa products reach European consumers. For free fatty acids, if cocoa has in excess of 1.75%, chocolate makers will reject the cocoa. Products from countries that repeatedly fail to comply with these standards are put on a list. This list is included in the Annex of European Commission Implementing Regulation (EU) 2019/1793.

Contaminants

Several contaminants are regulated in cocoa products, based on advice from the European Food Safety Authority (EFSA). These include heavy metals (like cadmium), pesticide residues, mycotoxins (like ochratoxin A), polycyclic aromatic hydrocarbons (PAHs), microbes and foreign matter. You can also consult the Swiss pesticide database for an overview of the maximum residue levels (MRLs) for each pesticide.

Extraction

Solvents Directive 2009/32/EC regulates the use of extraction solvents in food production. For cocoa, there is a maximum residue limit of 1 mg/kg of 2-methyloxolane in cocoa butter extraction. This solvent is commonly used in the production or fractionation of fats, oils or cocoa butter.

Quality requirements

Buyers in Switzerland and elsewhere currently assess the quality and flavour of cocoa beans in different ways and often use a combination of two or more methodologies. The guide "Cocoa Beans: Chocolate & Cocoa Industry Quality Requirements" offers advice on cocoa growing, post-harvest practices, and quality evaluation methods that help improve cocoa quality. Not having the right quality can lead to losses. Other common cocoa quality assessment methodologies and international cocoa standards used among chocolate makers and cocoa traders include the following:

- ISO’s Standards on classification and sampling for cocoa beans;

- The Fine Cacao and Chocolate Institute (FCCI): check its website and contact FCCI for its sampling protocol and grading form;

- Heirloom Cacao Preservation’s genetic evaluation of cocoa to identify and value cocoa and its flavour;

- Equal Exchange/TCHO’s quality assessment and tasting guide to assess the quality of cocoa along the value chain.

A working group of the Cocoa of Excellence Programme is co-ordinated by The Alliance of Bioversity International and CIAT. They have launched the International Standards for the Assessment of Cocoa Quality and Flavour website. Here you can download the protocols on the quality standards.

These protocols describe step by step how to:

- Sample cocoa beans for evaluation;

- Assess their physical quality;

- Process them into coarse powder, liquor and chocolate;

- Establish a sensory evaluation of the flavours expressed in these three products.

Labelling requirements

The information provided by labels must be easy to understand, easily visible, clearly readable and written in a language easily understood by the purchaser. That is usually English.

The label should include the following topics to ensure traceability of individual batches:

- Product name;

- Grade;

- Lot or batch code;

- Country of origin;

- Net weight in kilograms.

If your cocoa is organic and/or fair-trade certified, the label should contain the name/code of the inspection body and certification number. Labelling rules make sure that consumers receive essential information.

Figure 1. An example of cocoa-bean labelling

Source: Zorzal / Credit: Gustavo Ferro.

Packaging requirements

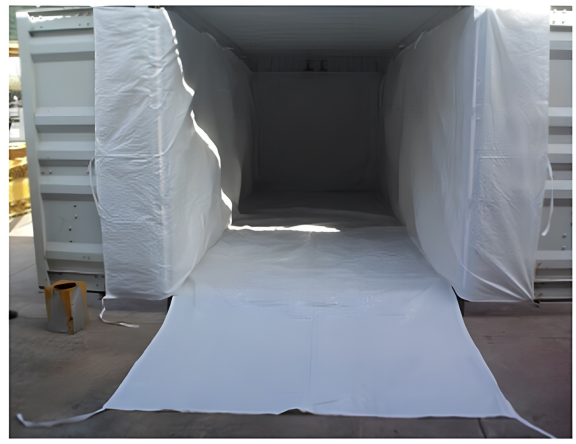

Although no specific packaging regulations exist for cocoa or cocoa products, all food packaging must follow Regulation (EC) no. 1935/2004 on food contact materials. Cocoa beans are traditionally shipped in jute bags, which can weigh between 60 and 65 kg. On the mainstream market, bulk shipment of cocoa beans has become more popular. This means cocoa beans are loaded directly into the ship’s cargo hold or in shipping containers having a flexi-bag (see Figure 2). This mega-bulk method is often adopted by larger cocoa processors, who handle cocoa beans of standard qualities.

Jute bags are still commonly used in the specialty cocoa segment. For very high-quality micro lots, vacuum-sealed GrainPro packaging can be used. GrainPro offers airtight storage bags and liners that stop moisture, insects and mould from affecting stored cocoa beans. This helps farmers and exporters to keep their cocoa fresh and high-quality during storage and transport.

Figure 2: Container lined with flexi-bag

Source: Manual for cocoa extension in Ghana

Figure 3: Cocoa packaged in jute sacks

Source: Amonarmah Consults

Figure 4: Cocoa in a GrainPro bag

Source: Victor Dela Casa

Payment and delivery terms

A proposed rule for EU suggests a 30-day maximum for all food products. The EU’s Access2Markets website provides detailed information about taxes, rules and other factors affecting trade, including specific details for chocolate (HS code 1806).

What additional requirements and certifications do buyers often have?

Next to general European food safety regulations as listed above, you can expect buyers in Switzerland to request extra food safety guarantees from you. This also depends on where your cocoa or product’s final destination will be. For production and handling processes you should consider the following:

- Implement good agricultural practices (GAPs). The main standard for good agricultural practices is provided by GLOBALG.A.P. This is a voluntary standard for the certification of agricultural production processes that provide safe and traceable products. Note that certification organisations (such as Rainforest Alliance/UTZ) often incorporate GAP in their standards.

- Implement a quality management system (QMS). A system based on Hazard analysis and critical control points (HACCP) is often a minimum standard required at the level of storage and handling of cocoa beans. If you export semi-finished cocoa products, some buyers will also expect you to have certification, such as International Featured Standards: Food (IFS), Food Safety System Certification (FSSC 22000) or British Retail Consortium Global Standards (BRCGS) certificates, for your manufacturing facilities.

Also, many Swiss chocolate and cocoa companies have specific sustainability policies emphasising the contact with producers, transparency in their operations, and their social and environmental impact.

Adopting codes of conduct or sustainability policies related to your buyer’s environmental and social impacts may give you a competitive advantage. In general, it is likely that buyers will require you to comply with their code of conduct and/or fill out supplier questionnaires about your sustainability practices.

For certification programmes, Fairtrade certification is popular in Switzerland. Sales of Fairtrade products in Switzerland exceed one billion Swiss francs. In Switzerland, this generates a total of USD13.3 million in Fairtrade premiums, while the total worldwide amounts to over USD 200 million. Obtaining a Fairtrade certification might give you an advantage over other suppliers.

Common fair trade standards on the Swiss market include Fairtrade, for which the accredited certifier is FLOCERT, and Fair for Life. Fair for Life certification was developed by the Swiss Bio-Foundation and the Institute for Market ecology (IMO). But keep in mind that Fair for Life may be less known in the marketplace. This certification standard has the advantage of being cheaper than some others, as the control body may combine the fair-trade audit with the organic or Rainforest Alliance audit. However, you should always check demand for and interest in a specific certification with your (potential) buyer. It is also recommended that you check what kind of a premium will be paid, as this is not regulated, unlike Fairtrade’s minimum price.

From 1 January 2025, the European Union changed its import rules. Imports from most countries must now show full compliance with all EU laws (Regulation 2018/848). This also affects Swiss organic imports, which must be certified under the EU Organic Regulation if they come from most countries outside the EU. Switzerland’s own organic ordinance (SR 910.18) follows these regulations.

A mandatory national logo for organic products does not exist in Switzerland. However, the private label of Bio Suisse, the Swiss private organic sector association, is widely used. But the standards of this label are stricter with regard to agricultural production and processing than the Swiss Organic Law, or EU Organic regulation. So EU organic certification is a basic requirement to obtain Bio suisse certification.

Retailer Coop, the largest seller of organic food in Switzerland, only accepts organic products from this standard. Other organic standards used in Switzerland are Demeter and Migros Bio, the private organic label of retailer Migros. Each scheme has its own requirements and may be required by specific buyers.

What are the requirements for niche markets?

Meeting the niche market requirements in Switzerland offers advantages like direct relationships with chocolate makers, price premiums and stronger brand reputation. Niche buyers may look for fine flavour cocoa or cocoa products. Exporters who want to access the niche market must be ready with solid documentation, certifications and transparent practices.

Fine flavour

Fine flavour or specialty cocoa is another niche with strong demand among Swiss bean-to-bar and artisanal chocolate makers. Buyers require high standards in fermentation, flavour profile, moisture content and traceability. These evaluations are done by the Swiss Food Biotechnology Research Group. Exporters targeting this segment often need to provide detailed documentation, proof of origin, and sometimes even farm-level traceability.

Tips:

- Refer to the International Trade Centre Standards Map or the Global Food Safety Initiative website to learn about the different food safety management systems, hygiene standards and certification schemes. Find out which standards or certifications are preferred by potential buyers in your target segment. Buyers may have preferences for a certain food safety management system or sustainability label depending on their end clients and/or distribution channels.

- Consult the EU pesticide database or the Swiss pesticide database for an overview of the maximum residue levels (MRLs) for each pesticide.

- See our study on certified cocoa for more information about the demand for sustainable cocoa on the European market, trends and specific trade channels.

2. Through which channels can you get cocoa on the Swiss market?

You have several channels to introduce your cocoa and cocoa products to the Swiss market. Your entry strategy will depend on the quality of your cocoa beans and your supply capabilities. More and more retailers and cocoa-processing companies are sourcing their cocoa beans directly. In some cases this can allow you to take advantage of the shift towards shorter supply chains. Others are also processing cocoa beans locally or partnering with local processors to produce premium products.

How is the end market segmented?

The confectionery industry can be segmented according to the quality of the end products. For cocoa beans, the end products mainly consist of chocolate bars.

Figure 5: Percentage distribution of chocolate market segments based on quality.

Source: Mordor Intelligence

In Switzerland, supermarkets remain the main sales channel for chocolate products. They stock a wide variety ranging from low-end to higher-end products. Supermarkets also sell an extensive range of own-label chocolate products. These continue to grow popular as they offer the same characteristics as branded products but usually at more affordable prices. The total share of Switzerland’s private-label market reached 51% in 2025. The two biggest grocery retailers are Migros and Coop, together holding about 70% of the market.

Low-end

The low-end segment offers affordable chocolate products with lower cocoa content. These are mainly produced by large chocolate manufacturers using bulk cocoa from West Africa (Forastero variety). Bulk cocoa is characterized by high volumes, low value, and standard quality. In Switzerland, it is also common to find some chocolate products in this segment carrying an organic and/or fair-trade certification.

In Switzerland, key distribution channels for low-end chocolate include major supermarket chains like Migros and Coop as well as discount retailers like Aldi, Lidl and Denner. Many mainstream and lower-end chocolate products in these outlets are mass-market or private-label items. These are often produced using mass balance sourcing. This is a system where certified and non-certified cocoa may be mixed during processing, but the volumes of certified cocoa purchased must match the volumes sold as certified. The approach is common across the Swiss cocoa sector, as highlighted by the Swiss Cocoa Platform and Rainforest Alliance. It is also confirmed in company policies such as those of Lindt & Sprüngli.

Below are some examples of lower-end chocolate brands found in Swiss supermarkets, with an indication of their consumer prices.

Table 1: Examples of lower-end chocolate brands found in Swiss supermarkets based on 2025 prices

| Product | Image | Price (CHF/kg) |

|---|---|---|

| COOP Naturaplan (organic Fairtrade dark chocolate, 100 grams) |

| 25 |

| Coop Naturaplan Organic Dark Chocolate Bar with Salted Pistachios – 60% Cocoa – 150g – Fairtrade, 150 grams) |

| 36 |

Middle-range

The middle-range segment includes chocolate products of good quality, which are commonly sustainably certified. Storytelling and the origin of the cocoa beans are important in this segment, mainly for marketing purposes.

Middle-range products are mainly sold through supermarkets and are usually the high-quality category for these retailers. Supermarkets are increasingly offering their own premium private label chocolate products. These offer much the same quality and characteristics as branded chocolates, but their prices are usually more competitive. Besides mainstream supermarkets, middle-range products can also be found in more specialised shops such as Farmy (an online outlet for organic products).

The table below gives some examples of middle-range products available in Switzerland, with an indication of their consumer prices (based on COOP’s retail prices in 2022).

Table 2: Examples of middle-range chocolate brands found in Swiss supermarkets based on 2025 prices

| Product | Image | Price (CHF/kg) |

|---|---|---|

| Lindt Excellence (dark chocolate, 85%, 100 grams) |

| 48 |

| Amarrú (organic Fairtrade dark chocolate, 71%, 100 grams) |

| 53 |

| Munz (organic Fairtrade dark chocolate, 85%, 100 grams) |

| 46 |

High-end

Smaller, more specialised chocolate makers produce high-end chocolate products, mainly using fine-flavour cocoa (usually Criollo, Trinitario and/or, to a lesser extent, Forastero). These products are characterised by a high cocoa content. Single origin of the cocoa beans is important, both for the taste as the traceability of the cocoa. Single origin means that the buyer knows exactly where their cocoa beans are from and that it is a specific cocoa rather than a blend. Bean-to-bar chocolate is a good example of a high-end product.

High-end products are mainly sold at chocolate events, at trade fairs and in specialist shops. Choba, La Flor, Orfeve, Sadé Chocolat and Taucherli are examples of Swiss bean-to-bar makers. Examples of other speciality chocolatiers in Switzerland are Max Chocolatier and Teuscher. An example of a speciality web shop is Chocolats du Monde.

Some examples of high-end chocolate products, with an indication of their consumer prices are shown below.

Table 3: Examples of high-end chocolate brands found in Swiss supermarkets based on 2025 prices

| Product | Image | Price (CHF/kg) |

|---|---|---|

| La Flor (dark chocolate, Brazil) |

| 148.6 |

| Esterre 80, Orfeve (dark chocolate, bean-to-bar) |

| 147.1 |

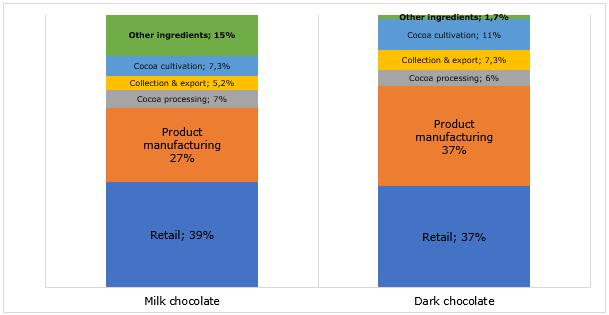

It is important to realise that trade and retail prices for chocolates are not always directly linked. As the figure below shows, depending on the end product in which cocoa beans will be used, between 7.3% and 11% of the added value goes to farmers. In general, cocoa-bean export prices, and the share kept by cocoa producers, will depend on multiple factors. These include the cocoa beans’ quality, the size of the lot and the supplier’s relationship with the buyer. The largest shares are kept by chocolate companies and retailers.

Figure 6: Estimated value distribution per actor in %, for dark and milk chocolate.

Source: BASIC, 2020.

Tips:

- Learn more about the promotion of standard quality and speciality chocolate by mainstream Swiss supermarkets such as Coop. Compare their product assortment and price levels with specialised stores such as Chocolats du Monde.

- Refer to our study on trends in the cocoa sector to learn more about developments within different market segments.

Through which channel does cocoa end up on the end market?

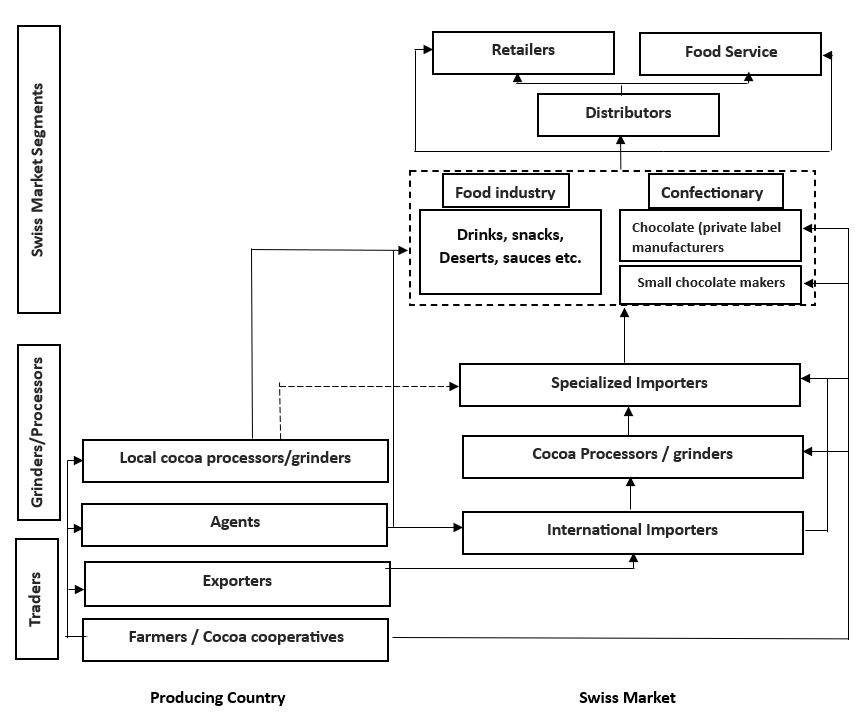

As an exporter, you can use different channels to access the Swiss market with your cocoa. Entry into the market will depend largely on the quality of your beans and your supply capacity. The figure below shows you the most important channels for cocoa beans in Switzerland.

Figure 7: Channels through which cocoa beans end up on the Swiss market

Source: Profound

Here is a brief description of each channel through which your cocoa can enter Switzerland.

Cocoa bean processors/grinders

Large processors/grinders source their cocoa beans directly from producing countries. They process the raw material into cocoa mass, cocoa butter and/or cocoa powder. The processors/grinders then distribute it to confectionery, food, cosmetic and pharmaceutical industries throughout Europe. Some cocoa processors also make end products to supply directly to the retail or food service sector.

Large processors like Lindt & Sprüngli and Barry Callebaut operate extensive facilities in Switzerland, which is a cocoa-processing centre. Pronatec specialises in organic and Fairtrade semi-finished cocoa products and chocolate. Smaller grinders that focus on artisanal techniques, small-batch production and niche markets include Felchlin and Stella Bernrain.

Importers

Most cocoa beans are imported directly from producing countries. Large processors maintain their own sourcing networks. They purchase substantial quantities of raw beans to supply their large-scale grinding and processing facilities. These companies engage directly with producing countries and rely on well-established supply chains to ensure consistent output.

Next to meeting domestic needs, some of these importers also supply other Swiss companies or re-export to European markets. Alongside large players like Barry Callebaut, Lindt & Sprüngli and Nestlé, specialised importers and processors like Pronatec, Felchlin and Stella Bernrain import smaller quantities. They often work directly with producers or cooperatives to secure beans that meet specific quality or certification requirements.

Other specialty trading companies in Switzerland are Minka SCS (sustainable cocoa), Caboz (fairly traded African cocoa), Walter Matter (fair trade cocoa), Chocolats Halba (fair trade cocoa) and Stella Bernrain (organic and fair trade cocoa). Specialised importers could also be interested in value-added cocoa products processed at the country of origin. They might even want finished products like chocolate.

Large (private label) chocolate manufacturers

These manufacturers source cocoa beans directly from producing countries and often have their own importing departments. They produce chocolate under their brands and private labels. Key player is Barry Callebaut, which is the largest industrial chocolate manufacturer worldwide and has production and grinding facilities in Switzerland. Other large chocolate manufacturers active on the Swiss market are Camille Bloch, Maestrani, Mars, Mondelez and Nestlé.

These manufacturers often work directly with suppliers to source high-quality cocoa, bypassing large importers. They are growing in importance as it becomes more common for large brands to outsource their production to specialised private-label manufacturers. Exporters can approach private-label companies, highlight their capabilities and unique offerings, and negotiate favourable contract terms to establish direct supply partnerships. This can provide exporters with more control and transparency in the supply chain, better pricing and diversification beyond relying solely on large importers as customer.

Small chocolate makers

In this segment, cocoa beans are increasingly traded directly from farmers or cooperatives to artisan chocolate makers. In some cases, direct trade still involves intermediary importers who manage logistics and certification. This channel remains small compared to the mainstream market. But it is steadily growing as demand for bean-to-bar and traceable chocolate rises. Specialised Swiss chocolate makers that source cocoa directly from producing countries include Choba Choba, La Flor, Orfève and Sadé Chocolat. Companies like PRONATEC and Stella Bernrain also emphasise direct sourcing from smallholders and cooperatives, strengthening the position of direct trade in Switzerland’s chocolate industry.

Intermediaries/agents

In the cocoa trade, intermediaries/agents serve as a link between exporters, importers, and chocolate manufacturers. Depending on their role, they may work independently or be contracted to source cocoa beans on behalf of a company. By leveraging their market expertise, agents can help exporters identify reliable buyers and facilitate trade.

What is the most interesting channel for you?

Exporters should carefully assess which channel best fits their product, market, and resources. Each option, such as agents, distributors, or direct sales, offers different benefits and challenges.

Small chocolate makers

For exporters of specialty cocoa, small chocolate makers in Switzerland offer a valuable channel. These artisan producers often seek high-quality, fine-flavour beans and are willing to pay premiums for unique profiles, emphasising direct trade with producers to ensure quality, traceability and sustainability. They typically require detailed information on the cocoa’s origin, processing and certifications like organic or Fairtrade.

Representative/agent

Chocolate makers entering the Swiss market can benefit from partnering with local agents or representatives, who assist in identifying buyers, negotiating deals, and handling communications while representing exporters’ interests. Fees usually range from 5% to 10% commission on sales, plus potential extras like marketing costs. In cocoa-producing countries, processors often collaborate with Swiss-based branches or independent agents; examples are Cocoasource for trading and Felchlin for direct sourcing.

Importers

Importers provide an effective gateway to the Swiss industry. This is particularly so for standard-quality beans in high volumes, as direct processor access is rare. They leverage long-term supplier relationships to streamline market entry, ensure compliance, and share insights on quality and regulations. Focus on those specialising in cocoa or niches like organic products for tailored expertise. Key players include Barry Callebaut, Lindt & Sprüngli and Nestlé for large-scale imports. For specialty and sustainable cocoa the main players are PRONATEC, Minka SCS, Caboz, Walter Matter, Chocolats Halba and Stella Bernrain.

Online retail store

The online retail channel is experiencing strong growth in Switzerland’s chocolate market, projected at a CAGR of 2.2% from 2024 to 2030, reaching USD 2,582.7 million by 2030. This expansion is driven by Switzerland’s internet infrastructure, with over 99% penetration, making e-commerce highly accessible. It is an appealing entry for chocolate makers targeting the Swiss market.

Tips:

- Find buyers in Switzerland who match your business philosophy and export capacities (in terms of quality, volume, certifications). For more tips on finding the right buyer for you, see our study on Finding Buyers on the European Cocoa Market.

- Use industry associations to find potential buyers in Switzerland, such as ChocoSuisse, the Association of Swiss Chocolate Manufactures. Also check the members of the Swiss Platform for Sustainable Cocoa.

- Invest in long-term relationships. Whether you are working through an importer or directly with a chocolate maker, it is important to establish a strategic and sustainable relationship with them. This will help you manage market risks, improve the quality of your product and reach a fair quality/price balance. For more tips, read our study on Doing Business with European Cocoa Buyers.

3. What competition do you face on the Swiss cocoa market?

Switzerland’s cocoa market remains highly competitive, shaped by contrasting dynamics in bulk and specialty segments. Bulk cocoa is dominated by large suppliers competing on volume. But record-high cocoa costs in 2024 have made this segment increasingly challenging for smaller exporters. The specialty cocoa market, while smaller in volume, continues to grow in strategic importance as Swiss chocolate makers focus on quality, flavour, traceability and sustainability. Rising regulatory demands, particularly compliance with the EU Deforestation Regulation (EUDR), further intensifies competition by raising entry barriers.

Which countries are you competing with?

Switzerland sources cocoa from several countries, each with a distinct profile. Ghana remains Switzerland’s largest supplier, providing the bulk of standard quality cocoa beans. Côte d’Ivoire also continues to supply bulk cocoa, though with a much smaller share compared to Ghana. Ecuador, Peru and the Dominican Republic stand out in the specialty segment, offering fine flavour and organic beans that meet the growing demand for traceability and premium quality.

Source: ITC calculations based on UN COMTRADE and ITC statistics

Ghana: Switzerland’s main supplier of cocoa beans

Ghana, renowned for producing high-quality cocoa beans, is a main part of the global cocoa supply chain. It is one of the largest producers of Forastero cocoa beans worldwide. Forastero beans are mainly used in the mainstream market. A large share of cocoa produced in Ghana is Rainforest Alliance, which is a market entry requirement to large manufacturers and retailers operating in Switzerland.

The cocoa supply chain in Ghana is well-established, and the Ghanaian government is involved in all facets of it. Ghana Cocoa Board Cocobod encourages production, processing and the marketing of cocoa beans. It is also the main trader of cocoa beans to international markets.

Ghana remains Switzerland's primary supplier of cocoa beans, accounting for approximately 38% of total Swiss imports in 2024. Swiss imports have remained stable, averaging just under 25,000 tonnes annually between 2020 and 2024, reflecting a consistent, long-term demand for Ghana’s cocoa.

However, Ghana’s cocoa sector is under significant environmental and biological stress. The World Bank (2023) documented changes in annual rainfall and temperatures are rising. These factors place substantial pressure on production. Adding on to this is the spread of the Cocoa Swollen Shoot Virus Disease (CSSVD), which has led to an estimated 17% annual loss in production. The disease has affected over 592,230 hectares, representing an 88% increase in just 6 years. Illegal mining also poses a serious risk to Ghana’s cocoa farms. The combination of these factors not only threatens immediate yields but also puts the long-term sustainability of Ghana’s cocoa industry at risk.

As a response, Cocobod has put measures in place to rehabilitate the diseased farms for replanting. Ghana’s cocoa traceability system has also moved from pilot to national rollout. This makes Ghana particularly attractive to buyers interested in ethical sourcing and consistent quality, while meeting latest EU requirements. Some cocoa exporters and producers’ organisations from Ghana are ABOCFA and Kuapa Kokoo Co-operative Cocoa Farmers and Marketing Union Limited.

Source: ITC calculations based on UN COMTRADE and ITC statistics

Ghana not only exports premium beans but also produces value-added products like cocoa paste, butter and powder. The country stands out among cocoa-producing countries for semi-finished products to Switzerland. It ranked third in exporting cocoa butter and was the main supplier of cocoa paste and cocoa powder in 2020-2024, reflecting its growing capacity to move up the value chain and remain competitive in the global cocoa market.

Source: ITC calculations based on UN COMTRADE and ITC statistics

Source: ITC calculations based on UN COMTRADE and ITC statistics

Source: ITC calculations based on UN COMTRADE and ITC statistics

Increasing imports from Côte d’Ivoire

Côte d’Ivoire continues to solidify its position as a key supplier of cocoa beans to Switzerland. Import volumes show a steady increase over recent years. While its output remains far below that of Ghana and select Latin American specialty origins, Côte d’Ivoire excels in producing bulk cocoa beans. In 2024, Switzerland imported 3,870 tonnes of cocoa beans from Côte d’Ivoire, up from 3,345 tonnes in 2020. This shows a compound annual growth rate (CAGR) of approximately 3.72% over this period. Despite minor year-to-year fluctuations, the overall trend since 2020 indicates consistent growth.

While Côte d’Ivoire is a reliable source of bulk cocoa, its beans are often perceived as lower in quality compared to fine flavour varieties from regions like the Dominican Republic, Ecuador or Peru. The country faces significant challenges, notably cocoa swollen shoot virus disease (CSSVD), which is endemic to West Africa and threatens long-term production stability. Nevertheless, its role as a cornerstone of the global cocoa supply chain remains unchallenged, placing Switzerland as a dependable source of bulk cocoa to meet growing demand.

Like Ghana, Côte d’Ivoire relies on a well-established cocoa supply chain. The Conseil du Café-Cacao (CCC) is the regulating body in Côte d’Ivoire and is responsible for the management and promotion of the country’s cocoa sector. The CCC sells 70-80% of the main crop before the harvest starts. Six multinational traders dominate the Ivorian cocoa trade: Cargill, Barry Callebaut, ofi, Ecom, Sucden and Touton. However, at least 20% of exports from Côte d’Ivoire must be exported by local processors and exporters.

Some cocoa exporters and producers’ organisations from Côte d’Ivoire are ECOOKIM and ECAKOOG.

Dominican Republic: leading supplier of organic cocoa

The Dominican Republic has rapidly emerged as Switzerland’s overall second-largest cocoa supplier. The country surpassed Ecuador in growth momentum in 2024. It exported 14,825 tonnes of cocoa beans to Switzerland, up from 4,069 tonnes in 2021. This represents nearly a threefold increase in just three years, making the Dominican Republic one of the fastest-growing cocoa origins for Switzerland.

The country is a global leader in organic cocoa, with over 87% of its cocoa area dedicated to organic cultivation. Much of its production is also Fairtrade-certified, aligning with the demand of Swiss chocolate makers and traders. One of the largest suppliers is the Confederación Nacional de Cacaocultores Dominicanos (CONACADO), which unites thousands of smallholder farmers. They offer a large list of certifications, including Rainforest Alliance, Fairtrade, Fair for Life and Bio Suisse (Swiss private label organic certification) to enable exports to Switzerland. Swiss company Pronatec sources significant volumes from the Dominican Republic for its own sustainability projects, including Yacao. Pronatec is also a major importer of organic cocoa with Bio Suisse certification.

Ecuador: largest producer of fine flavour cocoa

Ecuador remains a major Latin American cocoa supplier, with a total cocoa exports reaching $3.6 billion in 2024. Recently export volumes declined slightly. Shipments to Switzerland dropped from 10,457 tonnes in 2023 to 8,542 tonnes in 2024, an 18% decline. Ecuador’s climate-related issues, including El Niño effects and pests, combined with aging trees, hurt yields and quality. This puts pressure on its fine flavour segment.

To counter these risks, Ecuador has introduced reforms across its cocoa sector. With support from international partners like the EU, FAO and UNDP, the country is taking action. They are rolling out national traceability systems, piloting deforestation-free certification schemes and strengthening good agricultural practices among farmers. Projects like PROAmazonía and AL-Invest Verde are also helping smallholders replant with improved varieties, adapt to climate stress and meet the requirements of the EU Deforestation Regulation (EUDR). These programmes are designed to secure Ecuador’s place in premium markets where traceability and sustainability are non-negotiable.

For Switzerland, this makes Ecuador a dependable source of cocoa beans. Even when volumes dip, Ecuador continues to supply fine flavour beans backed by traceability and sustainability guarantees. This confirms its position as one of the most reliable and competitive origins for the Swiss premium chocolate industry.

Some successful exporters of cocoa beans from Ecuador are UNOCACE, COFINA, Ecuacoffee SA and Cacaos Finos Ecuatorianos SA.

Peru stands out for its production of organic and high-quality cocoa beans

Peru has also strengthened its role in the Swiss cocoa market. Swiss imports of Peruvian cocoa beans reached 5,892 tonnes in 2024, up from 2,237 tonnes in 2021. This consistent growth underscores Peru’s reputation for organic and fine flavour cocoa.

The country produces mainly Trinitario and Criollo beans, with around 75% of exports classified as fine flavour cocoa. Peru is the world’s second-largest producer of organic cocoa by area, and is a key supplier to Europe’s organic and specialty markets. The national association APPCACAO has been instrumental in uniting farmers, exporters and institutions to promote Peruvian cocoa worldwide.

Exporters include Ecoandino and Norandino, both of which supply high-quality organic beans to Switzerland.

Malaysia: largest exporter of cocoa butter to Switzerland

Malaysia has established itself as a global leader in cocoa processing, even though its domestic cocoa bean production is relatively small compared to West Africa. The country’s strength lies in its advanced processing industry and infrastructure. These allow it to consistently supply large volumes of semi-finished cocoa products to international markets. Between 2020 and 2024, Malaysia was by far the top exporter of cocoa butter to Switzerland. Averaging well over 10,000 tonnes annually, it put them far ahead of Indonesia and Ghana.

Global players like Barry Callebaut have invested in facilities like the 40,000-tonne capacity cocoa warehouse in Pasir Gudang, Johor, which streamlines storage and supply chains. This makes Malaysian cocoa butter highly competitive for buyers in Europe – particularly Switzerland’s chocolate makers, who depend on reliable, large-scale suppliers.

Looking ahead, Malaysia’s strategy focuses on sustainability and premium value chains, especially in meeting EU deforestation regulations and strengthening quality standards. It cannot match Madagascar on fine flavour reputation. But Malaysia’s scale, efficiency and investment in compliance ensure it remains the leading supplier of cocoa butter to Switzerland’s chocolate industry.

Which companies are you competing with?

Switzerland is home to some of the world’s largest chocolate manufacturers and cocoa traders. This makes it a highly competitive destination for cocoa exporters. Your main competitors are therefore these large multinationals with processing operations in producing countries. Others are the small and medium-sized chocolate makers that specialise in premium and ethical cocoa products.

Large multinational companies

Many of the large companies in Switzerland like Barry Callebaut, Nestlé and Lindt & Sprüngli, alongside international processors like Cargill, Olam and ECOM, operate grinding and processing facilities directly in cocoa-producing countries. This helps them secure supply at scale and reduce costs. This strategy is reinforced by supportive policies in producing countries.

For instance, in Côte d’Ivoire export taxes are reduced on processed cocoa products for companies that expanded their facilities. Instead of a fixed rate of 14.6%, the export taxes on cocoa butter are reduced to 11%. Export tax for cocoa paste is also reduced to 13.2%, and that of cocoa powder to 9.6%. In Ghana, the second leading producer, there is a special area called the Ghana Free Zones allocated to processing companies. These companies receive benefits if they export at least 70% of their products, plus are allowed to import raw materials and machinery without paying taxes.

Multinationals use their resources to leverage economies of scale, invest in sustainability programmes, and build direct farmer partnerships. Cargill has invested heavily in processing capacity in Côte d’Ivoire and promotes sustainability through its Cocoa Promise programme, which emphasises traceability and farmer support. Similarly, Barry Callebaut runs initiatives like the Cocoa Horizons programme, positioning itself as a sustainability-driven supplier aligned with European consumer expectations for ethical chocolate.

These multinationals have the greatest influence in Switzerland’s cocoa supply chain. They dominate the bulk and semi-finished product trade, making it difficult for smaller exporters to compete on volume, price and certification requirements.

Small and medium-sized chocolate makers

While Switzerland hosts global giants like Barry Callebaut and Lindt, it also boasts a vibrant ecosystem of small and medium-sized chocolate makers that thrive on craftsmanship, sustainability and origin-driven storytelling. Brands like La Flor and Chocolat Stella Bernrain have successfully carved out niches by focusing on transparency, ethical sourcing, and partnerships with smallholder farmers. Even mid-sized firms like Felchlin, renowned among pastry chefs for its fine flavour cocoa, demonstrate the value of quality consistency and strong supplier relationships. SMEs can learn from these competitors by investing in traceable supply chains, building authentic brand narratives, and leveraging sustainability as a market differentiator in the premium Swiss segment.

Tips:

- Consider teaming up with other cocoa companies in your area if your business isn’t very big or you don’t have a lot of cocoa. This can help to win bigger orders, share operations/costs and improve financing/marketing reach. Agree on specs plus standardise fermentation/drying, collection points, shared warehouse standards, joint brand, shared website/catalogue, target buyers, and how you will split costs and share revenues. Pilot one shipment, review results, reinvest in shared tools.

- To sell your cocoa products in competitive markets like Switzerland, you have to stand out. So focus on what makes you special, what you are good at, and communicate consistently.

What are the prices of cocoa on the Swiss market?

The cocoa market has seen major fluctuations over the last five years due to supply disruptions and rising demand. The sharpest increases occurred in 2023 and 2024, driven by poor harvests in West Africa. As of 30 April 2025, the ICCO daily price stood at $8,392.56 per tonne. This is lower than the 2024 peak but still well above historic averages. Switzerland, home to some of the world’s largest chocolate manufacturers, has felt these price changes directly in its processing costs.

These rising processing costs have been passed on to consumers. Chocolate prices in Switzerland climbed steadily, especially in 2023-2024. In this period record cocoa prices combined with broader inflation pushed retail prices higher. Premium Swiss brands like Lindt & Sprüngli and smaller bean-to-bar producers have had to adjust retail prices accordingly. At the same time, sustainability regulations such as the EU Deforestation Regulation (EUDR) is raising compliance costs.

This regulatory environment interacts with another defining feature of the Swiss market: its strong consumer demand for sustainability. Cocoa certified by Fairtrade or Rainforest Alliance requires additional premiums. For example, the sustainability premium is $240 per tonne for Fairtrade, plus $300 for organic, or at least $70 under the Rainforest Alliance’s Sustainability Differential. These labels matter because Swiss consumers are highly responsive to ethical and environmental concerns.

Tips:

- Visit the websites of Fairtrade and Rainforest Alliance to get regular updates on premiums for cocoa.

- Visit the International Cocoa Organization (ICCO) website to get regular updates on cocoa prices.

Amonarmah Consults carried out this study in partnership with Molgo Research and Ethos Agriculture on behalf of CBI.

Please review our market information disclaimer.

Search

Enter search terms to find market research

Do you have questions about this research?

If you want to supply organic cocoa to the Swiss market, you should first connect with a Swiss buyer who is interested in your cocoa. Then, find out what specific certifications are important for them. Also consider whether the economic benefits would exceed your production costs.

Hans Ramseier, Head of Quality Assurance and Development Imports at Bio Suisse