How the Iran-US conflict increased fertiliser prices, and what you can do

The conflict between the United States (US) and Iran is a long-running political disagreement that involves strict economic sanctions. These tensions often create challenges for international security and global trade. And now, shipping restrictions in the strait of Hormuz have driven up fertiliser and energy prices, putting the global food system under serious pressure. Learn what farmers and exporters can do.

To feed the growing global population, farmers need fertilisers. Since 1965, global fertiliser consumption has grown considerably, rising from 46 to 206 million metric tonnes in 2024. During the same period, the world’s population has grown from 3.3 to over 8 billion people.

Due to the Iran-US conflict, traders in fertiliser do not have access to the Strait of Hormuz, a narrow sea passage through which about one-third of all global fertiliser trade passes. Saudi Arabia, Qatar, Bahrain, and Iran together supply around 30% of global urea exports. Urea prices have risen as much as 49%, and those of ammonia by around 20%. This is happening at the worst possible time: spring planting season, when fertiliser demand peaks.

The Russia-Ukraine conflict showed the same pattern

In 2022, Russia's invasion of Ukraine caused fertiliser prices to rise by around 50% in just a few weeks. At the time, Russia was the world's biggest fertiliser exporter. The price of urea reached $ 925 per tonne in April 2022. As a result, more than 22 million extra people faced famine. Prices declined slightly in 2023, but the damage in sub-Saharan Africa was long-lasting. A few large agrochemical companies dominate the global fertiliser production:

- Canadian Nutrien

- US-based CF Industries

- Norwegian Yara.

Whenever a conflict disrupts even a single part of this system, the effects spread quickly across global food supply chains.

Low- and middle-income countries feel the impact most

Countries that import the majority of their fertilisers are at greatest risk. India is the second-largest regional market for fertilisers, with demand reaching $ 45.7 billion in 2024, and it relies on imports for 44% of its supply. East and South Asia together used more than 103 million metric tonnes in 2024, more than half of the world’s total. Brazil imports over 85% of what it needs.

Higher fertiliser prices result in higher food prices

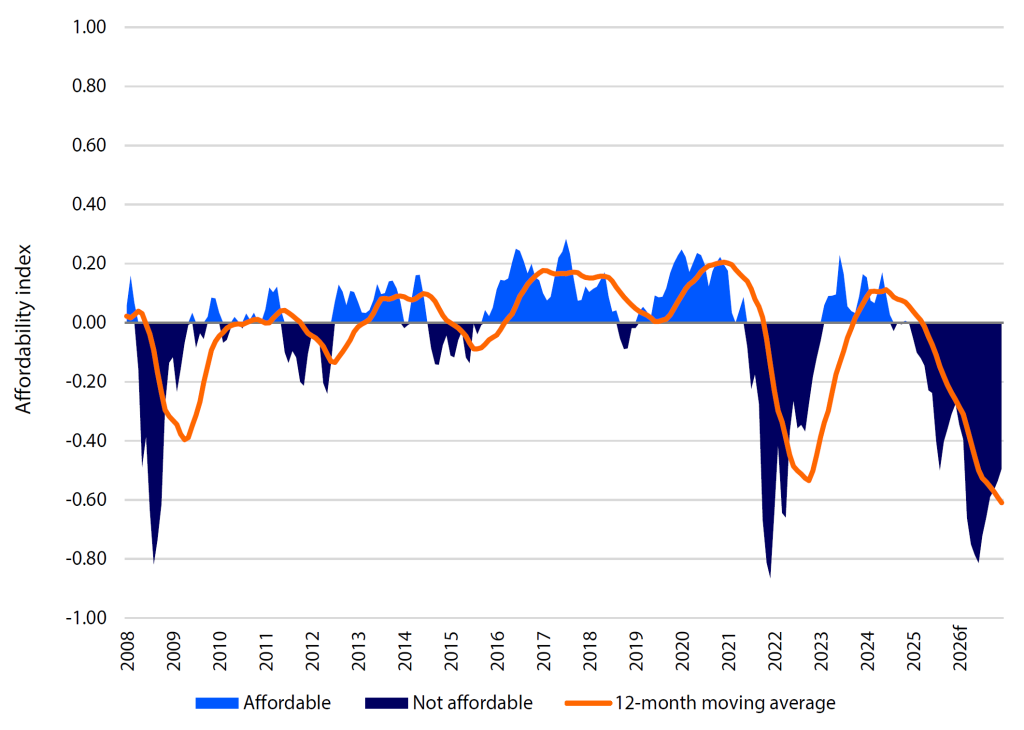

When fertiliser prices rise, food prices follow within 1 or 2 growing seasons. RaboResearch's Semiannual Fertiliser Outlook for April 2026 reports that fertiliser affordability has fallen to negative levels and expects it will remain there throughout 2026. They expect that urea demand will fall by around 5% and phosphate demand by 7%, with high prices expected to continue into 2027.

Rabobank warns that a decline in demand is inevitable: Farmers need to reduce application volumes in the coming season. In Europe, farmers will likely shift away from nitrogen-intensive crops such as corn toward soybeans and other legumes. In low- and middle-income countries, where food accounts for a larger share of the household budgets, the impact will be even greater.

Figure 1: Global fertiliser affordability index

Source: RaboResearch, 2026

What can farmers and exporters do?

It is difficult to overcome dependency on chemical fertilisers in the short term, but there are steps that can help to reduce the use:

- Test your soil before each season: This helps you apply only what you need and avoid extra costs.

- Use bio-fertilisers or compost as a partial alternative: These are more resilient to price shocks and increasingly valued by European buyers.

- Diversify your crops: A mix of crops reduces the risk when one input becomes too expensive.

- Adopt precision agriculture tools to use fertilisers more efficiently and lower input costs.

- Talk to your buyer early. European buyers are also under cost pressure. Planning together helps protect your margins.

Learn more

Read CBI's study on trends in the fresh fruit and vegetables sector and our 11 tips to go green in the fresh fruit and vegetables sector for more guidance on sustainable practices that can also help reduce input costs.

CBI Market Intelligence wrote this news article.

Stay informed

To stay informed on the latest developments in the fresh fruit and vegetable sector, subscribe to our newsletter.