Entering the European market for black pepper

Food safety certification combined with reliable and frequent laboratory tests creates a positive image for pepper exporters to Europe. Sustainable production and implementation of corporate social responsibility standards will provide extra advantages for emerging suppliers. The strongest competitors to new pepper suppliers are Vietnam, Brazil, Indonesia and India.

Contents of this page

1. What requirements and certifications must black pepper meet to be allowed on the European market?

Black pepper must meet several mandatory (legal) requirements to enter the European market. Buyers can have additional requirements and ask for certification. Mandatory requirements for black pepper in Europe focus on consumer health and safety. Sustainability requirements are also becoming more important.

What are mandatory requirements?

Most mandatory requirements for the import of black pepper relate to food safety. The European Commission for Health and Food Safety is responsible for the European Union’s policy and for monitoring the implementation of related laws.

Official food controls

Food imported into the European Union (EU) undergoes official food controls. These can take place at the border or later in the supply chain. Violations of European food legislation are reported through the Rapid Alert System for Food and Feed (RASFF). In 2024 and 2025, 7 and 6 issues with black pepper were reported, respectively. These numbers were down from previous record highs of 48 in 2022 and 22 in 2023. These were mainly due to salmonella contamination in black pepper from Brazil.

If imports of a certain product from a specific country repeatedly violate European food legislation, they are officially checked at the border more often. Brazil currently has a 50% frequency for black pepper (HS code 090411) due to a salmonella hazard. Black pepper in Brazil takes is produced on small family farms that sun-dry the pepper in the open air. This increases the risk of salmonella contamination by animals and birds. Contamination can also come from irrigation with unsafe water, using untreated manure as fertiliser and harvesting with dirty hands.

Tip:

- Search the RASFF database for examples of withdrawals from the European market.

Figure 1: Salmonella species growing on XLD agar

Source: Wikimedia Commons – original photo by Nathan Reading from Halesowen, UK

{kind=link}

Contaminants

Food contaminants are substances that are present in food but have not been intentionally added. They may be the result of production, packaging, transport or holding, or environmental contamination. They can pose a health risk to consumers. To minimise these risks, EU Regulation (EU) 2023/915 sets maximum levels for certain contaminants in foodstuffs:

- Mycotoxins: Limits apply to black pepper. The maximum level of aflatoxin for black pepper is between 5 μg/kg for aflatoxin B1 and 10 μg/kg for total aflatoxin content (B1, B2, G1 and G2). For ochratoxin A, there is a maximum level of 15 μg/kg in place. Between 2020 and 2025, 3 aflatoxin-related cases were reported in RASFF for black pepper. One of these happened in 2025 (ginger from China).

- Polycyclic aromatic hydrocarbons (PAH): PAH can increase the risk of cancer. Because of this, the EU has set PAH limits for spices like black pepper: 10μg/kg for benzo(a)pyrene and 50μg/kg for the sum of all PAHs. Between 2020 and 2025, 6 issues with PAH were reported in RASFF.

- Metal contaminants: Since 2021, the EU has lead residue limits for spices. For black pepper (as a fruit spice) this limit is 0.6 mg/kg.

EU Regulation (EC) No 2073/2005 on microbiological criteria for foodstuffs does not set specific limits for any spices and herbs. The most common type of microbiological contaminant is salmonella. It must be completely absent from pepper.

In 2022, 45 out of the 47 black pepper issues reported in the RASFF database related to salmonella. 45 of the shipments with reported issues came from Brazil. Since then, the number of reported salmonella issues for Brazilian black pepper has dropped a lot: from 45 in 2022, to 18 in 2023, to 3 in 2024, and 1 in 2025. Although promising, this was largely due to less Brazilian black pepper being exported to Germany, which has always been the main country that has reported these issues in RASFF.

Tips:

- Check the national legislation in your target countries through the My Trade Assistant tool at EUAccess2markets to see if country-specific legislation for black pepper is in place.

- Comply with the Codex Alimentarius Code of Hygienic Practice for Low Moisture Food (CXC 75-215) and the International Organization of Spice Trade Associations’ General Guideline for Good Agricultural Practices on Spices and Culinary Herbs to prevent microbiological contamination. The latter is available through national and international spice associations. The American Spice Trade Association also offers a Good Manufacturing Practices (GMP) Guide for Spices.

- Apply proper drying techniques (below 12% moisture), and store and transport in a low-humidity atmosphere to decrease the risk of mycotoxin contamination.

- Consider heat sterilisation as a natural, chemical- and radiation-free option. Since heat sterilisation equipment is rather expensive, it might be interesting to use a third party.

- For the control of contaminants in black pepper, only use the services of laboratories that are ISO/IEC 17025 accredited.

Pesticide residues

EU Regulation (EC) No 396/2005 sets maximum residue levels (MRLs) for pesticides in or on food products. Products containing more pesticide residues than allowed are withdrawn from the European market. In 2025, 2 of the 6 issues reported in RASFF for black pepper were related to pesticides. A shipment from Madagascar was rejected for excessive levels of Anthraquinone and Chlorpyrifos (which is banned in the EU). A shipment of organic black pepper from Sri Lanka was rejected for excessive levels of Anthraquinone.

Tip:

- Select your product or the pesticide you use in the EU pesticide database for a list of relevant MRLs.

Labelling requirements

Packaging for black pepper must protect the flavour, colour, and other quality characteristics of the product. The content of the packaging must correspond to the indicated quantity on the label.

Every export package should declare:

- Name of product, such as ‘black pepper’;

- Batch code;

- Net weight in metric system;

- Shelf life of the product or best-before date, and recommended storage conditions;

- Lot identification number;

- Country of origin and name and address of the manufacturer, packer, distributor or importer.

The lot identification and the name and address of the manufacturer, packer, distributor or importer may be replaced by an identification mark. Labels can also include details such as brand, drying method and harvest date. These batch details can also be included in the product data sheet, which contains the specific characteristics of your product.

For consumer packaging, product labelling must comply with Regulation (EU) No 1169/2011 on the provision of food information to consumers. This regulation includes requirements for nutrition, origin and allergen labelling, and a minimum font size for mandatory information.

Tips:

- Find out how to label your product in Food and Drink Industry Ireland’s practical guide to food labelling.

- For an idea of what a product data sheet can look like, look at this example for organic black pepper.

What additional requirements do buyers often have?

European buyers often have additional demands, beyond legal obligations. These usually involve meeting the European Spice Association’s (ESA) minimum quality levels for spices. Others relate to food safety and to sustainable and ethical business practices.

Quality requirements for black pepper

Quality is a major issue for European buyers. Several factors determine the quality of pepper, some as subjective as flavour. Other quality criteria relate to the pepper cultivar, such as the size of the fruit or pungency. However, the same cultivars can have different qualities, even when produced in the same country. This is because agricultural practices, climatic conditions during the production season and post-harvest operations also have an effect on quality.

European traders and processors commonly use at least one of these sets of criteria:

- ESA minimum quality levels;

- American Spice Trade Association (ASTA) Cleanliness Specifications;

- Codex Alimentarius Standard CXS 326-2017 for Black, White and Green Peppers;

- ISO specifications for black pepper; or

- International Pepper Community (IPC) standard specifications for black, white and green pepper.

Black pepper can be classified into 3 quality categories according to several physical and chemical parameters. Generally, good pepper should have a bulk density of 500–600g per litre. Low bulk density shows that there are more immature berries without kernel (‘light berries’) and undeveloped berries (‘pinheads’).

The most common criteria for black pepper quality include:

- Cleanliness or purity: Pepper must be free from diseases, foreign matter and odours, and any other issues. ESA sets the maximum presence of external matter at 10 g/kg. ASTA also uses criteria such as the presence of dead insects, excreta, foreign matter and peppercorns damaged by mould or insects. For first-class black pepper, the Codex Standard also states that light berries can be ≤2% of the total sample weight and pinheads can be ≤1%.

- Size of peppercorns: Whole pepper is sorted by size, which affects the price. Indian producers use the most detailed sizing classification. ‘Tellicherry’ refers to large pepper berries from Kerala of ≥4.25 mm. The most expensive category is Tellicherry Garbled Special Extra Bold (TGSEB), with berries of ≥4.75 mm. TGSEB pepper must be clean and dried so they have low moisture content (often 7–10%).

- Piperine content: Piperine is the main pungent component in pepper. According to the Codex Standard, the piperine content must be ≥2% for whole black pepper and ≥3.5% for ground black pepper. The minimum piperine content for the first class is set at 3.5%, while this is 4% in the IPC standard. However, buyers may require an even higher content, like 5%.

- Ash content: Ash refers to the inorganic residue remaining after burning the organic matter in a pepper sample. The Codex and IPC Standards use maximum ash content in their quality grades. ESA sets the maximum total ash content for black pepper at 7%, and the acid-insoluble ash limit at 1.5%.

- Moisture content: ESA sets the maximum moisture content for black pepper at 12%. Still, buyers may request a lower moisture content of 7–11%.

- Mesh or particle size: When black pepper is exported in its powdered form, it is ground to pass through a sieve of a specific diameter. Sieves are often specified in micron sizes. 95–99.5% of the ground pepper should pass through the specified sieve size.

- Volatile (essential) oils: Essential oil content is important for the sensorial characteristics of black pepper. The quality is higher when the percentage of ash is low and the essential oil content is high. The ISO specifications for black pepper give a minimum essential oil content of 2ml/100g.

Packaging requirements

Black pepper is mostly exported in bulk in sealed polyethylene bags that can be placed in paper bags or cardboard boxes. The size of the bulk packaging varies depending on the buyer’s requirements, but it is often 25kg. The dimensions should conform to conventional pallet sizes (800mm x 1,200mm and 1,000mm x 1,200mm). Please note that, in some European countries, labour health and safety legislation mean workers can lift a maximum of 20kg. So smaller weights of packaging, such as 10-20kg, are being used more and more often.

The net weight of retail packaging is usually 20–40g. Retail packaging includes glass containers, plastic or paper bags, and plastic containers. Transparent glass containers are particularly popular, as they allow consumers to inspect the pepper visually before buying. Single-use grinders are also common.

Figure 2: Single-use black pepper grinders in a Dutch supermarket

Source: GloballyCool (June 2023)

Food safety certification

Food safety is very important in the European market. Although legislation deals with a lot of potential risks, it is not enough alone. For this reason, some black pepper buyers ask their suppliers to use advanced food safety systems recognised by the Global Food Safety Initiative. One example is Food Safety System Certification (FSSC 22000) – the most widely accepted certification programme. Another is to have a certificate from an approved certification body.

However, putting these systems in place and getting certified costs a lot of money. It is usually only suitable for medium-sized and large processors that want to supply big supermarket chains in Europe. For them, certification shows a high level of professionalism. Smaller buyers often have less strict food safety certification demands.

Sustainability compliance

Although less important than product and food safety requirements, European buyers demand social and environmental compliance more and more. This often means that suppliers must undersign their buyer’s code of conduct. Buyers can also ask for certification against a third-party scheme, like Rainforest Alliance, or a social audit like SMETA.

Codes of conduct vary from company to company, but they are often similar in structure and the issues they cover. In 2022, ESA published a guideline for their members that requires them to monitor their own and their suppliers’ operations on different social and environmental criteria. Since many European spices and herbs companies are ESA members, you will likely come across this guideline sooner or later.

Tips:

- Comply with the most commonly used quality criteria for black pepper.

- Check out ESA’s Quality Minima Document for all details on quality parameters.

- Always ask your buyer for their specific packaging requirements.

- Read more about payment and delivery terms in our tips for organising your spices and herbs exports to Europe.

- Read our tips on how to become more socially responsible and tips to go green in the spices and herbs sector for trends and developments in social and environmental compliance.

What are the requirements for niche markets?

Black pepper niche markets have their own, specific requirements. While Fairtrade lays down requirements for sustainability in the social, environmental and ethical domains, product certification for the organic market mainly focuses on environmental requirements.

Organic certification

If you want to sell your black pepper as organic in Europe, it must be grown using organic production methods that comply with EU organic legislation. Growing and processing facilities must be audited by an accredited certifier. If you become certified, you can put the EU organic logo on your products. Your label must include the name/code of the inspection body and certification number. Regulation (EU) 1235/2008 also lists requirements for imports of organic products from third countries.

Fairtrade

The fairtrade market is built on fairtrade certification. Each player in the supply chain needs to be certified to participate in this market, which is privately regulated.

Fairtrade International has a specific standard for herbs, herbal teas and spices from small-scale producer organisations. For black pepper in general, the Fairtrade premium is set at 15% of the commercial price. For organic black pepper from India and Sri Lanka, the Fairtrade minimum price is set at €1.13 p/kg, with a Fairtrade premium of €0.08.

As of February 2026, there are 43 Fairtrade-certified black pepper producers in Sri Lanka (of which 28 also have a trade function), 20 in India, 1 in Thailand, 3 in Vietnam, and 1 each in Madagascar and Thailand. There are a lot more Fairtrade-certified producers in Sri Lanka and India than in 2023.

Dual certification

Dual certification is a clear asset in both the European fairtrade and organic market. Consumers in these markets are typically more aware than mainstream consumers. As a result, they are more likely to appreciate and buy products with both logos. An example of a black pepper producer with both organic and Fairtrade certification is Ceylbee International from Sri Lanka.

Figure 3: Consumer package of black peppercorns with dual certification

Source: GloballyCool (June 2023)

Tips:

- Read our study on requirements for exporting spices and herbs to the European market for a full overview of requirements, including organic and fairtrade certification.

- Check the guidelines for trade in organics into the EU to familiarise yourself with the requirements for exporting organic spices and herbs into the EU.

- Check Fairtrade International’s standard for herbs, herbal teas and spices and other Fairtrade standards relevant to your production, processing and trade.

- Try to combine organic certification with other sustainable initiatives like fairtrade (dual certification) to increase your competitiveness.

- Consult ITC Standards Map for a full overview of relevant certification schemes and their requirements.

2. Through which channels can you get black pepper on the European market?

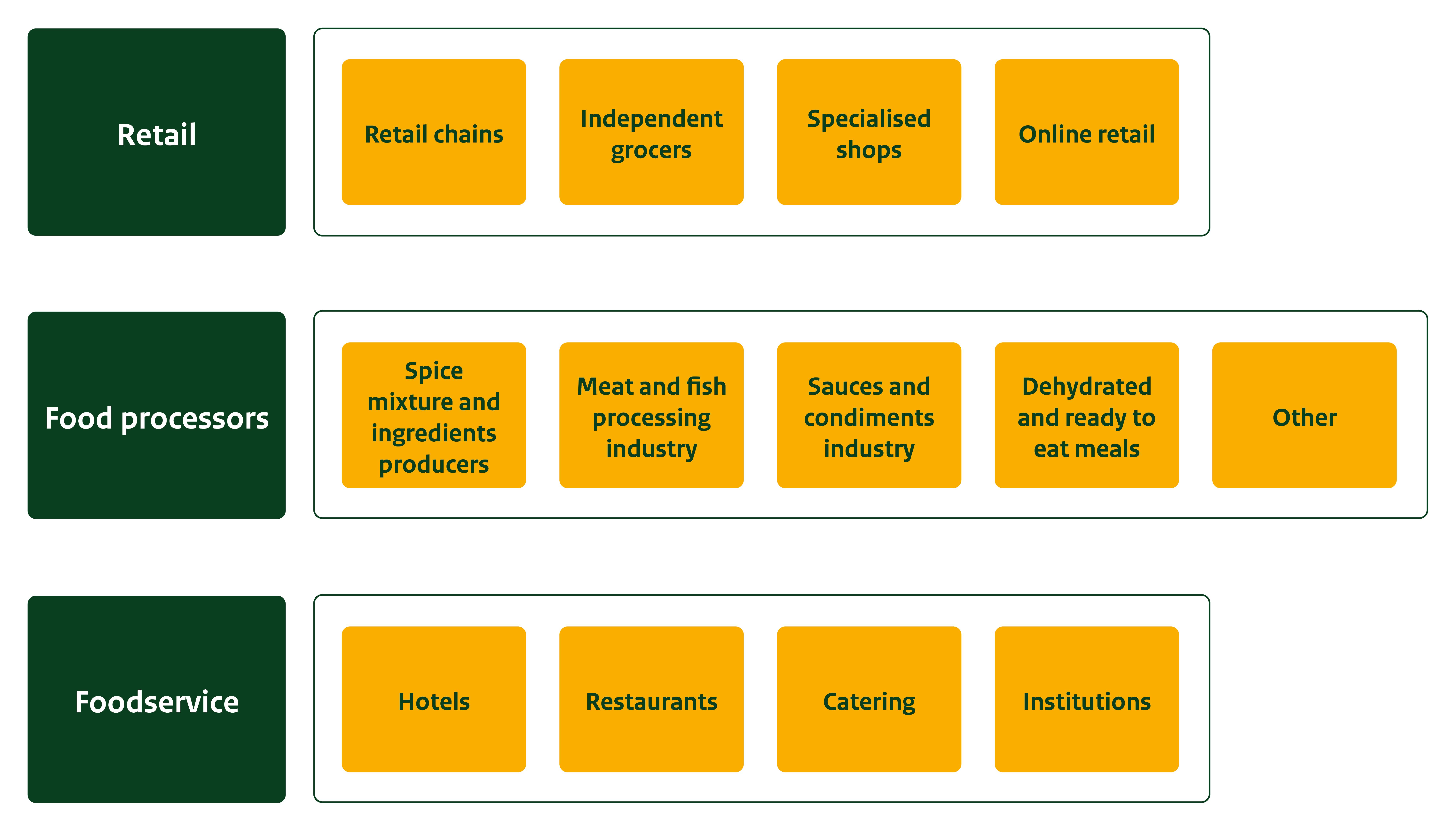

The European food industry uses large amounts of black pepper in a wide variety of products, such as meat, fish and vegetable products, spice mixtures, sauces, soups and ready meals. This pepper usually reaches the European market through specialised spice importers. The largest market segment is the food processing industry.

How is the end-market segmented?

The largest user of black pepper in Europe is the food processing industry, followed by retail and foodservice. Most pepper is imported whole and is sterilised and crushed after import.

Figure 4: End-market segments for pepper in Europe

Source: GloballyCool (March 2026)

Food processing

Food processing is the largest market segment for pepper in Europe:

- Spice mixture and ingredient producers specialise in the production of spices and seasonings for different applications. They constantly invest in research to develop custom formulations for food processing companies and help launch new flavours. These companies produce either dried or liquid spice ingredients. Examples are AVO, Kerry, IFF, Faravelli Group, Food Ingredients Group, Kalsec and EHL Ingredients.

- The meat and fish processing industry is an important user of black pepper, often not supplied directly but through spice and food ingredient companies. Larger groups of companies may import black pepper directly, like OSI. Black pepper is used in throughout the industry, for example, in the production of sausages and other meat specialities. However, meat processors more commonly use customised mixtures with pepper as an ingredient.

- The sauces and condiments industry is dominated by international brands such as Kraft Heinz, McCormick, Nestle’s Maggi and Unilever brands (e.g. Knorr, Calve, Colman’s and Conimex).

- Other industries include a wide variety of ready meals and other products. One example is the vegan meal industry, which is developing quickly in Europe. The Vegetarian Butcher (taken over by plant-based foods market leader Unilever) is one of the companies that has developed this market.

Retail

Another important segment is retail. European (often national) brands and private labels share the retail and food-service segments. Fuchs Gruppe and McCormick are the global and European market leaders, with several brands. Leading brands in Europe include Fuchs (Germany), Ostmann (Germany), Schwartz (United Kingdom), Ducros (France, Belgium), Euroma (Netherlands), Verstegen (Netherlands), Cannamela (Italy), Santa Maria and Prymat (Poland).

The retail sector can be further segmented into several subcategories:

- Retail chains that have the largest market shares in Europe are Schwartz Gruppe (Lidl and Kaufland), Carrefour, Tesco, Aldi, Edeka, Leclerc, Metro Group, Rewe Group, Auchan, Intermarché and Ahold Delhaize (Delhaize and Albert Heijn). The increasing market share of private labels is the main development for these chains.

- Specialised spice shops offer a wide range of spices from different origins, usually in the high-end market segment. They commonly sell spices by weight but also have their own branded products. Examples include Jacob Hooy (the Netherlands), Épices Rœllinger (France) and Spice Mountain (UK). Some have grown into specialised chains like Schuhbecks, named after a German celebrity chef.

- Specialised organic and health food shops are specifically relevant for suppliers of organic certified pepper. Many are part of specialised organic food retail chains, especially in Germany, such as Biomarkt and Alnatura. Organic pepper is also sold in specialised health and wellness shops like Holland & Barrett, next to supplements, herbal teas and other health products. Some organic retailers import directly.

- Specialised fairtrade and ethical shops are a niche segment which provides opportunities for certified suppliers. Sales of fairtrade-certified products are strong in the UK and Scandinavia. Examples include Hecosfair (France) and RISC World Shop and Global Refills (UK).

- Online retail is currently dominated by the leading retail chains. Specialised online food retailers (that do not have physical outlets) include Ocado (UK) and JustIngredients.

Food service

Specialised distributors supply the food service channel, which includes hotels, restaurants, catering and other institutions that prepare and serve food for customers. These distributors can import pepper directly, but they often buy from wholesale bulk importers. The food service segment often requires specific packaging, like 300g to 1kg packs, which is different from bulk or retail packaging. Examples of distributors supplying the food service segment with black pepper include METRO and Brakes.

Tips:

- Study the exhibitor lists of large trade fairs like Anuga, SIAL Paris and Alimentaria to find potential buyers.

- If you intend to supply to private labels for retail, search for opportunities at PLMA.

- To find potential buyers in the food ingredient segment, search the list of exhibitors at the specialised trade fair Fi Europe.

- For opportunities in the food service segment, visit Sirha and Internorga.

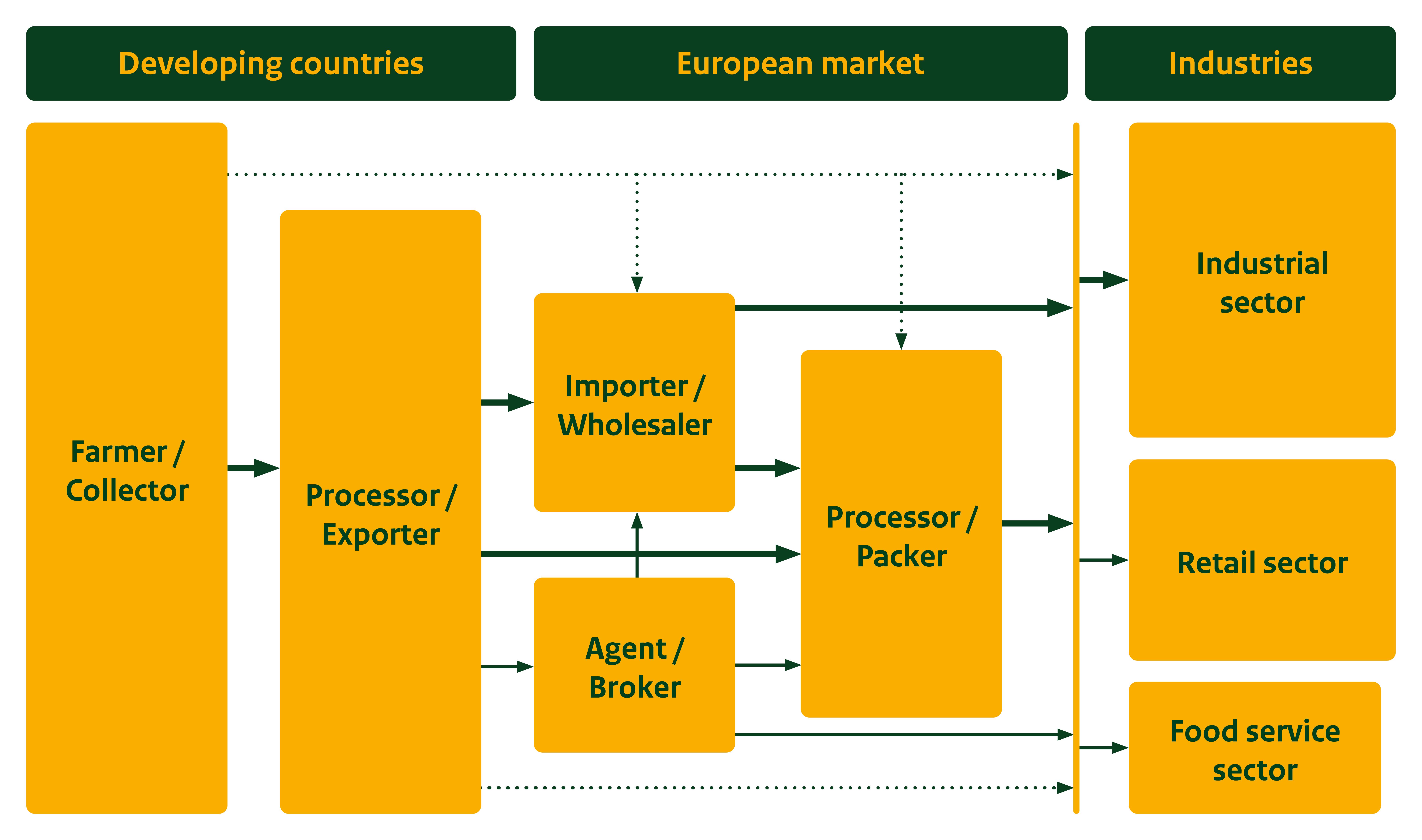

Through which channels does a product end up on the end-market?

Specialised spice importers are the most important channel for black pepper in Europe. Many established wholesalers also have packing facilities and usually supply private-label pepper brands. Some leading importers have a permanent presence in pepper-producing countries, through either their own sourcing offices or their own production facilities. Sometimes, black pepper is placed on the market through agents or directly supplied to food processors or service companies.

Figure 5: Trade channels for black pepper in Europe

Source: GloballyCool (March 2026)

Importers/Wholesalers

Importers and wholesalers can be general spice importers or further specialised in specific roles. Some deal exclusively with ingredients for the processing industry, while others pack pepper for retail chains. Some importers also deal with a broader range of products apart from spices, such as beans and seeds.

The position of importers and food manufacturers is under pressure from retailers. Higher requirements from the retail industry determine the dynamics throughout the supply chain. This pressure translates into lower prices, but also into added-value aspects such as ‘sustainable’, ‘natural’, ‘organic’ or ‘fair trade’ products. Transparency in the supply chain is needed. To achieve this, many importers develop their own codes of conduct and build long-lasting relationships with preferred suppliers from developing countries.

Agents/brokers

Agents and brokers are intermediaries who bring buyers and sellers together. They charge a commission for their services. Their role in the black pepper trade is limited, but they are interesting if you have a specialised product (e.g. high quality or sustainable) for which buyers are harder to find. The role of the agent is slowly changing due to the increased transparency and other legal and customer requirements.

Examples in this category are Van der Does and AVS Spice Brokers. Both are located in the Netherlands, close to Rotterdam, one of Europe’s main ports in the international spices and herbs trade.

Tip:

- Search ESA’s member list to find buyers from different channels and segments.

What is the most interesting channel for you?

Specialised importers are the best contacts for placing black pepper on the European market. This is especially relevant for new suppliers, as supplying the retail segment directly is very demanding and requires a lot of quality and logistical investments.

Packing for private labels can be a good option for well-equipped and price-competitive producers. Still, private-label packing is often done through importers that have contracts with retail chains in Europe. As labour costs in Europe are increasing, black pepper importers sometimes search for opportunities to pack brands in developing countries if they can assure full traceability and quality control.

3. What competition do you face on the European black pepper market?

Vietnam, Brazil, Indonesia and India are the 4 main competitors for pepper-supplying countries to Europe. They account for more than 90% of the market. Although Vietnam is Europe’s leading black pepper supplier, these exports are not always of Vietnamese origin. This is because Vietnam imports, processes, mixes and re-exports pepper from several other producing countries too.

Which countries are you competing with?

Source: UN Comtrade (August 2025)

Vietnam: Europe’s leading supplier but production is declining

Vietnam dominates the global production and supply of pepper. The country is home to about 200 pepper processing and trading companies. Of these, 15 leading companies make up about 70% of the export volume. Production mainly takes place in the highlands. Around half of Vietnam’s pepper output comes from the Dak Nong and Dak Lak provinces, followed by Ba Ria-Vung Tau, Dong Nai and Gia Lai. Most of this pepper is harvested between January and April.

But production is declining and stocks are decreasing. Vietnamese pepper production reached an all-time high of 322,000 tonnes in 2018/2019. This oversupply led to very low prices. Since then, production has dropped to around 153,000 tonnes in 2025/2026. Although the plants’ average yield is relatively stable,the amount of land used for pepper has dropped. This is because farmers have switched to more profitable crops like durian and coffee.

To maintain export capacity and a stable supply for the country’s large production and cleaning facilities, Vietnamese processors import pepper from countries like Brazil, Cambodia and Indonesia. This means black pepper exports from Vietnam are often a blend of different origins.

This means that Vietnam’s pepper exports to Europe grew from 45,000 tonnes in 2020 to 58,000 tonnes in 2024, at a compound annual growth rate (CAGR) of 6.8%. About 74% of this was whole peppercorns. The main European destination for Vietnamese pepper is Germany. It made up a share of 28% of exports in 2024, followed by the UK, France, Poland and the Netherlands (10–12% each).

Vietnam saw a large increase in whole organic pepper exports to Germany. It went up from 63 tonnes in 2020 to 161 tonnes in 2021. In 2022, it supplied France with 50 tonnes of whole pepper. By 2023 and 2024, the focus shifted to ground pepper, where exports to Germany grew from 295 tonnes to 390 tonnes. Vietnam also exported 206 tonnes of ground pepper to France in 2023.

Brazil: Decreased supplies

Brazil is a major player in the global pepper trade. Most of its pepper comes from the states of Espírito Santo and Pará, followed by Bahia. Production reached a peak of 110,000 tonnes in 2021/2022. It dropped to 89,000 tonnes in 2024/2025. Many Brazilian farmers have expanded their cultivation areas, but yields dropped when drought and heatwaves in regions like Pará led to crop failures. If there are favourable weather conditions, production can increase.

This means that Brazil’s pepper exports to Europe dropped from 22,000 tonnes in 2020 to 13,000 tonnes in 2024, at a CAGR of -13%. Whole peppercorns made up 73–96% of this number. The main European export market for Brazilian pepper is Germany (43% in 2024), thanks to the strong presence of the German Fuchs Gruppe in Brazil. But these exports dropped from 14,000 tonnes to 5,400 tonnes due to reported salmonella issues. Still, a growing volume of Brazilian pepper is coming to Europe via Brazil’s supplies to Vietnamese facilities.

Brazil’s organic pepper exports to Germany peaked at 113 tonnes in 2021 before falling to 74 tonnes in 2022. The country then moved towards processed products. Its ground pepper exports to Germany doubled from 32 tonnes in 2023 to 64 tonnes in 2024.

In addition to black pepper, Brazil is famous as the leading world supplier of pink peppercorns (Schinus terebinthifolia). These are very popular in multicolour pepper mixes in Europe and worldwide.

Indonesia: White pepper leader

Indonesia is famous for its production of white pepper, covering around 50% of the global white pepper market. Around a third of all pepper in Indonesia is produced as white. Most of Indonesia’s pepper output comes from Lampung and Bangka, followed by Kalimantan. Planted areas have decreased a lot, especially in Bangka, and yields vary.

Indonesia’s pepper exports to Europe varied around 5,600 tonnes between 2020 and 2024. Whole peppercorns made up 68–90% of these exports. The main European export market for Indonesian pepper is Germany, which had a share of 28% in 2024. This was followed by France (23%), the Netherlands (18%) and the UK (16%).

Indonesia’s main market for organic pepper is Germany. It exported 85 tonnes of whole pepper in 2020. This increased to 173 tonnes in 2021 but then dropped to 79 tonnes in 2022. In 2023, organic ground pepper exports took off to reach 40 tonnes in 2023 and 76 tonnes in 2024.

India: Balancing between imports and exports

As domestic consumption is very high, India imports more pepper than it exports. Most of the pepper production takes place in Karnataka and Kerala, followed by Tamil Nadu. Production of pepper in India fluctuates, but is commonly around 60,000 tonnes. But unpredictable rainfall is impacting the output.

India’s pepper exports to Europe varied around 6,000 tonnes between 2020 and 2024. About 70% of these exports were whole peppercorns. The main European export markets for Indian pepper are the UK (19% in 2024), Germany (18%) and Sweden (16%).

India’s organic pepper export remained relatively low until 2023, with volumes of below 40 tonnes whole pepper per year sent to Sweden and France. But in 2024, India showed strong growth in ground pepper, with exports to the Netherlands and France reaching 62 tonnes and 66 tonnes, respectively.

Which companies are you competing with?

To get an idea of the types of companies you are competing with, below are a few profiles of several types of companies.

ofi, Vietnam

ofi (formerly Olam Food Ingredients) is the world’s largest fully integrated black pepper supplier. It owns a pepper estate in Vietnam’s rural Chu Puh District. The company processes pepper through its own facilities to meet global quality and traceability standards. ofi controls supply from the field through to processing. It also uses advanced agricultural methods, such as drip irrigation, cover crops, composting and digital crop monitoring, to ensure consistent quality and supply. Its processing uses inline steam sterilisation to maintain purity and food safety.

The company works closely with farmers to support better agricultural practices and traceability. ofi’s approach to sustainability covers training on pest management, organic methods and regenerative agriculture to help farmers improve yields and reduce environmental impact. The pepper from the Chu Puh plantation can be traced back to specific planting blocks. This gives buyers more insight into origins.

ofi has just launched its Spice Maps Sustainability Strategy, including tailored 2030 goals for black pepper. In Vietnam, it focuses on “climate-smart practices to protect farmers from market and climate shocks.” The company started a project with Rainforest Alliance in 2019. It helps 470 pepper farmers to achieve certification for sustainable, responsible and economically viable farming. This includes training, soil analysis, customised improvement guidance, protective equipment, packaging and a higher price for certified pepper.

Video 1: Women at Olam’s Chu Puh black pepper plantation

Source: Olam Group

Social sustainability is also part of ofi’s work in Vietnam. The Spice Maps black pepper goals include access to essential health and education services for farming families. ofi’s Chu Puh plantation provides employment opportunities for local minority women, offering steady income and training in good agricultural practices and environmental care. The company runs programmes that improve farmer support, diversify income and connect growers to better market opportunities. Its integrated focus on quality, sustainability and traceability helps ofi supply stable, premium pepper to demanding markets like Europe.

Sacconi, Brazil

Sacconi is a black and white pepper producer and exporter based in São Mateus, Espírito Santo, a major pepper‑growing region in Brazil. The company focuses on delivering quality dried and ground pepper for global food and seasoning markets. Its products are sold in over 28 countries.

Video 2: Sacconi’s quality and sustainability practices

Source: Janete de Souza

One of Sacconi’s strengths is its attention to post‑harvest quality and handling. It uses mechanised threshing, dedicated dryers and hanging drying platforms that keep pepper free from ground contact. This helps to maintain cleanliness before packing. The company also manages its own storage facilities and transport fleet for reliable deliveries. Sacconi is family-run and guided by core values of ethics, trust, transparency and continuous improvement.

In terms of environmental and social sustainability, Sacconi uses practical resource‑saving measures at its processing site. It reuses pepper residues on plantations, fuels dryers with macadamia husks and recirculates process water for irrigation. This shows how waste can be reduced and reused in pepper production. These measures show a focus on sustainable growth that many European buyers value, even though Sacconi does not promote formal sustainability certification at the moment.

Harris Spice, international

Harris Spice is a global spice company based in the United States that works with spice growers around the world. Between 2020 and 2025, its Organic Pepper Project supported farming communities in Lampung. In partnership with GIZ and local cooperatives and organisations, the company has helped more than 1,000 pepper farmers adopt organic and regenerative farming methods. This included training in soil health, natural pest control and intercropping. The aim is to improve quality and yields and help protect the environment.

The project has helped farmers move towards certifications such as EU organic and Rainforest Alliance. Many are now working on gaining certification. Harris Spice has also helped set up 33 farmer cooperatives to improve harvest collection, quality management and collective sales. It has trained farmers in financial literacy and digital banking to manage transparent transactions and strengthen their long-term financial independence. The project’s results include healthier crops, higher yields, stronger incomes, healthier ecosystems and more access to global buyers.

Jayanti, India

Jayanti is a long‑established Indian spice company. It is present in more than 50 countries. The company has sourcing and processing operations in India, Turkey and Vietnam. It supplies spices like black pepper to markets in Western Europe, North America and Asia. Jayanti works closely with its farms, agronomy teams and in‑house laboratories to manage food safety and quality throughout the supply chain. Its state‑of‑the‑art BRCGS‑certified processing plants can clean, grind, blend, steam‑treat and package spices.

Video 3: Jayanti’s farm-to-fork quality management

Source: Jayanti Herbs Spices

The company also believes sustainability and responsible sourcing are very important. It helps farmers earn more money and improve their practices by working directly with them from cultivation to export. Jayanti’s community-building initiatives invest in education, medical outreach and access to water. Its direct‑farm sourcing programme includes training and capacity‑building. In this way, it supports farming communities with fair pricing, improved market access and long‑term partnerships. This direct approach also ensures traceability, quality and transparency. Jayanti is a member of the Sustainable Spice Initiative (SSI) and has EU organic certification.

Tips:

- Check the member list of the Vietnam Pepper Association to learn more about Vietnamese suppliers.

- Visit European trade fairs like Anuga and SIAL Paris to meet your competitors.

Which products are you competing with?

There are no substitute products for pepper. Due to widespread pepper availability, the food industry, culinary experts and retailers are not searching for any kind of substitute.

4. What are the prices of black pepper?

Export prices depend on origin and quality. Usually, the highest prices are paid for Malaysian pepper, followed by Indian, Indonesian and Vietnamese pepper. The lowest prices are paid for Brazilian pepper. Export prices also vary depending on the production volumes in the main producing countries (Vietnam, Brazil and Indonesia).

Black pepper export prices reached a peak of nearly $10/kg (USD) in 2015. They decreased to about $2/kg in 2020. After pepper prices shot up by 69% in 2024, they stabilised at about USD6.6/kg in 2025.

Pepper is mainly sold as an ingredient for the foodservice and food processing industries. In these segments, analysis of prices is hard. But retail (shelf) prices provide useful insights. Retail prices in European supermarkets vary per brand, type and packaging of black pepper. Prices of packs of glass containers are higher than packs of plastic containers and bags. Prices of pepper in small packages can vary from €12–140/kg. The price of ground pepper is higher than that of whole peppercorns.

The price breakdown below is a very rough indication and only demonstrates the margins throughout the retail segment, which is only part of the market. Supply to the industry and foodservice segments has a different structure and the final price is lower because it does not include retail margins. Many factors contribute to the price, like quality, variety, origin, sterilisation costs, food safety certification costs, taxes, sales and network margins.

Source: GloballyCool (March 2026)

Tips:

- Subscribe to a price monitoring service such as those provided by Expana or the International Pepper Community.

- Check prices of retail packages of pepper online, for example of the Dutch retailer Albert Heijn.

GloballyCool carried out this study on behalf of CBI.

Please review our market information disclaimer.

Search

Enter search terms to find market research

Do you have questions about this research?

Risk diversification in black pepper sourcing is no longer optional. Alongside established suppliers, buyers are exploring new origins like Madagascar to strengthen supply security.

Harold Leurink, manager sales at Spice United.

Webinar recording

25 October 2021